OGN - Why Organon & Co. Is A Smart Investment

2023-05-08 11:41:03 ET

Summary

- The share price of Organon & Co. has taken a dramatic tumble after reporting quarters with sluggish revenue and earnings numbers.

- The dividend is holding at about a 5% yield and its safety seems of only slight concern because the company has strong cash flow.

- It makes and sells over 60 products in female healthcare drugs and devices and is proving its biosimilar drug production has great potential.

Reasons to Buy-In

We are days away from pharmaceutical house Organon & Co. ( OGN ) going ex-dividend. We own the stock since May 2021 plowing the ~5% yield, or $0.28 per share, back into our reinvestment plan. We are holding the shares but are increasingly bullish for five reasons.

- We believe the share price falling close to its 52-week low is a potential opportunity.

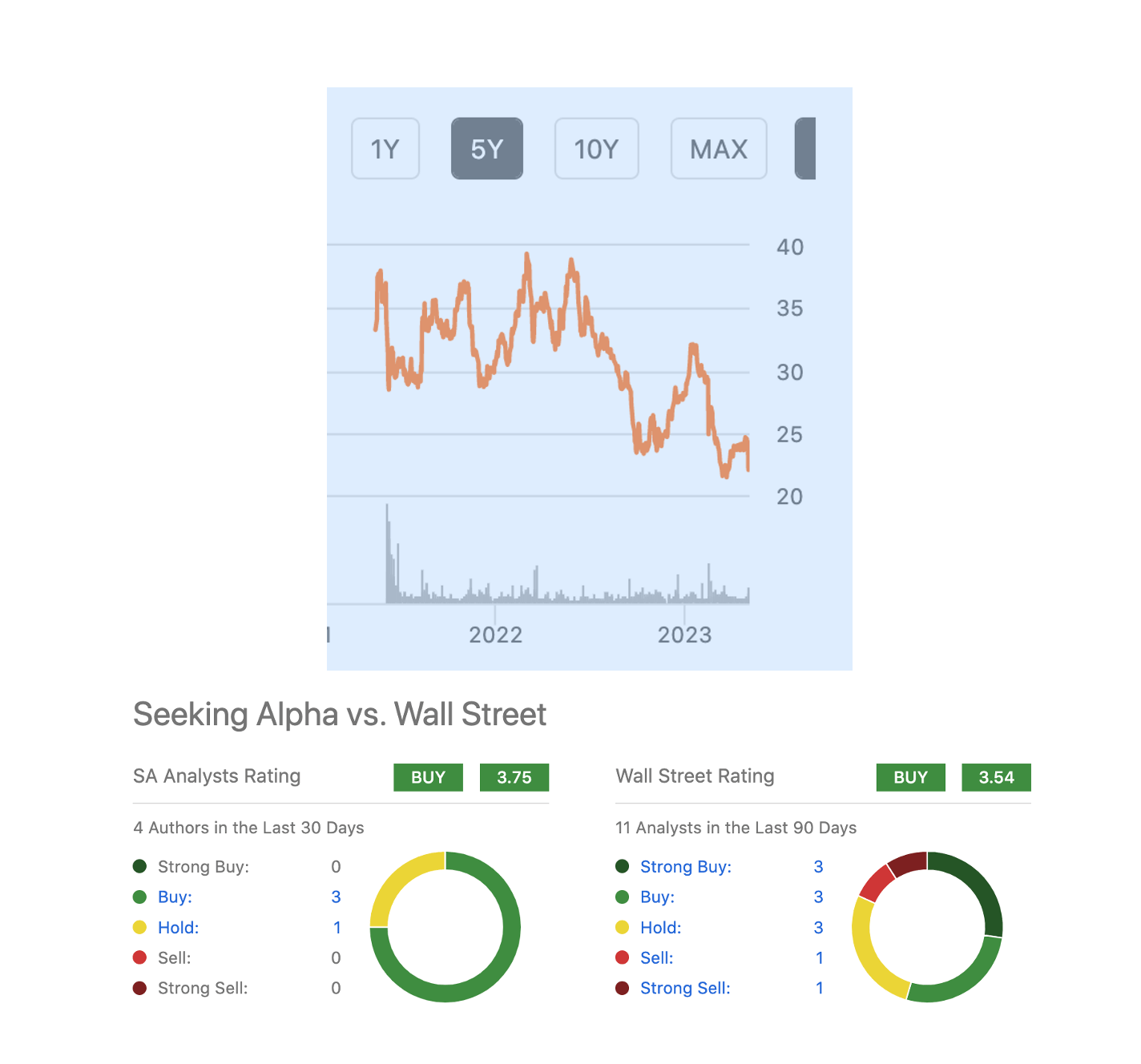

- Second, we are impressed with the enthusiasm for the stock among Seeking Alpha and Wall Street analysts, and retail value investors with a long-term perspective will probably do well having Organon & Co in their portfolios.

- Third, the PE ((FWD)) ratio is 5.22%; short interest is modest 2.66%, and the dividend has been paid consistently since August ’21.

- Our fourth reason for growing enthusiasm for the potential of Organon & Co is their dedication to the field of female healthcare betterment around the world through pharmaceuticals, medical devices, and biosimilar drug development.

- Fifth, analysts forecast higher average price targets for the stock over the next 12 months.

Share Price, Analysts' Positions (seekingalpha.com/symbol/OGN)

{kind=link}

Dividend Yield Holding, But...

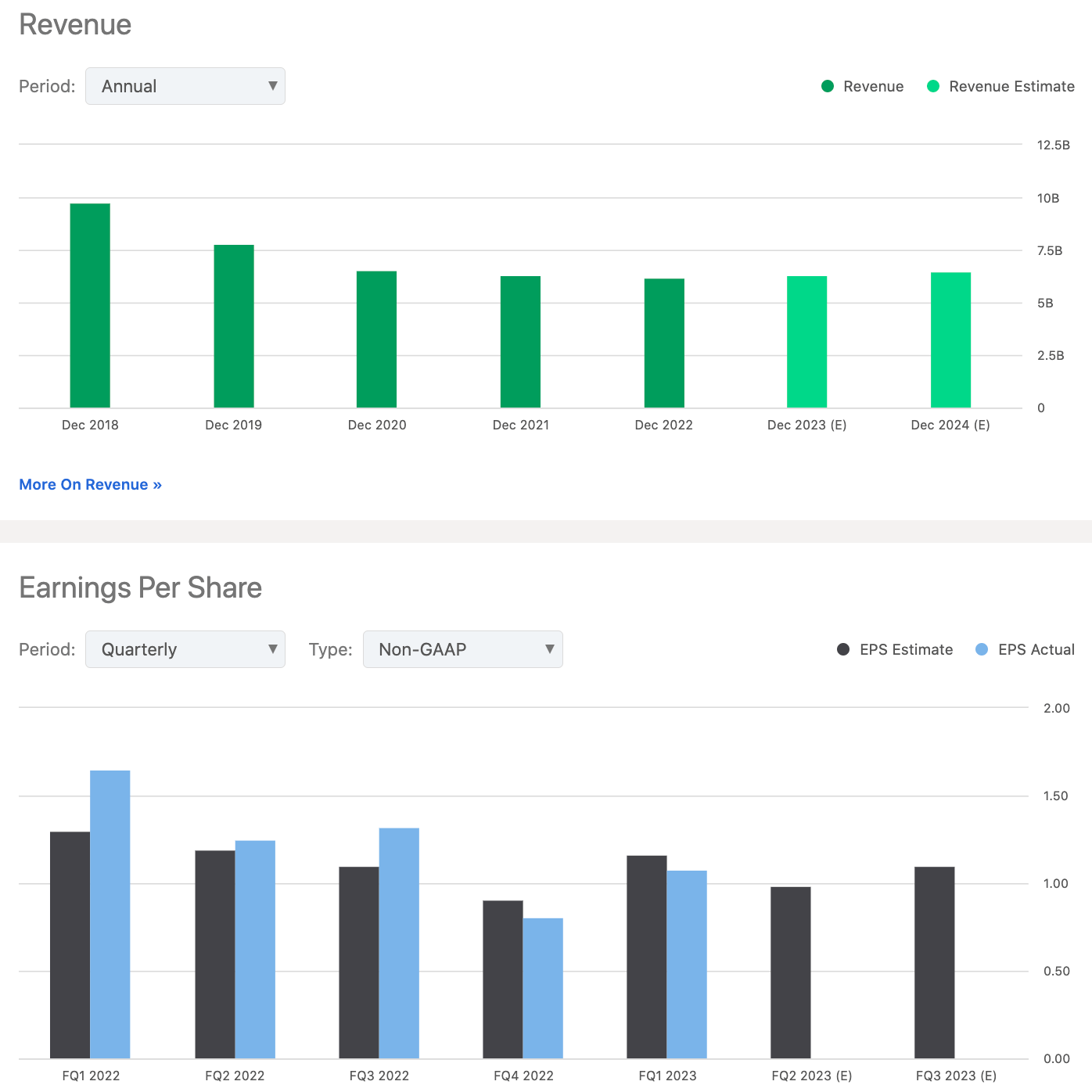

The dividend yield is attractive and appears safe at this time. A dividend is only as safe as the company’s earnings and cash flow. Caveats to consider include that the company’s recently reported Q1 ‘23 numbers are sluggish causing the share price to collapse (-35.4% over the last 12 months and about -20% YTD). The share price fell 10% in February to ~$26 following the report for its full-year results. On May 4, ’23, Organon reported Q1 Non-GAAP EPS of $1.08 and revenue of $1.54B (-1.9% Y/Y).

One analyst at Simply Wall Street tells us :

The ex-dividend date is usually set to be one business day before the record date which is the cut-off date on which you must be present on the company's books as a shareholder in order to receive the dividend. The ex-dividend date is important as the process of settlement involves two full business days. So, if you miss that date, you would not show up on the company's books on the record date. In other words, investors can purchase Organon's shares before the 12th of May in order to be eligible for the dividend, which will be paid on the 15th of June. The company's next dividend payment will be US$0.28 per share… Dividends are an important source of income to many shareholders, but the health of the business is crucial to maintaining those dividends. As a result, readers should always check whether Organon has been able to grow its dividends, or if the dividend might be cut.

In sum, the annual dividend totals $1.12. Dividends account for 38% of profits and 68% of its free cash flow until now. The future yield, however, appears ominous: debt is not well-covered by operating cash flow, revenue stumbled from 2018 through 2022, and earnings per share last reported on March 31, ’23, for Q4 ’22 and Q1 ‘23, did not meet consensus forecasts.

Numbers Are A Drag

The numbers management reported on May 4 reflect the global market penetration Organon & Co is making. It bodes well for the company’s future but in the meantime, the numbers are a thunderclap of bad news.

Adjusted EPS fell -34.5% Y/Y to $1.08. We forecast the ‘23 Q2 EPS, tentatively scheduled to be reported on August 9, ’23, will be between $1.02 and $1.04; i.e., last quarter and next quarter EPS reports will be less than the $1.25 for Q2 ’22. Revenue declined in Q4 by -1.8% Y/Y to ~$1.54B. Revenue from the Women's Health segment rose less than 1% Y/Y to $381M; the segment had strong sales in oral contraceptives Marvelon and Mercilon.

Sales of birth control implant Nexplanon fell 1% ex-FX mainly due to the impact of distributors' buying patterns in prior periods, according to the company. The biggest decline was -7% in infertility products. The company attributes the slip to incessant lockdowns from COVID across China. Established Brands sales decreased -4.8% Y/Y to $1B.

On a positive note, cash and cash equivalents were $459M. Debt was $8.7B on March 31, 2023, after a voluntary $250M debt repayment on a term loan. Debt and interest payments and dividends are covered by cash flow and the market cap is $5.74B.

Revenue & Earnings (seekingalpha.com/symbol/OGN)

{kind=link}

The Company

Organon & Co. develops and sells numerous prescription therapies and medical devices for contraception and fertility. The female contraceptive market is forecast to grow by 8.5% ((CAGR)) between 2022 and 2027. Organon is among the top 5 major corporations addressing needs in the female contraceptive market.

For example, among its major portfolio of products and devices is Nexplanon/Implanon, a long-acting reversible contraceptive. NuvaRing is a monthly vaginal contraceptive ring. Cerazette is a daily pill used to prevent pregnancy. Marvelon is taken daily to prevent pregnancy. Jada is for abnormal postpartum uterine bleeding or hemorrhage. And the list goes on.

Additionally, the company has a portfolio of biosimilar immunology products, two oncology products, treatments for hypertension, respiratory products, dermatology products, non-opioid pills for pain management, and treatments for male pattern hair loss. June 3, 2021, the first day of official life for Organon, management claimed to have +60 drug products to improve female health “and Merck’s ( MRK ) former biosimilars portfolio.” Organon was formed as a spinoff from Merck that we analyzed for Seeking Alpha followers.

PharmaVoice expects biosimilars to have an exciting future. They expect the market to reach $44.7B by 2026 and grow at a CAGR of 23.5%. Biosimilars are drugs that are like other biological drugs (reference drugs) approved by the U.S. Food and Drug Administration (FDA). Biosimilar drugs and reference drugs are made from similar or different living organisms but they may be made in different ways and of slightly different substances.

Biosimilar drugs are to be used in the same way, at the same dose, and for the same condition as the reference drug. Biosimilar may cost less than the reference drugs and are more akin to generic drugs in this regard. Big and small companies are rushing into the biosimilar drugs field. The new CEO of Teva Pharmaceutical Industries Limited ( TEVA ), for example, is cited in our article expecting Teva’s biosimilar drug for arthritis treatment “to boost Teva revenue.”

Biosimilar drugs revenue at Organon grew 17% to $116M. Some drug sales increased by over 30% in the U.S., Canada, and Brazil. The company had strong performances of some brands in China and in the Asia Pacific/Japan region. In April 2023, the China Daily headline read, “A new giant in women’s health, Organon looks to future growth in China.”

WHO Cares

The World Health Organization and the World Economic Forum told 2023 Davos attendees that female health care “Is the world’s best-and most under-financed-investment.” And, “A healthier future starts in the lab.” That is precisely the company mission: A better and healthier every day for every woman. Corporate insiders seem to care; they are on a buying spree of shares in February through May.

Fintel shows that 1369 funds or institutions reporting positions in Organon seem not to care. This is a decrease of 38 owners as the share price tumbled. Hedge funds increased their holdings by 123K shares last quarter. The average portfolio weight of all funds in the stock increased by 26.47%.

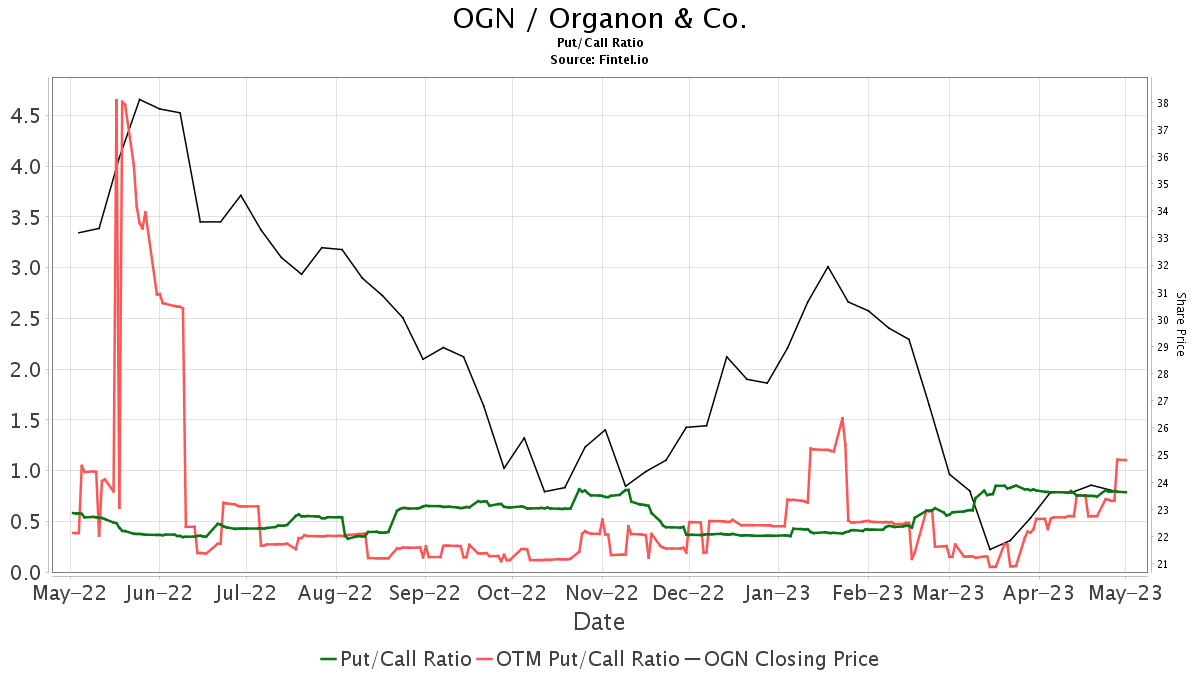

Puts/Calls (nasdaq.com/articles/organon-ogn-declares-$0.28-dividend)

{kind=link}

The put/call ratio is 0.84, which we assess as a bullish outlook. We forecast the average price target over the next 12 months will be in the low $20s to $32 on the upside. One analyst has the share price target topping $45.

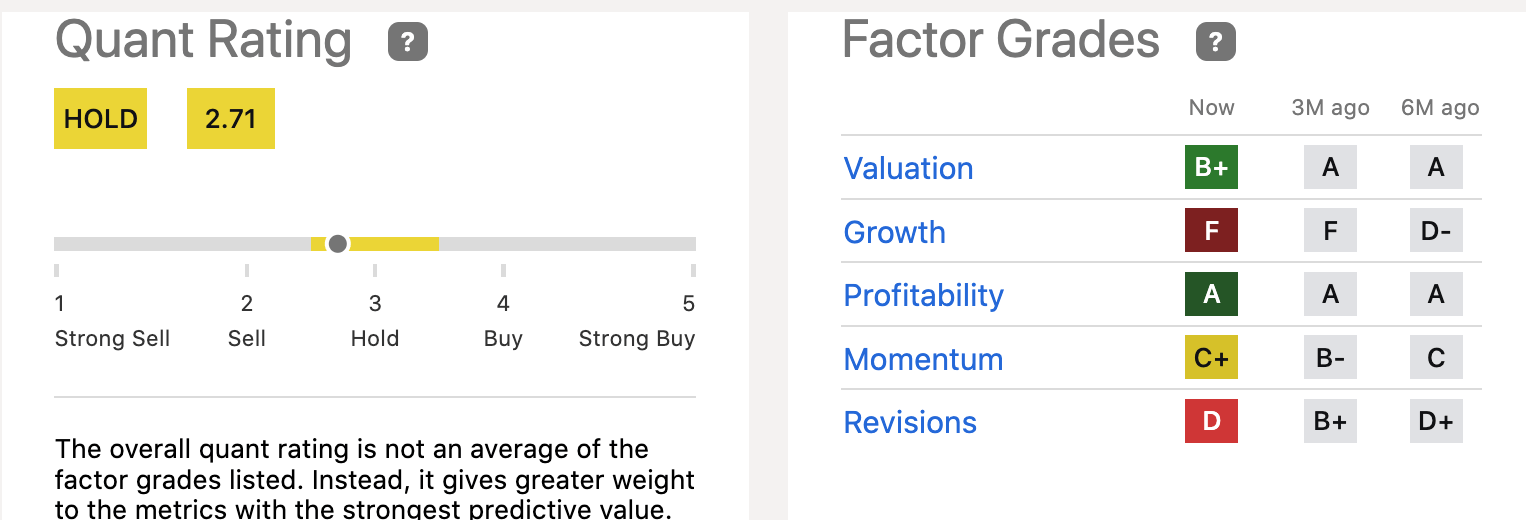

Quant Rating/Factor Grades (seekingalpha.com/symbol/OGN/ratings/quant-ratings)

{kind=link}

The SA Quant Rating now leans toward the Buy-side of its assessments after more than 18 months of rating the stock a Hold. The SA Factor Grades support our notes of caution to retail value investors. Growth is a weak link in the chain of Factors. The company limits its M&As. Organon & Co bought 2 companies in the last 5 years. Both were in segments to fulfill the company mission through life science and medical devices.

Growth we think will come because management has a global perspective. Welcoming Organon to China, the extraordinarily positive China Daily article tells of the company's plans to sell products and undertake deals with local biotech companies. We think investing in women’s health is the smartest thing an investor can do for oneself and the portfolio.

For further details see:

Why Organon & Co. Is A Smart Investment