CRGY - Why Occidental Petroleum For Warren Buffett

2023-04-11 16:45:35 ET

Summary

- Warren Buffett, through Berkshire Hathaway Inc., increased his holdings of Occidental Petroleum Corporation yet again.

- Berkshire Hathaway needs a large company to "move the needle" for its investors. This limits potential investment targets.

- Investors can win from Anadarko optimizations and a return to more historical valuations from currently cheap industry valuations.

- Fiscal year 2022 accelerated the deleveraging strategy.

- The benefits of the Anadarko acquisition may take a while to become apparent to the market.

(Note: This article was in the newsletter on March 29, 2023.)

Warren Buffett of Berkshire Hathaway Inc. ( BRK.B ) made the news when he again purchased more shares of Occidental Petroleum Corporation ( OXY ). There are investors wondering why he would purchase more shares of Occidental Petroleum when there are so many cheap alternatives in the industry.

One of the easy answers is that he needs a target large enough to "move the needle" for his investors. The industry is loaded with cheap buys. Many of those cheap stocks, though, are not large enough to be significant for an investor like Warren Buffett. Instead, he is restricted to larger companies that do not mind a large generally passive shareholder.

He not only looks at things like assets, but he also reviews management succession plans. So not only does the business have to prosper, but plans have to be made for the business to do well into the future.

Occidental is not only doing well now, but the Anadarko acquisition may uncover additional value in the future that is not obvious to the market currently. Much has been made of the fact that Occidental outbid Chevron Corporation ( CVX ) for the assets. But the difference in the winning bid from the last Chevron bid is not all that much percentage wise.

The unexpectedly good fiscal year 2022 gave Occidental some time to actually clean up the balance sheet much faster than expected. Large acquisitions often take time to outperform and live up to expectations. The logistics of such a big acquisition almost predetermine such an outcome. A simple example would be that all the wells producing at the time of the acquisition do not "all of a sudden" begin to outperform simply because the ownership changed.

What is far more likely to happen is that new operations put into place will likely ensure new well outperformance going forward. But it will take time for new operations to have an effect on an acquisition that large.

Therefore, Occidental profitability is likely to improve for years because of the Anadarko acquisition (rather than one large profitability jump). The cyclical nature of the business makes it a bit hard to become apparent to the average shareholder because profitability will likely be greater at different oil prices throughout the industry cycle. This is something that is more likely to be measured by management in detail rather than easily apparent to the market.

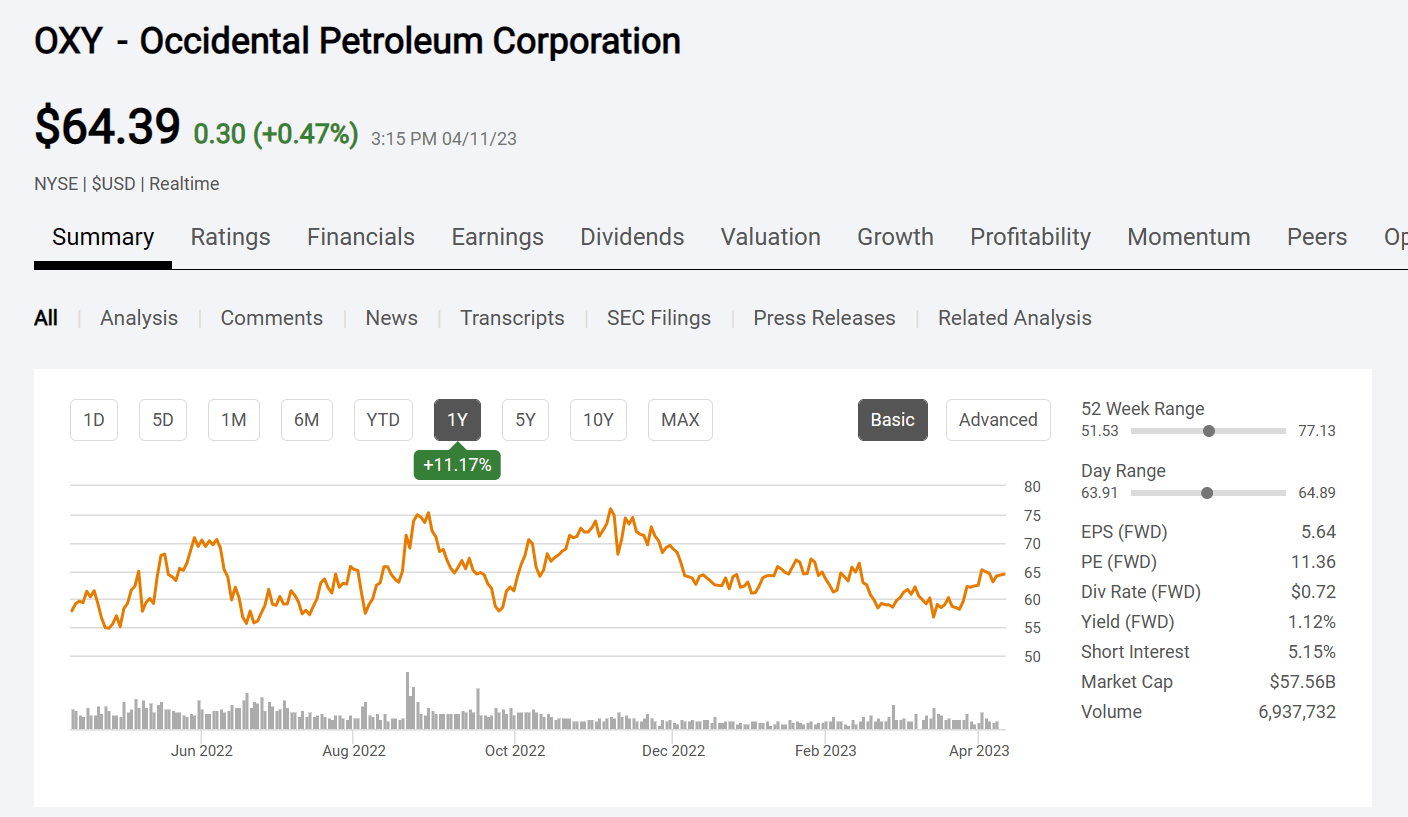

Occidental Petroleum Common Stock Price History And Key Valuation Measures (Seeking Alpha Website April 11, 2023)

{kind=link}

The other thing that is every bit as important is that the market collapsed the price-earnings ratios (or valuation) of these companies when fiscal year 2020 became the latest disappointment in a series of disappointments beginning with the big oil price decline in 2015. Therefore, the rather decent fiscal year of 2022 was not valued as highly as cyclical earnings tops of the past years.

This led to a lower peak common price as shown above compared to the historical peak prices. Now admittedly, unconventional is not growing as fast as it did in the past. Plus, the outlook for the industry is more cyclical than one of growth. Still, the valuations throughout the industry are cheap compared to just about any historical measure you may choose.

As shown above, the stock has quite a ways to go to get back to the high prices achieved before the start of 2015. That valuation gap is likely to narrow over time. Industries regularly go into and out of favor with Mr. Market all the time. Oil and gas is very unlikely to repeat the hard times of 2015 to 2020. A return of normal industry cycles alone is likely to allow for better valuations going forward.

Many in the investment industry predict a down year for the industry because prices are not expected to return to the levels of fiscal year 2022. Yet any advantages of the acquisition are not really factored into the forward valuations. Nor is there any return of the industry to market average valuations. Let us face it, just about anything in the market is more highly valued than oil and gas at the current time.

Yet insiders have a very different take on things if their actions are any indication. Baytex Energy ( BTE ) made an offer to acquir e Ranger Oil ( ROCC ). Crescent Point Energy ( CPG ) recently offered to acquire some Montney Assets. Vital Energy ( VTLE ) recently acquired the assets of a private company. Meanwhile Earthstone Energy ( ESTE ) recently completed a long shopping spree.

The insiders through their actions appear to agree with Warren Buffett that the energy industry is cheap. That would appear to mean that better valuations lie ahead even if oil prices do not get to values seen in fiscal year 2020 for a while.

That gives an investor in Occidental Petroleum more than one way to win. There is talk that there are lower priced better bargains available in the industry. So why invest in Occidental Petroleum? But such an argument assumes that everyone has the same goals and same risk profile. Clearly the choice to invest is always personal and always dependent upon the investor and the investor's situation.

Key Takeaways

Warren Buffett may not be an industry insider. He may be what some would call a rich investor. But he is a rich investor with an attractive track record. Right now his thoughts parallel a lot of industry insiders that I follow. Many CEO's have mentioned in recent conference calls how cheap the industry is. Then there are investors like John Goff and KKR that combined forces to form Crescent Energy ( CRGY ) to take advantage of the cheap prices available throughout the industry right now.

People always ask, "When do you get out and what is your target?" Generally, I follow industry insiders and people like Warren Buffett. But I follow the "going public" crowd as well.

For example , one company, HighPeak Energy ( HPK ), has gone public. Compare this to all the automobile companies that have recently gone public. That sheer number of new automobile companies should signal that a lot of insiders thought they were getting good value for their existing shareholders. It is nearly always the sign of an impending top for valuations.

Another sign is when oil and gas company executives start selling their companies in large numbers. Mergers often happen after or during a market bottom. They happen again, near market tops. Generally, I wait for a sign of maximum valuations before I decide to set a target to sell. For me, selling at the right time is far more important than having a one-year price goal. Maybe I will not hit the exact top. But at least I try to find a time to sell when it is a seller's and not the current buyer's market.

For further details see:

Why Occidental Petroleum For Warren Buffett