VTI - Why Short-Term Treasuries Should Continue To Outperform The Overall Market

2023-10-17 11:54:06 ET

Summary

- Since the Federal Reserve began their current policy of monetary tightening in March of 2022, short-term treasuries have easily outperformed equities.

- Given the central bank's history of errant forecasts and triggering frequent "accidents" in the economy and markets, chances of a "soft landing" are low.

- A review of recent Federal Reserve mistakes and why short treasuries should continue to provide better returns than stocks follows below.

If the federal government is an addict, then the Federal Reserve System is its enabler. " — Thomas E. Woods Jr.

I have been fascinated by the markets since an early age. I was watching Wall Street Week with Louis Rukeyser on PBS before I was old enough to drive. At the time, I did not understand the show's and panelists' intense focus on the Federal Reserve and monetary policy.

After 40 years of investing, not only do I understand the obsession, I share it. Of all the things that can influence the direction of equities, monetary policy and the actions/commentary of the Federal Reserve remain the undisputed 800lb gorilla in the room.

There are a few things I have observed over four decades of watching and investing in the markets around the Federal Reserve. These boil down to three key tenets.

The Fed Controls The Punch Bowl

When monetary policy is accommodative, equities and risk assets like real estate almost always provide higher than average annual returns. The latest instance of this was in 2020 after the lockdowns were lifted through 2021. Equities boomed thanks to near zero interest rates and the central bank's quantitative easing, or QE.

National Association Of Realtors

From the start of the third quarter of 2020 to the end of 2021, the S&P 500 rose just over 55%, including dividends. Easy money also triggered an avalanche of IPOs and SPACs, most of which destroyed a tremendous amount of shareholder value once the Fed pivoted and started to tighten monetary policy early in 2022.

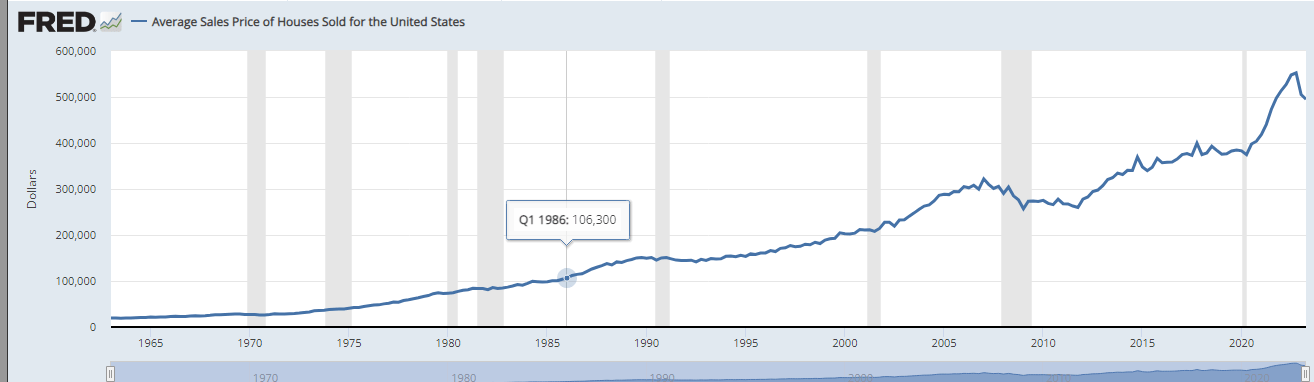

U.S. Housing Prices (St. Louis Federal Reserve)

{kind=link}

Housing prices also exploded across the country. One of two reasons, housing affordability is now at all-time lows, the other being the highest mortgage rates since the turn of the century.

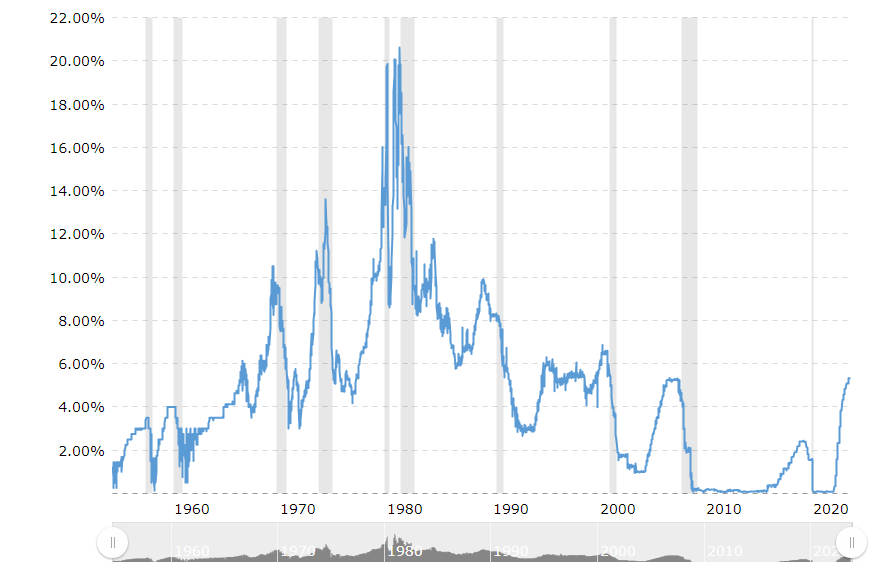

FreddieMac

Of course, when the Fed takes away their punch bowl, equities and risk assets underperform. At the close of the week in Mid-March of 2022, when the central bank first started to lift the Fed Funds rate of .25% to .50% at the time, the Dow Jones Industrial Average (DJI) stood at 34,754, the S&P 500 (SP500) was 4,463 and the Nasdaq 100-Index (NDX) traded at 13,893. The same averages started trading Tuesday morning at DJIA 34,069, S&P 500 4,389 and Nasdaq 15,237.

So, basically the Nasdaq has gained 10% and both the DJIA and S&P are down slightly since Chairman Powell first began this course of monetary tightening. Other parts of the markets have performed much worse, especially the higher beta parts of the market. The small cap Russell 2000 Index (RTY), as but one example, is down some 15% since the Fed Funds rate first started to go up. Even the 10% rise in the Nasdaq is less than what it appears. Take away the massive gains from the likes of Microsoft ( MSFT ) , Nvidia Corporation ( NVDA ) and the rest of the mega caps that make up the " Magnificent Seven" and returns from the tech heavy index turn negative.

Magnificent Seven Market Cap From September 2022 to September 2023 (Seeking Alpha)

The Federal Reserve Isn't Clairvoyant

To say the central frequently errors in its forecasts and economic commentary is being generous. Probably the most famous of these glitches was Chairman Bernanke's statement that the Subprime Crisis was " contained" in March of 2007. Ironically almost 15 years to the day that Chairman Powell began the monetary tightening phase we are currently experiencing. And who can forget all the reassurances from the Fed and its board members throughout most of 2021 that inflation was " temporary" and " transitionary ." Something that could have been easily dispelled by just taking more frequent trips to the grocery store.

"Accidents" Almost Always Happen

The one consistent thing about Federal Reserve is sustained monetary tightening almost always triggers a bear market and often an economic recession. The most notable example in my lifetime is the Great Financial Recession a decade and a half ago.

{kind=link}

As you can see above, the Internet Bust of early 2000 was preceded by a series of rate hikes in the late 90s and the massive rise in the Fed Funds rate in the late 70s led to the double-dip recession of 1980-1982. Importantly, monetary policy also acts with a considerable lag. As but one example, the Federal Reserve stopped raising rates in April of 2006. Bear Stearns did not occur for nearly two years after that last rate hike and " Lehman Moment" happened nearly two and a half years later.

I noted in an article yesterday how monetary policy was already causing a large spike in delinquency rates in commercial real estate loans, a situation that will only get worse with time as some $2.5 trillion in CRE debt needs to be refinanced at much higher rates over the next five years.

Morgan Stanley Research, Trepp

This is why I have 50% of my portfolio in short-term treasuries at the moment. They currently yield 5.5%, which I expect to continue to outperform the overall market and that yield is nicely above the current rate of inflation (3.7% according to the September CPI report ). They also pay a half of a percent over the two-year treasury (US2Y) currently.

I see no reason to lock in my money for any more than three to six months. The federal government is spending like drunken sailors, amassing an almost $2 trillion deficit in FY2023 despite two percent GDP growth. The treasury has some $7.6 trillion worth of government debt to refinance over the next 12 months as well.

Given this, it is hard to see short term treasury yields coming down meaningfully, outside a recession. An economic contraction would also knock equities down significantly, which would provide much lower entry points for my treasury holdings once they expire. Given the Federal Reserve's history of achieving few "soft landings," the probability of a recession in 2024 is high.

A large holding of short-term treasuries is hardly a " sexy" portfolio configuration, but 40 years of following the Fed has taught me it is a prudent one.

I was reading in the paper today that Congress wants to replace the dollar bill with a coin. They’ve already done it. It’s called a nickel. ”? Jay Leno.

For further details see:

Why Short-Term Treasuries Should Continue To Outperform The Overall Market