DGX - Why Quest Diagnostics Isn't A 'Buy' My Oh My

Summary

- I've been covering Quest Diagnostics for some time. While it can be argued that the company has beaten estimates, it's also clear that positive catalysts are few.

- I've been neutral going on for a year now at this time, and I see no reason to change my tune going into early 2023.

- Here are the reasons why going into Quest Diagnostics in 2023 is a bad idea, as I see it, and why you should stay away until we have more clarity.

Dear readers/followers,

Quest Diagnostics ( DGX ) is far from a "bad" company. It's qualitative as heck, as a matter of fact. But the problems the company has goes beyond some of the recent trends. Since my last article, the company has actually seen some decent performance - if index development at 9% can be called "decent". However, this has not taken away from the company's overall challenges - and those are what we're going to be taking a closer look at in this particular piece.

By the end of it, I believe you'll agree that DGX stock offers very little in terms of compelling arguments for a long-term investment - which is what we want to do.

Quest Diagnostics for 2023 - A "No"

So, there are well-established reasons why the company, from a fundamental point of view, can be considered a solid "BUY". Many of those arguments can be found in previous articles I've published on DGX, such as this one found here.

The company's role has only evolved since posting that particular piece. It's achieving a role as a leader in diagnostic IS in the healthcare field, which cannot be argued with - at least, I won't be trying to argue with it.

{kind=link}

DGX IR (DGX IR)

The company estimates to manage 2022E revenues of nearly $10B even without the massive tailwind we saw from COVID-19 - in no small part due to the trends that we see above. Quest Diagnostics seems, on a surface level, to have "it all". It has driven and capable management with decades of experience - centuries, if you add it all up. It has dividends, and it has a somewhat timeless set of business segments, even if we can see that some of them really go up and down quite a bit.

However, the market that the company is in is a very low-growth industry. Even the most optimistic forecasts, reading science-specific journals and publications as well as estimates, forecast no more than a 2-3% growth rate on a CAGR basis from 2022E. These include the company's own numbers. That's GDP-type growth rates if that (not now, for certain).

However, DGX is also at the heart of an incredibly fragmented, $100B+ global lab market. The US alone has an $80B+ lab market, where Physician lab services, the area that the company is in, account for 64% and is worth $52B. This in turn is split into independent labs and POL/Other and Hospital outreach. Independent is over 50% here, and that's where DGX operates at this time a $28B market in the US alone, where DGX has almost 25% of everything. That's an impressive share of the pie.

However, due to the meager growth rates estimated here, there is a significant cap on what can be earned by the company through growth here. And while the company has been expertly managing and pushing its relationships...

{kind=link}

DGX IR (DGX IR)

...and other things seem to be working extremely well also...

{kind=link}

DGX IR (DGX IR)

..."profit" in itself does not mean "investable." These are two very different things, and DGX is a great lesson for those not well-versed in value investing to see what a company may have going for it, and where it might go.

The latest set of results was quite excellent. The company increased its buybacks and increased the dividend by over 7.5% as well. It beat both on an EPS and revenue basis. However, while both of these beats were true "there" the company failed to address, or respond to one of the core issues I have been talking about for over a year with regard to DGX.

What happens Post-COVID?

DGX is a massive COVID-19 beneficiary. The company's numbers have been inflated for years due to the positive business volume from the COVID-19 trends, and while this has been absolutely superb for the business itself, it does throw a wrench into longer-term trends and valuation, because what it means is that what goes up, must come down. Unless the company has found a way to boost earnings and retain the non-recurring levels we saw during the pandemic.

From the earnings, and from the current set of forecasts, it's clear that DGX has not found a replacement for this tailwind, and the market was disappointed despite good bottom-line results.

{kind=link}

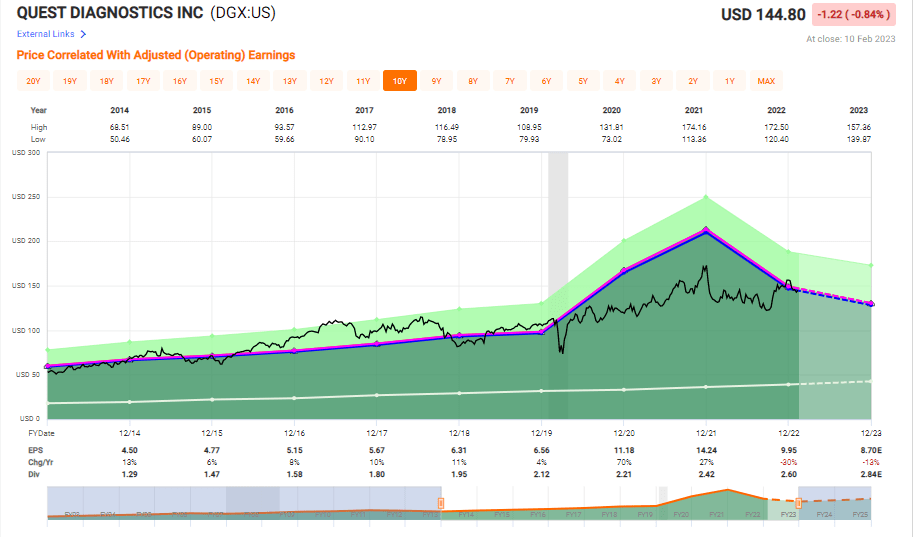

DGX Valuation (F.A.S.T Graphs)

2022E is a 30% decline, and 2023E is set to bring another double-digit set of declines. It's still a good result from a 10-year perspective, but this does not help investors who bought at the top or as the company was relatively richly valued.

The fact that the company still relies on COVID-19 testing is clear. Let's be perfectly transparent, it's still $1.4B in 2022 so far, and that's an amount of sales revenue that needs to be shed from the annual numbers. And while EPS exceeded consensus, there's still not much one can say when the result represents a 43% decline in operating income YoY, and a full-year net income decline of 53%, under around a billion dollars for the full year.

DGX has been trying to keep its focus on growth by reinforcing its base business and increasing productivity and margins - but this is hampered by the fact that we're in an incredibly inflationary and cost-heavy sort of macro. That's before the company's own estimates call for a 2023E decline in COVID-19 testing of upwards of 88%, which would imply under a billion in test revenues.

The initial guidance from the company calls for earnings to go as high as $9/share for the 2023E Fiscal. This would still be significantly above the pre-COVID-19 numbers, but it would also call for close to a double-digit decline YoY, at the most positive company guidance.

The company's fundamentals are absolutely solid - BBB+ and sub-50% debt/cap, but the dividend is meager, to say the least, at 1.96%. I could have accepted this with a higher conservative upside in terms of EPS growth, but this is not to be found in DGX either.

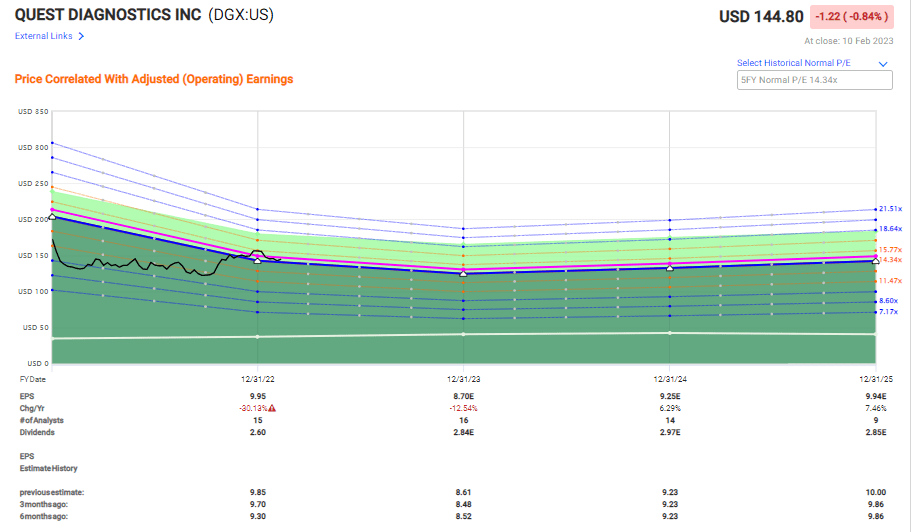

The simple fact is that DGX is set to normalize its earnings from a non-recurring top, which looks the following way when put into a graphical representation.

Quest Diagnostics Valuation - Any Upside is Hard to Find

{kind=link}

F.A.S.T graphs DGX (F.A.S.T Graphs)

This graph is basically saying the following - if historical valuation patterns in terms of P/E hold, which they statistically tend to do for DGX, then the future 2-3 years are unlikely to bring much upside beyond the yield, and in fact negative upside without the dividend of negative 0.55% per year on a 14.34x P/E, which is the average forecasted here based on these estimates.

While you may argue with the models and methods used, let me assure you that any thesis where this one shows a negative RoR , to begin with, that's a tough one to get positive enough to invest in.

Because let's also be clear here, it's not just P/E or other similar, simple multiples where we have difficulties finding an upside. No matter where you end up looking in terms of its peers, DGX isn't particularly appealingly valued in terms of its potential. Usually, pharma and healthcare companies can point to above-GDP-type growth - DGX cannot. In fact, in the next years, it's unlikely it can achieve GDP on an average basis.

I would classify Quest Diagnostics to be a healthcare provider and services-type sector, which contains such peers like Lab Corp of America ( LH ), Sonic Healthcare (SKHCF), Premier (PINC), and others. The problem is that based on this peer group, the company is still higher-valued than both the domestically-listed and internationally listed peers.

That's strike two.

Analysts following the company aside from me don't like DGX particularly much either at this valuation. The range for the 14 analysts from S&P Global following DGX starts at $125 and goes to $175, with an average of around $142.5. That's below the current share price as I am writing this, of almost $145. Only one analyst is at an "outperform" here, with 4 at "BUY", the rest at "HOLD" and even 2 at "SELL".

DCF is another method I use to try and achieve valuation-related clarity. Unfortunately, there is nothing to like about DGX in a conservative DCF model as it's being priced today. I forecast it at a 9-10% discount rate, allowing even an above-3.5% terminal growth rate for illustrative purposes. You still get a range from $110 to around $130 at most - and you'll note most targets are significantly higher than that - including mine. I would probably be more interested at $110/share than I am today.

I've scoured revenue multiples, EBITDA multiples, levered free cash flow yield, tangible BV, and enterprise value multiples. There is nothing in the math that supports this sort of premium on the company, and I believe the market knows this. Just as an example, DGX is trading at a 2.3x revenue multiple. The 15+year mean for DGX is below 1.95x, and here we're talking about extremely long-term trends.

In order for this sort of pricing to be justified for DGX, there would have to be a second pandemic that would ensue similar sales revenue patterns as we saw during COVID-19. We do not have that. What we have is a company that seeks to adjust to a reality where its pre-COVID-19 EPS was around half of the top we saw in 2021, and there will, as I see it, be further normalization here.

When things go back down to more solid, humane levels, I will be the first one to call this solid business a "BUY" if I can see my way to earning double digits conservatively.

For now, though, I don't view this as being even remotely possible, no matter how I go about estimating the earnings here.

This leads me to my current thesis for DGX.

Thesis

- This is a great player in the healthcare services/lab market. It has the proven and admirable ability to make attractive returns from superb customers and markets. At the right price, this company is a definite "BUY" to me.

- However, at $140+, this company is too expensive. I currently don't see an appealing RoR for the company based on current valuations.

- I would be interested at $110-$120/share.

- DGX is a "HOLD" and should be avoided.

Remember, I'm all about :

1. Buying undervalued - even if that undervaluation is slight, and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

2. If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

3. If the company doesn't go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

4. I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them ( italicized ).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

None of the valuation-related multiples, which make up the core of my approach, are fulfilled here - which makes this one a no-go.

Thank you for reading.

For further details see:

Why Quest Diagnostics Isn't A 'Buy', My Oh My