PATK - Why Patrick Industries Is A Solid Investment Opportunity

Summary

- With its solid track record of growth and profitability, Patrick Industries has established itself as a leading supplier in the RV and marine industries.

- The company's stock performance has underperformed the S&P 500's total return significantly over the past five years, leaving investors disappointed.

- With a current share price that is significantly lower than its intrinsic value, the company presents an attractive buying opportunity for investors.

Overview

Patrick Industries, Inc. (PATK) is a leading manufacturer and distributor of building products and materials for the recreational vehicle (RV), marine, manufactured housing, and industrial markets. The company is headquartered in Elkhart, Indiana, and operates over 130 manufacturing and distribution facilities across the United States. Patrick Industries' products include a wide range of components and accessories, such as furniture, flooring, and lighting, for use in RVs, boats, and manufactured homes.

Under the leadership of CEO Andy Nemeth, Patrick Industries has achieved consistent revenue and free cash flow growth over the past decade, driven by numerous strategic acquisitions. The company has a strong track record of integrating acquired businesses and generating cost synergies, which has helped to expand its product offerings and improve its operating margins.

Despite its strong performance, Patrick Industries' valuation remains relatively attractive, with a current free cash flow yield over 15%. This suggests that the market may be underestimating the company's growth potential and the quality of its management team. As the RV and marine industries continue to grow, driven by strong consumer demand for outdoor recreation, PATK is well-positioned to benefit from these trends and generate long-term value for shareholders.

The Business

Headquartered in Elkhart, Indiana, Patrick Industries, Inc. is a manufacturing and distribution company that has been in operation since 1959. The company has a simple business model as it sells components, building products, and materials to some of the largest players within the recreational vehicle (RV) and marine industries including Thor Industries ( THO ), Forest River, Winnebago ( WGO ), MasterCraft Boat ( MCFT ), and Malibu Boats ( MBUU ) among others.

PATK also caters to a couple other markets, including the manufactured homes industry and industrial markets. PATK does business in the United States, Canada, and China and organizes itself into two operating segments which include the Manufacturing segment and the Distribution segment.

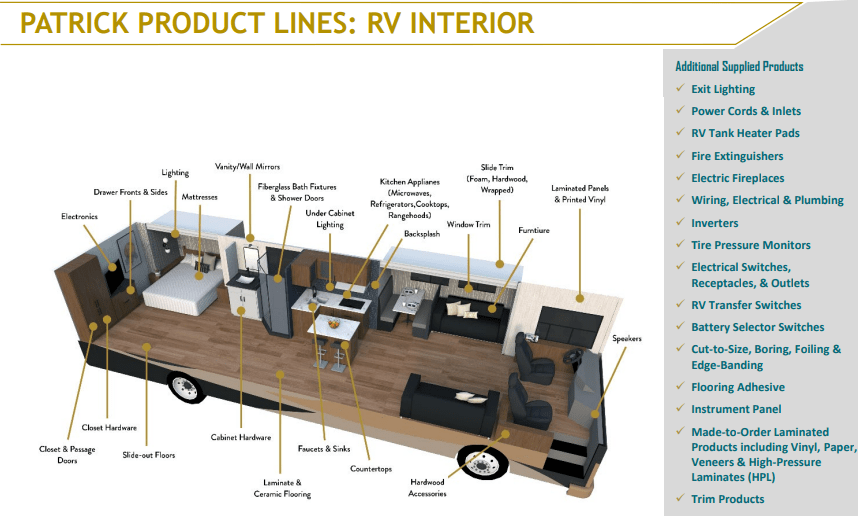

PATK's Manufacturing segment offers a wide range of products such as furniture, shelving, countertops, cabinets, fiberglass bath fixtures, sound systems, solid surface and granite countertops, aluminum products, and other items for recreational vehicles, marine, manufactured housing, and industrial markets.

The company's Distribution segment distributes pre-finished wall and ceiling panels, appliances, electrical and plumbing products, roofing, laminate, and ceramic flooring products, furniture, and other items. Additionally, the Distribution segment provides transportation and logistics services. PATK has such a wide range of products that the next time you step foot in an RV or boat you will find yourself surrounded by products made by PATK.

{kind=link}

Leadership

One of PATK's biggest strengths is its experienced leadership team who combine have over 100 years of industry experience spanning across multiple economic cycles. Since January 2020, Andy Nemeth has held the top position of Chief Executive Officer of the company, having previously served as President from January 2016 to July 2021.

Before becoming CEO, Nemeth worked as Executive Vice President of Finance and Chief Financial Officer from May 2004 to December 2015, as well as Secretary-Treasurer from 2002 to May 2016. From 2003 to 2004, he was the Vice President of Finance and Chief Financial Officer.

With over 31 years of experience in the recreational vehicle, marine, manufactured housing, and industrial industries, Nemeth has held various financial and managerial roles. He has also served as a director of the company since 2006. Even though Nemeth has only served as CEO for a short period of time, the company has seen impressive financial results under his leadership.

Track Record

PATK's outstanding performance over the past decade begins with its revenue growth. During the past ten years, the company has achieved a revenue growth rate of over 800%, which is a remarkable achievement. Additionally, it is noteworthy that there hasn't been a single year of revenue declines during this period.

Data by Stock Analysis

PATK has an impressive history of generating free cash flow and achieving growth. The company has experienced a substantial increase in its free cash flow by 1300% over the last decade, although the growth has been choppy with three years of declines during the period.

In addition, PATK has established a robust record of profitability. In the last ten years, the company has achieved an average return on equity of just over 31%, and not a single year fell below 15%. These high ROE levels show the company is managing its assets and liabilities effectively, and that it is making good use of its available resources to generate profits.

Turning to PATK's balance sheet, the company's impressive growth continues with its book value. Over the last decade the company has grown book value every single year and over 1200% overall. It's important for companies to grow their book value because it shows that the company's assets are increasing in value relative to its liabilities which can lead to an increase in the company's net worth, which is a positive for shareholders.

Data by Stock Analysis

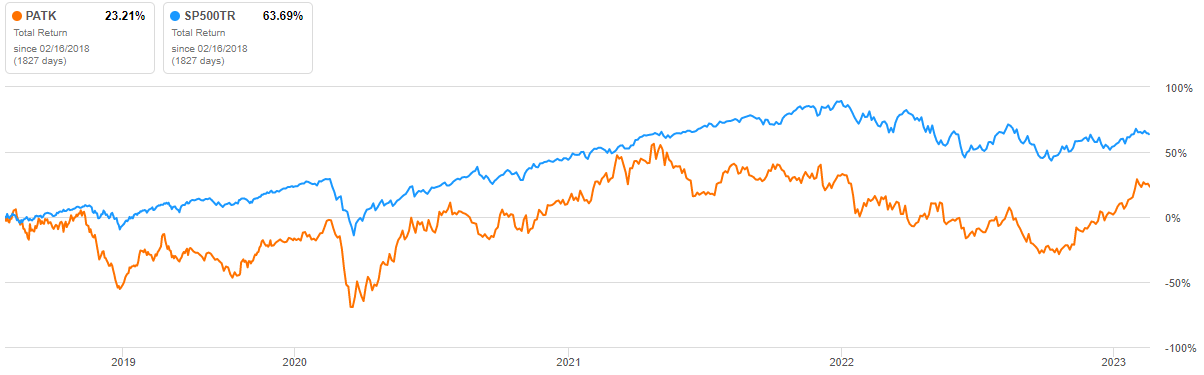

Though PATK's financial performance has been impressive, the company has trailed the total returns of the S&P 500 over the past five years by almost 40%, leaving investors to question what the company can do in the future to turn these results around.

{kind=link}

Outlook

A key component of the PATK's growth strategy has been growing through mergers and acquisitions. PATK seeks to acquire businesses with strong management teams that fit in with the company's core values, business model, and customer base.

The goal of these acquisitions is to acquire additional product lines, facilities, or other assets that can expand the company's existing businesses. In 2021, the company spent over $500M on acquisitions, and management intends to continue looking for more acquisitions in the future.

Perhaps, PATK will look to make acquisitions in the marine industry which happens to be the company's fastest growing product category. Currently, marine sales make up 18% of the company's total revenue, up from 11% in 2017. The marine industry is growing fast, with US power boat registrations up nearly 20% from 2017 through 2021.

PATK is positioned well as the marine industry continues to grow but today, the company's largest product category is from the RV industry which makes up close to 60% of the company's revenue. The company stands to benefit from favorable RV industry trends as a recent survey by GO RVING found that 20.9M US households plan to purchase an RV, with 9.6M planning to purchase within the next five years.

Risks

It is important to consider some of the risks associated with investing in PATK. First and foremost are the company's customers mainly operate in the RV and maritime industries which are heavily influenced by the overall health of the economy. In a recession, consumers tend to cut back on discretionary spending and RVs and boats are a discretionary purchase, meaning that they are not a necessity making them particularly sensitive to changes in consumer spending habits.

Another risk to consider is that PATK is heavily reliant on its largest customers which include Thor Industries and Forest River. If the company were to lose one or both of these customers, it would take a major financial hit resulting in lost revenue, free cash flow, and reduced profitability.

Valuation

To estimate PATK's intrinsic value, we will run comparative and discounted cash flow ("DCF") analyses. To begin, we'll start with the comparative analysis and look at the highest, lowest, and median price-to-earnings ratios the market has paid for PATK over the past five years. We'll also look at the sector median P/E, which is 14.79 . Finally, we'll multiply these ratios by PATK's consensus 2024 EPS estimate of $9.08 per share.

| Scenario |

| P/E |

| Next Year Earnings Estimate |

| Intrinsic Value Estimate |

| % Change |

| Bear Case |

| 2.996 |

| $9.08 |

| $27.20 |

| -63.27% |

| 5Y Median P/E |

| 10.29 |

| $9.08 |

| $93.43 |

| 26.14% |

| Bull Case |

| 25.6 |

| $9.08 |

| $232.45 |

| 213.82% |

| Sector Median Valuation |

| 14.79 |

| $9.08 |

| $134.29 |

| 81.31% |

On a comparative analysis, PATK has a wide range of scenarios that can play out. Investors could realize an excellent 213.82% return if the market were bullish and applied the 25.6 multiple, seen in 2020, to next year's average analyst earnings estimate, should those estimates materialize. On the downside, investors could realize a -63.27% loss if the market were to value PATK at the bearish P/E ratio seen just a few months ago in October 2022.

Based on the 5-year median P/E ratio, the most likely scenario for PATK is the base case, which is considered the most significant. If this scenario plays out, it could result in a 26.14% return for investors.

The final scenario is if the market values PATK at the sector median multiple which would represent an 81.31% return. Taking everything into account, this comparative analysis suggests that PATK is undervalued and has greater potential for upside than downside at its current share price.

In the discounted cash flow analysis for PATK, we will start by averaging the last five years of free cash flows, which comes out to $140M. We will then apply a 7% growth rate for the next ten years, following the rule of 72 which states that a 7% growth rate will double the original value in ten years.

We have chosen this rule to guide our DCF analysis because it is difficult to make accurate forecasts of free cash flow growth rates for several years into the future. Nevertheless, I am confident that PATK has the potential to double its free cash flow over the next decade based on its track record of growth and future outlook.

After the 10th year, we will assume a perpetual growth rate of 2.5% to determine the terminal value. To discount the cash flows, we will use a 10% discount rate, which reflects my personal required rate of return. Given these inputs, the DCF analysis produces an intrinsic value of $110.66, suggesting a potential upside of 49.40% from PATK's current price.

{kind=link}

In case you think that a 7% growth rate for PATK over the next ten years is too optimistic, it's worth noting that even if the company grows at a rate of just 1.5% per year over the next decade, its intrinsic value based on this DCF analysis would still be slightly higher than its current share price. This suggests that PATK's share price has a considerable margin of safety at present.

Takeaway

With its solid track record of growth and profitability, PATK has established itself as a leading supplier in the RV and marine industries, among others. Despite this success, PATK's stock performance has underperformed the S&P 500's total return significantly over the past five years, leaving investors disappointed.

However, PATK is poised to take advantage of the growth potential of the RV and marine sectors, which are expected to continue expanding in the foreseeable future despite near turn macroeconomic concerns. Additionally, with a strong management team and a current market price that is significantly lower than its intrinsic value, the company presents an attractive buying opportunity for investors.

Please let me know your thoughts on PATK in the comments section below.

Thank you for reading!

For further details see:

Why Patrick Industries Is A Solid Investment Opportunity