VNQ - Why REITs Will Likely Beat Other Stocks In 2024

2023-10-15 09:00:00 ET

Summary

- REITs have sold off to their lowest valuations in a decade.

- Stocks, on the other hand, remain priced at high valuations.

- I explain why REITs should pummel stocks going forward.

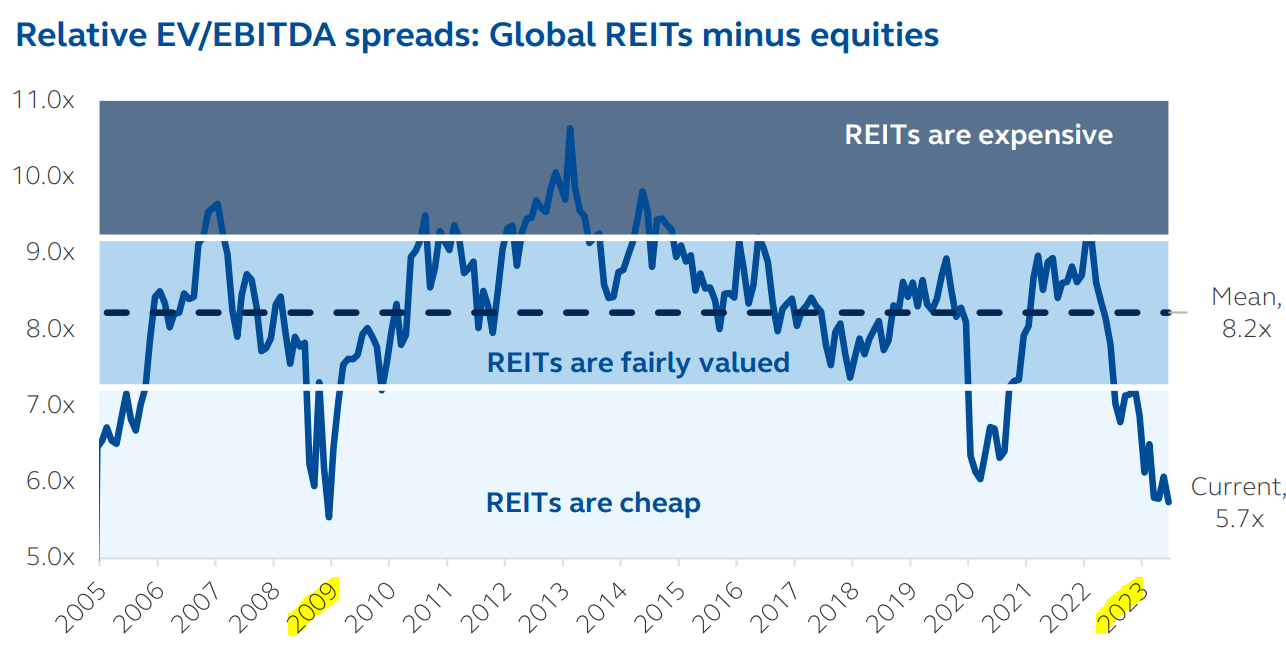

REIT share prices dropped by another 10% over the past month, and as a result, their valuations have now reached levels not seen since the great financial crisis:

{kind=link}

This chart is especially interesting because it compares the valuations of REITs vs. stocks. It clearly shows you that the market appears to think that REITs are far more sensitive to interest rates than regular stocks.

As interest rates rose, REITs ( VNQ ) crashed... but regular stocks ( SPY ) were barely impacted:

I believe that this is a clear case of market inefficiency.

It would imply that only REITs use debt and only REIT cash flows should be discounted for the now higher interest rates.

In reality, nearly all companies use some debt on their balance sheet, and the discount rates of all valuation models should be adjusted higher.

In fact, I would even argue that REITs should be far less impacted than most stocks because REITs use little debt with an average LTV of just 30% and debt maturities are long since they are secured by real estate. In comparison, regular companies will typically use more debt, and their maturities aren't nearly as long.

Moreover, it is worth remembering that interest rates only surged because inflation got out of control. And what companies benefit the most from inflation? It is real asset-heavy companies like REITs and this explains why their cash flows and dividend payments have kept on rising even as their share prices crashed.

NAREIT

Finally and perhaps most importantly, the cash flows of most stocks, and especially growth stocks, have a higher duration and therefore, the impact of rising interest rates should be far greater on them. A typical tech stock ( QQQ ) may not earn much profit today, but they are expected to grow rapidly and earn significant profits sometime far in the future. Such distant profits should be now far less valuable because of the time value of money. A higher discount rate will have a far greater impact on the profits of year 10 than the profits of year 1.

Now explain to me why REITs, which generate a lot of profits today, have seen their valuations drop far more than tech stocks, which are expected to generate significant profits far in the future.

This doesn't make sense and there is even proof to back this up.

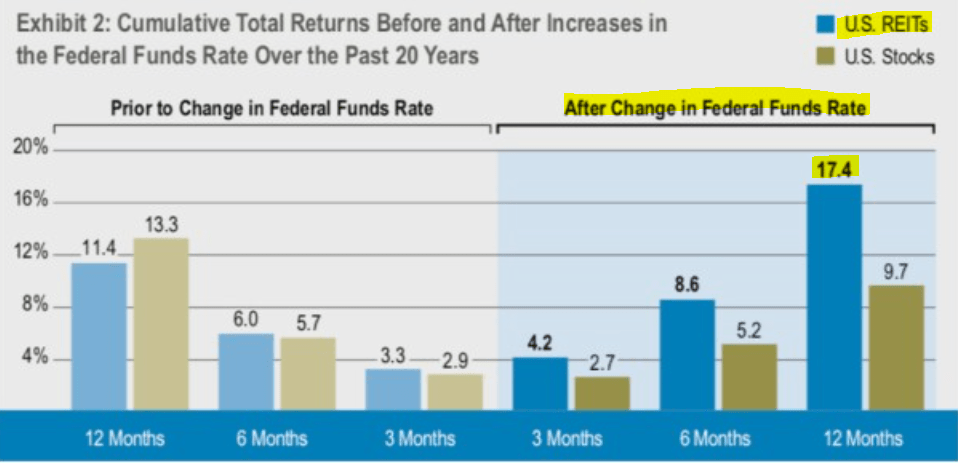

Historically, during most time periods of rising interest rates, REITs have performed far better than other stocks and generated strong positive returns as you will see in the chart below:

{kind=link}

But this time, REITs crashed as if none of this mattered:

Even the bluest blue chips like Realty Income ( O ), Crown Castle ( CCI ), and Alexandria Real Estate ( ARE ) have crashed. That's despite having fortress BBB+/A- rated balance sheets and growing cash flow:

I believe that the market has simply gotten it wrong.

The vast majority of market participants appear to believe that REITs are far more sensitive to interest rates than they really are, and this narrative has been self-fulfilling in a very strong way.

But it is not just REITs. It seems that anything with a dividend has crashed as if paying a dividend meant that the business should be suddenly devalued because interest rates have risen.

In reality, the dividend is just a capital allocation decision and it shouldn't have such an impact on the valuation of a company.

What appears to have happened here is that dividend-paying stocks have been more heavily impacted, not because of their fundamentals, but because their investor base is income-focused.

They bought a lot of these stocks in recent years as bond replacement when interest rates were low, but as soon as they got the chance, they sold these stocks, irrespective of their fundamentals, and reallocated the capital into bonds, which now offer attractive yields.

Growth stocks, on the other hand, did not experience the same sell-off because their investor base isn't income-focused so they don't care about interest rates nearly as much.

As a result, I believe that REITs are now heavily underpriced even as most growth stocks have become overpriced and this is perfectly captured by the chart below:

This chart was produced by Principal Asset Management , which is one of the biggest investment firms in the world. They explain that:

"It appears contrarian to favor REITs today compared to the negative news headlines about real estate, but these challenges are well understood in REIT markets. When sentiment does shift back in favor and relative valuations are too cheap to ignore, REITs are poised for potentially strong fund inflows. After all, the number of potential buyers is outnumbering the remaining sellers by a bigger margin every day."

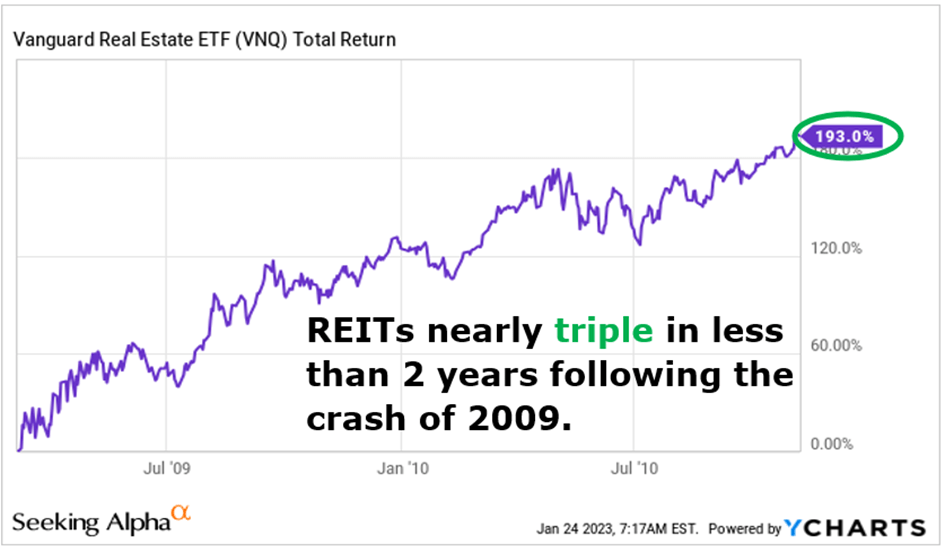

I would go a step further and say that I think that this is a once-in-a-decade chance to win big by investing in REITs.

The last time they were so cheap was following the 2009 crash and REITs then tripled in the next two years as they recovered:

{kind=link}

Today, REITs are once more heavily discounted and that's despite enjoying strong fundamentals for the most part. They have behaved as if they were bonds because their investor base is income-focused, but as we approach the end of this rate hiking cycle, the narrative will change again and this will likely push REITs to much higher levels as total return-oriented investors join to take advantage of the discounts.

But even if you don't buy into that, you need to ask yourself:

Which investments offer the best prospects going forward?

Would you rather buy REITs with strong balance sheets and growing cash flow at just 12x cash flow on average?

Or would you prefer to buy Tech stocks that have failed to reprice for the higher interest rates and still trade at 40x cash flow?

I believe that the decision is simple.

REITs offer significant margin of safety following their recent crash and this sets them apart in today's market environment.

For further details see:

Why REITs Will Likely Beat Other Stocks In 2024