WELL - Why I Stopped Buying Treasuries To Buy REITs Instead

2023-05-20 09:00:00 ET

Summary

- Treasuries now offer a 5.5% yield.

- Many investors are turning to Treasuries for safety.

- I think that this is a mistake. I am buying REITs instead, and here is why.

Short-term Treasuries (SPTS) are now yielding over 5%.

That's the highest yield they have offered in a very long time:

Real estate investment trusts, or REITs ( VNQ ), on the other hand, are only yielding about 4% on average, and that's despite being a lot riskier investments. Their share prices have dropped by 30%+ over the past year, and many fear that REITs could face even greater losses if and when we go into a recession:

This has led many of you to tell me that they have stopped buying REITs to buy Treasuries instead.

After all, why would you buy REITs when you could get a higher and safer yield by investing in Treasuries?

Here is one of these comments, just to give an idea:

"We can debate all day, but why bother? Sitting in 5% Treasuries laddered out a few years. I doubt many REIT will be able to provide a comparable return, at least through the downturn/recession on the horizon. Buying stocks or non-Treasuries is pickup up dimes in front of an accelerating Steamroller. Pros can possibly, but average reader here? Doubtful."

I completely disagree and I am doing the opposite.

I have stopped buying Treasuries to buy REITs instead. It is funny to me how everyone knows that the time to invest is when stocks are down, but then when a crash actually occurs, very few end up having the courage to take action and you will hear countless reasons why "this time is different."

So why are REITs a better investment opportunity than Treasuries?

I am going to give you two simple reasons.

Reason #1 - Inflation Protection

Yes, with Treasuries, you may earn a 5% yield, but that's a nominal yield.

If inflation is 6%, what's your real yield? It is negative 1%.

Are you really getting ahead with that? No, you are going actually backward.

Moreover, you have no protection against the risk of accelerating inflation.

What if inflation shoots even higher for one reason or another?

You won't get more than 5%, and your purchasing power will be permanently impaired.

So yes, Treasury yields may seem historically high, but they really aren't that high once you account for today's inflation. The real yields are actually very low...

REITs provide much better protection against inflation because when you buy shares of a REIT, you are essentially buying an equity interest in a diversified portfolio of income-producing properties.

This real estate is needed and cannot be inflated away. Most REITs own essential properties that are undersupplied. This includes things like apartment communities, e-commerce warehouses, cell towers, hospitals, etc.

The high inflation is leading to higher property replacement costs, lower supply, and higher rents, and this is why real estate - and by extension REITs - have been a great inflation hedge over the past centuries.

Just look at the latest results of some REITs across various property sectors:

- Apartments: The sunbelt apartment REIT, Camden Property Trust ( CPT ), reported that its same property NOI had risen by 8.1% in the first quarter compared to the same time period last year. The coastal apartment REIT, AvalonBay Communities, Inc. ( AVB ), reported even stronger same-property NOI growth that exceeded 10%, and it also hiked its full-year guidance.

- Healthcare: Alexandria Real Estate Equities, Inc.'s ( ARE ) life science properties experienced the highest rent growth ever on its expiring leases at 24.2% in the first quarter. Welltower Inc.'s ( WELL ) senior housing portfolio also grew its same property NOI by 11% in the first quarter, allowing it to raise its guidance. Even the more speculative names like Medical Properties Trust, Inc. ( MPW ) and Global Medical REIT Inc. ( GMRE ) reported strong same-property NOI growth.

- Retail: Whitestone REIT's ( WSR ) strip centers also saw their rent increases surge to an all-time high, now surpassing 20% on expiring leases. Simon Property Group, Inc. ( SPG ) again hiked its dividend after its same property NOI rose by another 4%. The sales of square feet of its malls have never been greater.

- Industrial: EastGroup Properties, Inc.'s ( EGP ) urban class A industrial properties grew their same property NOI by nearly 8% in the first quarter. Its Class B peer, STAG Industrial, Inc. ( STAG ), on the other hand, grew its same property NOI by about 6% in the first quarter.

This explains why REIT cash flows and dividends have kept on rising even despite the surge in interest rates. Most REITs are conservatively financed with a low ~30% LTV, fixed-rate debt, and long maturities. Therefore, the positive impact of inflation is greater than the negative impact of rising rates - leading to higher profits in many cases.

So, you are not relying just on the "dividend yield" to generate returns when investing in REITs.

Your total return equation has more elements:

There is the yield. Then there is the growth. And finally, there is a third element, which we discuss below:

Reason #2 - Valuation & Upside

A lot of investors will look at the dividend yields of REITs and conclude that they are probably fairly valued.

If the dividend yield is just 4-5%, then that may not seem attractive relative to Treasuries as an example.

But the dividend yield itself says nothing about the valuation of a REIT.

Today, REITs retain more cash flow than ever. To give you an example, Alexandria Real Estate only offers a 4.1% dividend yield, which may not seem cheap, but that's because its payout ratio is low at 54%.

So its real " cash flow yield " is about 7.7%, and that is one of the lowest valuations ever for the company following the crash of its share price:

The REIT has a fortress, investment-grade rated balance sheet with little debt, and it owns Class A life science buildings that are enjoying 20%+ rent hikes as leases expire because their current rents are below market. It also has many new development projects underway and it is able to self-fund these growth projects thanks to all the cash flow that it retains.

Therefore, we believe that the company has the potential to deliver ~6-8% annual growth in the coming years, and if you add that to your dividend yield, you are getting ~10-12% annual total returns.

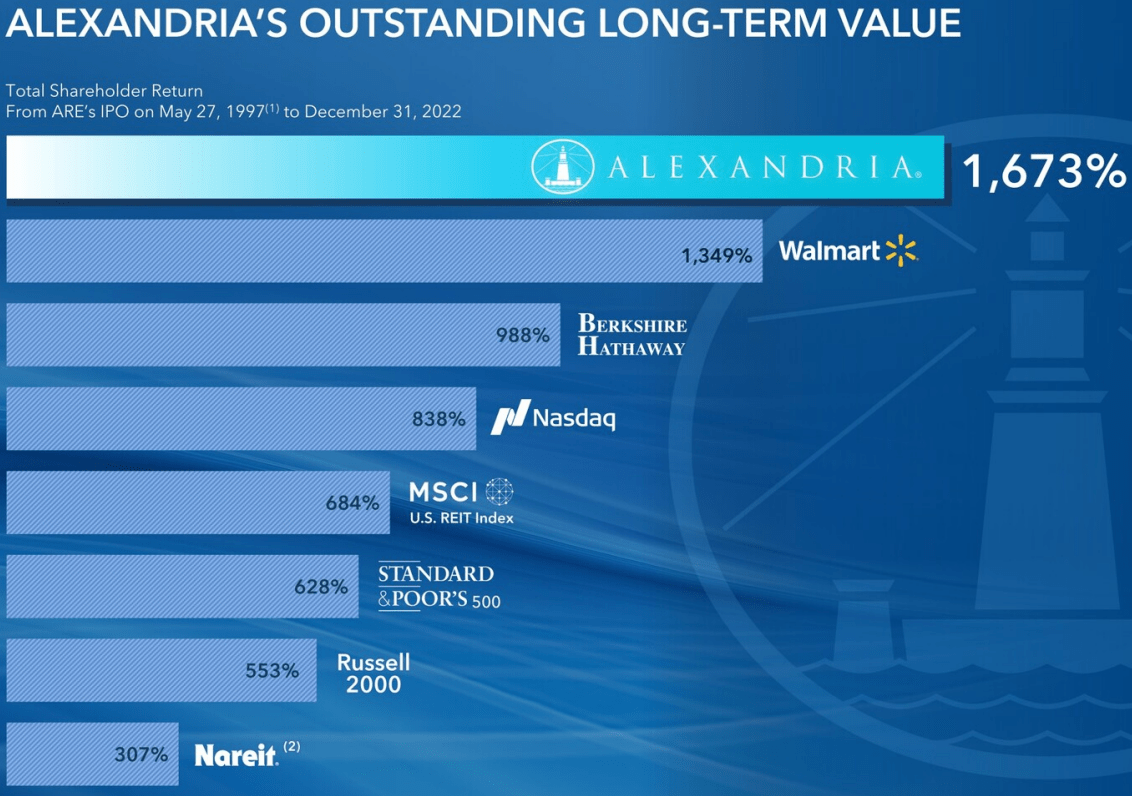

That's already quite a bit more attractive than what Treasuries are offering, and I believe that it is a conservative estimate given that Alexandria has historically generated much higher annual returns than that. It has even beaten the likes of Berkshire Hathaway Inc. ( BRK.B ) and Walmart Inc. ( WMT ):

{kind=link}

And that's not all.

Here we have not yet included the potential upside that we expect once the company's valuation recovers, and that's really going to make up the bulk of our returns.

Today, we estimate that the shares of Alexandria are priced at a 40% discount to the net asset value of their real estate. The company routinely sells assets at valuations that are much greater than what's currently implied by their share price.

Following its crash, the shares are about 50% below their early 2022 levels, and that's despite generating higher cash flow and paying a higher dividend today. Adjusted for that, the valuation is about 60% lower!

To return to its previous peak, the share would need to double from here, and it would price the company at 24x funds from operation ("FFO").

Now, that may be too much in today's higher interest rate environment, but even if it only reached 18x FFO, that would still lead to 40% upside from here and that valuation would still be very reasonable for a company of this quality.

So here is our return calculation:

4.1% dividend yield + 7% growth + 40% upside potential.

Assuming that it takes 3 years for this repricing to occur, we could expect to earn 20+% annual total returns.

Now, you start to understand why buying Treasuries may not make so much sense after all.

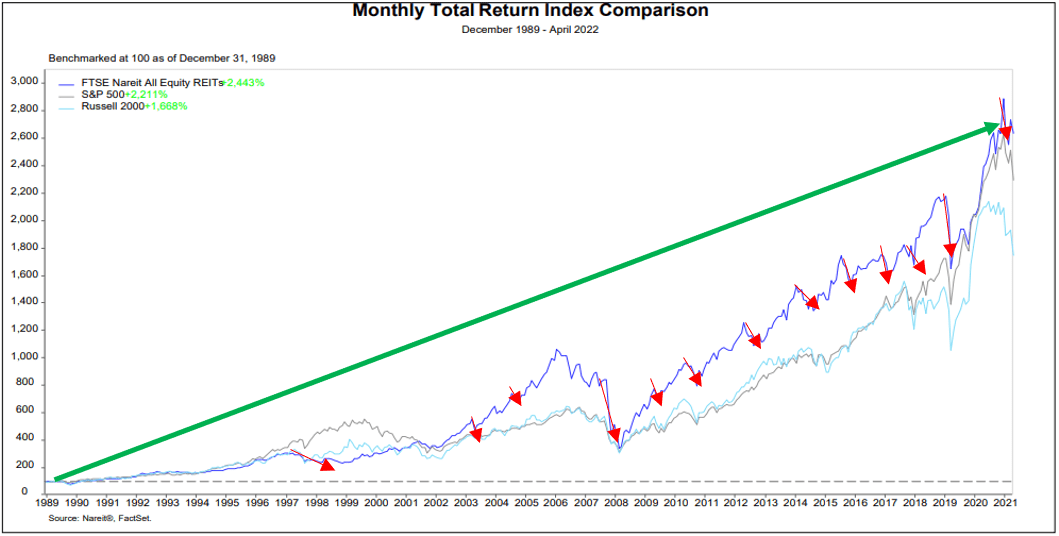

Sure, REITs are volatile, but historically, it has always been a good idea to load up on them after a crash. The market always overreacts, and REITs eventually recover and richly reward those who had the courage to buy them:

{kind=link}

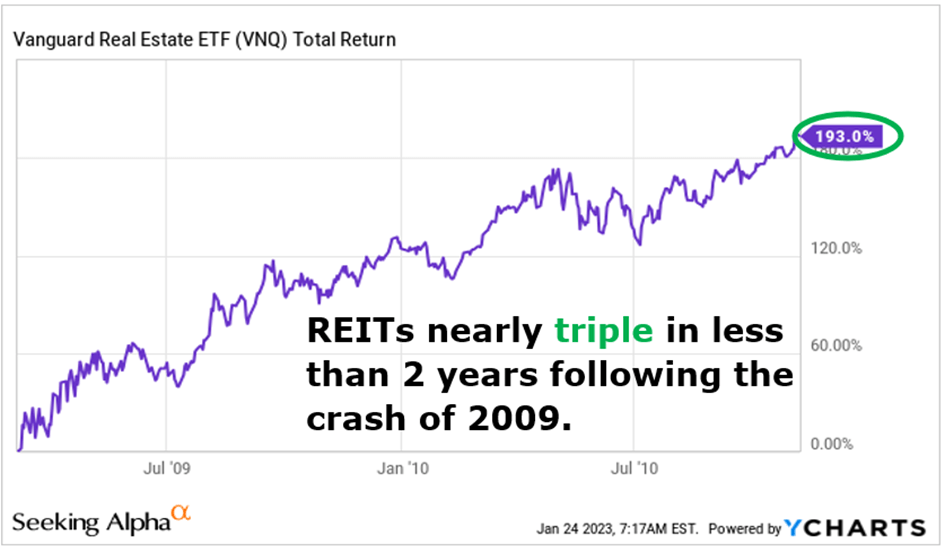

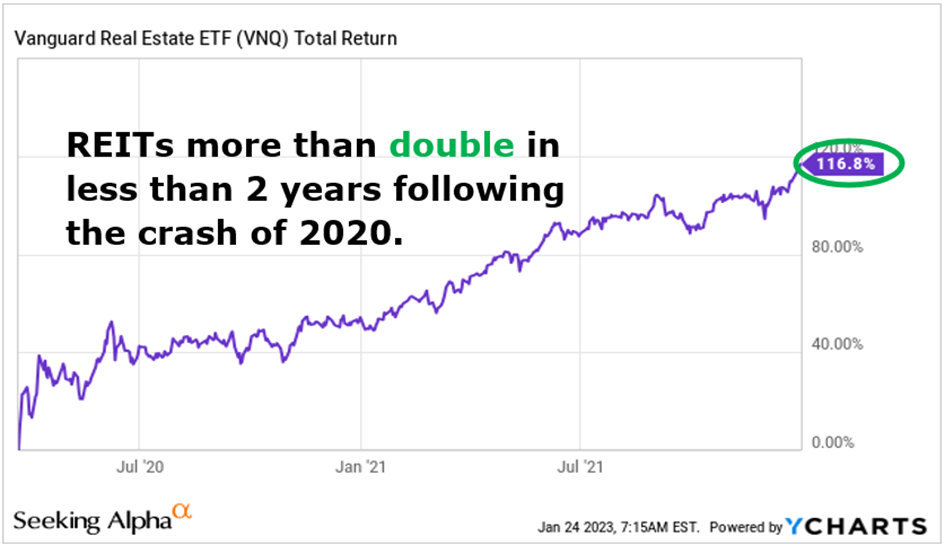

The last times REITs were so cheap were following the great financial crisis and the pandemic.

Here are the results following the great financial crisis:

{kind=link}

And here are the result following the pandemic:

{kind=link}

Today, we are yet again presented with a similar opportunity, but many individual investors are wasting this opportunity by buying Treasuries instead.

Meanwhile, big private equity players like Blackstone Inc. ( BX ) and Starwood Property Trust, Inc. ( STWD ) are loading up on REITs. Here is what Starwood's CEO said the other day about REITs (emphasis added):

"By the way, when credit comes back, you are gonna see REITs take off. REITs are on sale. There are some unbelievable bargains in REITs. We did the same thing during the pandemic. We bought a dozen stocks all over the world and we had a 70% IRR on that stuff. We are already buying some stuff in the public market because I do think that rates are going down."

So in short, this is why I have stopped buying Treasuries to buy REITs instead. They are priced at historically low valuations, offer significant upside potential, and earn high cash flow that's growing while I wait. That's a lot more attractive than earning a negative real return from Treasuries.

For further details see:

Why I Stopped Buying Treasuries To Buy REITs Instead