ITJTY - Why Intrum AB Has A Great Long-Term Upside

Summary

- In this environment, we want to be looking at credit and finance companies that come to be beneficiaries of the current rate increase trend.

- One of my favorite companies for this is actually Intrum AB - a company you may not even have heard of.

- In this article, I will present you with Intrum, and why I own 3.5% of my portfolio in the company.

Dear readers/followers,

In this article, I'm going to be presenting you with an upside that I believe to realistically be in the triple digits. I'm talking about the European company, and Swedish-listed business Intrum AB ( ITJTY ) ( INJJF ).

In this exclusive piece, I'm taking you through the company's specifics and telling you why I recently pushed significant capital to work for the long term in this company.

Looking at Intrum AB - What it is and what it does

It shouldn't be a surprise to you that companies that work with credit, insurance, and payment delinquencies are somewhat volatile businesses to own. Intrum is no different.

Intrum AB, as it stands, is a market-leading credit management company. It specializes in debt collection.

Most people's first encounter with Intrum is when a letter falls into your letterbox because you've missed or been unable to pay an invoice or a debt - sometimes as low as $10, sometimes as much as $20,000 or more.

Intrum does business in 24 countries across Europe but has also expanded to LATAM, with a Brazilian business. The company employs over 10,000 people across the group and has a market cap approaching $2B at this time. For a Swedish company, this is massive.

The company also owns several subsidiaries you might be familiar with, including Lindorff, Intrum UK Limited, Lowell Norge AS, MER, and others.

Its trading history as a stock is quite interesting. More than once during the past 5 years, the company has crashed with a very suddenness, only to very quickly recover to what would be viewed as "Normalized" levels.

So when the company crashed only a few weeks/months back, my alerts were ready and immediately notified me that the company had gone below 140 SEK/share.

The market has a strong tendency to underestimate the fundamental stability of this business. Given the company's operating areas, this might not be all that strange.

Intrum categorizes its operations into two primary businesses, under the ONE operating platform.

First, it has a servicing arm. The servicing arm is the meat & potatoes of the business, which contacts 250,000+ customers daily to assist and encourage them with debt payments. Intrum has over 80,000 clients using their services, and generates over a billion dollars in external revenues, with another $300M in internal ones. Some of the major client wins the company has include businesses like Credit Agricole ( CRARY ), Cembra Money Bank (No Symbol) out of Switzerland, and the UtP Italia Fund.

The second segment is its portfolio investments. Intrum takes assets and invests these, currently at a book value of around 40B SEK from 19,000 batches. The ONE operating platform guides the company in its daily work, and the recent highlights here are good, despite what the share price development would suggest.

{kind=link}

Now, the company's services are considered crucial in today's macro. Why?

Because a recession is widely expected despite rising consumer confidence, the implications are that 23% of European households are having problems paying their bills, especially energy. This also comes with a significantly higher cost of borrowing and increasing inflationary pressure.

Intrum, in response, is expecting significant volume increases in servicing, which is materializing, increased demand for its services from clients - also materializing, and the overall higher volume of collectibles weighing up for the lower ratio of collectability , as most customers have struggling to actually "pay up".

In short, collections volume is driving revenue and earnings, with the conversion lagging things at this time.

{kind=link}

The company's portfolio investments are also seeing the impacts of the market. Increased uncertainty and higher funding costs mean that acquiring portfolios is harder and more expensive (already materializing), non-paying clients are typically far more challenging to "activate" or motivate during adverse macro, which is also materializing, and the overall repricing of risk in the sector with increasing IRR's mean that the company has its work cut out for it. Intrum meanwhile, has significant liquidity of nearly $2B, its entire market cap, invested $130M at an IRR of 15% in 3Q22 and continues to focus on high-quality deals.

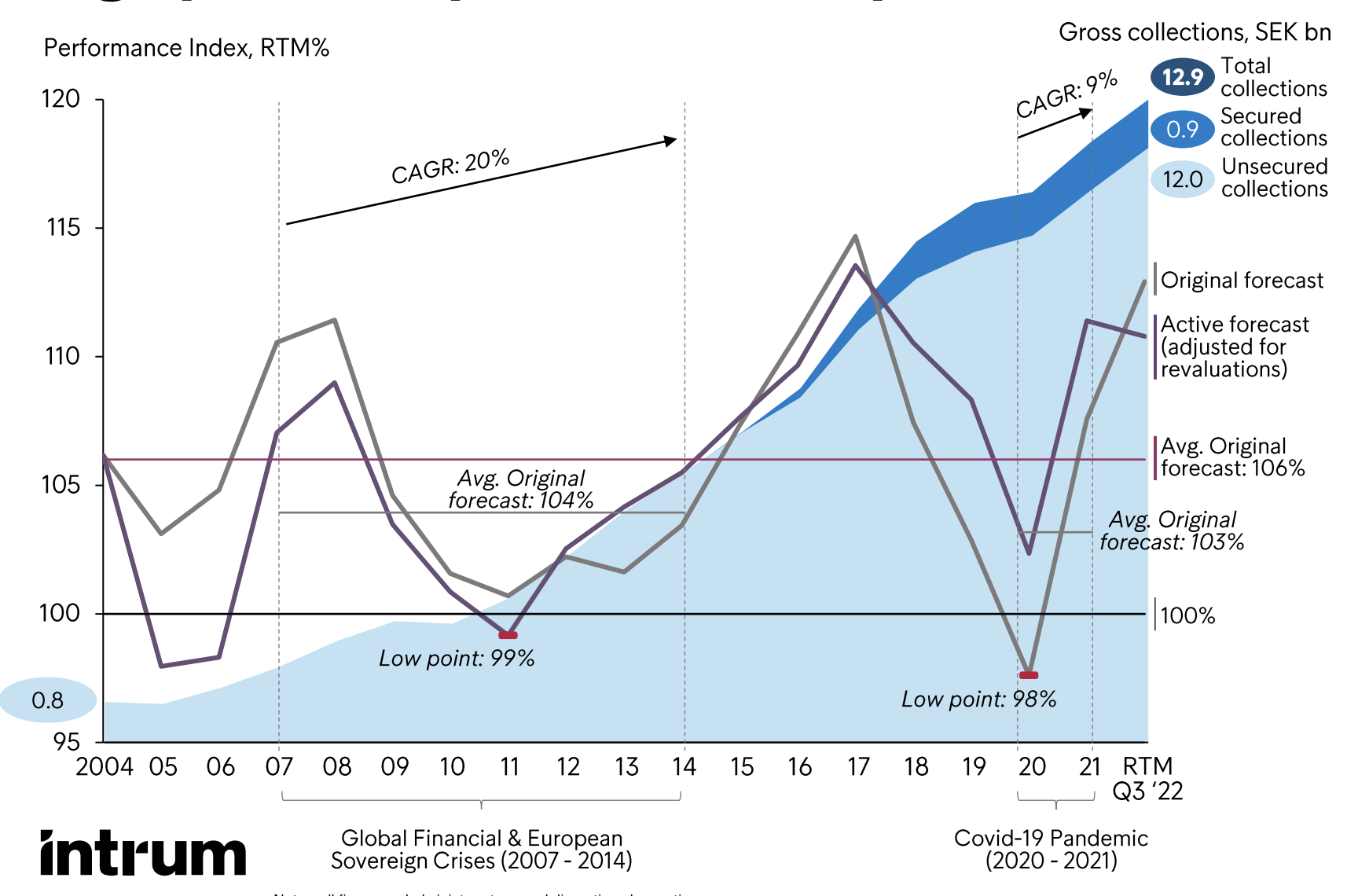

The market very typically expects Intrum's portfolios to underperform in a crisis. The result has always been the opposite.

{kind=link}

Since 2004 and including multiple severe crises, the performance index versus the original underwriting forecast has never dropped below 98%. The recoveries, as you can see, have been sustained and immediate, and collections/servicing have grown throughout the crises. Intrum has expertise in quality underwriting, and good diversification and is experienced in providing sustainable and "workable" payment plans for its clients.

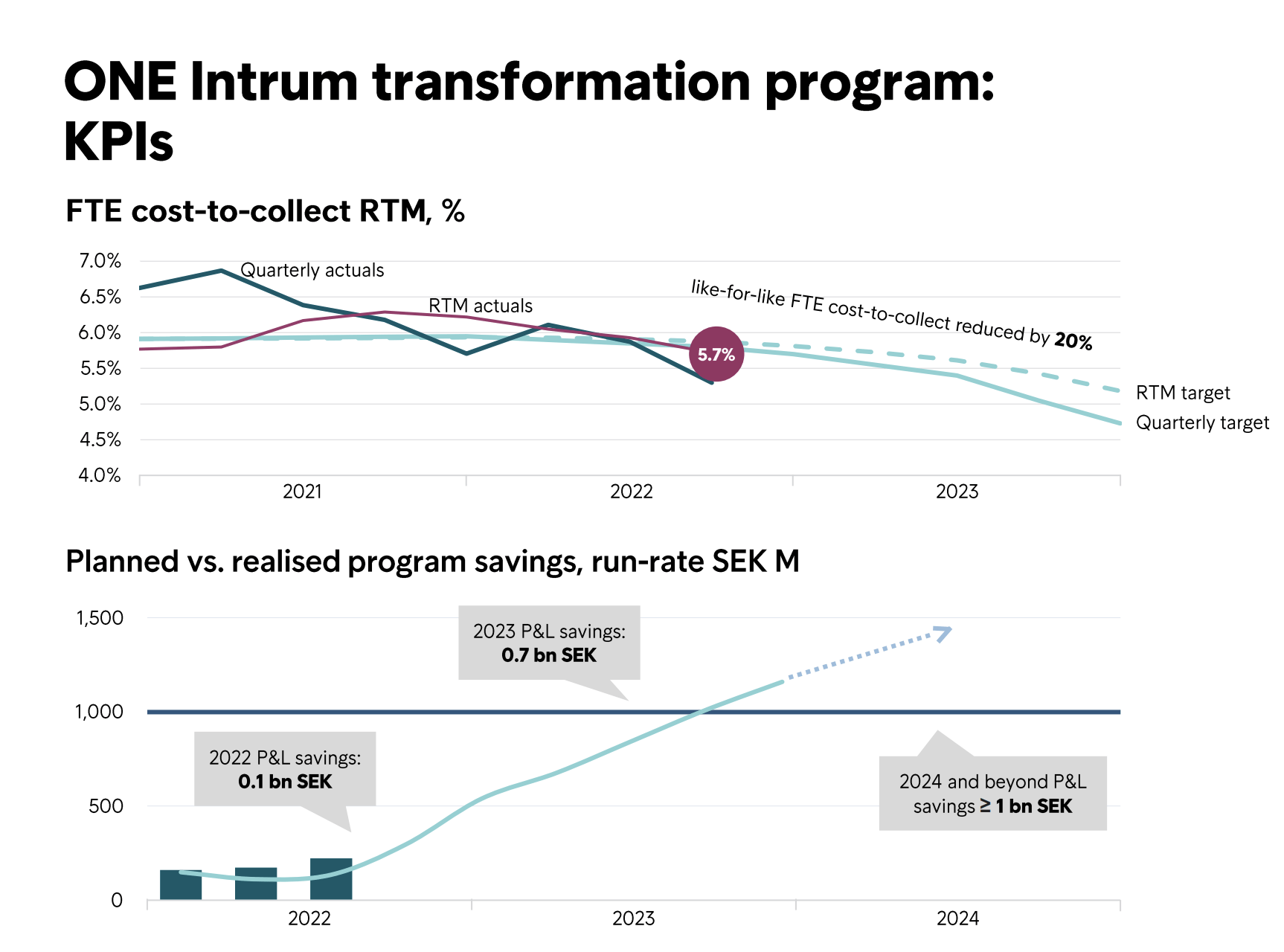

The company has multiple transformation plans in the works, with Its ONE Intrum transformation leading to reduced spending and at least 1B SEK of benefits collected. The program is working above expectations, with spend 4% below expectations YTD. Here are the benefits so far of that transformation plan.

{kind=link}

Intrum plays a core role in a healthy economy. It may not be popular to work with, invest in, or boast that you own a collections agency, but the fact is that this is a necessary part of modern society.

I have personal experience with Intrum, as I once missed paying a phone bill and got a small $8 fee charge from Intrum, but their processing and simplicity of paying it were impressive. I realize that some of you might perhaps not put payment collectors and debt servers as high on your attractive investments lists, but let me assure you that these companies can be superb investments.

{kind=link}

Also, fundamentally speaking, they're extremely sound. The company's Cash EBITDA has been growing at 8% CAGR throughout 2022 since 2018, and the company's leverage is down to just south of 4x net debt/Cash EBITDA, with a 7% CAGR increase in dividends since 2018.

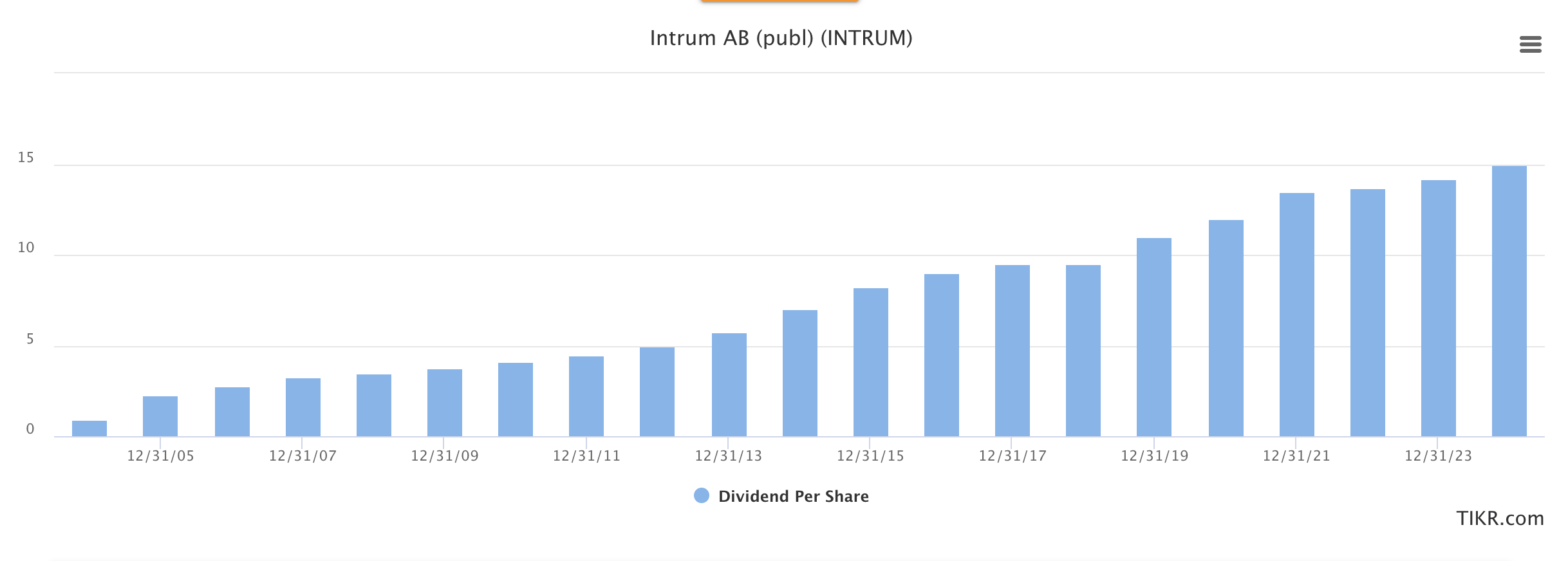

Speaking of the dividend, it's potentially massive.

At its current valuation, the company's native yield is no less than 9.5% , and that dividend is very well-covered with a strong tradition. Here is that tradition historically, and expectations for the next few years.

Intrum Dividend (TIKR.com/S&P Global)

{kind=link}

Take a look at that tradition. The company has not lowered the dividend through multiple crises. The closest it came was freezing it at 9.5 SEK for one year. For next year, we're expecting a small token increase that would bump the current YoC up to around 9.66%. My own YoC is over 10%, given that my cost basis is closer to 135 SEK at this time.

And yes, I view this dividend, all things being equal, as relatively safe despite recent troubles.

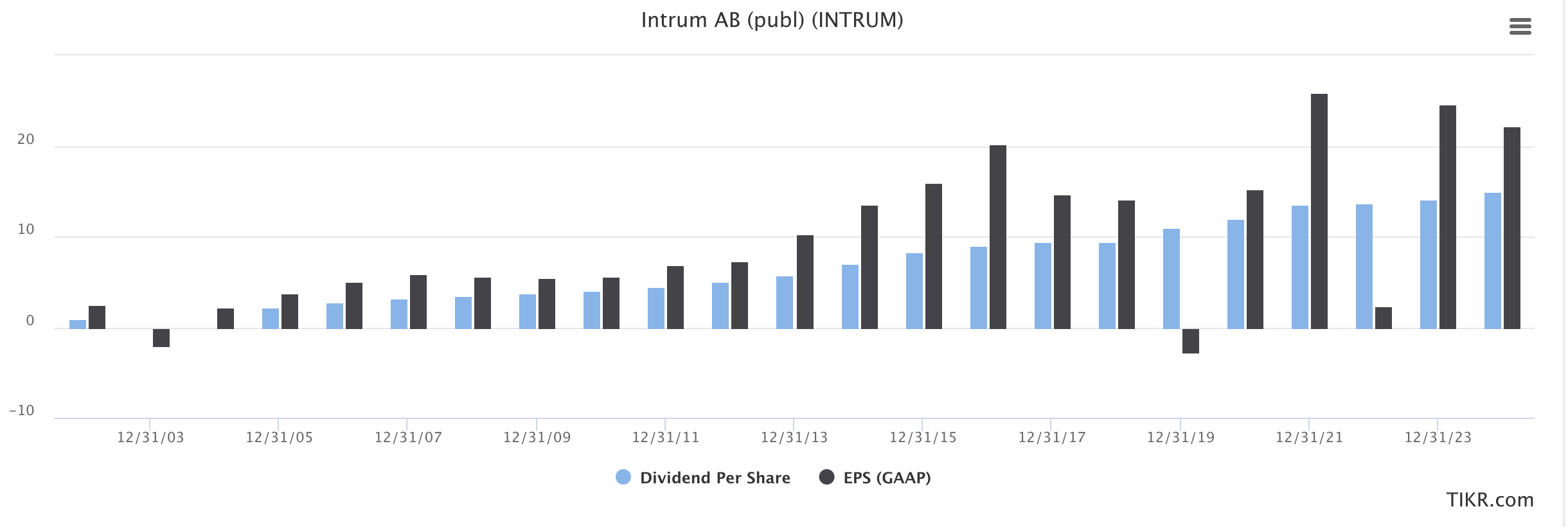

That isn't to say that EPS is always stable. The nature of the company's business is that we can sometimes see years of volatile GAAP EPS ups and downs, and we're expecting to see one such in the coming year.

This is also part of the reason why the company is trading down so much.

Intrum EPS/Dividend (TIKR.com/S&P Global)

{kind=link}

But as you can see, this has happened in the past, and it did not influence the dividend at the time. Still, there might be 2022 dividend impacts (more on that in the next few paragraphs).

The latest results confirm substantial cash generation and showcase the company's incredible resilience in a difficult macro. Collections are up over 30%, driving both costs and income, with an inflow mix that tends to highlight higher collections costs, but lower conversion (as mentioned before). It's more difficult to get people to pay when things go down the drain.

Like any company, Intrum has to re-evaluate its portfolios and assets on a continual basis - and one such recent change was a non-cash adjustment to the Italian JV portfolio, which saw a $250M+ reduction in BV on that portfolio, impacting the P&L. The company was back up to 160 SEK and above but dropped again when only a week ago or so, it was forced to make another adjustment amounting to the BV of SPV of around 3.1B SEK. This was a non-cash item and won't impact leverage and performance KPIs as such, because it's related to one specific transaction on a specific, secured portfolio, but the market still reacts - and justifiably so.

The company hosted a special call on the 28th as to this fact, explaining this write-down.

What happened last week was a reflection on our books of a price established via transaction between 2 independent third parties on a corresponding asset held on our balance sheet. Specifically, CarVal, our co-investor on this deal, has sold their 37.5% stake in Ithaca DAC, which is the Italian SPV, which holds 95% of the portfolio, that we, together with investors, acquired from Intesa in 2018. They sold that 37.5% stake to Kistefos for consideration of approximately EUR 10 million. We have to acknowledge this reality and reflect this objective price point in the valuation of our corresponding 62.5% stake in the same Ithica DAC SPV, which implies a write-down as was announced of SEK 3.1 billion and also applies a residual book value for our stake of around EUR 17 million and a write-down of the estimated remaining collections of SEK 5.4 billion, with a residual ERC for the investment of just under EUR 80 million.

(Source: Andres Rubio, Special Call, Intrum AB)

Obviously, this is far from any sort of positive, but my view is that it's all related to a single transaction initially done in 2018, with a refi during the last year. Intrum has no choice but to reflect this in the BV despite it being third-party, and its actual cash impacts won't begin until 2025 and beyond. It does impact the company's necessity to pay down its senior notes, reducing leverage, and this is potentially where a dividend cut could come into play if the company feels that such a lever is necessary to sort of get ahead of the market on this. Even if this was the case, I would still view the company as an excellent investment, as such a reduction or cut would be temporary, and the underlying value of Intrum would be closer to 100% higher than the current share price suggests.

In the end, what happened here cannot repeat itself, because Intrum accepted a very unfavorable derivative agreement with the counterparty that is not accepted in any other of its related SPV's.

The company's current share price reflects the challenges that the company is facing in the near-term. Intrum stands before the choice of carving out either part of, or cutting the dividend entirely to reach its delevering target, which has been made trickier by this recent derivative agreement and write-down. So the current price, and the drop, reflects this near-term uncertainty.

If you're not a fan of such near-term uncertainty and can't accept it as a risk in order to invest at Intrum at what is close to COVID-19 valuations, this might not be for you.

However, let's look at valuation.

Intrum's valuation

The company is cheap, simply put, but there are reasons for it.

The uncertainty currently reflected in the share price is a real one. The company, given the clear messaging about priorities, could realistically decide to reduce or cut the dividend to address its leverage priorities prior to shareholder remuneration.

Will they?

That's hard to say.

If they were to cut it by 50%, it would still be an attractive dividend in the near term. They would also cut their own dividend tradition, which is implied as being of high importance to the company here.

I would say that in order to invest in Intrum, you need to accept the possibility of a year of reduced or no dividend, in order to harvest that potential triple-digit RoR in the longer term. If you are unwilling to take on that risk, you would do better looking at other investments.

Current price targets for Intrum reflect this reality. We currently have 4 analysts following the company, with PTs of 140 to up to 300 SEK per share. Half of them are at a buy, and the average PT is around 200 SEK per share, with 4 months ago being around 300 SEK per share. In an unencumbered environment without the recent write-down, I view the company as easily being worth 300 SEK per share, implying a triple-digit upside here.

But it may take time for the company to reach this target again. The company's underlying business is absolutely timeless - it's going nowhere - and the only question on everyone's mind here is essentially how the company will go about using its impressive cash flows to address its various concerns - will they be directed to delevering, dividends, or growth?

I think we can discount growth for the time being - the question and choice are between maintaining its dividend and "quickly" cutting down to that 3.5x target that investors want to see. Because doing both with the highest priority is obviously not possible in the next year.

I believe realistically, that the company will choose a middle ground, trying to appease both dividend investors as well as the credit and bond market, which could result in a somewhat reduced dividend for at least one year's time.

Given that all other fundamentals are solid, and given the company's progress in delevering prior to this, its Cash ROIC and its recurring EPS, the question with regards to the risk here is a temporary one as I see it.

And for my investment approach, I know how to account for temporary risk. I accept it, and I see it being weighed up by the upside for the longer term.

I would never buy Intrum at 300 SEK. But at current valuations, the company trades at sub-10x P/E and less than a 0.8x BV, which to me is a most definite "BUY" signal. Even if they were to cut the dividend in half for the next year, my YOC would be equal to that of Intrum during "good" times, when the company trades at twice at high share prices.

For that reason, I view myself as being safe for the long term - and that is why I invest so much capital in Intrum, willing to wait for the company to normalize and turn my investment into a double.

It's a risk, but a modest one, and more importantly, one I can account for.

So, here is my thesis for Intrum

Thesis

- Intrum is a market-leading debt collection and credit company. In Europe and LATAM, it's one of the more significant ones. The company is currently trading down due to a mix of headwinds, primarily from assets it got as part of an M&A.

- I view these issues as temporary, even if that "temporary" could turn into 1-2 years prior to normalization, given the pressures on the company to de-lever, and do so quickly.

- I rate Intrum a "BUY" here, at any time the native share price is below 140 SEK. My long-term expectation is for the company to go above 200 SEK again.

Remember, I'm all about:

1. Buying undervalued - even if that undervaluation is slight, and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

2. If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

3. If the company doesn't go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

4. I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them ( italicized ).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

For further details see:

Why Intrum AB Has A Great Long-Term Upside