SYM - Why Investors Should Be Cautious About Symbotic: A Critical Assessment Of This High-Flying Company

2023-12-29 07:23:44 ET

Summary

- Symbotic uses AI-enabled robotics technology to process pallets and cases in warehouses, meeting the increasing demand for warehouse automation.

- The company's unique warehouse architecture maximizes space usage, increases speed, reduces costs, and reduces errors compared to traditional warehouses.

- It has a strong backlog and fundamentals that investors love, but there are risks associated with customer concentration and its dual-class share structure.

One company that has generated a lot of buzz among investors this year is Symbotic ( SYM ), a company that uses Artificial Intelligence ("AI") enabled robotics technology to process pallets and cases in warehouses or distribution centers for retail and wholesale companies. Management outlined its thesis on why its business has become essential in its 2023 Annual Report :

The global supply chain has reached a point of critical stress, driving an inflection in demand for warehouse automation across all industries. As the labor force shifts toward an older, more highly educated demographic, the warehouse labor pool is shrinking and becoming more expensive, while most well-located distribution centers are either operating manually or utilizing outdated, static mechanized conveyor systems.

Source: Symbotic 2023 10-K

If you add that retailing has rapidly evolved toward an omnichannel business model, where retailers offer customers the option to shop via e-commerce or physical stores, the complexity of supply chains and warehouse operations has drastically increased, raising demand for Symbotic's solutions. This demand has translated into rapid revenue growth and a $23.3 billion backlog for Symbotic to deliver warehouse systems from 2023 through 2029 as of the end of the September quarter. Management expects to recognize 8% of that backlog or $1.86 billion as revenue in Fiscal Year ("FY") 2024. If that forecast is accurate, that would produce 58.3% year-over-year annual revenue growth. Investors enamored with the company's high revenue growth and a solid business pipeline have bid the stock up around 360% this year.

This article will discuss the company's warehouse technology, fundamentals, competing solutions, risks, valuation, and why the stock is only a Hold despite its high potential upside.

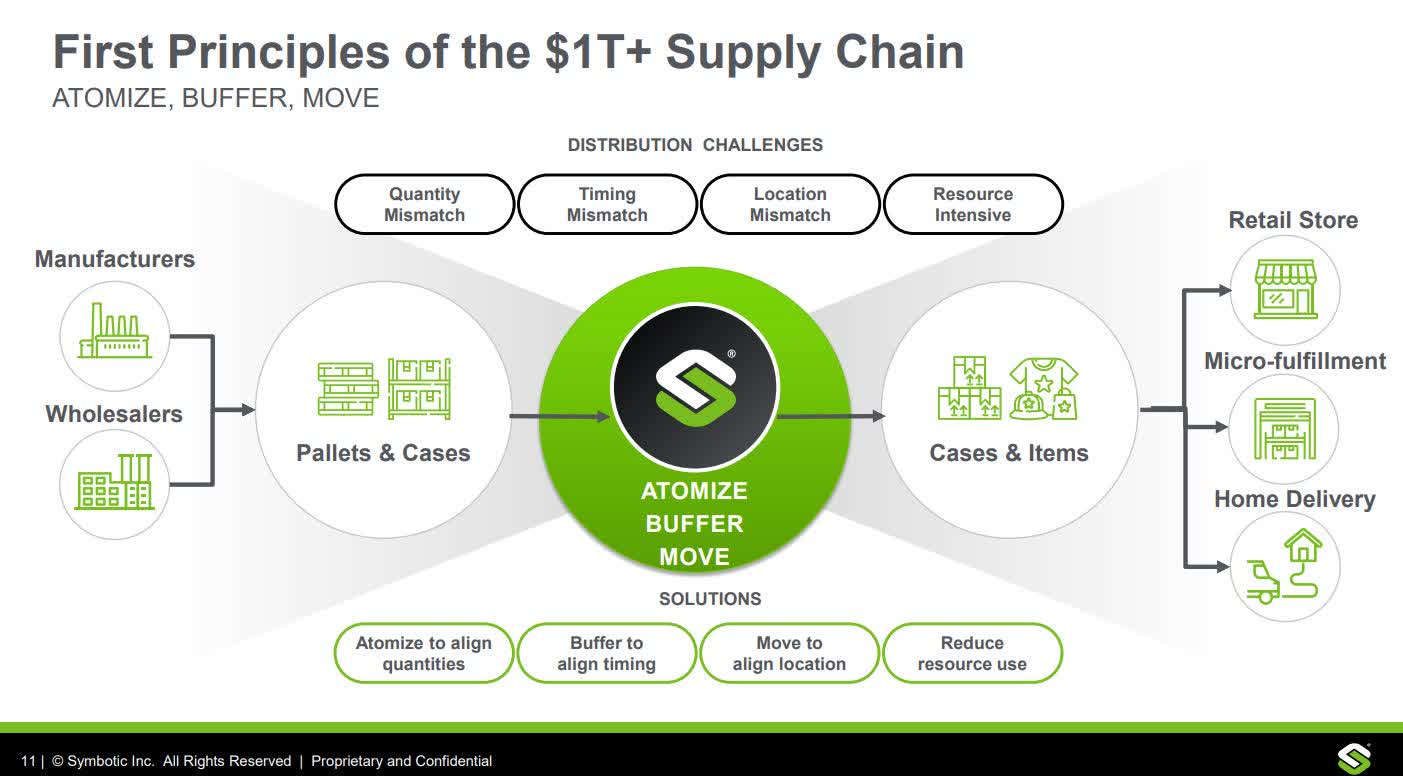

It has a unique warehouse architecture

Symbotic has reimagined and redesigned the warehouse by changing how incoming pallets and cases from manufacturers and wholesalers are handled and stored. Traditionally, warehouses have handled incoming pallets by either bulk storage of whole pallets, storing pallets on specialized racks, partially breaking up the pallet, or cross-docking , which is shipping the pallet out immediately upon arrival.

Symbotic Investor Presentation

{kind=link}

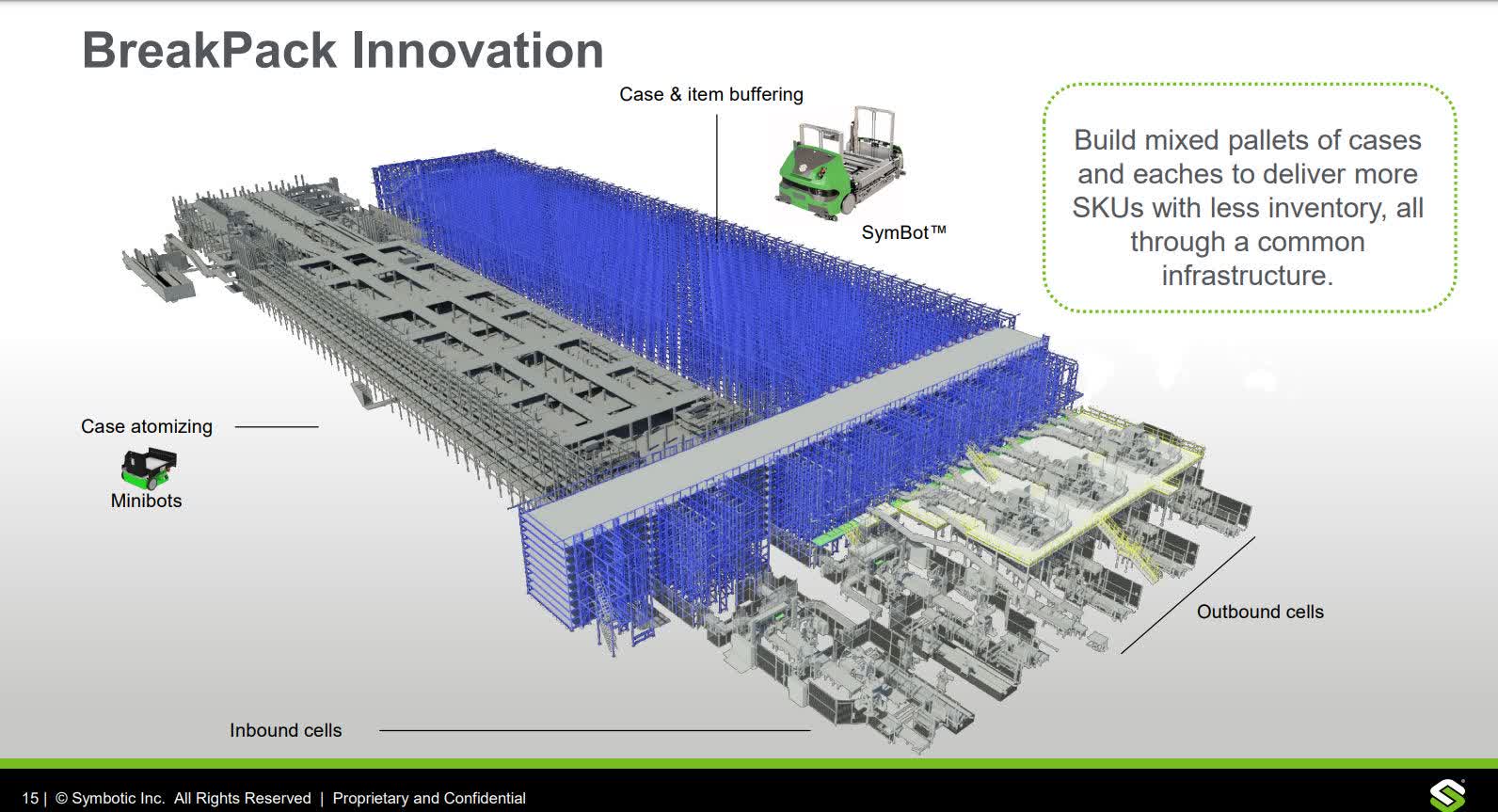

In contrast, Symbotic will break down incoming pallets from manufacturers and wholesalers into as small a storage unit as possible, saving space and making moving cases faster using robots compared to traditional warehouses using human pickers and conveyor belts. Symbotic calls the process of breaking goods down into smaller units, "Atomizing." In the image above, buffering refers to where robots temporarily store individual cases (product boxes) or items in a high-density shelving structure. Once the fulfillment time comes for a case, an autonomous mobile robot, a SymBot, retrieves it from the buffering area for another robot to build a pallet for outbound delivery to a retail store. The company is currently prototyping Omnichannel mode, where robots "Atomize" inbound pallets to individual items -- when fulfillment time comes, SymBot retrieves and packages the item for direct home delivery. This YouTube video shows the Symbotic system in action.

Symbotic Investor Presentation

{kind=link}

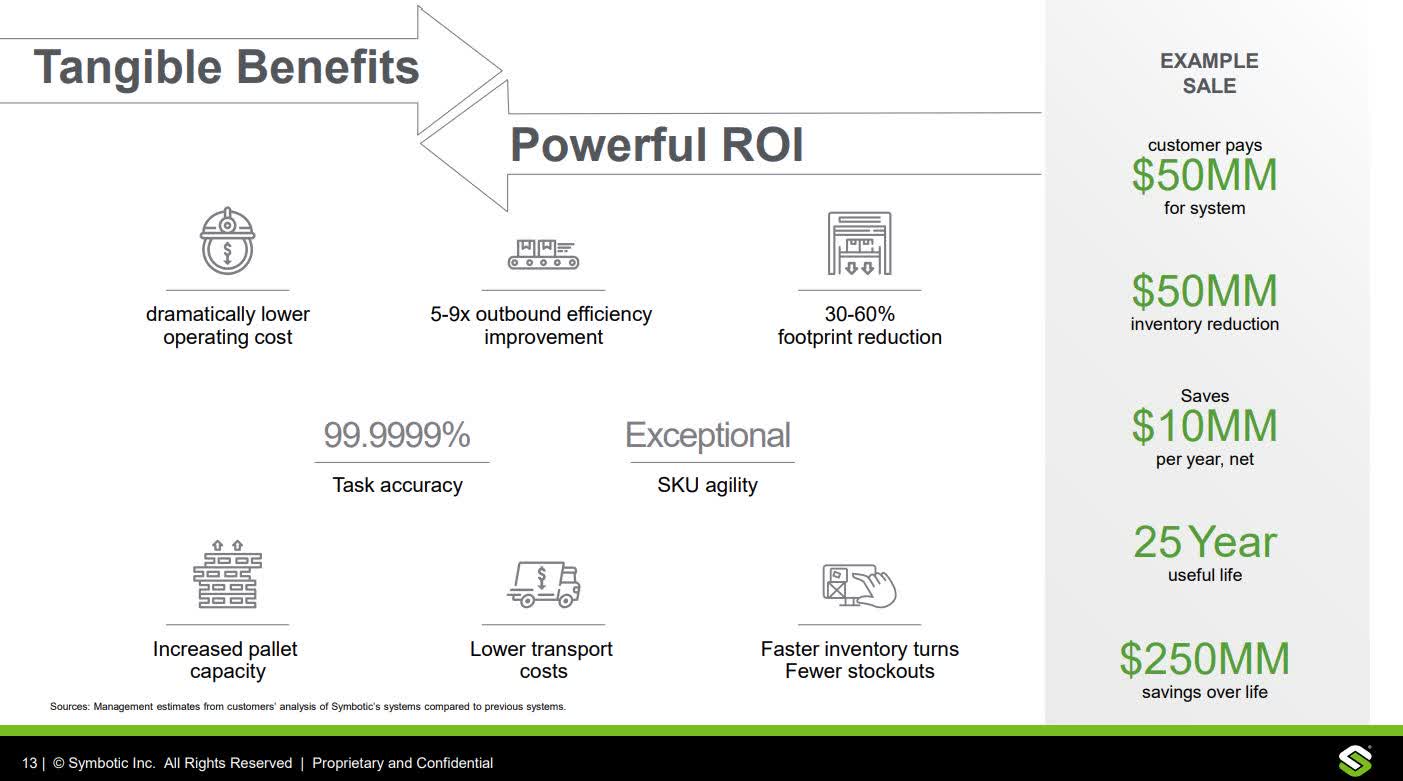

The advantage of this warehouse system is that it can maximize space usage, increase the speed of cases and items, reduce costs, be adaptable to changing product types, and reduce errors compared to warehouses using human labor and conveyor belts. The company's latest 10-K states, " The advantages of this approach are so compelling, as quantifiably measured by performance data in real world applications, that we believe our approach can become the de facto standard approach for how warehouses operate. "

Symbotic Investor Presentation

{kind=link}

Most of the tangible benefits of the image are self-explanatory. Increased outbound efficiency suggests faster order fulfillment, a key benefit for retailers. Dramatically lower operating costs mean a retailer can offer more competitive pricing and improve profitability. Speedier inventory turns mean a retailer can sell products and restock faster, improving inventory management and lowering the risk of running out of a product in high demand. Increased pallet capacity suggests better space utilization, potentially reducing warehouse footprint needs. However, the term "SKU agility" might be unintelligible for some. SKU is an acronym for "stock keeping unit," a unique identifier for a product. SKU agility means the ability to move a product anywhere quickly and easily. The above benefits likely played a role in Symbotic's warehouse system gaining fans such as Walmart ( WMT ) and Target ( TGT ), who are now customers.

The company has fundamentals that investors love

Symbotic grew fourth quarter FY 2023 revenue by 60% to $392 million and FY 2023 annual revenue by 98% to $1.17 billion. This top-line growth potentially increased investors' interest in the stock in 2023.

In the fourth quarter of FY 2023, the company produced $58.8 million in GAAP (Generally Accepted Accounting Principles) gross profits with a gross margin of only 15%. Annual FY 2023 GAAP gross profits were $189.74 million at a gross margin of 16%. I am not a huge fan of companies with a gross margin below 20%, which makes it challenging to achieve bottom-line profitability. The quarterly gross margin has flat-lined since the beginning of 2022. I would like to see a steady improvement in the gross margin. However, it would be wise to remember that this company is at an early growth stage with a limited operating history.

The company's Chief Financial Officer ("CFO"), Tom Ernst, explains the company's gross margins in the following way on the company's fourth quarter 2023 earnings call, " These results still reflect significant costs associated with lower margin innovation projects, the burden of pass-through costs to protect gross profit dollars, but that can weigh on a reported gross margin percentage and costs associated with rapidly scaling our operations. "

The good news is the company has structured most of its backlog on a cost-plus fixed-profit basis , which helps the company maintain its gross margin during times of high inflation or other events that could cause Symbotic's expenses to rise. In addition, its contracts with its most significant customers provide Warehouse Automation Systems with 15-year contracts for supporting software and maintenance services with no provision to terminate the contract outside of insolvency or an inability for Symbotic to deliver a product up to pre-defined standards. So, unless something drastically goes wrong, like technological disruptions, market shifts, or legal disputes, the company should be able to maintain gross margins in at least the mid-teens. However, for investors to see good returns from this company, the company will likely need to improve gross margins further.

Because the company is at such an early stage, the company prefers to talk about bottom-line profitability in terms of adjusted EBITDA (Earnings Before Interest, Taxes, Depreciation, and Amortization), which measures Symbotic's core operating profitability without one-time factors like restructuring costs and non-cash expenses like depreciation and stock-based compensation.

Symbotic produced fourth quarter FY 2023 EBITDA margins of 3.4%, up 400 basis points sequentially and 1400 basis points from the fourth quarter of 2022. The CFO attributed this rapid improvement in EBITDA margins to " rapid revenue and gross profit growth along with slower operating expense growth. " However, sustaining this rapid margin improvement might prove challenging in this uncertain economy and competitive environment.

Symbotic ended its FY with cash and short-term investments of $546 million against no long-term debt. It produced a 12-month trailing FCF of $209 million. CFO Ernst said the following about the company's balance sheet:

These [cash] balances increased almost $200 million over the past year, driven by the positive working capital benefit of our customer and vendor invoicing terms. We also had some timing benefits in 2023 to provide a tough comparison in the first quarter of 2024. Otherwise, we anticipate seeing a working capital expansion again for 2024.

Source: Symbotic Fourth Quarter FY 2023 Earnings Call.

Analysts and investors were pleased with the company beating top and bottom-line earnings estimates. The stock rose 40% in response to robust revenue growth and improved profitability.

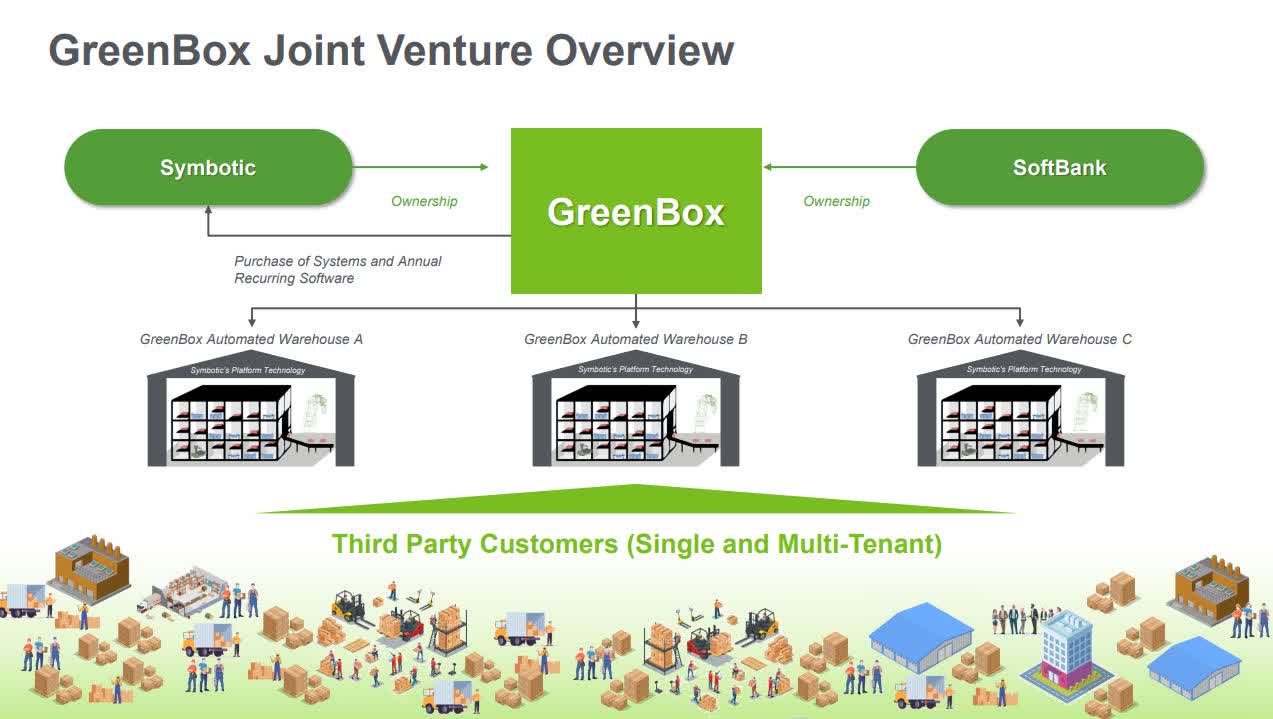

The company's Green Box initiative

Symbotic announced its new Warehouse-as-a-Service Joint Venture (JV) named Green Box with SoftBank ( SFTBY ) ( SFTBF ) on July 24, 2023.

Symbotic Investor Presentation.

{kind=link}

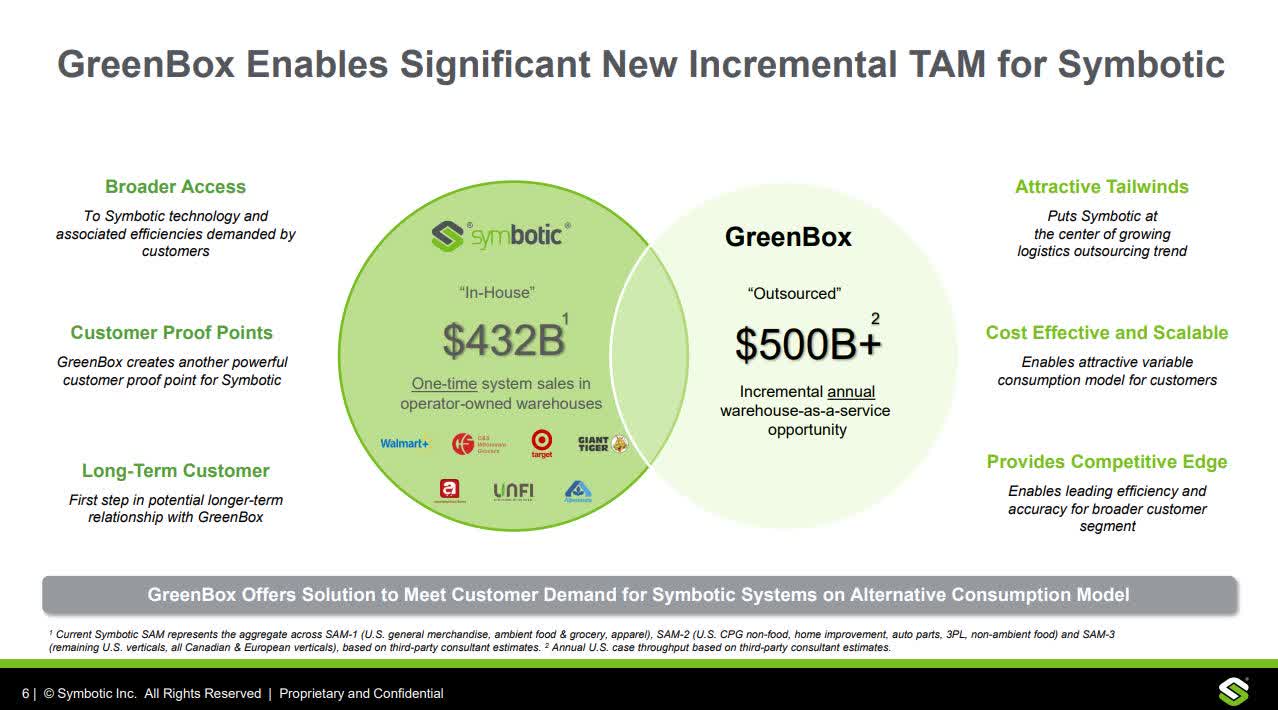

The GreenBox JV will offer warehousing services to third-party customers. Symbotic and Softbank own 35% and 65% of the JV respectively. In addition, the GreenBox JV also signed a $7.5 billion customer contract to buy Symbotic's warehouse systems. The company benefits from this JV arrangement in several ways.

Symbotic Investor Presentation

{kind=link}

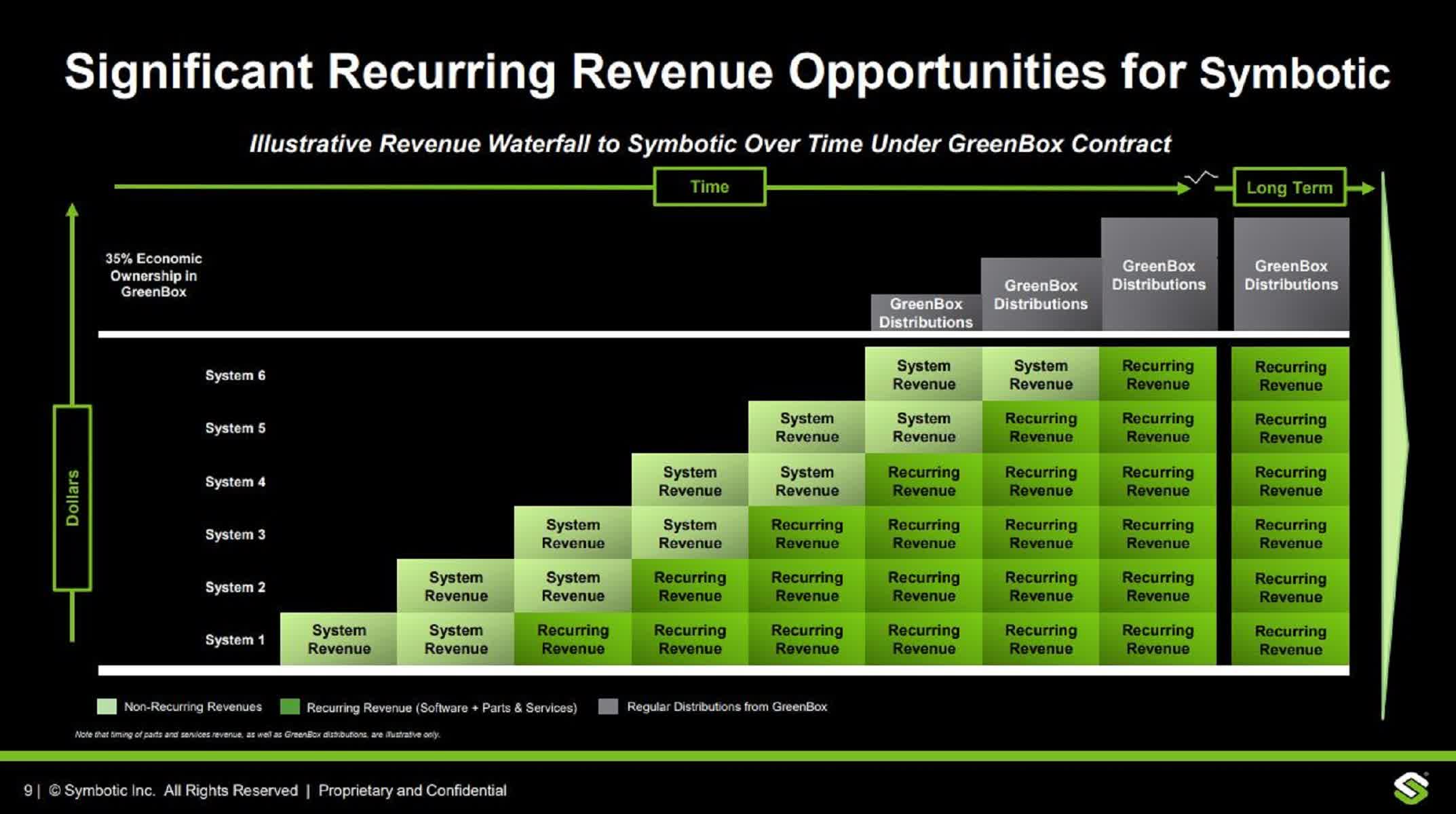

Over the longer term, its 35% economic interest will provide distributions from the JV. The boxes labeled System Revenue in the image above represent the income from its warehouse system's one-time sales (System One to System Six). The boxes marked recurring revenue represent ongoing income from services and parts sales. Over time, the company expects GreenBox to provide a high margin, $500 billion recurring revenue opportunity.

Symbotic Investor Presentation

{kind=link}

GreenBox potentially increases Symbotic's total addressable market, diversifies the business, improves margins, and moves the company away from a one-time sales model and towards a recurring revenue model. Suppose GreenBox achieves success; the company would become more attractive to investors, who may begin awarding it a higher valuation.

Risks

Not everyone likes this company. Symbotic has 21.52% of its float short, a high degree of bearishness in the stock. The company has several risks that investors should understand before considering an investment.

First, the company has massive customer concentration with just one customer. Symbotic stated in its 10-K:

Walmart, our largest customer, accounted for approximately 88% of our total revenue in the fiscal year ended September 30, 2023 and for a significant portion of our $23.3 billion backlog (as defined herein) as of September 30, 2023.

Source: Symbotic 10-K

Because of Walmart's importance, it could theoretically leverage its position to negotiate better contract terms over time, impacting Symbotic's margins. Although Symbotic's contracts with Walmart might include provisions safeguarding margins and limiting renegotiation frequency, Walmart's heavy customer concentration represents a risk that some investors may not ignore. Until Symbotic diversifies further, some investors may be reluctant to invest in it. Therefore, diversifying away from Walmart is in the company's best interests. Symbotic hopes its GreenBox initiative does a lot of the heavy lifting in diversifying its business away from Walmart. If GreenBox fails to gain traction, it could throw a monkey wrench in the company's plans to diversify, and Symbotic's revenue growth and margins may fail to increase as fast as management projects.

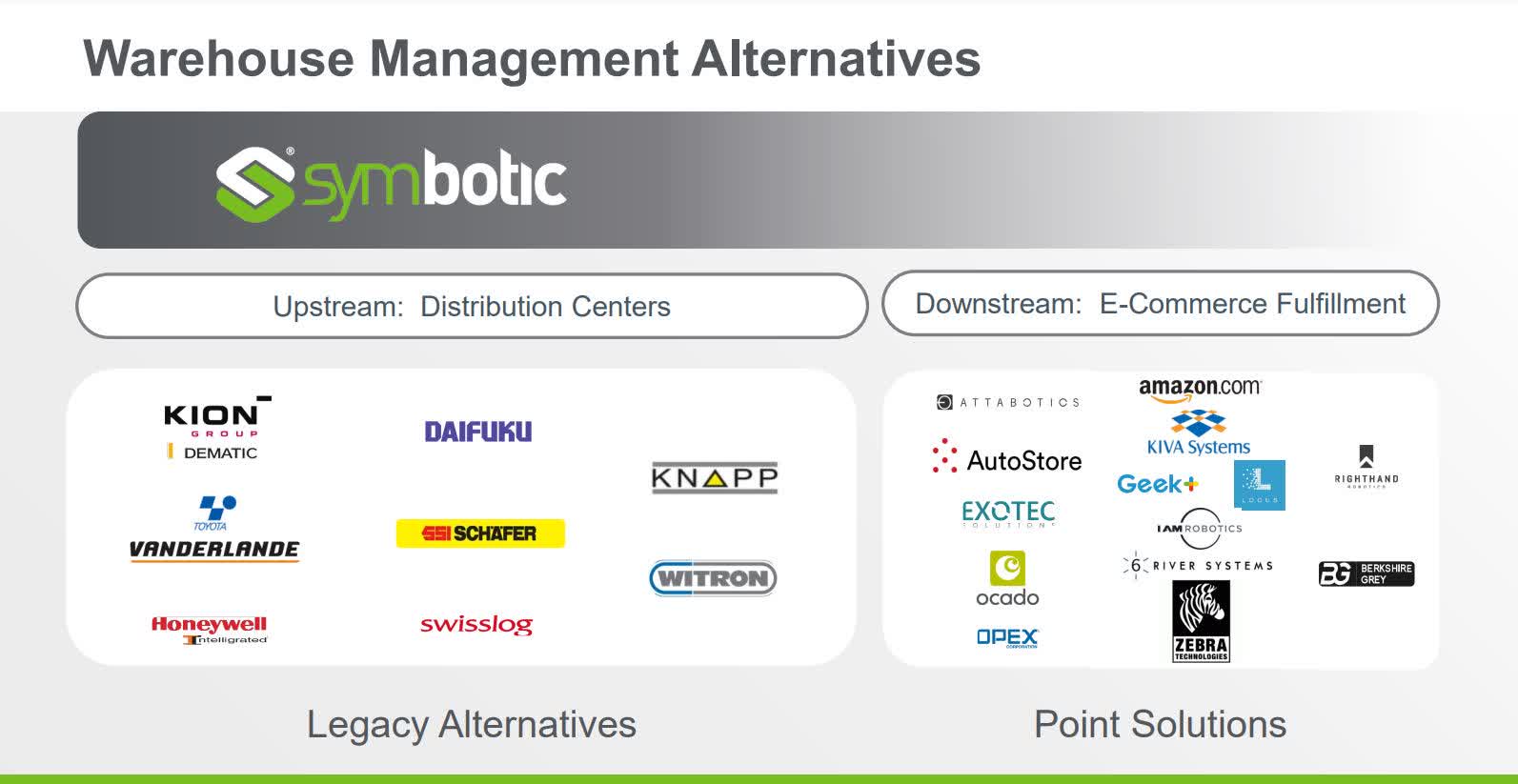

Next, although the company thinks it has the best warehouse solution in the market, it has many competitors, with some of the more prominent ones shown in the image below.

Symbotic Investor Presentation

{kind=link}

Symbotic doesn't consider many of the above companies as direct competitors. Some legacy alternatives focus on conveyor belt technology, and Symbotic believes its warehouse technology is superior to conveyor belts. Some of the other companies offer narrowly focused solutions that concentrate on e-commerce. For instance, Kiva Systems narrowly focuses on providing e-commerce solutions for Amazon ( AMZN ). However, although Symbotic management may downplay these companies as threats, they compete in similar enough markets that investors should not overlook them as potential threats. Additionally, as other companies observe Symbotic's success, copycat companies could arise, and Symbotic's ability to defend its patents could come into question. Further, the company acknowledges other competitive risks in its 10-K:

Our customers may also internally develop their own automated solutions for their warehouses and distribution centers. Our market may need further education on the value of automation solutions and our platform and products, and on how to integrate them into current operations. A lack of understanding as to how our automation platform and products operate may cause potential customers to prefer more traditional technologies or limited point solutions or internally-developed automated processes or to be cautious about investing in our warehouse automation systems and products. If we are unable to educate potential customers and change the market's readiness to accept our technology, then our business, results of operations and financial condition may be harmed.

Source: Symbotic 10-K

Last, although some experts believe the U.S. and other global economies can avoid a recession, we are not out of the woods yet. Some experts believe that inflation will remain persistently high and global growth will continue to slow. Slowing global growth could lead to reduced growth opportunities for the company. It could also negatively impact investor sentiment towards profitless early-stage companies like Symbotic.

It has a dual-class share structure

Symbotic entered the public markets via a reverse merger with a special purpose acquisition company (SPAC) in June 2022. The company has a dual-class share structure, with Class A shares representing the stock's public shares and trading under the SYM symbol. According to the company's registration statement S-1 , at the time of the merger, the company also issued " 60,844,573 shares of Class V-1 Common Stock and 416,933,025 shares of Class V-3 Common Stock, each of which is exchangeable, together with a New Symbotic Holdings Common Unit, into an equal number of Class A Common Stock. " Class V-1 and V-3 hold voting rights, with class V-1 getting one vote per share and class V-3 getting three, but they do not currently participate in Symbiotic's economic interests. Eventually, however, these Class V shares will convert to Class A shares, diluting current investors.

If you calculate Symbotic's price-to-sales (P/S) ratio only using Class A shares, its P/S ratio is 2.98 , making the stock look less expensive than it is when including V-1 and V-3 shareholders eventually participating in the company's profits and losses. If you calculate the P/S ratio with V-1 and V-3 shares included, its P/S ratio is 26.3 , which some investors might consider an excessive valuation.

Should you buy, sell, or hold?

Let's look at the company's reverse Discounted Cash Flow to see what today's stock price implies using a terminal growth rate of 3% and a discount rate of 10%.

Symbotic Reverse DCF

| The third quarter of FY 2024 reported Free Cash Flow TTM (Trailing 12 months in millions) |

| $209 |

| Terminal growth rate |

| 3% |

| Discount Rate |

| 10% |

| Years 1 - 10 growth rate |

| 34.5% |

| Current Stock Price (December 26, 2023, closing price) |

| $54.08 |

| Terminal FCF value |

| $4.171 billion |

The current stock price of $54.08 implies FCF will grow at 34.5% over the next ten years, an aggressive assumption. If you look at Seeking Alpha's measure of analyst consensus EPS estimates, there are exceedingly lofty expectations over the next three years.

GreenBox may not solely determine the company's success. Still, to validate the growth assumptions built into the stock's current price, the company needs GreenBox to succeed. If the GreenBox initiative meets the company's expectations, the market may justify today's aggressive growth assumptions. If GreenBox performs less than expectations, the market may consider the stock vastly overvalued at current prices. Additionally, investors believing in the potential upside of GreenBox heavily influence market sentiment surrounding Symbiotic. If GreenBox underperforms, market sentiment could turn decidedly negative against Symbotic.

If you don't already own Symbotic, avoid buying it at current prices, especially with the prospect of future dilution from class V owners converting their shares to class A over time. If you already own it and are playing the long game, the stock is worth holding on to for GreenBox's potential upside. I rate the stock a Hold.

For further details see:

Why Investors Should Be Cautious About Symbotic: A Critical Assessment Of This High-Flying Company