RCMT - Why I Think RCM Technologies Will Do Well This Earnings Season

2024-01-10 10:55:51 ET

Summary

- RCM Technologies is a $250 million market cap company operating in engineering, specialty healthcare, and life sciences and IT sectors.

- The company's next earnings are expected on March 13, 2024, and it has a history of surprising to the upside.

- Management is optimistic about the upcoming quarter and expects strong growth in 2024, which could lead to a significant beat in earnings.

RCM Technologies (RCMT) is a $250 million market cap company that operates in three segments: Engineering, Specialty Health Care, and Life Sciences and Information Technology. This article is part of a series where I analyze upcoming earnings to see if there's a potential angle to profit from the upcoming short-term event. In the case of RCMT, the next earnings are expected post-market on March 13, 2024, which is relatively late in the earnings season. There will be other companies reporting first that could help to gain an even better understanding. However, I think this is quite an interesting company, and the earnings profile is at least a little bit unusual. The company's share price has been on a tear lately:

I pulled up the Seeking Alpha data on the earnings data vs. the analyst data. The data on this company should be very weak compared to a lot of larger companies because there are only two analysts covering the company.

A limited number of forecasts doesn't tend to be as strong as the average of a number of forecasts. The current forecast is for $0.67 before supposedly coming back down a little bit.

In terms of earnings, the company has risen to the upside 3x in a row. It is almost always surprising to the upside. It is not unusual to surprise to the upside as managements are trying to coax analysts towards numbers they can meet and exceed. Management also tries to meet the expectations by perhaps shuffling earnings around a little bit between quarters.

EPS surprises RCMT (Seekingalpha.com)

{kind=link}

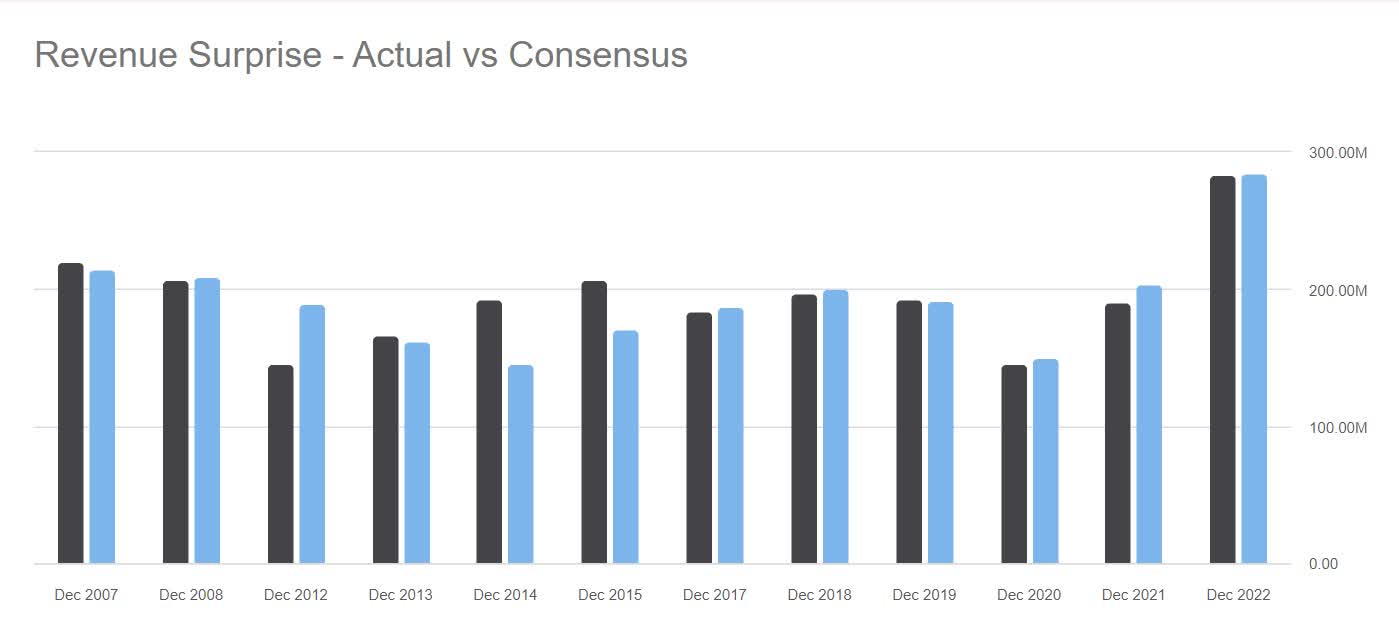

Revenue is a bit harder to shuffle around (less accounting discretion), and I see more misses there. That's the case here as well.

Revenue surprises RCMT (Seekingalpha.com)

{kind=link}

Beating on earnings doesn't always save the day, because the June quarter share price response was pretty bad while the company exceeded EPS forecasts and exceeded revenue expectations slightly. During the September quarter, the company exceeded EPS expectations but missed on revenue, which got the best reception in the last 4 quarters.

| Earnings Period | Earnings Date | Price Before | Price After | Percentage Difference (%) |

|---|---|---|---|---|

| Sep 2023 | ||||

| 2023-11-08 | ||||

| 19.01 | ||||

| 21.80 | ||||

| 14.68% | ||||

| Jun 2023 | ||||

| 2023-08-09 | ||||

| 19.80 | ||||

| 17.37 | ||||

| -12.27% | ||||

| Mar 2023 | ||||

| 2023-05-09 | ||||

| 12.21 | ||||

| 12.83 | ||||

| 5.08% | ||||

| Dec 2022 | ||||

| 2023-03-15 | ||||

| 12.94 | ||||

| 12.98 | ||||

| 0.31% |

Management has made a couple of statements about the upcoming quarter. One example can be found here :

“The cadence of our business continues to accelerate as we move through the year,” Bradley Vizi, executive chairman of RCM Technologies ((RCMT)), said in a statement. “As such, we expect the fourth quarter to be our strongest, and continue to be confident that the long-term outlook for RCM is bright.”

On the most recent earnings call , there is more:

Also of note, the outlook for 2024 and beyond is bright. Our ability to parlay our high-value capabilities into long-term partnerships, where we continue to deliver increased value into strategic accounts has taken hold. We believe our collection of high value capabilities is unique to the marketplace, serving as a key differentiator for which to land and expand.

Management tends to be overly optimistic, but when they sound this confident, in my experience, the ongoing quarter isn't going to be terrible when reported. At least, that's quite unusual. They don't give guidance except this time:

Before turning the call to Kevin, I would like to reiterate the financial expectations provided during the third quarter. We continue to anticipate EBITDA growth during the fourth quarter, a resumption toward our long-term objective, which is also in line with our expectation for 2024.

I also want to reiterate that as a general policy, we do not give guidance. However, we felt a more granular expectation as we close the year would be appropriate given the advanced macroeconomic noise in the marketplace.

And the CFO added to that later in the call:

As for fiscal 2024 adjusted EBITDA, we will be highly disappointed if we don't see at least low double-digit growth. Our internal goals will undoubtedly reflect a much higher percentage. We are optimistic about growing all three segments in fiscal 2024 and beyond.

I take the term "low double-digit growth" as referring to an annual growth rate of 10% to 15%. So far this year, they've done $4.6 million in EBITDA and 2x ~$6 million.

Last year, the annual figure was around $30 million. At a 12.5% EBITDA growth rate, the company should do $33.75 million for the year. That suggests the company would do around $17 million in EBITDA in the final quarter. That's almost as much as during the rest of the year. It's not impossible because the company has an engineering department that can start working on large projects leading to lumpy revenue/profit increases.

EBITDA per share translates quite nicely into EPS per share. The EPS number tends to fall in the 60%-80% range of EBITDA per share lately. Given we're expecting a very good quarter, I would lean towards the conversion being at the higher end of the range.

Something that I do want to call out as an orange flag here is that insiders are predominantly selling, although that's not a recent development.

insider selling RCMT (openinsider.com)

{kind=link}

As mentioned, there are only two Wall Street analysts that cover the name. They have strong buy recommendations on the stock, have been revising their estimates and price targets upwards over time, and the consensus EPS estimate for next quarter is $0.67 with revenue coming in at $72.29 million.

| Aggregate analysts |

| EPS Estimate |

| $0.67 |

| Revenue Estimate |

| $72.29 million |

It seems to make more sense to me if earnings are a lot higher than anticipated. Please keep in mind that this isn't based on deep fundamental knowledge. I'm experimenting with a relatively simple quantitative model (using the above analyst estimates as well) and then adjusting it based on common sense and knowledge of the business. I usually take a longer-term view of businesses, so I'm unsure whether these predictions will be useful. Having said that, here are my predictions:

| Bram de Haas |

| EPS Estimate |

| $1.25 |

| EPS GAAP Estimate |

| $0.66 |

| Revenue Estimate |

| $110 million |

My estimate is a lot higher. That's even though I incorporated the existing analyst estimates into my estimate. The disparity arises because: 1) management EBITDA guidance and the company's historically strong conversion of EBITDA to earnings; 2) The fact that the company fairly consistently beats; 3) I expect analysts to raise estimates as that's what they've been doing in recent history; and 4) Because there are only two analysts, I don't think the number is as solid as it would be with more analysts. Therefore I've taken the liberty to stray from it further than I otherwise might. Possibly to my regret.

What's more important is how the market will react. I think it is better to assess this closer to the date the company will report. A beat isn't necessarily enough for this company. The market expects it is likely the company will beat by a small margin. In this case, I expect the company to beat more spectacularly.

I'd be stunned if my estimates are closer than the analyst estimates but the share price doesn't respond favorably. What helps is that the company trades at around 16x earnings, and that's about 25% below its sector median. Historically, the company has traded at lower multiples, but it is now growing both revenue and earnings, which seems like it is sustainable. Then again, the earnings are still over a month away, and general market sentiment is likely to overshadow the impact of the earnings call over this timeframe. At the end of the day, I expect it is likely that RCM Technologies, Inc. will outperform the microcap space through this earnings season.

For further details see:

Why I Think RCM Technologies Will Do Well This Earnings Season