CUR - Why It's A Mistake To Confuse Gold As An Investment Opportunity

2023-11-07 12:31:01 ET

Summary

- Gold prices are currently high, nearing their all-time high price achieved in May of this year.

- Central banks' continued accumulation of gold has contributed to its recent surge in prices.

- Investing in gold as a short-term strategy to combat inflation or as a store of value during times of uncertainty may be logical, but I believe long-term investment in gold will underperform the market.

As anybody who is experienced in finance can testify, money takes many different forms. Throughout history, the things accepted as money have varied materially, and even, to some extent, that remains true to this very day. The island of Yap , for instance, still uses round stone discs with holes in them that they call Rai for money, or the Trobriand Islands where yams are used as currency. But perhaps no form of money has been more famous throughout history than gold. It's shiny and does not blemish, it's permanent unless destroyed, and it's easy to verify as legitimate. Although the days of individuals transacting regularly in gold are long gone and never coming back, there are many investors, speculators, and financial institutions alike, that like gold because of the safety they believe it offers.

While the word 'safety' is somewhat loaded, and the true stability of gold can be debated, nobody can deny that the recent surge in prices for it has piqued the interest of many. Between all of the geopolitical issues occurring in places like Ukraine, Israel, and Gaza, not to mention political infighting here in the US, worries about inflation globally, rising interest rates aimed at combating that inflation, and more, it's no wonder why so many have flocked to the precious metal.

While its primary use in the past may have been as a form of money, it has become something far larger over the years. It is perceived as a store of value. It's used in electronics and jewelry. And it is used heavily by central banks to promote the stability of their own currencies. When combined with the aforementioned uncertainties of this world, it has also become a major tool for financial speculation. I would argue that investors who are approaching gold from any sort of investment or speculative angle should view it as one of many tools in their arsenal in order to preserve value in their portfolios when times are rocky. I would discourage individuals from investing significant amounts of money into gold as part of a long-term strategy aimed at generating strong returns.

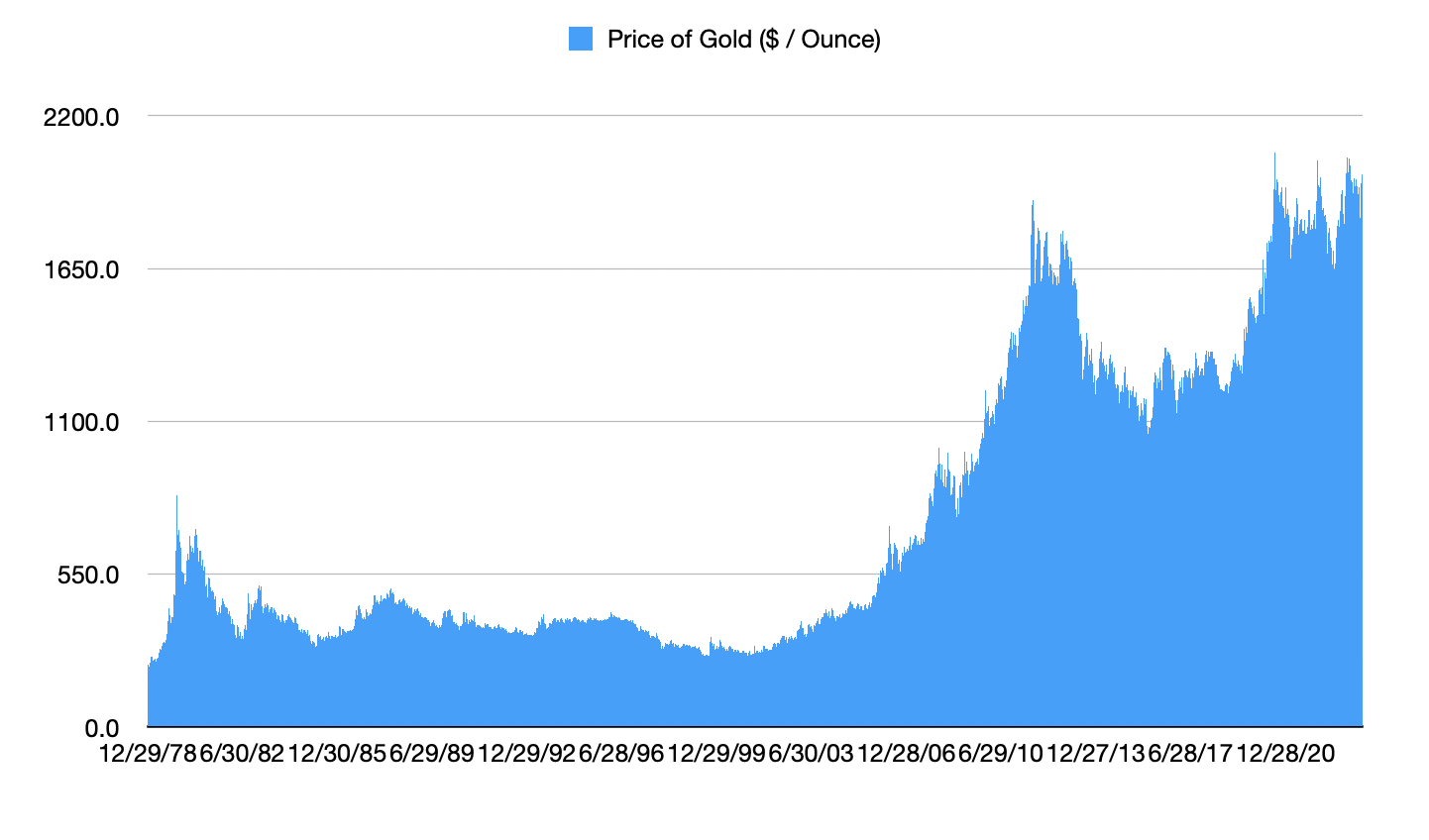

Gold prices are high right now

As of this writing, gold is going for a little under $2,000 per ounce. That places it within striking distance of its all-time high price of $2,080.72 per oz that was achieved in early May of this year. The fact of the matter is that, over the past year, the precious metal has generated quite a high return, with prices skyrocketing 19.4% over this window of time. The S&P 500 has also done quite well during this window, but it is up a more modest 15.6%. It's truly impossible to peg down every reason why prices are climbing. But it's undeniable that one of the most significant contributors to its appreciation in recent months has been the continued accumulation of it by central banks.

{kind=link}

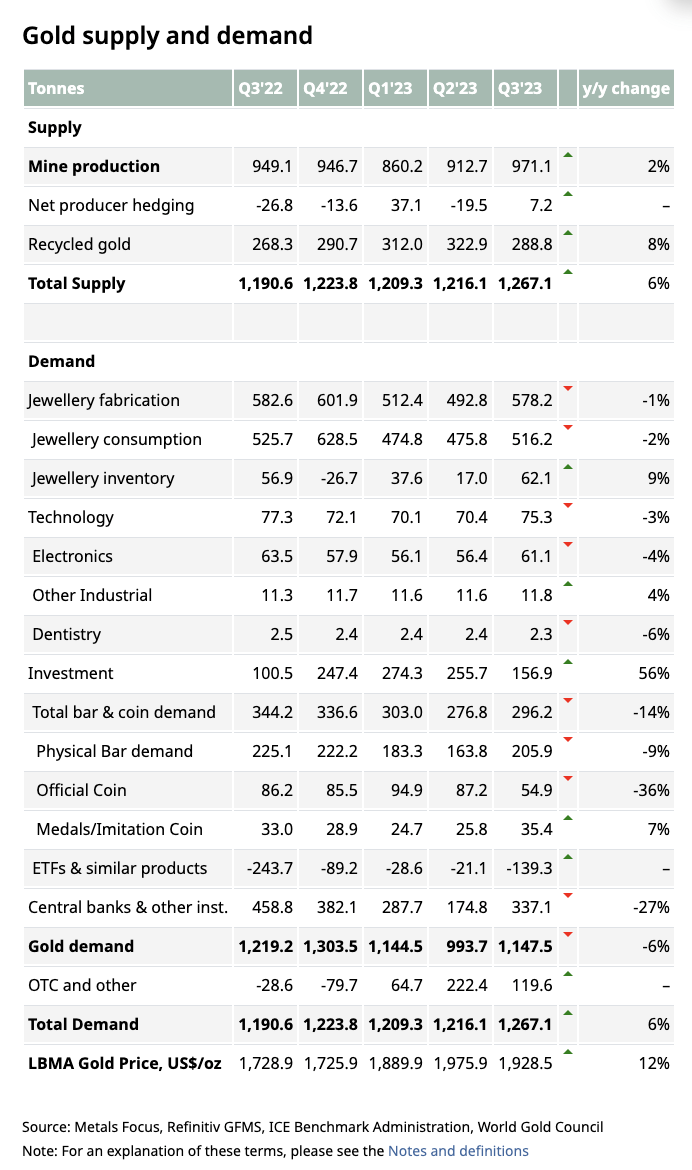

In late January of this year, the World Gold Council predicted that, while demand for gold in general would likely be positive this year, central banks would probably see a pullback in demand relative to what was seen back in 2022. The organization predicted that demand from central banks would be between 200 tons and almost 900 tons less than it was the year prior. The midpoint was 600 tons. While this may seem unrealistic when you consider that central bank demand for 2022 totaled 1,135.7 tons, it's worth noting that that number represented an all-time high and it was significantly higher than the 450.1 tons reported one year earlier. That surge was driven by broader economic uncertainty because of rising interest rates and high inflation, as well as by geopolitical issues. But alas, this projection would turn out to be incorrect. And that's because, according to the same source , gold purchases by central banks totaled 799.6 tons in the first nine months of this year. That represents a 14% increase year over year.

{kind=link}

This is not to say that supply is not rising. Because it is. In fact, it looks as though this year might represent an all-time high for mine production. But of course, as can be expected, mine production levels can be lumpy. For instance, in the third quarter of this year, output from mines was only about 2% higher than what it was at the same time last year. In order to fill that gap, recycled gold came into the picture with a year-over-year increase of almost 8%. This makes sense because, as gold prices rise, people become more willing to recycle jewelry, electronics, and other products. And year over year in the third quarter, prices for gold were up around 12%.

This all paints an interesting picture that, to me, shows that strong central bank purchases are proving to be instrumental in pushing prices higher. Central banks, understandably so, are using gold to promote stability. As for investors, the big question is what course should be taken. Gold for investment purposes has seen some rather mixed results. Gold ETF outflows, for instance, have now exceeded inflows for six quarters in a row. Though bar and coin investment has been up year over year. But even that can be rather lumpy. Total investments in gold in the third quarter, for instance, came in around 56% higher than they did at the same time last year.

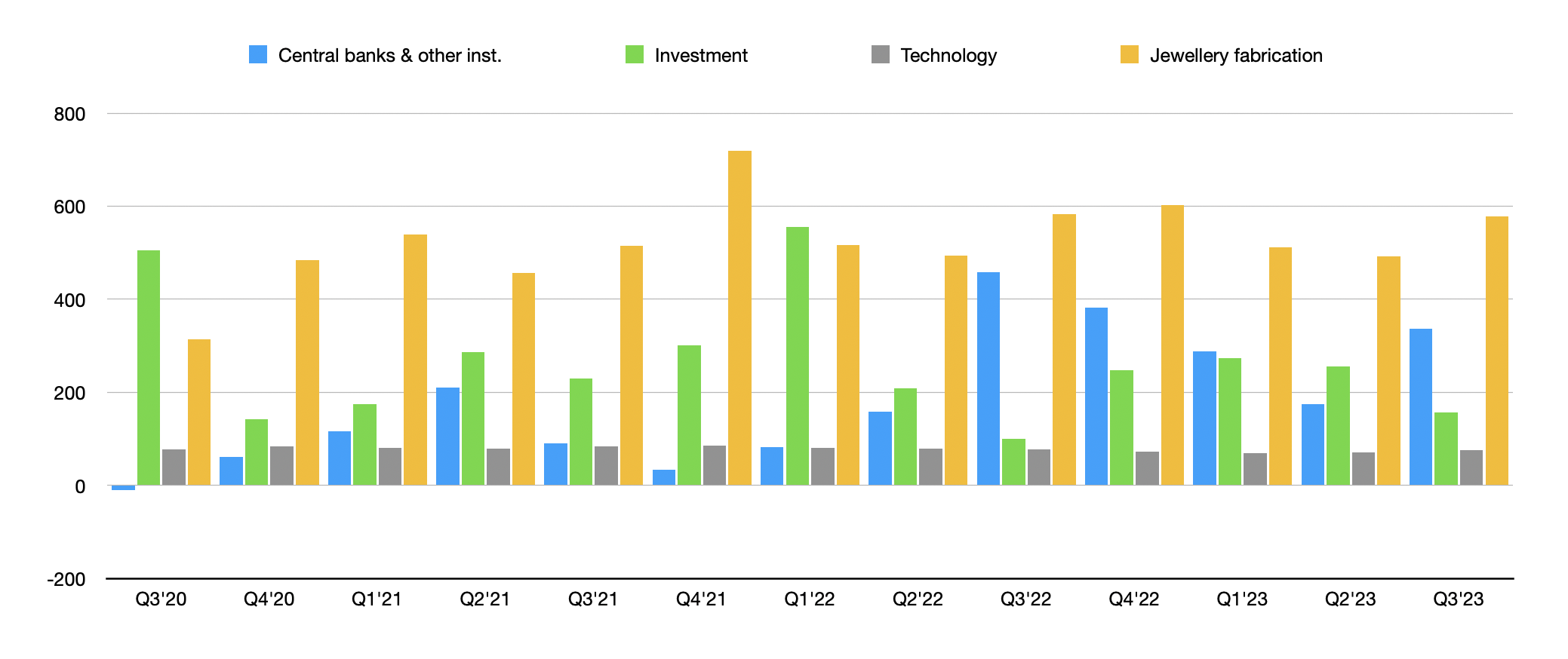

Author - World Gold Council Data

{kind=link}

*Demand in Tons

In the first chart above, you can see gold demand on a quarterly basis covering from the third quarter of 2020 through the third quarter of this year. It looks at each of the four major sources of demand. This chart is a little messy, however, because of the large volume that's used for jewelry fabrication. As you can see in the second chart, jewelry fabrication levels have been largely consistent, with the exception of a brief dip in 2020. Stripping that source out, we end up with a revised version of the first chart as shown below. Technology use has also been fairly consistent in the grand scheme of things. So the real changes in demand have largely stemmed from central banks and variations in gold demand associated with investment purposes. What's interesting is that, with the exception of a brief window of time in 2020 and 2021, higher prices have largely been correlated with higher demand from the combination of these two sources of gold demand. And while gold demand for investment purposes has weakened some, the demand from central banks has really counteracted this.

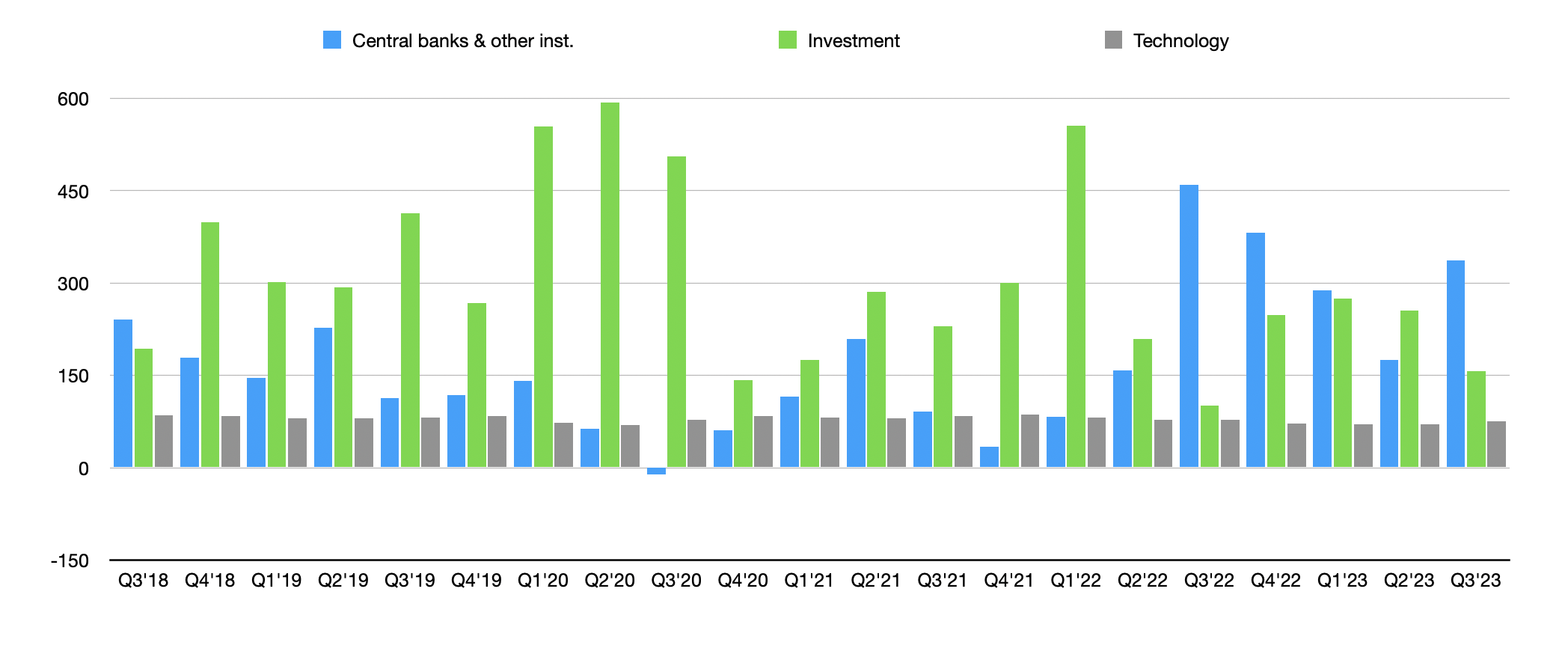

Author - World Gold Council Data

{kind=link}

Gold data is rather peculiar because, in order to match supply and demand, there is a category in the data that refers to over-the-counter and other sources. I liken this to a plug in the data. And what's interesting about this is that, if we exclude this from the equation and we ignore recycled amounts of gold to only focus on mining production, then the global demand growth rate has outpaced the global supply growth rate by an aggregate amount between 2018 and 2022 of 7.6%. If we include recycled gold supplies into this equation, then this expands to 8.2%. Keep in mind, I am not talking about overall demand and supply. Rather, I'm referring to the aggregate growth rates of each over time.

What this tells me is that high amounts of demand are largely caused by central banks or at least partially responsible for why prices have moved up. This doesn't tell an investor whether they should or should not buy into gold. The question boils down to whether demand will remain robust or not. For those who believe that inflation will come down in the not-too-distant future, which we have already seen evidence of to a limited extent, then demand from central banks might also weaken.

As part of a short-term strategy aimed at combating inflation or as a store of value during geopolitical uncertainty, it stands to reason that investors betting on gold in the same way that central banks do would be logical. Investors who do have concerns about the state of the world today might be wise to include some gold in their portfolio as a means to protect against the unknown. There are two big examples that I could point to regarding gold as a means of hedging against risk during times of tremendous volatility. In 2008, when it looked as though the world was falling apart, the S&P 500 plunged in value by 36.6%. That same year, gold increased in price by 4.3%. More recently, in 2022, when the S&P 500 plunged 18%, gold inched up by 0.4%. Anybody who thinks some sort of economic catastrophe is on the horizon might be wise to use gold as a store of value during such times.

{kind=link}

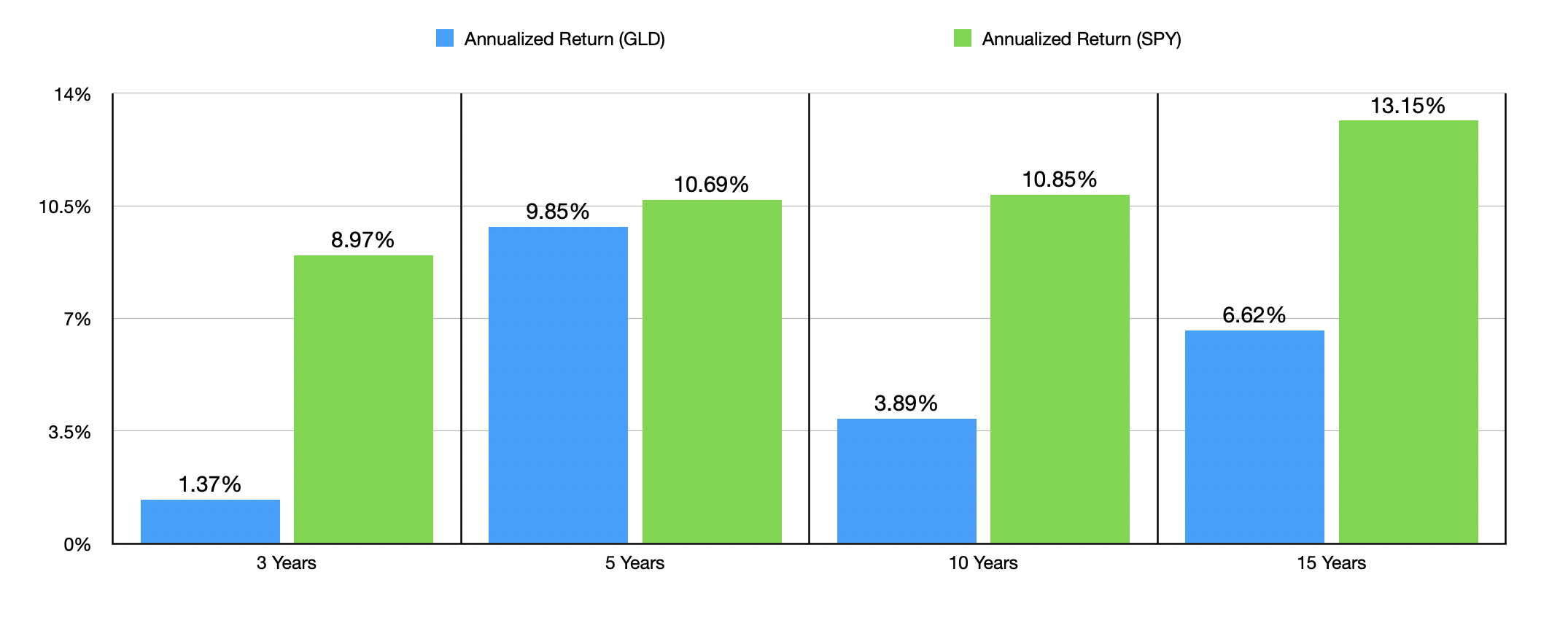

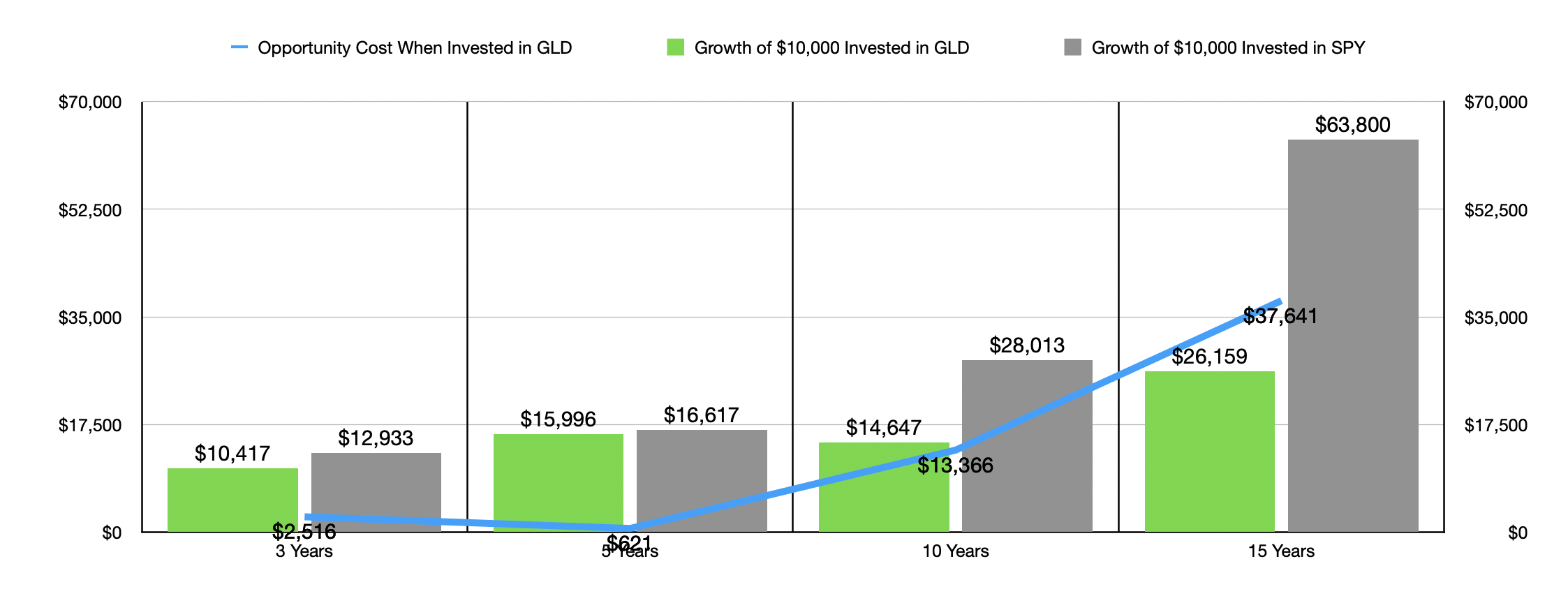

But there's a big difference between betting on gold in a short-term or strategic capacity and betting on it in the long run. This is because, historically speaking, there have been far better places to allocate capital. Looking back to the S&P 500, for instance, it becomes apparent, really fast, why somebody would prefer to invest in the market more broadly. Using the SPDR Gold Shares ETF ( GLD ) as our proxy for gold and SPDR S&P 500 ETF Trust ( SPY ) as our proxy for the S&P 500, we can see how, in the chart above, the market has outperformed gold over the past 3, years, 5 years, 10 years, and 15 years on an annualized basis. Because of the aforementioned economic uncertainty, the returned disparity over the past five years has been much smaller by comparison. But even in that window of time, by investing in gold, somebody putting in $10,000 would have missed out on $621 in appreciation. But even in that case, the overwhelming chunk of the strong returns that gold experienced came over the span of only two years. Over the past three years, the S&P 500 has averaged 8.97% per year compared to the 1.37% annualized returns seen by gold. And as the chart below illustrates, the dollar amounts missed out on over time by investing in gold over the S&P 500 can become rather significant.

{kind=link}

Takeaway

Personally speaking, I am a huge fan of gold. But I am less a fan of investing in it and more a fan of appreciating it. The fact of the matter is that gold prices have risen rather significantly as of late. The recent upswing seems to be the cause of robust buying from central banks that took the industry by surprise. For investors who believe that continued economic uncertainty will be the name of the game and/or who are worried about geopolitical issues, having some stake in gold might not be a bad idea. As part of a longer-term investment, however, I would take a more cautious approach. Unless you need guaranteed stability on an inflation-adjusted basis, holding any significant amount of the precious metal would be ill-advised. If you have some belief that issues will arise on a global or national scale, it is a good strategic tool for your portfolio. But any other approach will result in you significantly underperforming the market over the long haul in my opinion.

For further details see:

Why It's A Mistake To Confuse Gold As An Investment Opportunity