PCAR - Why Paccar Will Weather A Recession Better Than Iveco

2023-05-08 00:14:04 ET

Summary

- The economy can't go without trucks. Truck manufacturers are set to benefit because of this.

- Fears of a recession see a slowdown in freight transportation.

- In this article, I compare PACCAR to Iveco to see which one can face a recession in a better way than the other.

Introduction

Like or not, 74% of U.S. freight is moved by truck. Don't think it is much different elsewhere around the world.

PACCAR 1A 2023 Results Presentation

No matter how we look at transportation, a future without trucks seems yet very far out into the future.

However, these considerations do not automatically make any investment in trucks a good investment. For example, withing the truck manufacturing industry, there are several differences among the most important players. Even though they all benefit from the same environment, they do not deliver at the same level.

While there may be times when demand for trucks is so strong that any player in the market achieves good results. But when fears of a recession tamper general spending, making consumers more cost-conscious, freight movement is set to take a hit and trucking with it. Not only trucking, but also orders for new trucks may slow down.

In this article, I would like to compare Iveco Group ( OTCPK:IVCGF ) to PACCAR ( PCAR ) showing why I think the former is likely to take a much greater hit than the latter in case of a recession.

Geographic exposure

Iveco

Iveco is undergoing two transformational years after the spin-off from CNH Industrial took place at the beginning of last year. Iveco had always been the business that dragged CNH Industrial's margins down.

Now that it has to stand on its own, the focus on profitability has become more clear.

Secondly, Iveco is a strong company in Europe where it does 72% of its revenues. But in a globalized world it is at risk of being a regional player. In case of a recession, Iveco is much less diversified than other peers, such as PACCAR, that have different areas around the worlds as revenue sources.

Moreover, Iveco is highly exposed to trucks and doesn't have a meaningful spare parts segment since it doesn't yet report it. PACCAR, on the other hand, has made this segment a true cash cow of its business.

Iveco FY 2022 Results Presentation

However , being a strong regional player could offer some opportunities for Iveco investors since I consider the company to be one of the most likely candidates to be part of any M&A aiming at consolidating the industry.

PACCAR

PACCAR, on the other hand has two major markets that are equal in size: Europe and North America. In each of these two areas the company expects to sell around 300k vehicles for the ongoing year. There is a third market, which is South America, which is in size about 33% of the other two. Here the company's forecast sees vehicles sales around 115k units. It is clear that PACCAR is better diversified and can thus withstand a big economic drawdown.

Profitability

Iveco

Even during a strong year as 2022, Iveco barely achieved profitability, with an adj. EBIT margin at 3.7%. In fact, net revenues came in at €14.2 billion and adj. EBIT was €527 million. It is not a very strong result if a company wants to take advantage of a strong market to build the foundations to endure harder economic times.

In 2022, Iveco's FCF generation did improve to €690 million, considering that in 2021 Iveco had an absorption of €125 million, making Iveco a FCF negative company.

PACCAR

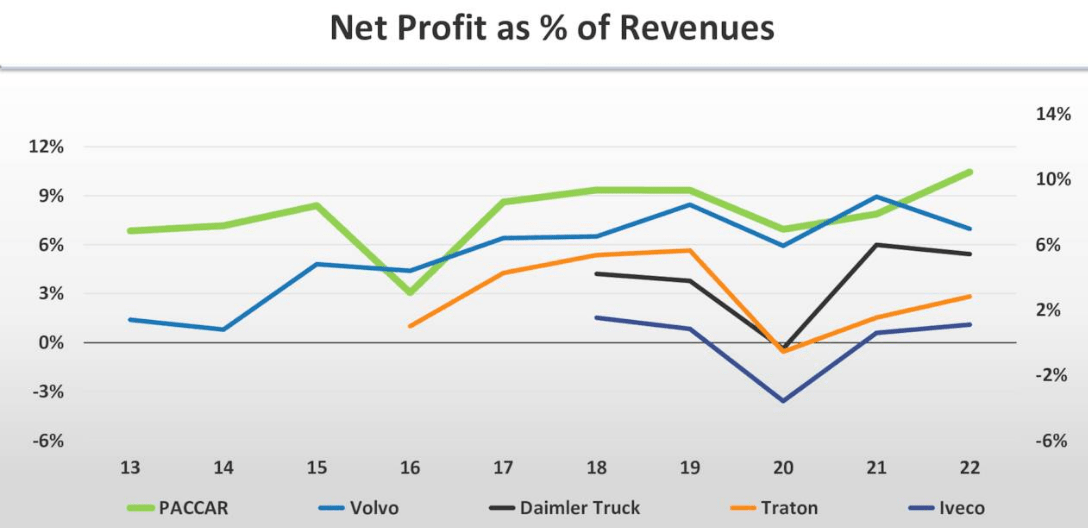

Profitability is what makes PACCAR so interesting. In fact, as we can see from the graph below that PACCAR regularly posts in its results presentation, the company keeps on leading the industry, alongside Volvo. We then see Daimler Truck that seems to be catching up a bit. Last is Iveco and, as we see, it was the only one that went deep into the negative during the pandemic.

PACCAR Q1 2023 Results Presentation

{kind=link}

In addition, as I have already outlined , PACCAR reports a ROIC around 22%, well above what other well-established companies such as Caterpillar, Deere and Volvo.

PACCAR has a secret to help it boost its profitability: its spare parts and services segment. The company has focused on growing this business, understanding how each truck sold is a tremendous opportunity to monetize the user and generate a constant stream of recurring revenue down the road.

PACCAR Q1 2023 Results Presentation

In Q1 2023, PACCAR reported it achieved a record quarterly income of $438.6 million. From a revenue point of view, Parts is now 20% of total revenues, helping increase the overall profitability of the company since its gross margins is above 32% against 16% gross margins for the truck division.

Other peers

The graph comparing the five most important players in the industry, assessing them by their profitability, gives us the chance to take a quick look out of the boundaries of the comparison we are considering. The most important thing I see is that the pandemic clearly helped identify the industry leaders and the rest. That is, on one side we have PACCAR and Volvo Group ( OTCPK:VLVLY ; OTCPK:VOLAF ); on the other Daimler Truck ( OTCPK:DTRUY ), Traton ( OTCPK:TRATF ) and Iveco. These last three are all European truck manufacturers that have recently been spun-off. Among the three , however, we see there is one that is quickly catching up with the leaders. It is Daimler Truck. The reason why this company is improving a lot is mainly due to its large exposure to high-margin markets such as North America. Since Iveco is mostly exposed to Europe, I find it difficult to see how the company will be able to compete on profitability with companies more widespread across the global market.

Incoming orders

Iveco

Iveco, as most of its peers has also seen an order decline starting already at the end of 2022. However, while other companies, such as Volvo Group, were really restrictive on order intake to defend their margins, Iveco used no such strategy. Therefore, its order decline is truly a problem because it shows demand for its trucks is slowing. Other companies, on the other hand, simply refused to take all at once the orders customers were placing. Now they can count on some pent-up demand for their trucks. I believe Iveco will barely benefit from this.

Iveco FY 2022 Results Presentation

{kind=link}

PACCAR

During the recent earnings call on Q1 2023 results, Preston Feight, PACCAR's CEO, explained how PACCAR's order book "is substantially full in all markets. So that includes South America, Europe, North America, Australia, Mexico, pretty much everywhere". Even though PACCAR doesn't disclose as transparently as some of its peers the number of incoming orders, the company felt confident enough to say how, after just one quarter, its order books already extends into 2024. This is because of two reasons, I believe. First, PACCAR owns important brands, such as Kenworth, Peterbilt and DAF, that have customer loyalty. Second, the company is better diversified than Iveco.

Other Peers

In terms of order intake, I have repeatedly pointed out how Volvo saw early in the game the problem inflation was creating for profitability. Therefore, it was among the first companies in the industry (as far as I know) to sacrifice volumes for the sake of profitability. We thus saw Volvo's orders decline, while its profitability remained above 10%. Why was Volvo able to do that? Because the company knows there are customers who are willing to wait until the can place an order for a Volvo truck instead of going to another competitor and buy another truck. Volvo's restrictive order intake policy has helped the company weather inflationary pressure, while creating some pent-up demand that could help it weather a mild recession. Iveco, unfortunately, never mentioned such a policy and I think the reason is easy to understand: it is not a policy it can carry out successfully.

Balance Sheet

Iveco

Iveco's balance sheet is in shape, with €4.4 billion of available liquidity, €2 billion of which of undrawn committed facilities. Total cash maturities add up to €872 million between 2023 and 2026. Most of this is bank debt.

Overall, considering all different debts, Iveco has a net cash position of €1.73 billion which gives it some strength to face harder economic times. However, if we look at the operating expenses, Iveco, in 2022 had to spend €1.5 billion to run its operations. Almost €1 billion went for SG&A, while €450 million were spent on R&D, which a company such as Iveco can't just simply reduce. This means Iveco has enough cash to fund one full year of operations in the case it didn't earn any revenue. Of course, this is very unlikely to happen, but it makes me think Iveco's cash position may not be as strong as it may seem. In addition, Iveco may run into a bit of trouble if Nikola ends up filing for bankruptcy. Iveco, in fact, has a stake in the company.

PACCAR

PACCAR is very conservative with its balance sheet. It currently holds $5.9 billion in cash and it has no manufacturing debt. This means the company can finance its operations on its own, without needing to raise more debt. It is no surprise, then, that its debit receives an A+/A1 rating.

Considering PACCAR spent $3.78 billion to operate its business, if we look at all the total operating expenses we see that PACCAR had to spend around $833 million, way less than Iveco even though it is a larger company. Therefore, I think PACCAR is more prepared to face any upcoming hic-up in economic activity.

EV Portfolio

Where I see as one of the areas of major concern for Iveco is its lack of heavy-duty electric trucks. True, Iveco partnered with Nikola ( NKLA ) to build the Nikola Tre. But is this partnership safe ? Can Nikola really be the company that will help Iveco become competitive in this space? In the meantime, companies such as Volvo Group, PACCAR and Daimler Truck are already selling electrified trucks and buses in the hundreds and thousands.

Conclusion

Even though in the past few months Iveco's stock has delivered very good results for investors , I think the company, even if still cheap, is too risky in the current economic environment characterized by many uncertainties. This is why I consider it a sell, pointing out how its low margins don't suggest Iveco can withstand a recession without becoming once again an unprofitable company. I have always had a sell rating on Iveco until a few months ago, when I switched to a hold. As I explained back then, I was not really upgrading the stock, but I was just saying I had become more neutral as Iveco first posted a profitable year. Yet, with a recession that I think is due, as mild as it may be, it seems like it will lead Iveco close to negative territory, when speaking of margins.

On the other hand, PACCAR has a better revenue mix and has understood how to leverage its sales to build a spare parts business that is truly unique.

PACCAR's share price has gone up 32% in the past twelve months, versus Iveco +58% in the same period of time. PACCAR now trades at a fwd PE of 10 and a price/cash flow of 11.4. We are close to ATHs and this is why I would currently suggest a hold instead of a buy. PACCAR is a stock that trades down from time to time and investors should be patient enough to wait for the next dip.

For further details see:

Why Paccar Will Weather A Recession Better Than Iveco