D - Why I Won't Be Buying This Dip On Dominion Energy

2023-03-24 07:09:53 ET

Summary

- Dominion Energy regularly carries high debt and a significant portion of its operating income is spent on interest payments.

- The long-term pace of revenue growth is lower than the long-term pace of dilution.

- Since 2017, a rise in revenue has been accompanied by a drop in net income and a net margin contraction.

- Dominion Energy is a Hold.

Thesis

Dominion Energy ( D ) has seen a significant decline in its valuation and at first glance this company looks like a buy-the-dip opportunity. Upon closer examination, the company regularly carries a heavy debt load and appears to be becoming less financially healthy over time. I am recommending a Hold for Dominion Energy because the financial situation of the company is too poor for me to be comfortable buying it for the long term.

Company Background

Dominion Energy is headquartered in Richmond, Virginia and provides electricity and natural gas to about 7 million customers in 16 states. Like many Utility Companies in the United States, they have pledged to be net zero emissions by 2050.

The company has long history of mergers and divestitures, but I am going to only bring up two of them. In 2018, Dominion stepped in and bought SCANA Corporation in the wake of the Nukegate scandal. Dominion paid for the purchase with $6.8B in shares, and also took on an additional $6.6B in debt. This dilution shows up later in my charts.

The second transaction I want to bring up was when Berkshire Hathaway (BRK.A) announced they were buying natural gas assets from them in 2020. Dominion was trying to shed $5.7B in debt during the transaction. Over a year later, Berkshire would change its mind about buying Questar Pipelines from Dominion.

Long Term Trends

The CAGR for both Natural Gas and the U.S. power grid, as well as the Inflation Reduction Act will all provide sustained tailwinds for utility providers in the United States, including Dominion Energy. The federal government is subsidizing a major equipment update. Typically, this is where I would cite a few facts about the Inflation Reduction Act and state that I like that the company has chosen to try to achieve net zero emissions; but instead, I'm going to talk about interest rates.

The Federal Reserve has a long term average inflation target of 2% , and this typically comes with a loose job market . In its quest to fight inflation, the Fed is expected to continue hiking rates and then keep them elevated for a while before lowering them. Expectations for the timing and pace of lowering fluctuate as events unfold, but current projections estimate it will be around 4.9% by the end of 2023, 3.1% by the end of 2024, and 2.4% by the end of 2025.

Financials

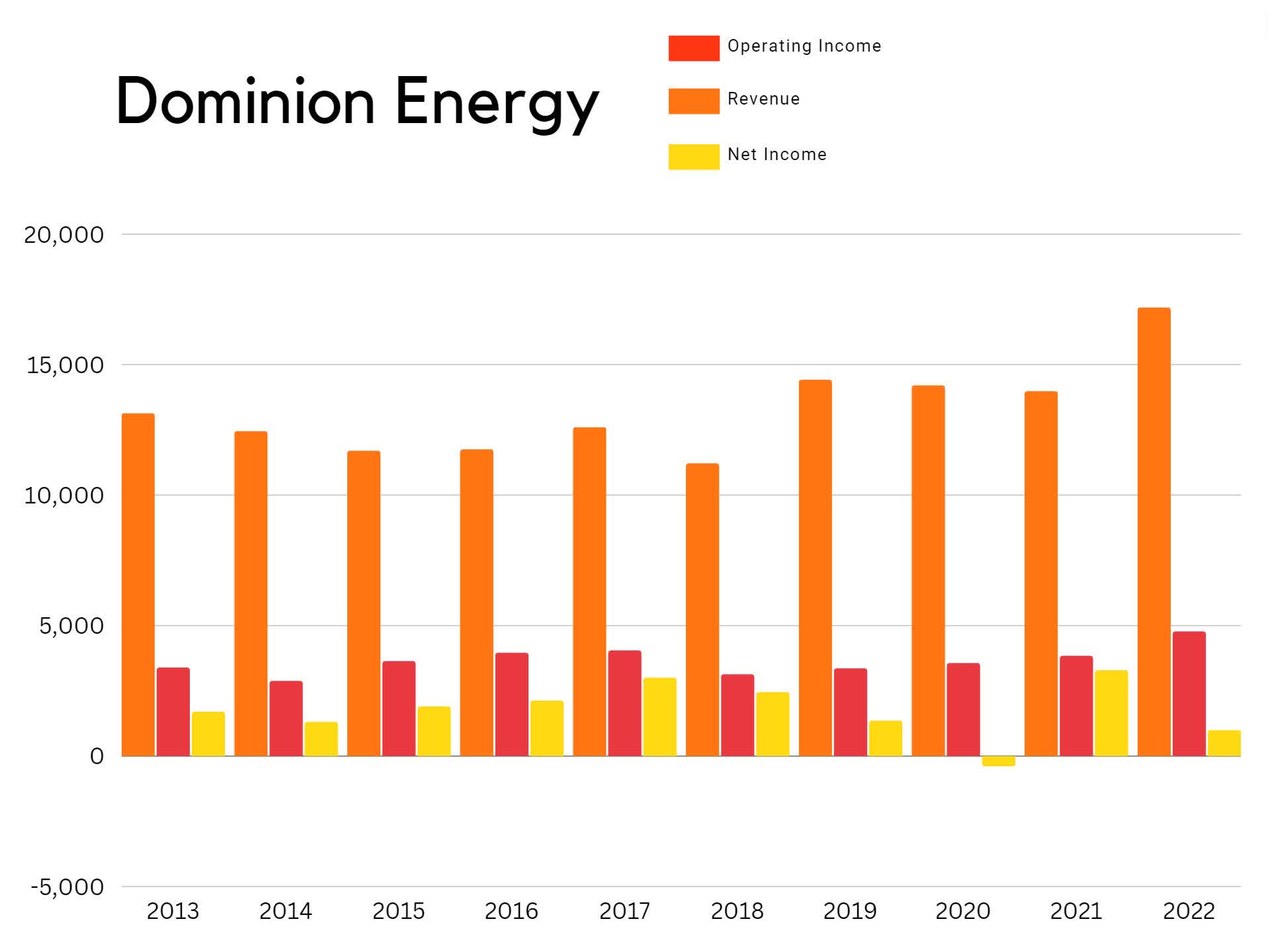

Looking at annual revenue over the last decade shows that the company has been growing. Their operating income has been stable, but their net income hasn't. Net income has been declining since they posted $2.999B in 2017, and by 2022, it was only $994M. The reason I am inclined to treat their 2021 net income as an outlier, is because a significant portion of the $3.288B was from unusual items and not regular operations.

Dominion Unusual Items (Seeking Alpha - Dominion Financials)

{kind=link}

{kind=link}

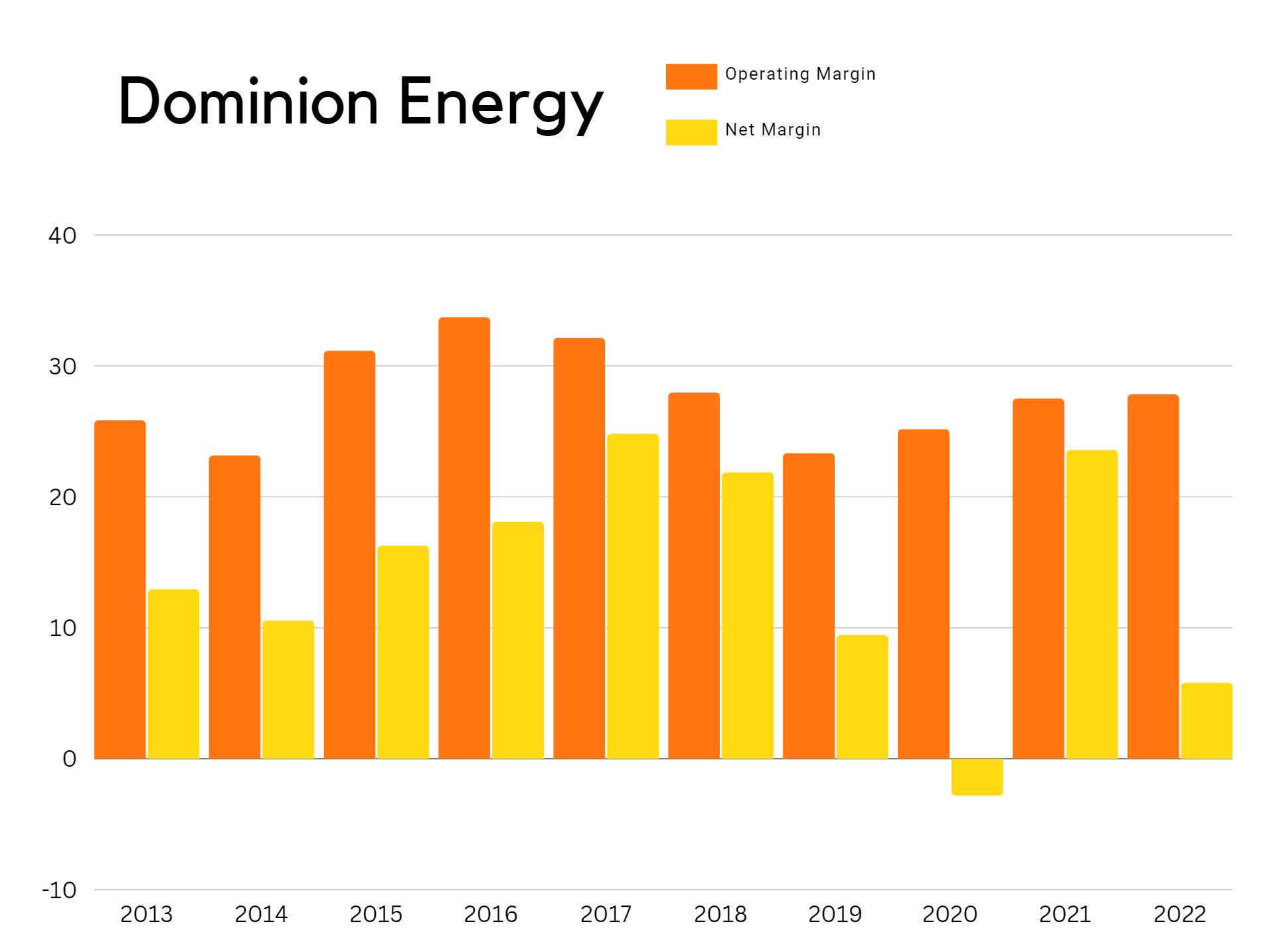

Operating margins have stayed fairly stable; this is a major positive. What jumps out here are the significant fluctuations in net margins from year to year. Utilities are subject to variations from both short term seasonality and the long term price movements of fuel, so although this might look alarming, this volatility is perfectly normal.

{kind=link}

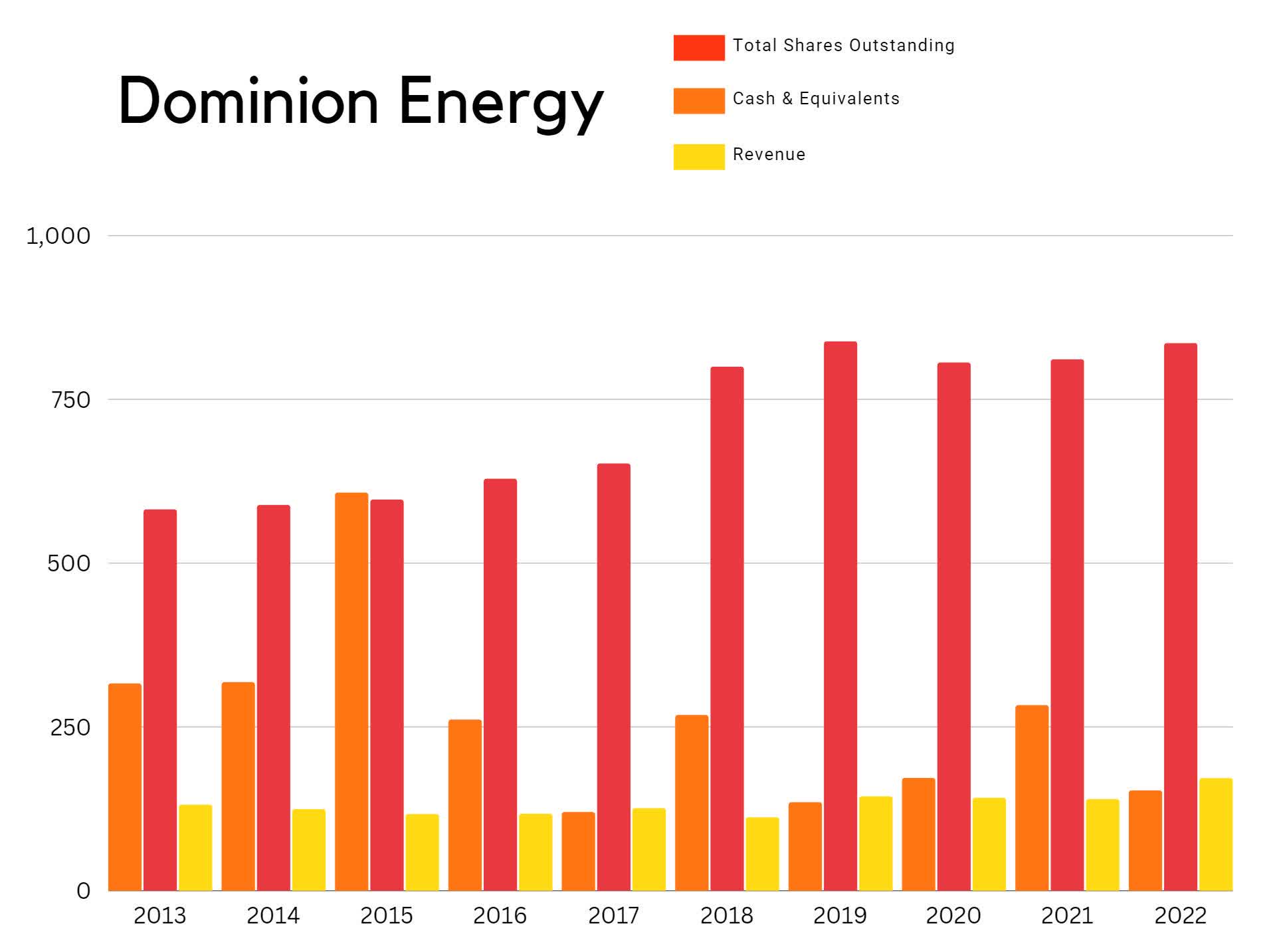

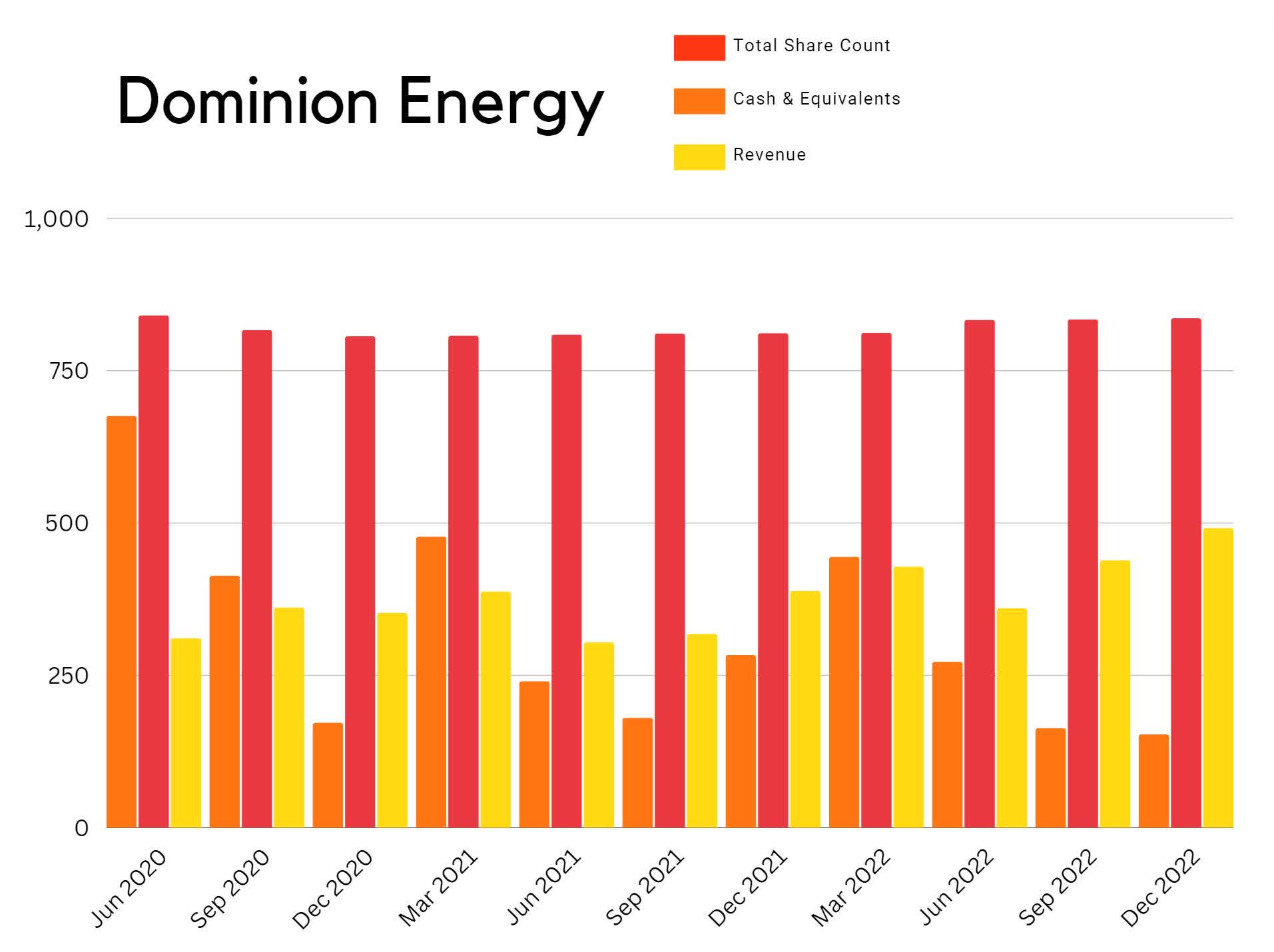

I always look at the relationship between float, cash, and revenue to get a sense for how well a company translates dilution into revenue. This does not include the accounts receivable that utility companies like to group with cash on their balance sheet. What I don't like here is that the increase in share count was not followed by a significant rise in revenue. The share count rose from 585.5M in 2013, to 835.2M in 2022, a 42.6% rise. Over that same time, revenue rose from $13.12B to $17.17B, a 30.9% rise. Even when dilution is accretive, it is typical for the revenue increases to lag behind the dilution events. But when the long term pace of dilution is higher than the pace of revenue growth, it's a red flag.

{kind=link}

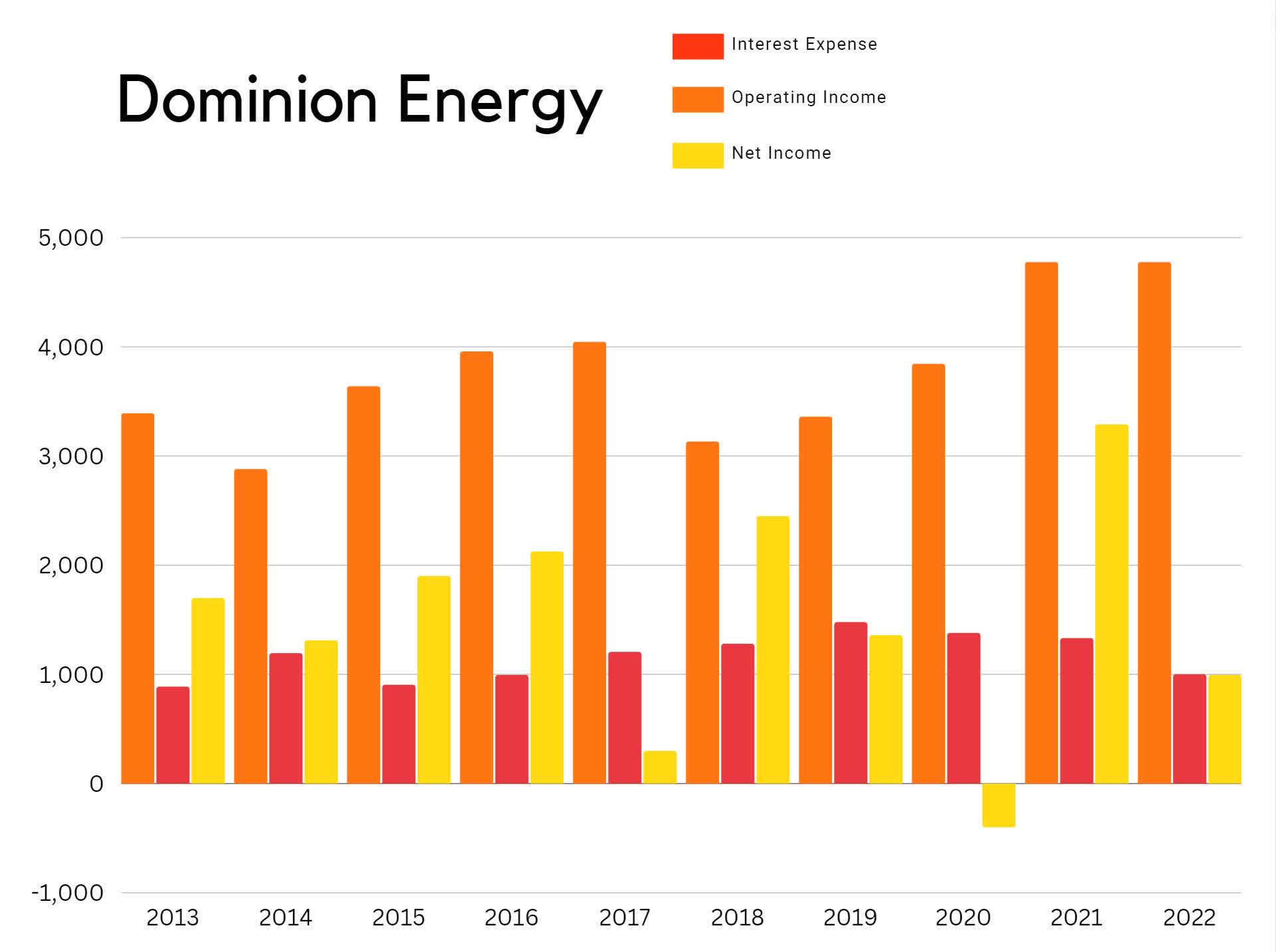

When I decided to take a deeper look into their balance sheet and cash flow statements, it became more clear that this company has a debt problem. Since operating income varies from year to year, their relatively stable interest payments are causing a significant drag on their net income.

{kind=link}

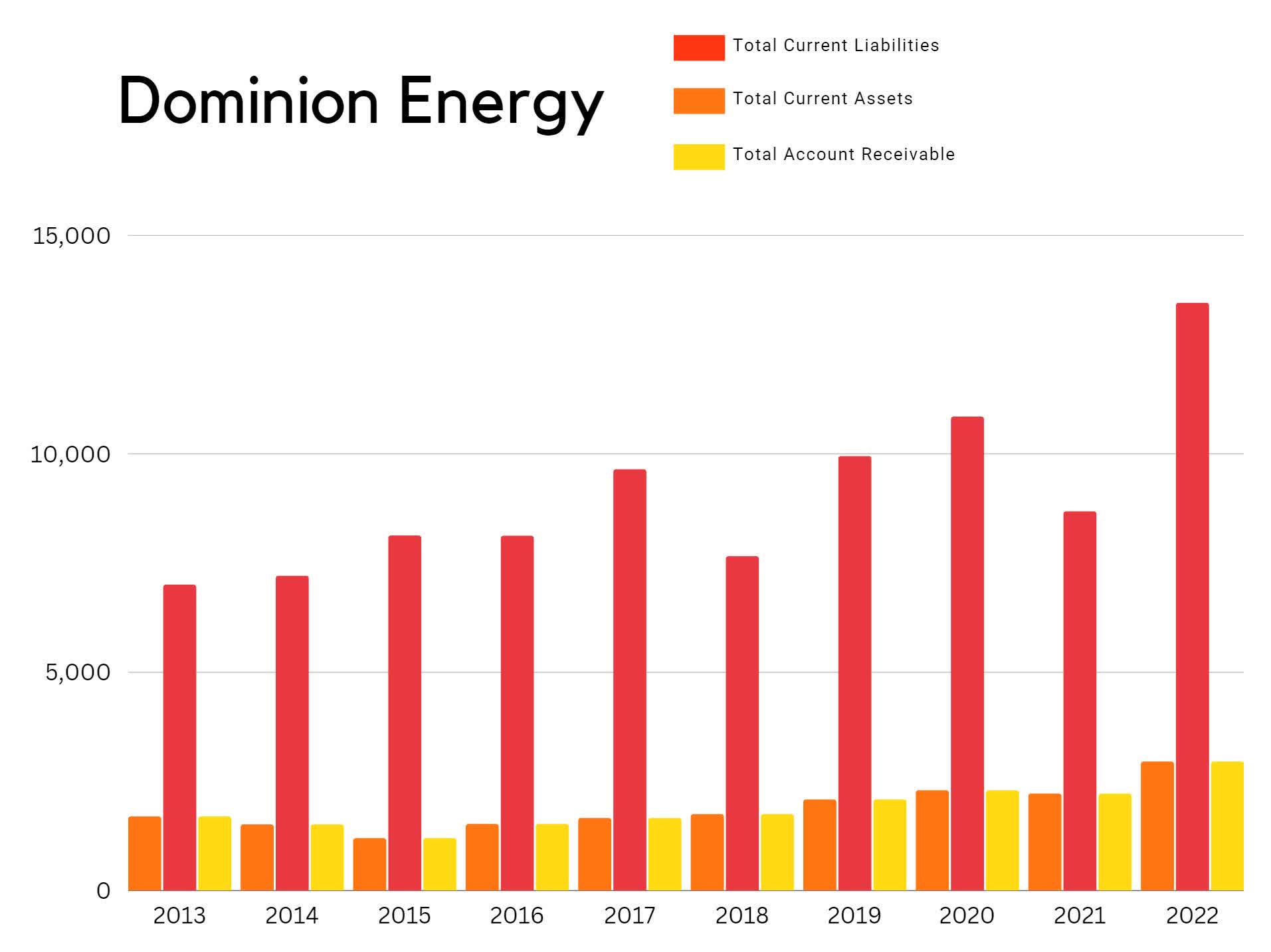

Since 2013, short term liabilities have grown from $6.99B to $13.45B, a 92% rise. Over that same time, current assets have gone up 66% from $5.94B to $9.85B. Accounts receivable went from $1.69B to $2.95B, a 75% rise. So their short term debt is rising faster than either their assets or their accounts receivable.

{kind=link}

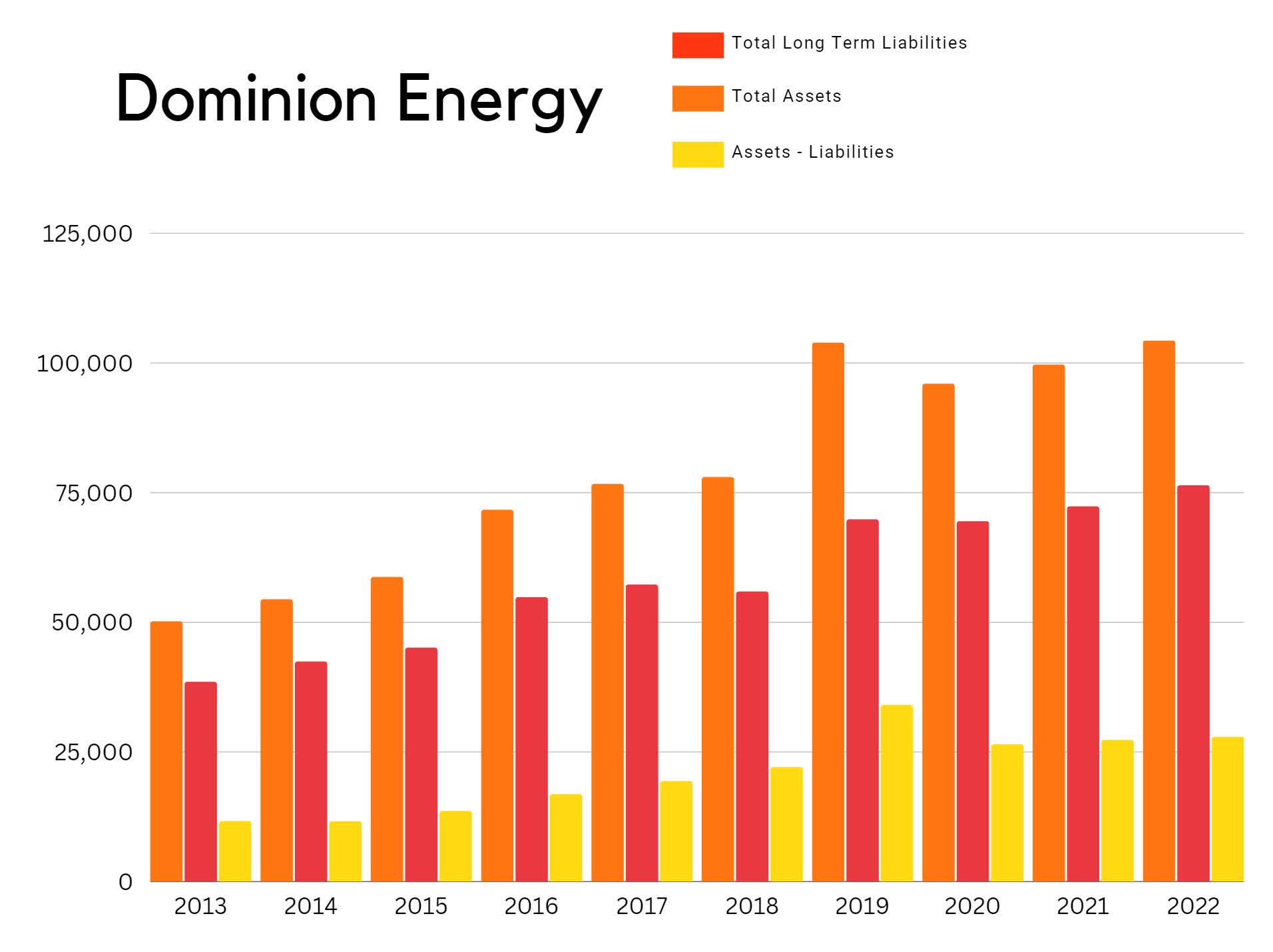

Assets minus liabilities has actually been slowly going up. This seems to be the one positive trend related to their debt. If this were going down slowly instead of up, the tone of this article would be bearish instead of cautionary.

{kind=link}

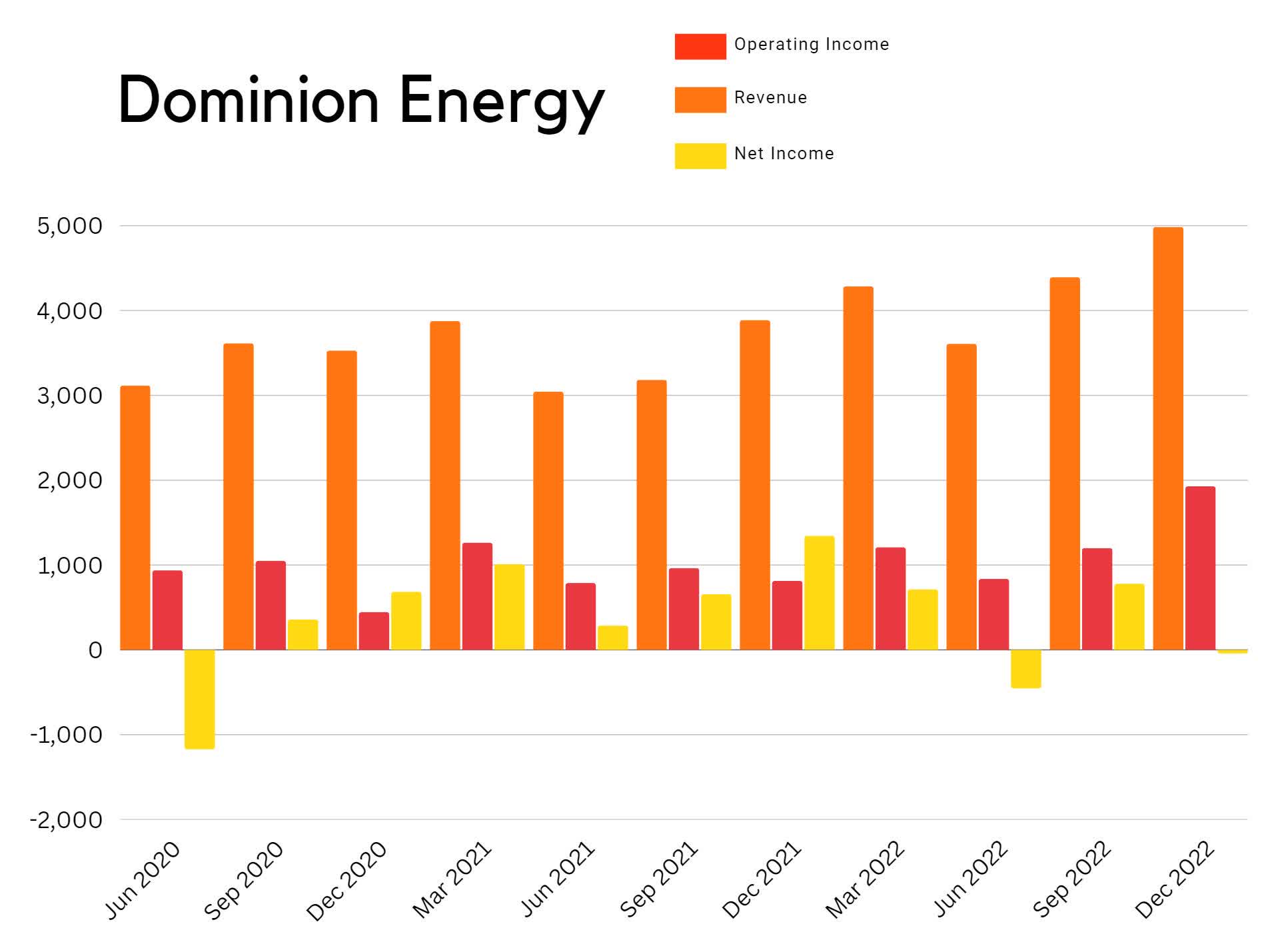

Taking a look over their quarterly revenue, it's clear that Dominion suffers from the same seasonality that is typical with the utilities sector. The seasonal swings in demand driven revenue affect each company uniquely. For this company it means weakness in their second quarter revenue, and strength in the fourth and first quarter of every year. Dominion also traditionally has negative net income in the second quarter of every year. I don't like that the most recent quarterly net income was negative even though previous Q4's have been good earners for the company.

{kind=link}

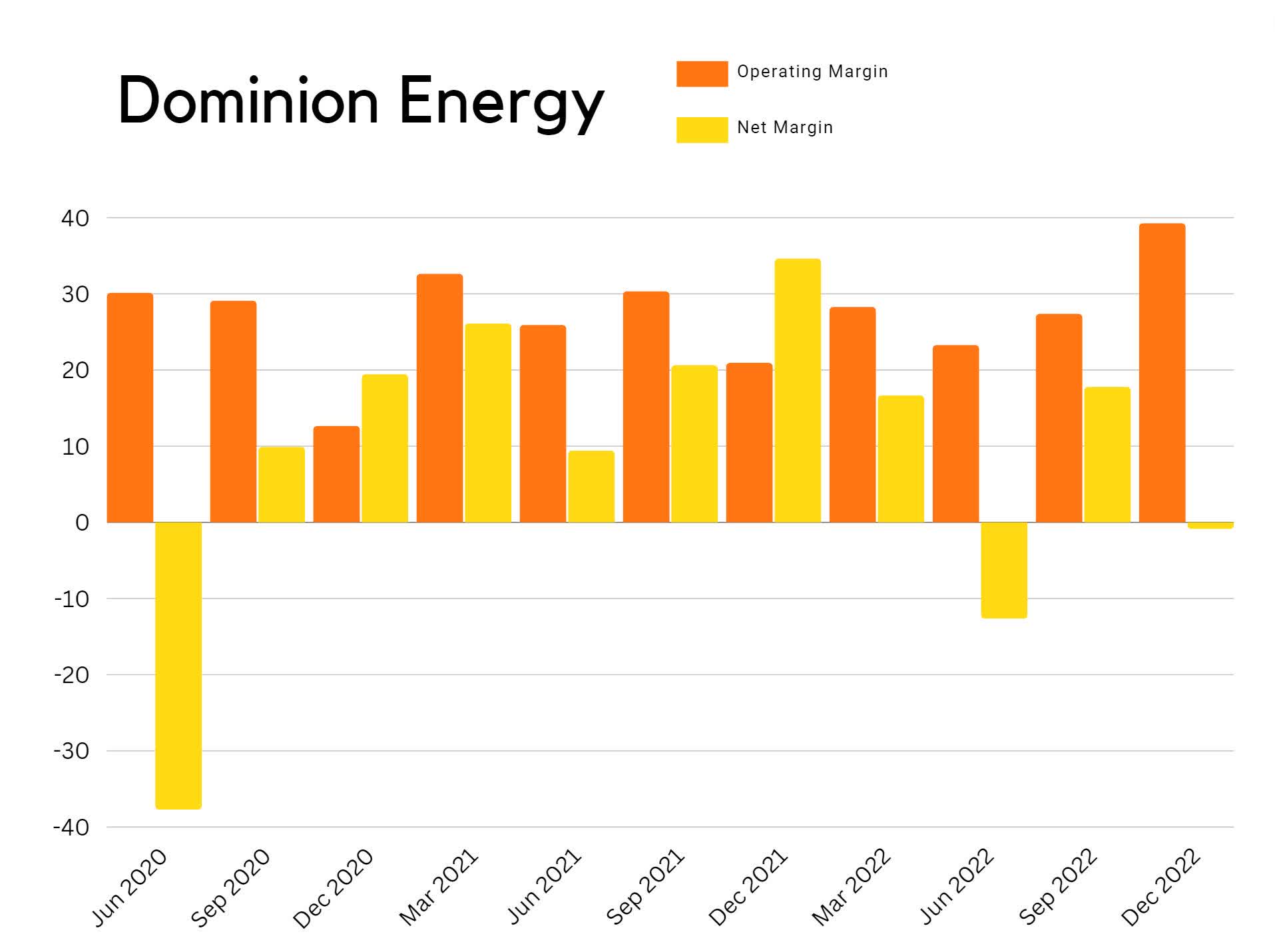

Their quarterly margins tell a similar story. The summer months do not generate very much revenue for the company. I like that operating margins are staying stable, but I don't like that net margins are this volatile.

{kind=link}

Taking a look at their share count compared to revenue on a quarterly basis, it's clear that revenue has been rising and the float has been relatively stable. Since Q2 2020, total shares outstanding dropped from 840M to 835M. Looking at their worst quarters because of seasonality, Q2 2020 to Q2 2022 revenue rose from $3.106B to $3.596B.

{kind=link}

Valuation

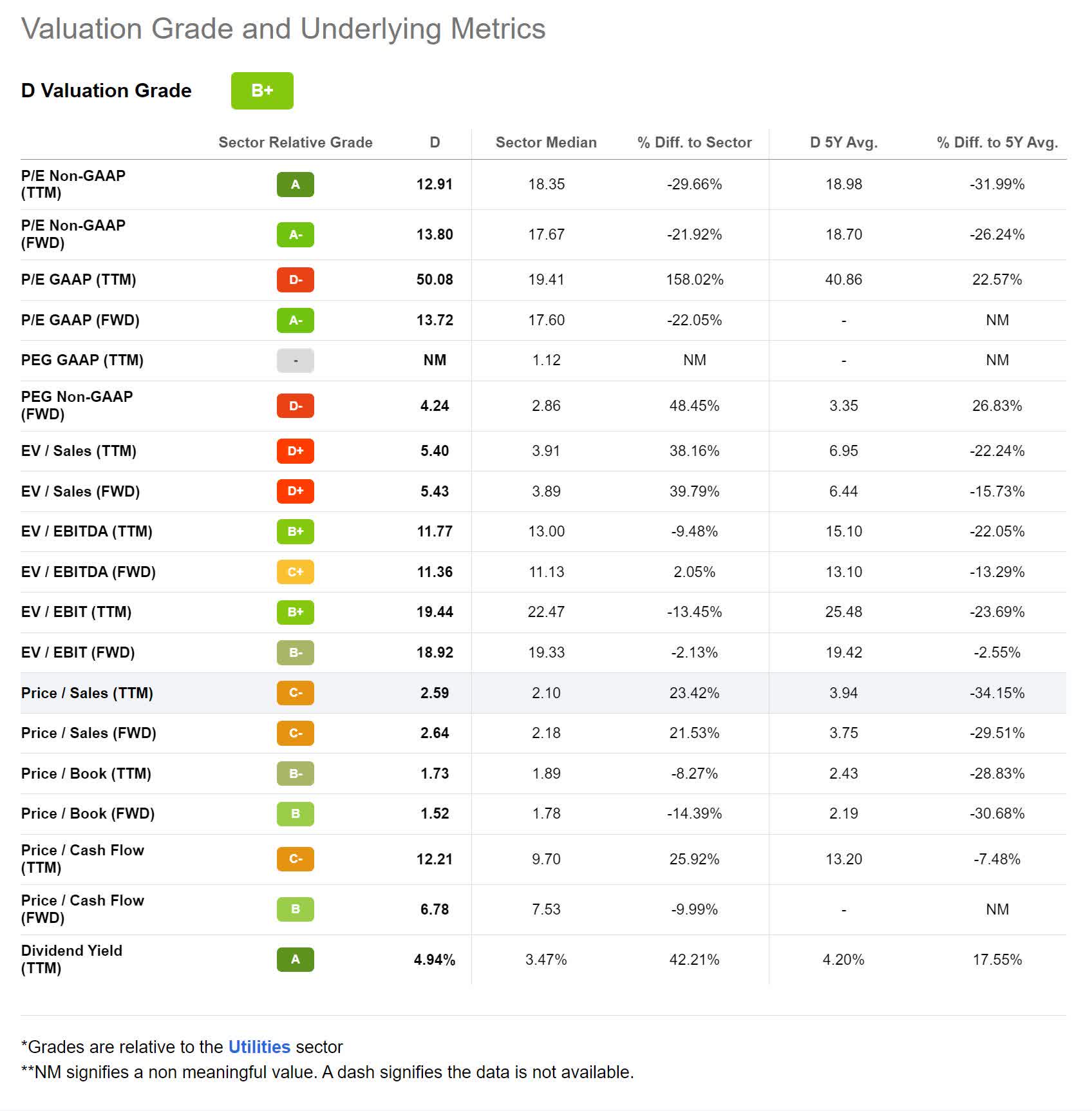

As of March 22 2023, Dominion Energy had a market capitalization of $45.18B and was trading for $53.21 per share. It has poor valuations for EV/Sales because of its large debt.

{kind=link}

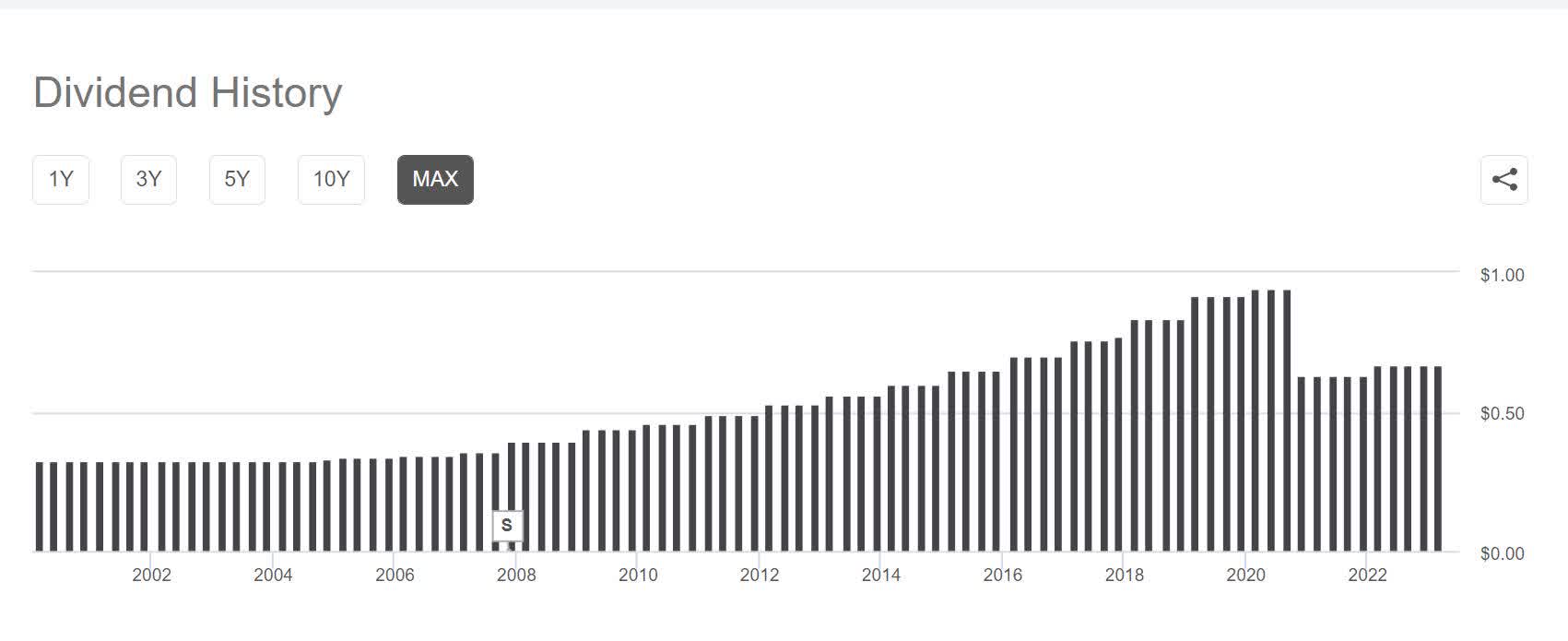

The dividend history shows a major correction at the end of 2020. Using today's annual dividend of $2.68, a dividend growth rate of 6%, and a discount rate of 10%, a discounted cash flow model produces a fair value of $49.94 per share.

{kind=link}

Risks

Although unlikely, the tailwinds provided by the Inflation Reduction Act would go away if it were repealed or undermined by new legislation.

Our energy grid is perpetually threatened by both natural disasters and malicious intent. Most disruptions of this nature will be temporary and have a low chance of causing permanent damage to the company.

The company already has debt obligations that represent significant, but not unsurmountable headwinds. If the company were to incur a major unexpected expense or drop in revenue, they would be in danger of having to either dilute or take out more loans to raise funding. This puts them at risk of either falling behind on their ability to keep pace with their debt, or lowering EPS through dilution.

If inflation proves to be stickier than the Fed is expecting, then they will be forced to raise rates suddenly and this company, along with all of the rest that are used to carrying a high debt load, will suffer.

Catalysts

If the Federal Reserve were forced to lower rates ahead of schedule, it could be a boon for this company. The present rate of expected lowering is gradual, but a black swan event could force the Fed lower suddenly.

Conclusion

Since 2017, revenue has been rising while net income has been going down. Ignoring the outlier caused in 2021, net margins have experienced a contraction over that same time period. Share count has been outpacing revenue growth. Their short term debt obligations are rising faster than their assets or their accounts receivable. They regularly carry high debt and a significant portion of their operating income goes toward making interest payments.

Even though the discounted cash flow calculator produced a fair value estimate of about $50, I am not willing to buy into this company. For me, their financial situation looks too unhealthy. I would be concerned that the dividend cut they experienced at the end of 2020 was not a one-time event and that the company might have trouble maintaining dividend growth. In order to turn me into a buyer, Dominion Energy would first have to slash its dividend even further to a level where it can begin aggressively paying down its debt obligations. I would need to see evidence the health of the company was improving.

For those of you who have more conviction in this company than I do, today's price of $53.21 per share is fairly close to the calculated fair value of $49.94, and the near future may present even better buying opportunities. If I were planning on investing into Dominion Energy, I would keep my overall position size small and sell out of the money covered calls against the shares. I would also not reinvest dividends. My goal would be to lower my cost basis as fast as possible.

For further details see:

Why I Won't Be Buying This Dip On Dominion Energy