VGR - Why Philip Morris Isn't The Best Tobacco Stock

Summary

- Philip Morris has an attractive dividend yield.

- However, it doesn't seem to be attractive as some of its peers.

- In addition, PM stock may not be at bargain prices at the moment.

Companies like Philip Morris ( PM ) are a great way to stabilize your portfolio during times of volatility and uncertainty. Indeed, its current dividend appears to be quite attractive. However, when compared to some of its competitors, we believe that there are better options to choose from. As a result, we are neutral on Philip Morris stock.

Tobacco Industry Snapshot and Growth Catalysts

The tobacco industry is commonly regarded as declining, but this is not the case. In fact, the tobacco market is anticipated to grow at a 3.75% CAGR from 2022 to 2027 globally , with the Asia Pacific region leading as the fastest-growing market. Developing economies are driving this growth due to their lenient regulations on tobacco products, which result in a significant portion of their tax revenues.

Moreover, tobacco products are highly addictive, and consumers are likely to prioritize spending on them even during periods of inflation or recession. Additionally, tobacco consumers tend to remain loyal to their preferred brands despite the price, unlike other products.

Furthermore, the perception that the industry has limited growth potential and is heavily regulated by the government restricts the number of new entrants into the market. Many young entrepreneurs are not enthusiastic about taking on established players in a shrinking market.

Therefore, tobacco companies have considerable pricing power, which allows them to increase their profits and dividends.

Competitor Analysis

Let's take a look at how Philip Morris compares to some of its competitors:

{kind=link}

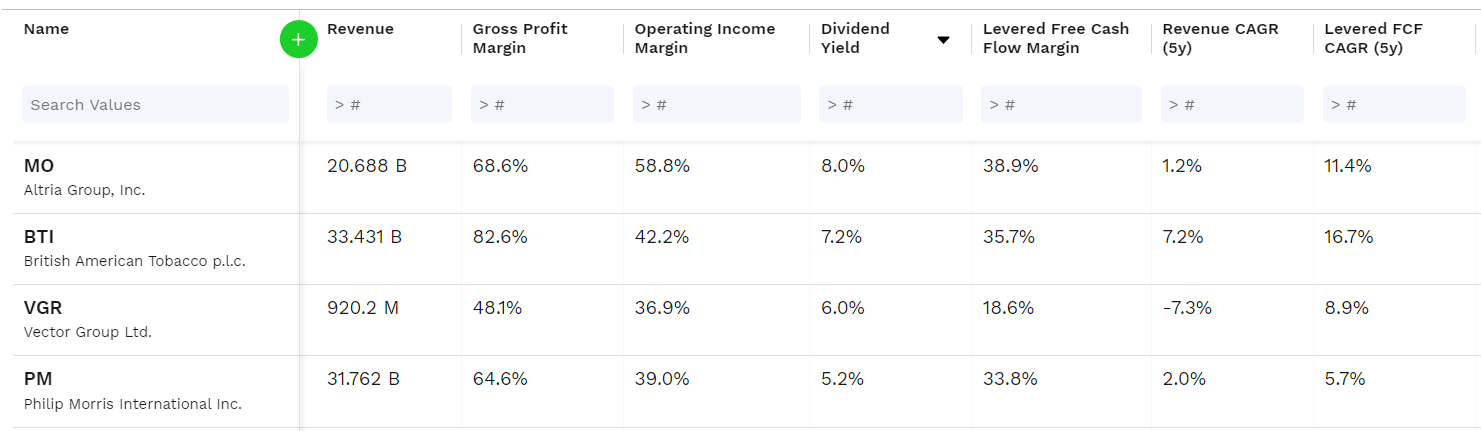

Starting with gross profit margins, Philip Morris comes in at 64.6%, slightly lower than Altria's ( MO ) 68.6% and well below that of British American Tobacco ( BTI ) at 82.6%. It also finds itself behind those two companies when it comes to operating margin, as it has an operating margin of 39%.

Its dividend yield of 5.2% is undoubtedly attractive, but it's below that of its peers. MO has the highest yield at 8%, while BTI and Vector Group ( VGR ) come in at 7.2% and 6%, respectively. Philip Morris does have the second highest 5-year revenue CAGR out of the bunch, although this doesn't really say much, at 2%.

In addition, its free cash flow growth, which is what investors should be focusing on the most, has been the least impressive. Over the past five years, it managed to increase FCF by a CAGR of 5.7%.

Is Philip Morris Undervalued?

Valuing Philip Morris stock is simple since it has stable dividends that analysts expect to grow at a CAGR of around 3.62% over the next five years. This type of growth rate is reasonably sustainable over the long term.

As a result, we will use a simple single-stage dividend discount model with a 3.62% perpetual growth rate. Using a discount rate of 11% (as per Finbox), the calculation is as follows:

- Fair Value = Dividend per share / (Discount Rate - Terminal Growth)

- $68.83 = $5.08 / (0.11 - 0.0362)

As a result, we believe that Philip Morris is worth at least $68.83 per share under the current market environment.

Risks Associated with Philip Morris

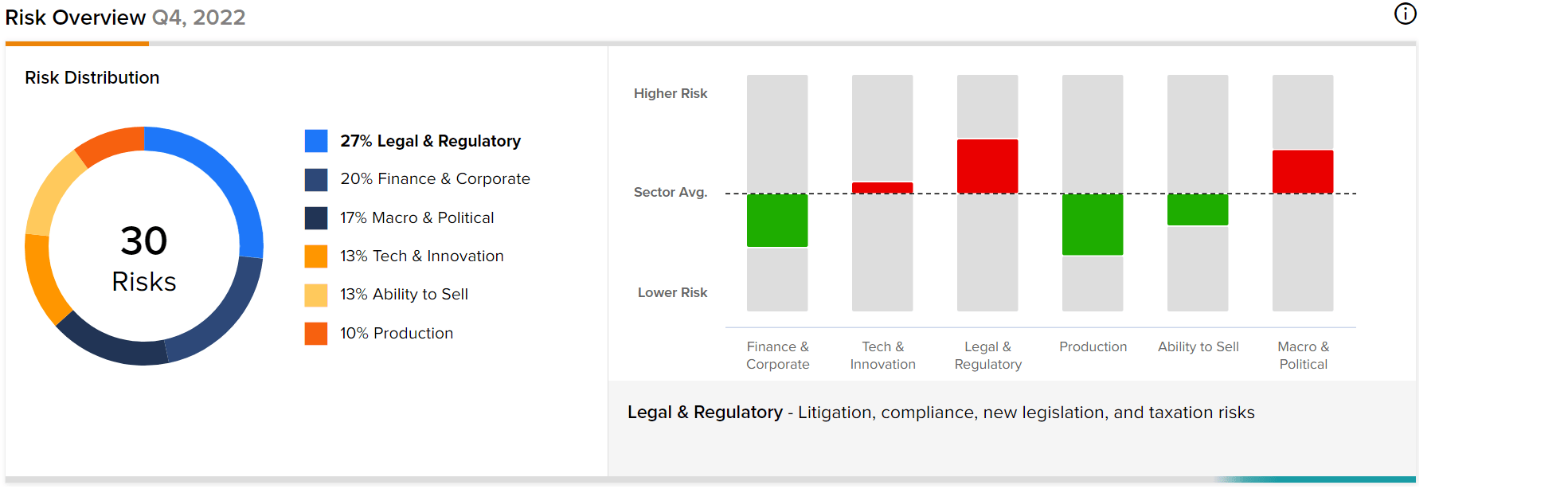

Investors of Philip Morris should be aware that it carries quite a bit of regulation risk. Indeed, its risk distribution shows Legal & Regulatory as the highest risk category, followed by Finance & Corporate. It's also worth noting that the Legal & Regulatory, Tech & Innovation, and Macro & Political categories have more risk disclosures than the sector averages:

{kind=link}

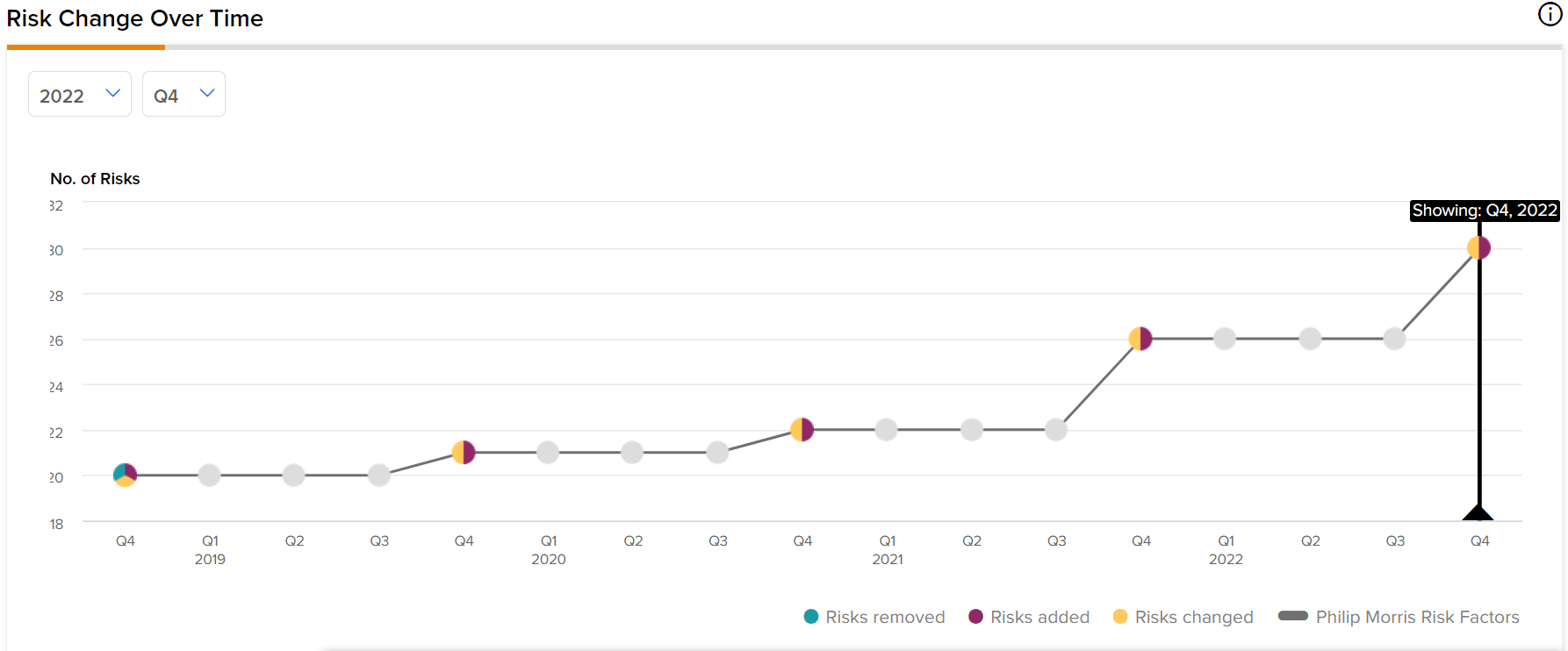

What's also interesting is that the overall number of risk disclosures has been increasing. Indeed, Philip Morris disclosed four new risks in its most recent quarter, bringing the current total to 30. This means that the number of risks has increased by 50% since Q4 2018, as indicated by the graphic below:

{kind=link}

Final Thoughts

Philip Morris is definitely a solid business with stable and predictable dividend payments that are useful during periods of market volatility and macroeconomic uncertainties. However, for investors looking to potentially open a new position, it seems that some of its competitors, like Altria, might be a better option at this juncture.

For further details see:

Why Philip Morris Isn't The Best Tobacco Stock