PLL - Why Piedmont Lithium Is Our Number 1 Stock Pick In 2023

Summary

- Piedmont Lithium Inc. is set to become a new lithium producer in 2023 from their 50% share of off-take from the NAL Project in Canada. By 2026, Ghana production should contribute.

- By end 2023, we forecast Piedmont Lithium's base (near worse) case valuation as 1.1x (10%) higher (NAL only). Yahoo Finance's price targets are US$107 & A$2.05.

- By end 2025/26, based "only" on NAL and Ghana production we forecast the potential upside for Piedmont Lithium's valuation is 1.7x (bear case), 4.3x (base case), and 6.9x (bull case).

- From 2026/27 onwards, there is significant potential further upside assuming Piedmont can bring on Carolina Lithium and several LiOH conversion plants in North America. These projects have the potential to at least double the above current upside potential.

- Risks revolve mostly around lithium pricing and Piedmont Lithium advancing their projects on time and budget. We view Piedmont Lithium as a great spec buy, suitable for a 5-year-plus time frame.

This article first appeared in 'Trend Investing Marketplace' when Piedmont Lithium was trading at US$49.11 (PLL) and A$0.73 [ASX:PLL]; but has been updated for this article.

Today's article focuses only on Piedmont Lithium's valuation and why it is our number 1 stock pick for 2023. We also briefly discuss Piedmont's most recent updated off-take agreement with Tesla, Inc. ( TSLA ).

For a background on Piedmont Lithium Inc. ( PLL ) [ASX:PLL], you may read our past articles:

- April 2019 - Piedmont Lithium - The Only US Lithium Spodumene Project - ASX:PLL was at A$0.15.

- Sept. 2022 - Piedmont Lithium: A Potential 60,000tpa U.S Lithium Hydroxide Producer By 2026 .

Piedmont Lithium 5-year price chart (PLL) - Price = USD $69.66 ( source )

Yahoo Finance

Note: 1 U.S Nasdaq listed PLL share = 100 ASX:PLL shares.

Piedmont Lithium's Australian Listing [ASX:PLL] price can be approximately calculated as PLL share price divided by 100, adjusted for the currency conversion from USD to AUD (E.g.: (69.66/100) x 1.42 = ~AUD 0.99).

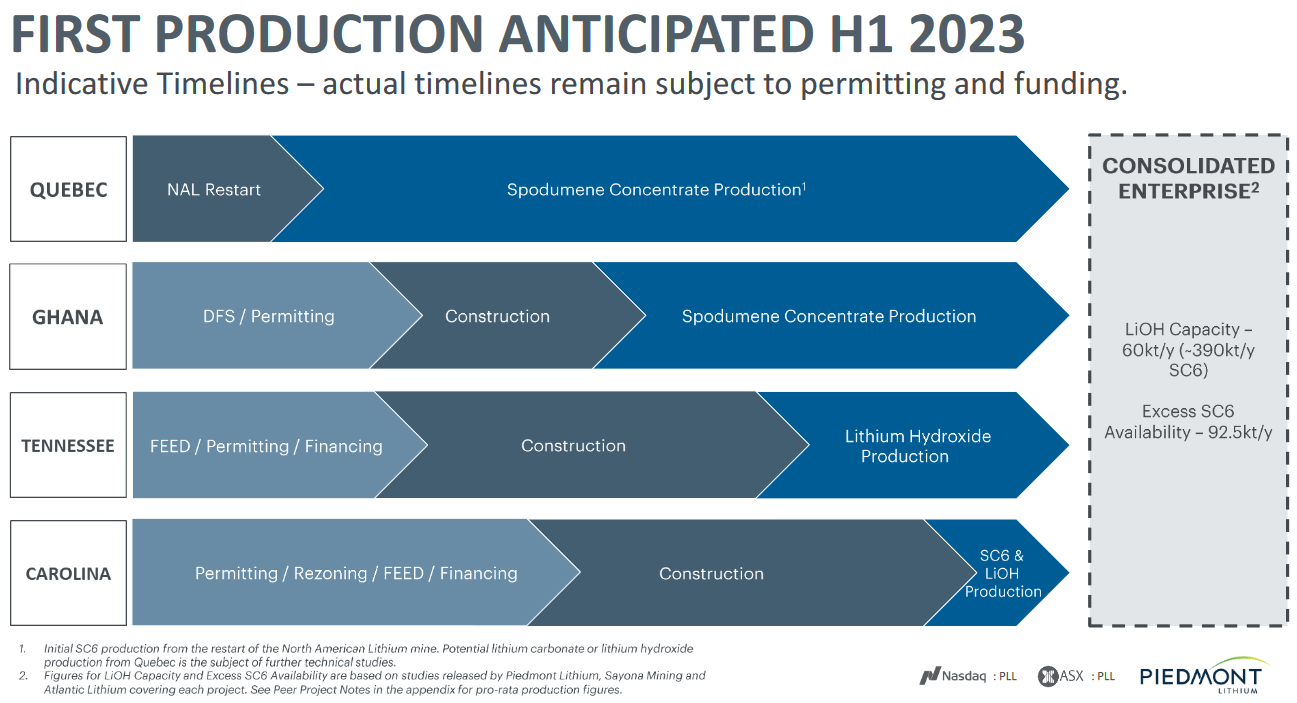

Piedmont Lithium's projects, JVs, and equity interests

Piedmont has the following key 3 lithium projects:

- Carolina Lithium Project [USA] (planned integrated mine and LiOH plant) (flagship) 100% owned . Spodumene Resource of 44.2Mt @ 1.08% Li2 O . Bankable Feasibility Study in progress. PEA result was a 30ktpa LiOH integrated operation, after-tax NPV8% of US$2.8b (assumes LiOH selling at US$22,000/t). Initial CapEx US$988m , OpEx US$4,377/t LiOH. Awaiting permitting and funding.

- 50% Ghana Project (earn-in from Atlantic Lithium) --> 100% Tennessee LiOH plant Project [USA] - Ghana Ewoyaa Project Resource is 30.1Mt @ 1.26% Li2 O . Ghana PFS resulted in a post-tax NPV8% of US$1.33b and initial CapEx of US$125m . Ghana DFS due in 2023 along with permitting and a mining licence. Ghana first production targeted for late 2024. Integrated Tennessee LiOH Project PEA after-tax NPV8% is US$2.2b . Tennessee Project initial CapEx US$600m , OpEx US$10,630/t LiOH. Tennessee LiOH production targeted for 2025, but this seems a little optimistic given it is not yet funded. It plans to be fed by Ghana spodumene.

- North American Lithium ("NAL") spodumene Project JV (Abiti Hub) (Piedmont has 25% project share, 75% is Sayona Mining) (Quebec, Canada) - Total resource of 119.0Mt @ 1.05% Li2O . Piedmont has favorable off-take rights (costs capped at US$900/t ) of the greater of 50% of production or 113,000tpa . Restart planned for Q1, 2023 and off-take to Piedmont from H1, 2023. Piedmont is also considering a JV LiOH plant in Canada, likely with Sayona.

Piedmont's equity interests include:

- 13.9% equity in Sayona Mining [ASX:SYA] ( OTCQB:SYAXF )

- 9.4% of Atlantic Lithium [LON:ALL] ( OTCQX:ALLIF )

Note: In the above project description, we have combined Ghana Project with Tennessee (LiOH plant) as they will work together.

Valuation breakdown on different scenarios (NAL & Ghana spodumene "only")

Piedmont Lithium's current market cap is US$1.255b (A$1.764b) with <1m debt.

The valuation section below looks at where Piedmont Lithium's stock price could potentially be in the next 4 years depending upon different pricing outcomes, assuming Piedmont achieves production targets for NAL and Ghana.

Note: The tables below exclude the added value of Piedmont's equity interests in Sayona Mining [ASX:SYA] ( OTCQB:SYAXF ) and Atlantic Lithium [ASX:A11] ( OTCQX:ALLIF )( US$250m as of Jan., 2023) and their cash ( US$118m as of Sept. 30, 2022). It also excludes Carolina Lithium and the next stage where Piedmont moves into lithium chemical processing (LiOH conversion) at Tennessee and elsewhere. ALL OF THIS IS A BONUS over and above what is discussed below, making the forecasts below effectively a near worse case scenario.

Piedmont Lithium's "forecast" net profit

| Year ending (spodumene attributable production) |

| Net Profit if spodumene selling at US$2,000/t [USD] |

| Net Profit if spodumene selling at US$4,000/t [USD] |

| Net Profit if spodumene selling at US$6,000/t [USD] |

| 2023 (65,000t) |

| 48.6m |

| 142.2m |

| 235.8m |

| 2024 (113,000t) |

| 86.6m |

| 249.3m |

| 412.1m |

| 2026 (228,000t) |

| 214.4m |

| 542.3m |

| 870.3m |

Note: Assumes a U.S corporate tax rate of 28% . Assumes 2023 and 2024 spodumene production from NAL (Piedmont's share of off-take) and 2026 ramped to full spodumene production from Ghana + NAL (Piedmont's share of off-take) reaches their production targets and is on time.

Note: Current spodumene contract prices are in the US$4-6,300 range. On Dec. 21, 2022, Pilbara Minerals reported their latest contract prices stating:

"Price reviews completed with major offtake customers, resulting in improved pricing outcomes, equating to an average SC6.0 equivalent price of approximately US$6,300/DMT (CIF China) when applying current pricing reference data."

Piedmont Lithium's potential market cap 2023-2026

| Year ending |

| Potential Market cap if spodumene selling at US$2,000/t [USD] |

| Potential Market cap if spodumene selling at US$4,000/t [USD] |

| Potential Market cap if spodumene selling at US$6,000/t [USD] |

| 2023 |

| 486m |

| 1.422b |

| 2.358b |

| 2024 |

| 866m |

| 2.493b |

| 4.121b |

| 2026 |

| 2.144b |

| 5.423b |

| 8.703b |

Note: Assumes Piedmont trades on a PE of 10x.

Conclusion from the tables

The table below shows the potential upside for Piedmont Lithium's shares assuming Piedmont can execute its short term plans with NAL and Ghana.

As shown above, by end 2026 (depending on the timing of the Ghana production ramp, etc.) Piedmont Lithium should potentially have a market cap of US$2.144b (bear case), US$5.423b (base case), and US$8.703b (bull case).

As shown below, by end 2026 the potential upside for Piedmont Lithium's valuation is 1.7x (bear case), 4.3x (base case), and 6.9x (bull case) .

Piedmont Lithium's potential upside

| Year ending |

| Potential upside if spodumene selling at US$2,000/t (bear case) |

| Potential upside if spodumene selling at US$4,000/t (base case) |

| Potential upside if spodumene selling at US$6,000/t (bull case) |

| 2023 |

| 0.39x |

| 1.1x |

| 1.9x |

| 2024 |

| 0.69x |

| 2.0x |

| 3.3x |

| 2026 |

| 1.7x |

| 4.3x |

| 6.9x |

Note: Based on the upside from the current market cap of US$1.255b. Assumes no equity dilution as Piedmont has sufficient cash to cover its share of initial CapEx at NAL and Ghana.

Note: All of this totally excludes the further potential upside from Piedmont's other planned projects (Tennessee LiOH plant Project and the US$141.7M DOE grant, Carolina Lithium Project, future LiOH projects at Carolina or NAL), equity interests, and cash ( US$118m as of Jan. 2023).

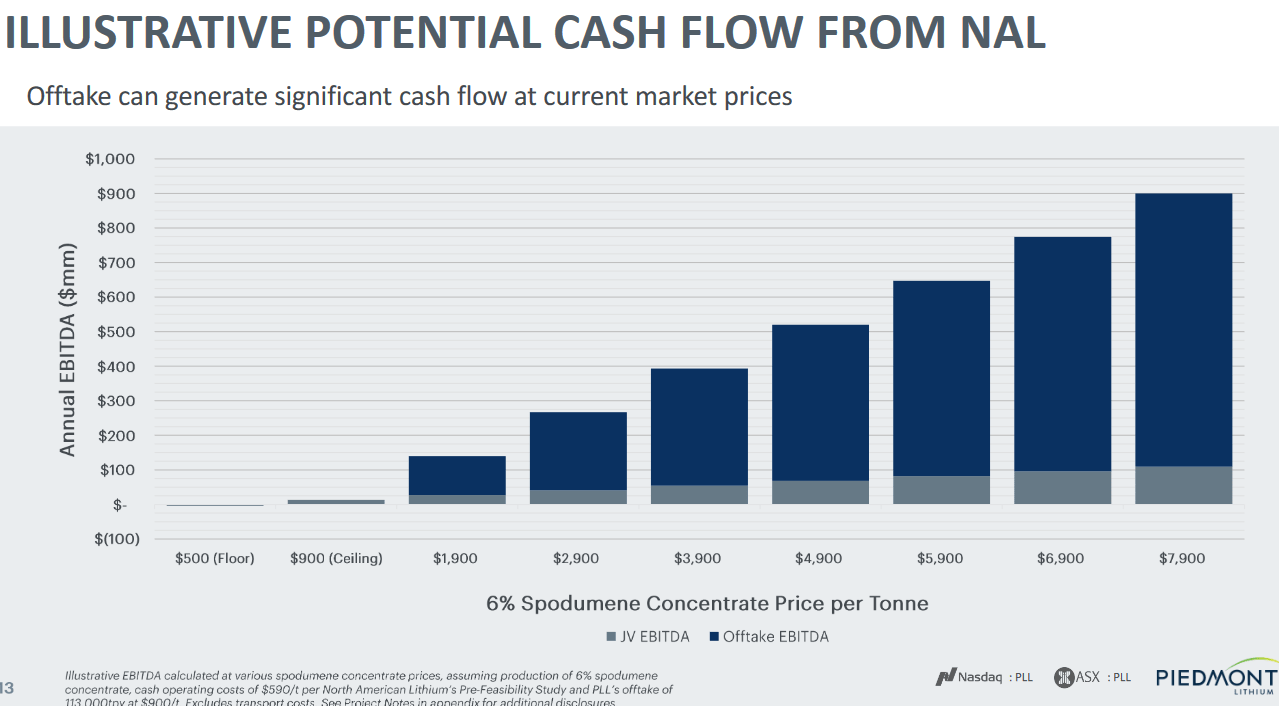

Piedmont is forecast to have very strong cash flows as it enters production soon, especially if spodumene prices stay at near US$5-6,000/t ( source ) - Eg: Spod at US$5,900/t equates to over US$600m of annual EBITDA for Piedmont from NAL only

{kind=link}

Analysts price targets

Yahoo Finance shows an analyst's price target of US$107.71 (1.55x upside) for U.S. listed PLL and A$2.05 for ASX listed PLL. Market Screener analyst price target is A$2.05 (2.1x upside).

Summary of Piedmont Lithium and its elements of value ( source )

{kind=link}

Piedmont valuation comparison ( source ).

The chart below shows Piedmont's production potential based on all three spodumene projects (NAL, Ghana/Ewoyaa, Carolina) as similar to lithium junior Liontown Resources [AS:LTR] ( LINRF ). While Piedmont's current market cap is US$1.255b , Liontown's is almost double at US$2.438b .

The chart below takeaway is that Piedmont trades on the lowest enterprise value of the group, yet has the 2nd highest production volume outlook. It appears the market assumes that the Carolina Lithium Project will never be permitted.

Piedmont valuation relative to peers ( source )

{kind=link}

Piedmont Lithium's targets for production ( source )

{kind=link}

Latest news

- Jan 31, 2023 - New NAL Milestone with Successful Ore Crushing Trial

- Jan. 16, 2023 - "NAL Restart Accelerates Towards Target."

- Jan. 3, 2023 - "Piedmont Lithium Amends Agreement with Tesla...

today announced that it has amended its agreement with Tesla, Inc. ("Tesla") to supply the U.S. automaker with spodumene concentrate ("SC6") from North American Lithium ("NAL"). Piedmont and Tesla have mutually agreed to amend their previous offtake agreement with the terms of this new agreement, which are binding for a three-year term and include an option to renew for another three years. Under the amended agreement, Piedmont has agreed to deliver approximately 125,000 metric tons of SC6 to Tesla beginning in H2 2023 through the end of 2025. According to the terms, the SC6 pricing will be determined by a formula-based mechanism linked to average market prices for lithium hydroxide monohydrate throughout the term of the agreement. The pricing received by Piedmont under the agreement with Tesla will be determined by market prices at the time of each shipment."

- Dec. 12, 2022 - North American Lithium Receives Remaining Permit Required to Restart Mining Operations.

A key takeaway from above is that the amended off-take agreement with Tesla is now from NAL, uses variable market price linked pricing (not fixed), and commences H2 2023. It is for 125,000t in total over 3 years, which is only part of Piedmont's production, so this leaves Piedmont open to sell and/or stockpile the remainder for their future Tennessee LiOH facility. In the current environment demand for spodumene from China is very strong.

The USA is ramping up battery factories this decade which will require ~725,000tpa of LCE supply. The Inflation Reduction Act rewards supply from North America or FTA countries ( source ).

{kind=link}

Risks

- Global, China, Europe, USA slowdown resulting in fewer EV sales, therefore, less demand for batteries and hence lithium.

- Falling lithium prices.

- The usual mining risks - Exploration, permitting, funding, production, partner, environmental risks. Project delays. The Ghana Lithium Project still has several hurdles to achieve before production including a DFS, permitting, mining license, & construction). Piedmont has had some permitting problems for their Carolina Lithium Project.

- Business risks - Management, liquidity, debt, and currency risk.

- Sovereign risk - Low in USA and Canada. High in Ghana.

- Stock market risks - Dilution, lack of liquidity (in Piedmont's case both ASX and Nasdaq have good liquidity for Piedmont's shares), market sentiment.

Further reading

- Feb. 2022 - Watch "Piedmont Lithium - Equity Overview with Rodney Hooper" on YouTube (video)

-

Piedmont Lithium website

- Piedmont Lithium company presentation - Jan. 2023

- Piedmont Lithium latest news

- Sept. 2022 - Pre-Feasibility Study Delivers Robust Project Economics Ewoyaa Lithium Project, Ghana, West Africa

- Nov. 2022 - Piedmont Lithium - A near-term cashflow generating North American lithium producer trading at a deep discount to its fair value

- Jan. 2023 - Piedmont Lithium nears first spodumene from North American Lithium joint venture (excellent video)

The U.S government is now highly motivated to accelerate lithium projects in the USA - Piedmont already received a US$142m grant for Tennessee LiOH Project and has two low interest rate loan applications in motion for Tennessee LiOH and Carolina Lithium ( source ).

{kind=link}

Conclusion

Piedmont Lithium is our number 1 stock pick for 2023 due to a superb lithium portfolio of projects and low valuation relative to the near term earnings potential. USA headquarters and favorable U.S government policies a bonus.

Valuation looks very attractive on a current market cap of US$1.255b.

By end 2023 we forecast Piedmont Lithium's base case (and near worse case) valuation ('only including NAL, so undervalues Piedmont for now) to be 1.1x (10%) higher. Yahoo Finance shows an analyst's 1 year price target of US$107.71 (1.55x upside) for US listed PLL and A$2.05 (2.17x upside) for ASX listed PLL. This assumes the NAL start up from mid-2023 goes to plan.

By end 2026 and based "only on NAL and Ghana production" alone, we forecast the potential upside for Piedmont Lithium's valuation is 1.7x (bear case), 4.3x (base case), and 6.9x (bull case) . From 2026/27 onwards there is significant potential further upside assuming Piedmont can bring on Carolina Lithium and several LiOH conversion plants (including Tennessee) in North America. These projects have the potential to at least double the above current upside figures, albeit not until later this decade. All of this excludes Piedmont's significant equity investments in Sayona Mining and Atlantic Lithium.

Risks revolve mostly around Piedmont Lithium advancing their projects, in particular permitting risks at Carolina Lithium, sovereign and development stage risks in Ghana, and raising the large CapEx needed for several North American projects (Carolina Lithium, Tennessee, other LiOH plants). Please read the risks section

Piedmont Lithium looks likely to become one of the top 3 U.S lithium producers this decade. We view Piedmont Lithium as a great spec buy, suitable for a 5 year plus time frame.

As usual all comments are welcome.

For further details see:

Why Piedmont Lithium Is Our Number 1 Stock Pick In 2023