CAT - Why Net Zero Is So Bullish For Caterpillar

Summary

- In this article, we start by discussing why global mining is the key to the world's push for net zero technologies.

- All trends point to massive material shortages and significant mining underinvestment, requiring hundreds of billions of additional spending in the industry.

- Caterpillar is in a fantastic spot to benefit from these developments for decades to come, thanks to the replacement cycle, new innovations, and billions in expected additional spending.

Introduction

It's time to talk about Texas-based machinery giant Caterpillar ( CAT ) . Earlier this month, I wrote an article mentioning Caterpillar as a great dividend growth stock to buy during a recession sell-off. In this article, we're going well beyond that, as we need to talk about both cyclical and secular trends impacting the yellow producer of heavy equipment.

In October, I wrote an article discussing Caterpillar's position in the trend for net zero. Since then, Caterpillar shares are up 40% as investors have recognized that the company is more than a cyclical machinery play.

Caterpillar is quickly becoming one of the most important players in the net zero supply chain, impacting the chances to decarbonize global economies. Mining equipment demand is expected to soar for decades to come as the entire trend for green energies is now dependent on our ability to mine metals. It's truly as dramatic as it sounds.

Even better, Caterpillar itself is investing in new technologies, working on major deals with the world's largest miners.

The only thing that bothers me is that I haven't aggressively added to my investment before it took off.

In this article, we'll discuss all of that and more.

So, buckle up, as there's a lot to discuss!

A Net Zero-Induced Commodity Super Cycle?

On Seeking Alpha, we regularly discuss macroeconomic developments, as I try to make that the cornerstone of most of my research.

In some cases, we discuss extremely important developments that will impact our lives and portfolios in a major way - often on a long-term basis.

The (forced?) trend towards net zero emissions is one of them. For example, the Paris Climate Agreement, signed by 196 nations, aims to reduce greenhouse emissions by roughly 50% by 2030.

Personally, I have my doubts when it comes to the human influence on our climate. However, that doesn't matter as one thing is clear: governments around the globe are pushing hard for environmental measures. This includes subsidies for electric cars, solar panels, and wind power, and penalties for pollution through carbon pricing and other measures.

One can imagine what this means for supply chains as the world is "suddenly" changing an organic trend in energy demand that started before the industrial revolution.

It means one thing: a much higher need for metals.

My friends at Kailash Concepts used a very fitting example in one of their most recent white papers on this very issue. They used the example of hybrid mobility. Toyota explained that three hybrid vehicles cut the same carbon output as one electric car. This could mean that electric cars are 3x "cleaner". Right?

In other words, 18 million hybrids cut the same direct pollution as 6 million electric cars.

The problem is that the battery materials needed to produce 18 million hybrids would produce just 260 thousand electric vehicles. In other words, hybrids are 70x more material efficient.

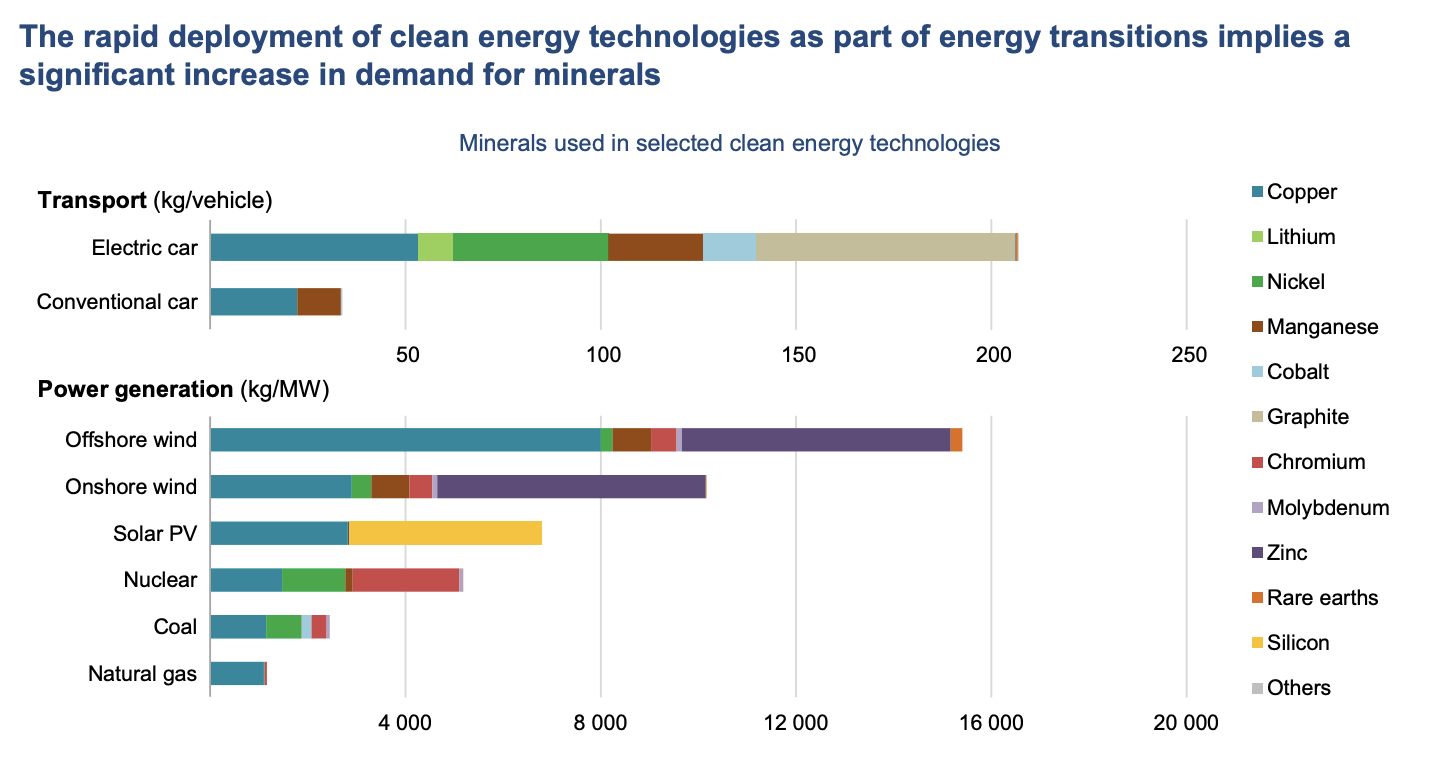

To give you another example, a conventional car uses between 18 to 49 pounds of copper - depending on its size. A hybrid car uses a bit more (roughly 85 pounds). A battery-electric vehicle uses more than 180 pounds of copper. Anything bigger than that creates exponential copper demand.

Copper.org

In light of what we are about to discuss next, it's interesting to mention that Ford ( F ) hiked the price of its electric F-150 Lighting from roughly $40,000 in 2021 to $56,000 in December 2022.

The International Energy Agency ("IEA") published a 287-page report in 2021, outlining the impact of the energy transition on critical minerals.

The head of the IEA hit the nail on the head when he explained how important materials are in this transition endeavor:

Today, the data shows a looming mismatch between the world’s strengthened climate ambitions and the availability of critical minerals that are essential to realizing those ambitions [...] - Fatih Birol

Or to put it differently, the success of the energy transition relies on our ability to mine an efficient amount of metals and minerals.

The IEA estimates that an electric car needs more than 200 kilograms of minerals, including copper, nickel, manganese, and a lot of graphite. The difference compared to a conventional car is truly stunning.

{kind=link}

As the numbers above show, it doesn't end there. "Renewable" technologies like on/offshore wind and solar need loads of critical minerals like copper and zinc. This also excludes steel. Up to 80% of wind turbines consist of steel and concrete.

As one can imagine, this creates a big surge in expected material demand.

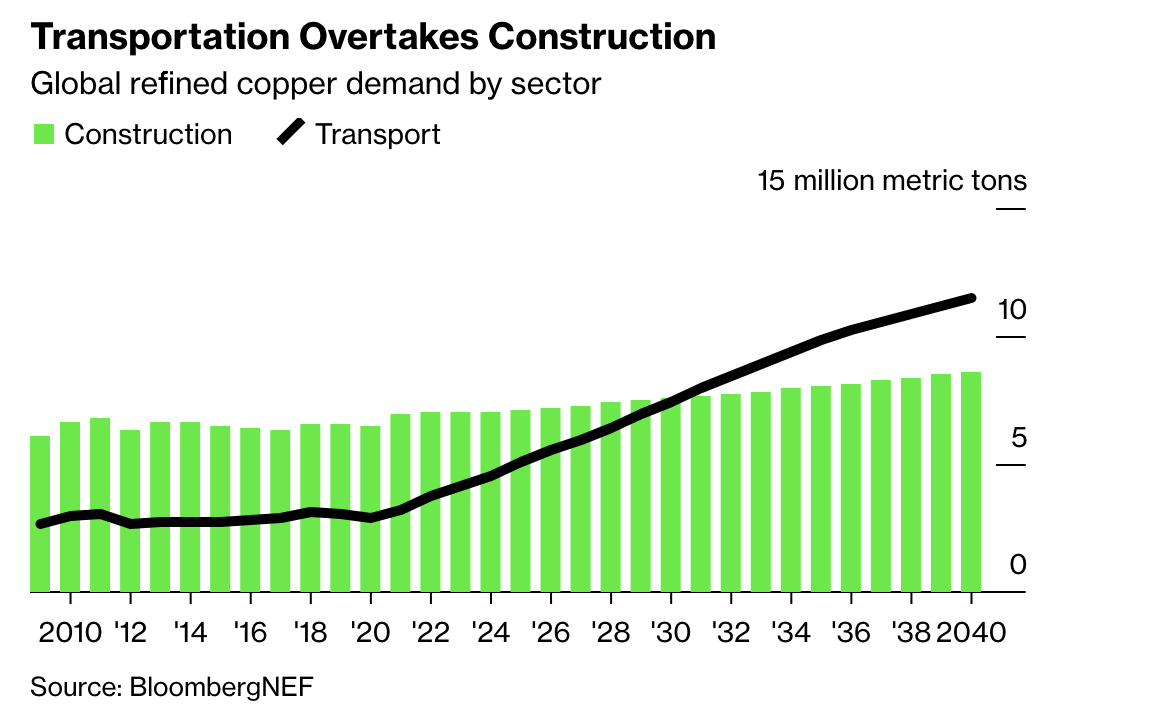

Between 2021 and 2040, annual copper demand is expected to grow by 53% to almost 40 million metric tons.

{kind=link}

Moreover, transportation demand for copper is expected to outpace construction demand in less than eight years. This underlines my comments regarding the metal intensity of the EV transition. Car companies will increasingly compete with construction companies for key input metals like copper.

{kind=link}

The biggest issue is that even if everyone agrees that we need to invest billions in mining, we won't be able to quickly grow supply.

According to a September Bloomberg article:

Commodities experts have been warning of a potential copper crunch for months, if not years. And the latest market downturn stands to exacerbate future supply problems — by offering a false sense of security, choking off cash flow and chilling investments. It takes at least 10 years to develop a new mine and get it running, which means that the decisions producers are making today will help determine supplies for at least a decade.

“Significant investment in copper does require a good price, or at least a good perceived longer-term copper price,” Rio Tinto Group Chief Executive Officer Jakob Stausholm said in an interview this week in New York.

The supply situation is actually pretty bad. It is estimated that global mine supply growth will peak in 2024 as new projects are in the works and existing sources dry up. In such a scenario, the world could see a historic copper deficit of as much as 10 million tons in 2035.

It also doesn't help that the quality of mined copper ore is declining. In 1900, the copper grade was 2.0%. In 2000, it was 1.0%. In 2030, it is expected to be 0.5%.

Miners will likely have to spend $150 billion in the next decade to solve an 8 million-ton deficit problem. Again, $150 billion!

The Bloomberg article I just mentioned also includes a comment from Goldman Sachs, which believes that the price of copper needs to be at least $9,000 per ton to get miners to invest. This is also due to high inflation, causing mining costs to surge. This would imply that copper prices need to rise at least another 12%.

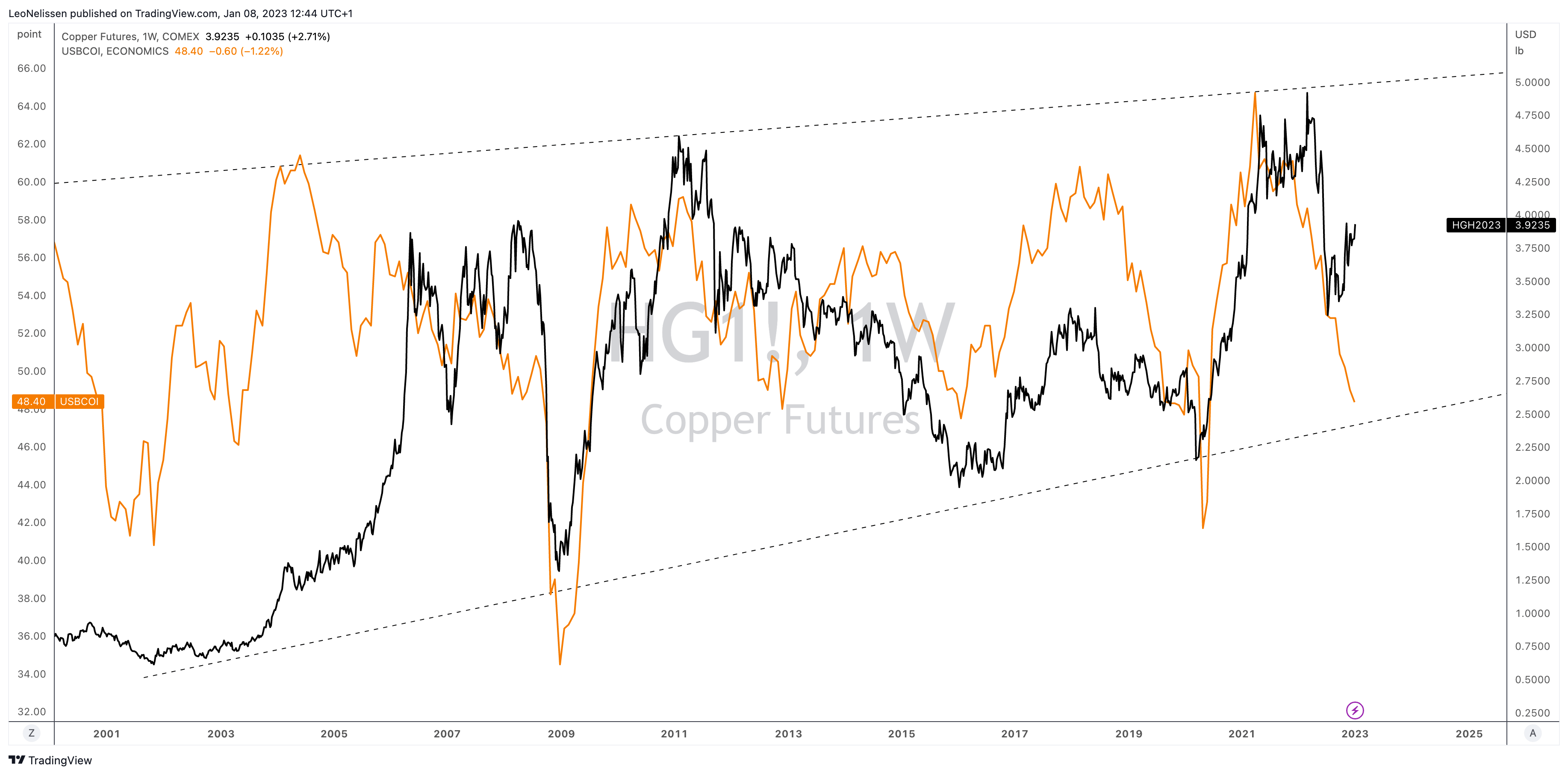

So far, copper prices have held up very well despite rising pressure from a slowing global economy. As the chart below shows, copper prices usually perfectly follow the ISM manufacturing index (orange line). This time, however, copper is strengthening again without the supper from economic expectations.

TradingView (Copper, ISM Index)

{kind=link}

The following chart shows that mining inflation has truly exploded. This is the result of higher fuel and labor costs, more expensive equipment, geopolitical risks, and legal issues.

Costmine

Moreover, as we already briefly discussed, capital expenditures need to accelerate meaningfully as real CapEx in the mining industry has been subdued for many years.

Twitter (@stockjock84)

As a percentage of GDP, it's even worse.

Crescat Capital, Bloomberg

With all of this in mind, I believe that Caterpillar is one of the best long-term investments to benefit from the forced push for net zero.

Caterpillar Is A Fantastic Net Zero Play

Texas-based Caterpillar has a $129.5 billion market cap and a $249 stock price while I am writing this. After last week's strong finish, the company is now trading at an all-time high, rising 3.9% year-to-date and 13% over the past 12 months.

The CAT ticker has outperformed the S&P 500 by 30 points over the past 12 months. Including dividends, the company has outperformed the stock market since the commodity peak of 2011, that's a fantastic performance as it includes more than 10 years of technology and growth stock dominance, which benefited the S&P 500 tremendously.

Interestingly, CAT has consistently beaten the market. Despite COVID, supply chain issues, strong growth stocks (like FANG) benefiting the market, the 2015 commodity crash, and so much more, CAT is generating serious alpha as the table below shows. The only issue is that CAT's standard deviation (volatility) is high with values consistently above 30%.

{kind=link}

With all of this said, Caterpillar is technically a commodity proxy. The company's stock price is highly correlated to the price of copper. However, while the correlation is high, Caterpillar tends to outperform during both commodity bull and bear markets. This is based on its ability to deliver value. This includes paying a steadily rising dividend and buying back shares. A commodity is unable to do these things for obvious reasons.

TradingView (CAT, Copper)

Moreover, it needs to be said that the commodity business isn't even a huge part of CAT's total business.

These are the company's third-quarter results per segment:

- Total 3Q22 revenues: $15.6 billion (16.2% operating margin)*

- Construction: $6.3 billion (19.3%)

- Resource Industries: $3.1 billion (16.4%)

- Energy & Transportation: $6.2 billion (15.1%)

*I excluded inter-company segment eliminations. Technically, sales are $15.0 billion.

Resource Industries accounted for roughly a fifth of total revenues, which is a lot, but not enough to make CAT a pure-play mining stock.

The reason why CAT is still a commodity proxy is that its other segments are also highly correlated to commodity prices. The Energy and Transportation segment is driven by energy prices and the need for transportation (highly cyclical). The same goes for construction.

It also helps that the company is seeing strength across the board. This includes pricing power in a time of shortages and high material prices. The short overview below shows year-on-year sales and operating profit growth per segment (as of 3Q22).

- Construction: sales +19%, operating profit +40%

- Resources: +30%, +81%

- Energy & Transportation: +22%, +32%

According to Morgan Stanley (as reported by Seeking Alpha ):

The upgrade to the machinery industry comes as investors contemplate how billions of dollars in federal spending on infrastructure will be allocated. In addition, the Inflation Reduction Act of 2022 signed by President Biden in August provides incentives for renewable energy projects. The law also offers credits for mining materials such as aluminum, lithium and graphite used to make batteries for clean-energy storage.

The company's backlog increased by $1.6 billion in the third quarter to $30 billion. Caterpillar also commented on the impact of the energy transition, which is favorably impacting its Resource Industries segment. According to the 3Q22 earnings call :

[...] our mining customers continue to exhibit capital discipline. However, commodity prices remain supportive of continued investment despite trending lower recently. We expect production and utilization levels will remain elevated, and our autonomous solutions continue to gain momentum.

Moreover

We expect the continuation of high equipment utilization and a low level of park trucks, which both support future demand for our equipment and services. We continue to believe the energy transition will support increased commodity demand, expanding our total addressable market and provided opportunities for profitable growth. In heavy construction and quarry and aggregates, we anticipate continued growth in the fourth quarter.

Going Green While Winning New Business

One of the things investors asked me about is Caterpillar's move to invest in Lithos Energy .

{kind=link}

Headquartered in San Rafael, California, the company specializes in designing, engineering, and building shock-resistant and high-performance battery solutions for applications like off-road vehicles.

"Caterpillar's collaboration with Lithos supports our commitment to delivering robust electrified products and solutions for our customers," said Joe Creed, group president of Caterpillar's Energy & Transportation segment. "Cat ® equipment – regardless of its power source – is designed to operate in the most demanding conditions. Lithos' experience manufacturing battery packs for similarly demanding environments will be an asset as we continue our electrified product development."

I wouldn't make the case that this is groundbreaking news. However, it is a step in the right direction and yet another move that makes Caterpillar a more powerful player in an industry that not only drives net zero efforts but also incorporates net zero itself.

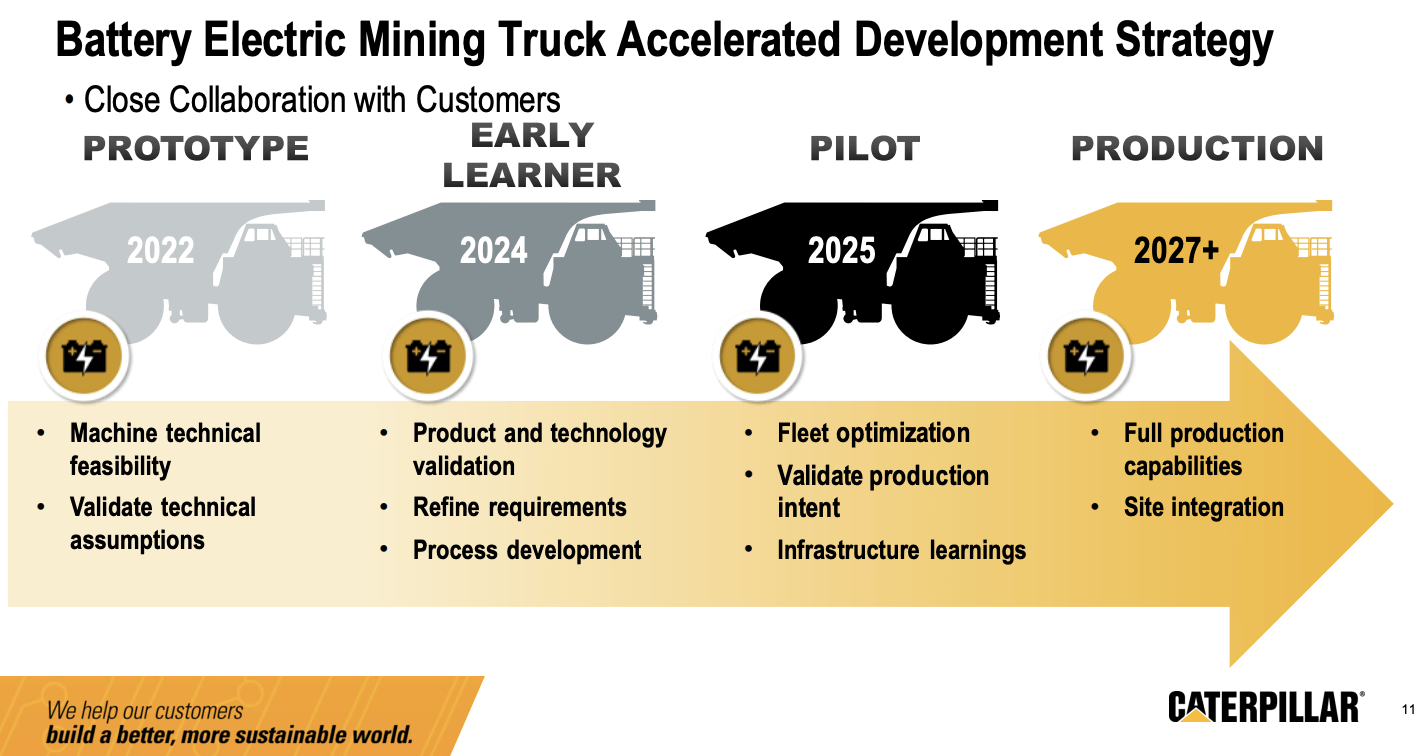

Caterpillar is working on gaining market share by offering electric mining trucks. In 2025, the company is expected to implement its first pilot projects before it moves to big-scale production after 2026.

{kind=link}

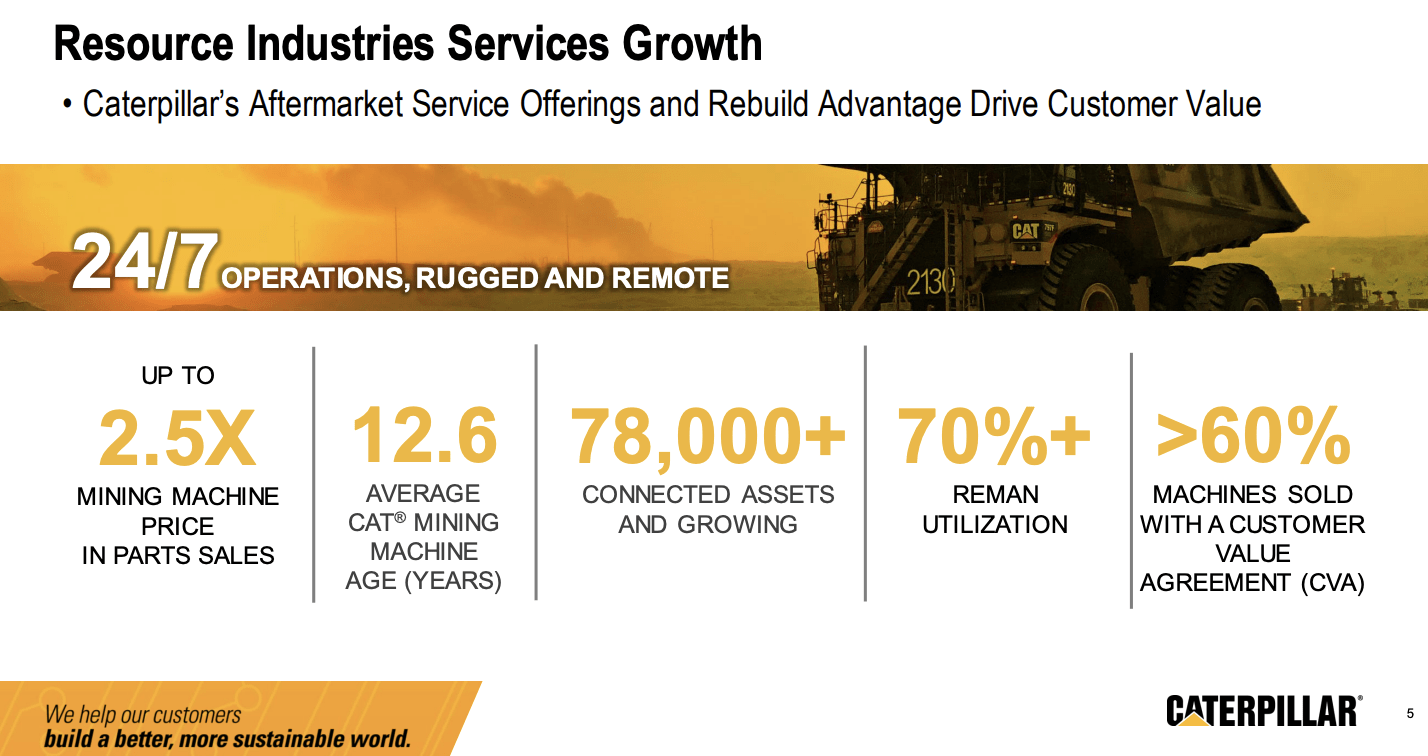

Caterpillar is also investing in autonomous mining options, to lower labor costs and improve 24/7 mining operations for customers.

The company has worked on autonomous alternatives for more than 25 years and solutions for oil sands customers, iron ore, copper, gold, coal, and lithium miners. The company has 155 million kilometers of autonomous driving experience, which is 2x more than the biggest car manufacturer.

These developments are expected to trigger customers into making new major investments. Especially because mining equipment has aged quite a bit over the past decade when commodity prices were low. As we already saw, mines have rapidly reduced CapEx.

The average CAT mining machine is now almost 13 years old.

{kind=link}

A lasting surge in commodity prices is poised to trigger a long-term replacement cycle.

In light of this discussion, the company is winning big deals with major customers. CAT will replace BHP's entire haul truck fleet at its Escondida Mine in Chile, the world's largest copper mine. Old vehicles will be replaced with 160 new CAT 798 AC electric dry haul trucks. Deliveries will start this year and extend over 10 years.

According to Caterpillar :

The new electric drive trucks will feature technology that delivers significant improvements in material moving capacity, efficiency, reliability and safety. The agreements allow BHP to accelerate the implementation of its autonomy plans by transitioning the fleet to include technology that enables autonomous operation. In addition, the agreement set forth a path for BHP to meet its decarbonization goals through the progressive implementation of zero-emission trucks.

Valuation & Risk/Reward

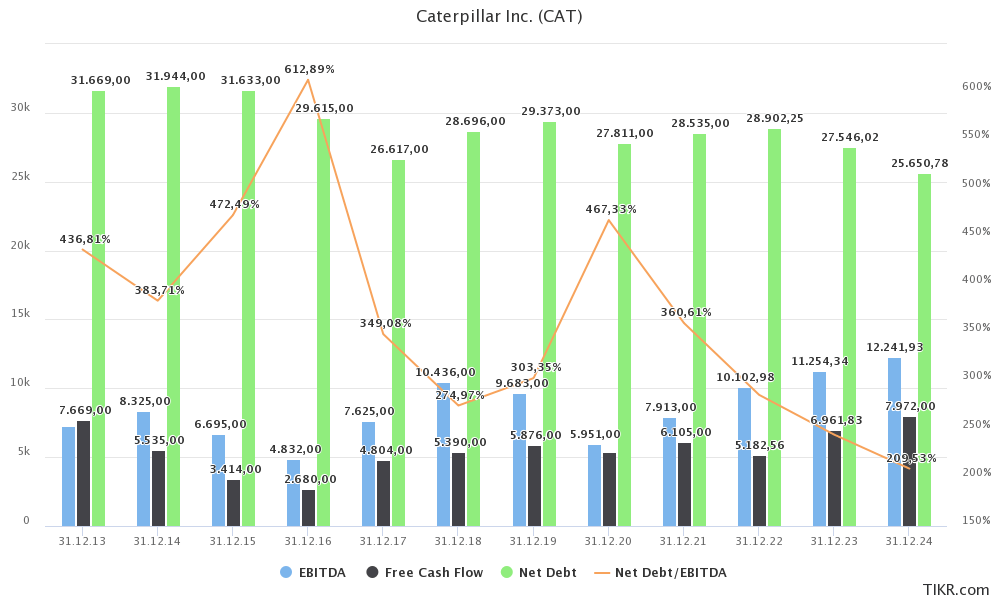

What's also highly interesting - in light of elevated recession risks - is that analysts do not expect Caterpillar's financials to weaken. The only thing expected to come down is net debt. net debt is expected to fall to less than $28.0 billion in 2023. That would imply a net leverage ratio of 2.4x, which is very low (healthy). The company has an A-rated balance sheet.

Adjusted EBITDA is expected to rise to $11.3 billion in 2023, with free cash flow rising to $7.0 billion. That would imply a 5.3% free cash flow yield, which supports the company's 1.9% dividend yield and 9.0% average annual compounding dividend growth over the past ten years.

{kind=link}

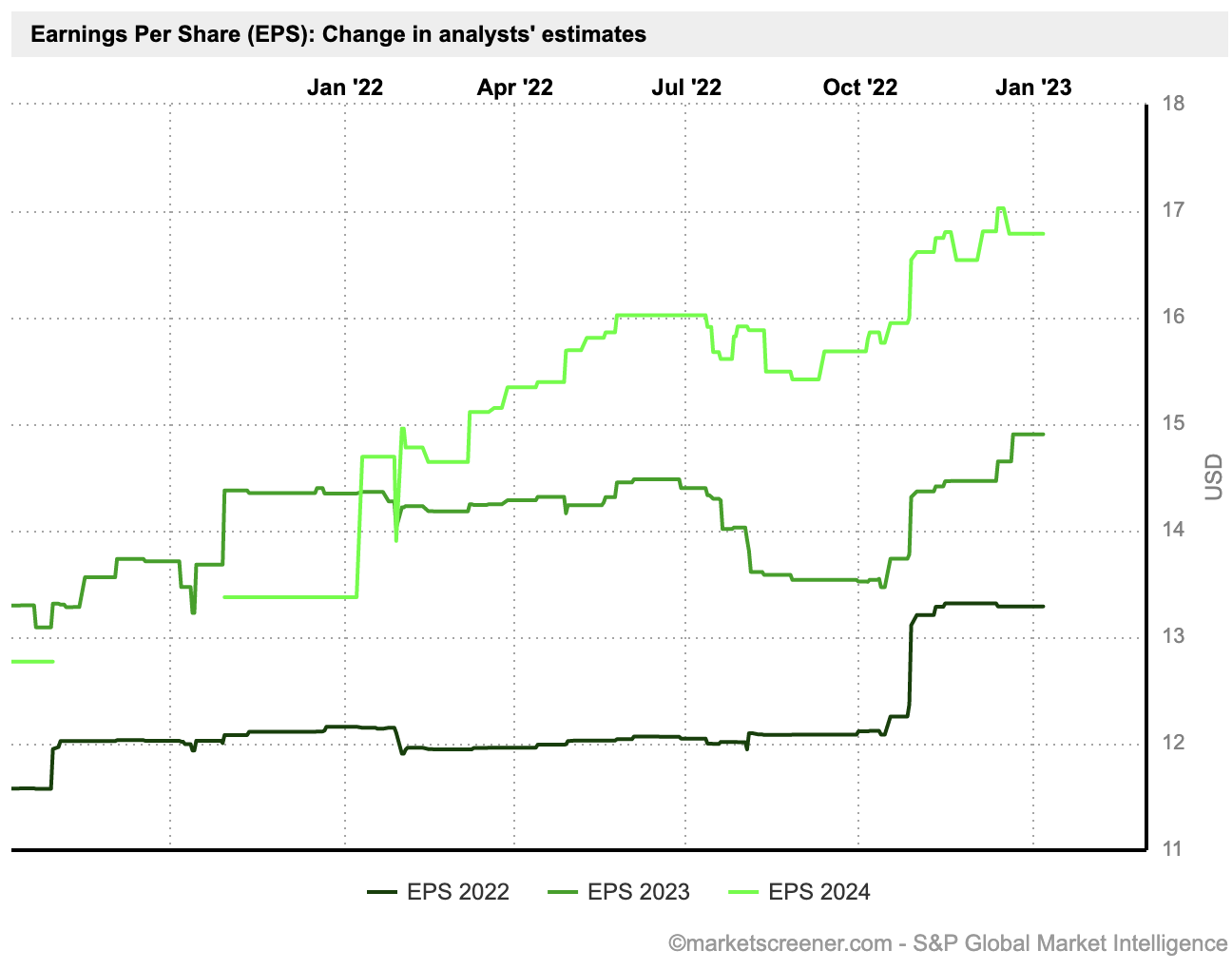

With that said, analysts aren't stupid. They know the global economy is very likely to enter a recession. A lot of industrial stocks we have discussed over the past few weeks have been subject to outlook revisions.

Caterpillar's EPS outlook, however, has not been lowered. Analysts have revised their estimates for 2022, 2023, and 2024 higher over the past four months as the overview below shows.

MarketScreener, S&P Global Market Intelligence

{kind=link}

Using 2023 EBITDA estimates of $11.3 billion, we find that CAT shares are trading at a 14.3x multiple. This is based on its $162 billion enterprise value, consisting of its $129.5 billion market cap, $27.5 billion in expected net debt, and $5.0 billion in pension-related liabilities.

This valuation is very fair. CAT is far from being overvalued.

However, I am trying to buy the stock as close to 12x EBITDA as possible. Back in October when I turned bullish (before CAT surged 40%), I was unable to increase my CAT exposure as I bought other cyclical stocks.

FINVIZ

Needless to say, I'm still trying to buy (much) more as I am very bullish on a long-term basis. Given economic developments, I believe that the market will give us another opportunity in 2023.

So please be aware that we could see some drawdowns, despite my bullish outlook.

Takeaway

Caterpillar remains one of my all-time favorite dividend growth stocks. While we didn't really discuss the dividend aspect in this article, we did discuss long-term tailwinds, which I believe are extremely important.

The ongoing energy transition is entirely dependent on the world's ability to mine metals and minerals. Years of subdued commodity prices, environmental standards, and underinvestment have caused a scenario where we're dealing with expected material shortages, risking derailing any plans to reduce global pollution.

Caterpillar is in a good spot to benefit from high pent-up demand, a prolonged replacement cycle, and strong pricing power for decades to come. The company can use its already large footprint in the industry, innovation, and deep customer ties to gain market share and grow its business well beyond its Resource Industries segment.

Given that I do have CAT exposure and the high likelihood of a recession, I am closely watching the CAT ticker to buy any 20% correction we might encounter this year.

(Dis)agree? Let me know in the comments!

For further details see:

Why Net Zero Is So Bullish For Caterpillar