DB - Why Is Deutsche Bank Valuation So Cheap?

Summary

- Deutsche Bank has clearly improved its fundamentals and profitability in recent years, but its valuation remains depressed.

- Its sustainable ROE should be between 6-8% over the next few years, which justifies a higher P/BV multiple.

- The bank needs to increase investors’ confidence in its business prospects to support a re-rating of its shares.

Deutsche Bank ( DB ) continues to trade at a discounted valuation that doesn’t seem to be warranted, but needs to execute its strategy and show the market that is sustainable profitability is now much higher than it was in the recent past.

I’ve analyzed Deutsche Bank several times in the past , but my last article on the bank was some three years ago , thus I think it’s now a good time to revisit its investment case to see if its shares are undervalued right now or if it remains a value trap.

Over the past few years, Deutsche Bank has been on restructuring mode, executing on its business strategy presented back in 2019. While the bank has improved its fundamentals and has reached a much higher profitability than compared to some years ago. Despite this background, Deutsche Bank shares continue to trade at one of the cheapest valuations in the European banking sector, measured by its price-to-book value ratio of about 0.38x (vs. 0.83x on average for its closest peers).

As shown in the next graph, Deutsche Bank’s valuation has not changed significantly over the past five years, with the bank trading in a relatively narrow range of 0.2-0.5x book value, which can be considered a depressed valuation. Indeed, other banks with high exposure to investment banking activities, such as Morgan Stanley ( MS ) or Goldman Sachs ( GS ) trade at a premium to book value, while European banks with a similar business profile to Deutsche Bank trade between 0.5x-0.7x book value. The only exception is Credit Suisse ( CS ), which is currently trading at only 0.24x book value due to some specific issues.

{kind=link}

This cheap valuation can either mean that DB stock is currently undervalued by the market, which continues to value it unfairly like a low quality bank, or there are still some specific fundamental issues to fix that the market is worried about.

Business Strategy

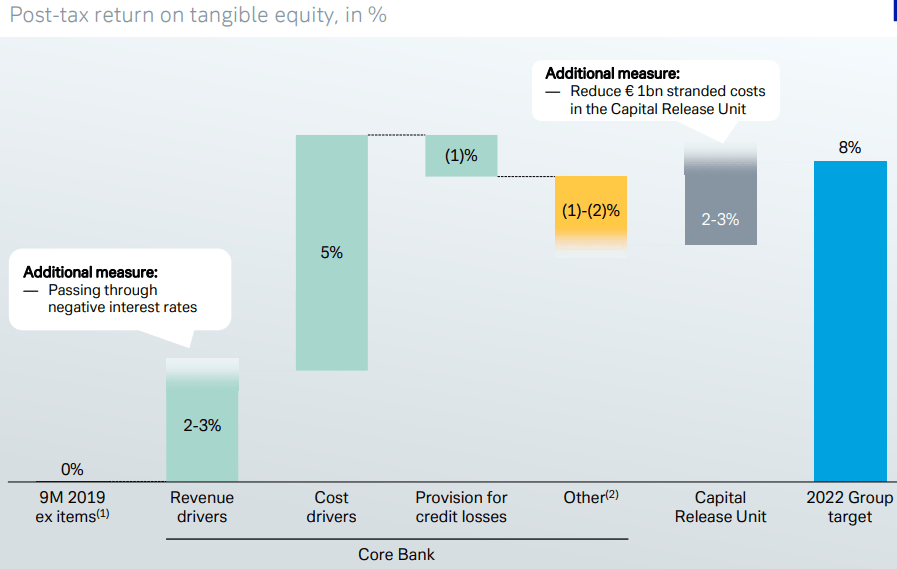

Deutsche Bank presented its last strategy update back in December 2019, aiming to improve the operating performance of the bank by scaling back from unprofitable activities, reduce its exposure to investment banking and grow other segments of the bank, such as corporate and private banking, plus improve profitability largely by cost cutting. In the next graph, it is represented the bank’s planned measures at the end of 2019, to achieve its return on tangible equity (RoTE) ratio of 8% by 2022.

{kind=link}

As can be seen, most of its planned profitability improvement was expected to be achieved through cost cutting, which is within the bank’s control, while revenue growth was not expected to be a huge contributor. This was a sensible strategy because revenue growth is largely outside of management’s control, as it depends largely on interest rates and customer’s activity levels, thus a strategy based on cost cutting was more likely to be ‘accepted’ by the market.

To reduce its annual expenses to about €17 billion by 2022, Deutsche Bank planned some 18,000 staff reductions, with the vast majority being planned in the investment banking division. However, of these planned reductions, actually only about 8,000 were executed over the past three years, as revenue growth in its investment banking ((IB)) segment was higher than expected.

Indeed, while Deutsche Bank’s strategy was to reduce its exposure to IB, this division accounted for about 37% of total revenue in 2022, remaining the bank’s largest segment, while in 2019 this division accounted for some 29% of its total revenue. This increase is justified by much better operating performance in activities related to capital markets in 2020 and 2021, which led to annual revenue growth of about 7% over the past three years, being its major growth engine, while in 2019 it was expected CAGR of only 2% in this unit.

Moreover, as interest rates also increased at a higher pace in the past twelve months than expected in 2019, its private and corporate banking segments achieved higher revenue growth than expected, leading Deutsche Bank to generate some €27.2 billion in revenue during 2022. This was above its goal of about €25 billion set three years ago, even though with a different mix than the bank was planning.

Revenue (Deutsche Bank)

While revenue was quite strong over the past three years and beat estimates several times during this period, on the other hand the bank’s track record on cost cutting was not impressive. While Deutsche Bank was targeting annual expenses of around €17 billion in 2022, it reported expenses of €19.9 billion. This is 17% above its target, which is explained, at least in part, by higher revenue growth than expected and the bank didn’t want to stop positive operating momentum in its investment banking.

Nevertheless, by missing its cost cutting target, Deutsche Bank also missed its efficiency ratio, as the bank was targeting a cost-to-income ratio of 70%, while it reported an efficiency ratio of 75% in the past year.

Cost to income ratio (Deutsche Bank)

While this is a clear improvement from very poor efficiency levels reported in the previous four years, Deutsche Bank is still one of the least efficient banks within its closest peers, with the exception of Credit Suisse that has reported very poor metrics in the past couple of years (cost-to-income ratio above 100%). Without considering Credit Suisse, the average efficiency level of its peers was close to 69% in 2022, showing that Deutsche Bank still has some work to do regarding its efficiency.

Despite not achieving its desired efficiency level, Deutsche Bank’s higher revenue than expected was enough for the bank to improve its profitability in a meaningful way. Its RoTE was 9.4% in 2022, above its 8% target defined in 2019, and it was the highest profitability level since 2011.

Group RoTE (Deutsche Bank)

Beyond an improved operating profile and higher profitability, Deutsche Bank also maintained a good capital position over the past few years and a conservative loan book profile, which is a strong backdrop for a potential economic recession in the coming quarters. At the end of 2022, its core equity tier 1 ratio was 13.4%, which is a good level, and not much different from what it was some years ago, showing that capital was not an issue when it presented its strategy back in 2019.

Capital (Deutsche Bank)

These improved fundamentals and profitability have enabled Deutsche Bank to resume dividend payments and share buybacks in the past year, while in the previous couple of years it had suspended capital returns to shareholders. This is another positive sign that its restructuring program was successful, even though capital returns were relatively small, but is a positive step and Deutsche Bank can now shift its focus from business overhaul to provide an improved shareholder remuneration policy.

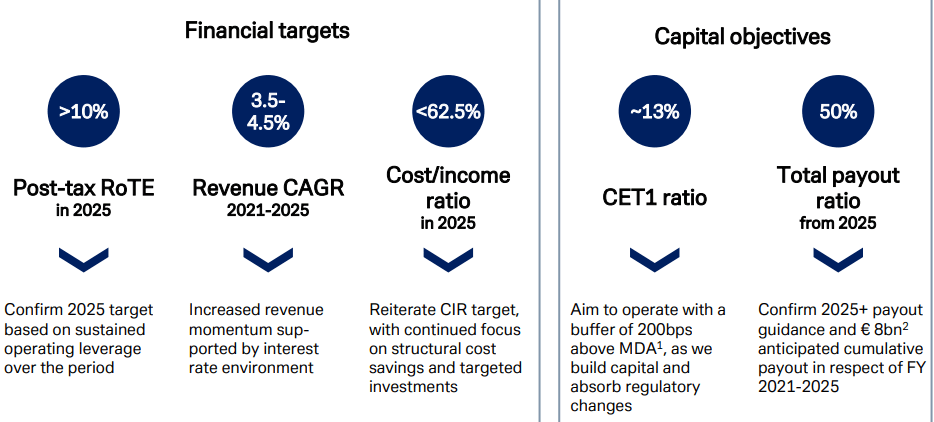

Going forward, the bank is expected to update its business strategy at the beginning of next month, but its strategy and goals shouldn’t be much different from what the bank has been communicating, namely continue to increase profitability by achieving some revenue growth and cost cutting, and distribute a good part of its earnings to shareholders over the coming years.

{kind=link}

Valuation

While the bank has clearly improved its fundamentals over recent years, and its future business prospects are stronger than in the past, its shares continue to trade at a significant discount to its closest peers and the average of the European banking sector.

I think this happens because after so many years of poor profitability and costs due to past misconduct, investors continue to be skeptical about Deutsche Bank’s sustainable earnings in the future. The fact that Deutsche Bank achieved its financial targets set in 2019 through a different path than planned also doesn’t help, especially regarding cost cutting, an area where it has clearly failed to reach its target.

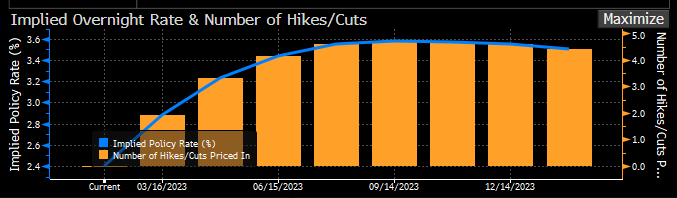

Moreover, the benefit of higher interest rates may be temporary given that the current hiking pace from the European Central Bank ((ECB)) is not certain to continue over the coming months. Market expectations are for a few more hikes in the short term, but with inflation already decelerating and the possibility of a recession in Europe ahead, the market is expecting the deposit rate (currently at 2.5%) to peak at 3.5% by mid-2023, and stay at that level thereafter.

{kind=link}

This means that Deutsche Bank should continue to benefit from higher interest rates over the coming three or four quarters, but further gains after that may be difficult to achieve. With economic activity slowing down and individuals and corporates being squeezed by rising borrowing and energy costs, default rates are likely to go up in the short term leading to higher loan-loss provisions, impacting negatively the bank’s bottom-line.

Taking into account this background, it is not surprising to see that street estimates are somewhat downbeat, given that Deutsche Bank’s revenue is expected to be €28 billion in 2023 (+2.9% YoY) and €28.7 billion in 2024 (+2.5% YoY), while its net income is expected to be €4.17 billion (-17% YoY) in 2023 and €4.7 billion in 2024 (-6.5% vs. 2022). Due to lower earnings expected over the next couple of years, its return on equity ((ROE)) ratio is expected to be 6.4% in 2023 and 7.1% in 2024 (vs. 8.4% in 2022).

Therefore, 2022 is expected to be an outlier year regarding profitability, and considering market estimates for the next two years, its average ROE for the period 2021-25 is only 5.1%. Note that I’m not counting 2019 and 2020, which were very weak years for the bank and would decrease even further its average ROE.

Using the Gordon growth model to value its shares, and assuming a cost of equity of 11% and ROE of 5.1%, its deserved P/BV multiple is 0.36x. This is in-line with Deutsche Bank’s current valuation, showing that Deutsche Bank’s discounted valuation is warranted.

However, as business prospects have improved and the bank is likely to report a higher ROE in the near future than compared to its history, assuming a ROE of 7.3% (its average during 2022-25E), this yields a deserved P/BV ratio of 0.58x. This would lead to a fair value above €17 per share, or an upside potential of close to 50% compared to its current share price.

Conclusion

Deutsche Bank is one of the cheapest banks within the European banking sector, and compared to its investment banking peer group, a valuation that is justified by its historical performance, but not by its potential ‘sustainable’ profitability in the near future.

If the bank can increase the market’s confidence in its business prospects, its shares seem to be undervalued, while downside at current levels appears to be low at its discounted valuation, making it a good value play within the banking sector right now.

For further details see:

Why Is Deutsche Bank Valuation So Cheap?