PREKF - Why Sitio Royalties Should Be On Warren Buffett's Radar

2023-05-08 15:16:54 ET

Summary

- Sitio Royalties Corp. owns mineral and royalty interests in top-tier oil and gas assets across the United States.

- It's a huge player in the Permian Basin, which Warren Buffett has invested heavily in through his Occidental purchase.

- Sitio is a lower-risk, more efficient company than oil & gas operators, however, and should be on his radar.

- I break down the investing case for Sitio Royalties below.

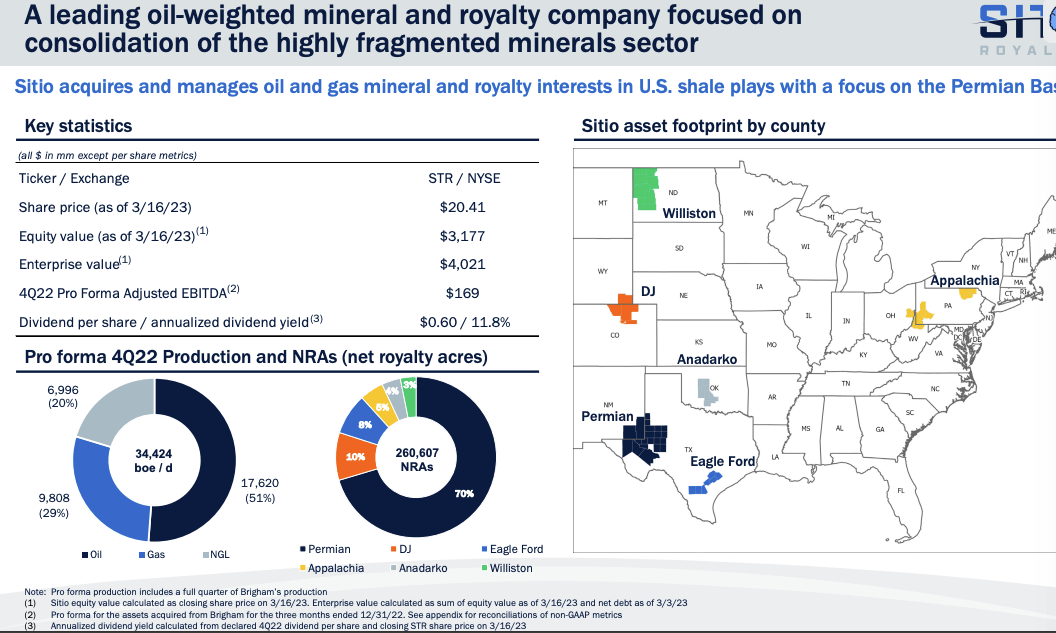

Sitio Royalties Corp. ( STR ) owns various mineral and royalty interests in top-tier oil and gas assets across the United States. As the largest publicly traded oil and gas royalty company, it has a market capitalization nearing $4 billion, with substantial long-term growth potential.

The company's extensive portfolio includes more than 260,000 net royalty acres, with over 180,000 of these acres situated in the prolific Permian Basin, which spans western Texas and southeastern New Mexico.

The region's high productivity makes it an attractive location for oil and gas operations, and Sitio Royalties' ownership of high-quality royalties and balance sheet strength puts it in an enviable position to capitalize on the region’s oil-producing potential.

With a current yield nearing 10% and low-cost production growth coming, here’s why I think Sitio is the best oil & gas royalty company to invest in today - and why it could be a prime addition to Warren Buffett's (or any investors) portfolio.

What are Oil Royalties? A Quick Overview

If you’ve been an investor in the precious metals sector, you likely already know how a royalty works. The concept is quite similar in the oil & gas sector.

Royalty holders own a share of the resource or the revenue generated from it. Unlike operators like Occidental Petroleum Corporation ( OXY ) or Exxon Mobil Corporation (XOM) - who are responsible for exploring for, developing, and producing oil, and thus incur substantial capital expenditures - royalty holders do not bear these operational responsibilities. However, they still reap the benefits of production by retaining a percentage of the income the oil well generates.

This is a lower-risk business model compared to operating oil and gas, because royalty holders get that benefit of the oil production, without any direct participation in its production and the associated costs.

Therefore, royalty holders profit from the production while avoiding many of the financial and operational risks typically faced by operators.

It also allows these companies to adopt a very lean business structure, requiring far less headcount to operate. The main risk, of course, is commodity price risk, as lower oil & gas prices obviously impact the earnings of the royalty holder.

Charlie Munger of Berkshire Hathaway Inc. (BRK.A) is probably the most famous investor in an oil royalty. In Berkshire’s recent annual meeting, Munger reflected on a tremendous royalty investment he made decades ago. Munger and his partner each invested just $1,000 to purchase oil royalties at an auction. That trade has worked out pretty well, as it currently generates an annual income of $70,000!

Oil royalty company sector breakdown

| Company |

| Market cap |

| Sitio Royalties |

| $3.9 billion |

| Permian Basin Royalty |

| $1.148 billion |

| Dorchester Minerals |

| $1.11 billion |

| Sabine Royalty |

| $1.03 billion |

| Kimbell Royalty |

| $1.02 billion |

The U.S. oil and gas royalty sector is surprisingly small, especially when compared to the precious metals royalty and streaming sector.

Sitio is by far the largest player in the sector, with a market cap nearing $4 billion, as of writing. Other top companies include the Permian Basin Royalty Trust (PBT), Dorchester Minerals, L.P. (DMLP), Sabine Royalty Trust (SBR), and Kimbell Royalty Partners, LP (KRP).

In Canada, Freehold Royalties Ltd. ( FRHLF ) and PrairieSky Royalty Ltd. ( PREKF ) are the top players.

This combined market cap of oil & gas royalty companies is pretty small compared to gold & silver. Take Wheaton Precious Metals Corp. (WPM), for example, a top gold royalty stock that carries a $23 billion market cap alone, almost more than the entire mineral and royalty sector!

Why is this sector so small? One potential reason: Oil and gas royalties are largely owned by private individuals and companies, and it’s a highly fragmented space.

{kind=link}

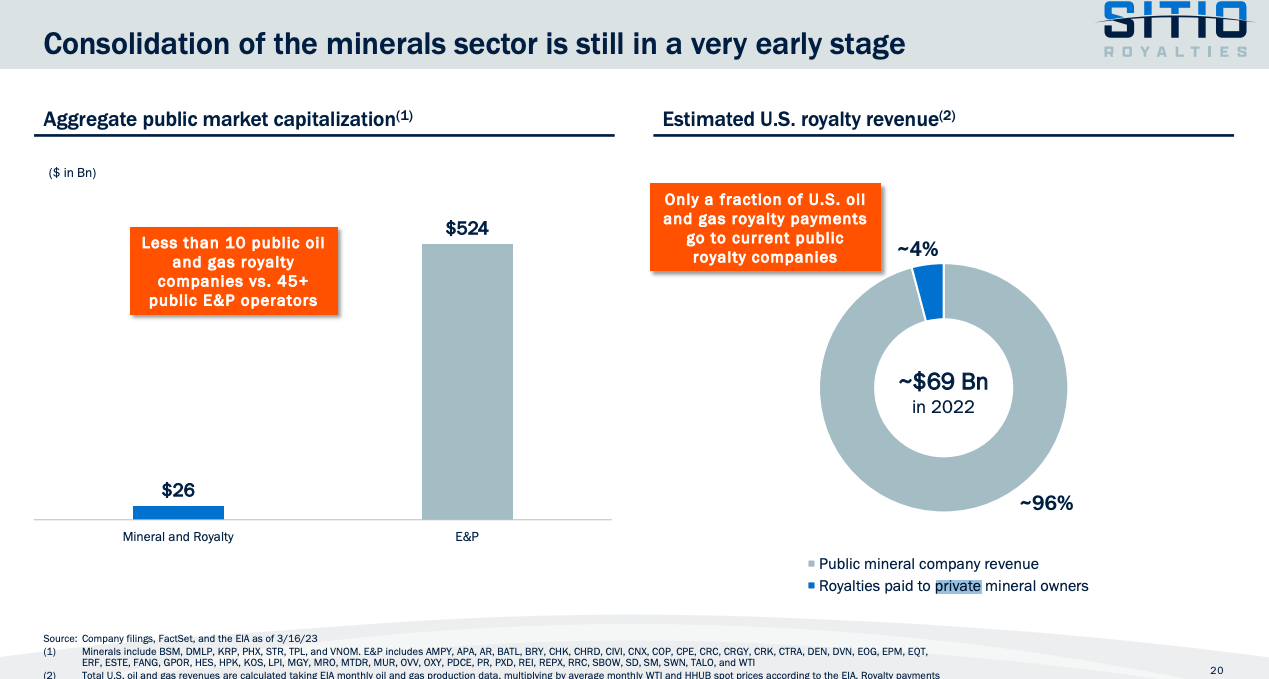

Sitio points out in its corporate presentation that just 4% of all oil and gas royalties in the U.S. are paid to public mineral companies in a $69 billion market. And compared to the oil and gas sector ($524 billion in size), the mineral and royalty sector is minuscule ($26 billion).

But Sitio believes there is potential to consolidate much of the sector. It appears to have already begun executing this strategy with the recent acquisition of Brigham Minerals.

Why Sitio? 3 Reasons to Buy The Stock Now

I believe Sitio is the best oil & gas royalty stock for several reasons, and the type of company Warren Buffett and Munger would invest in.

1. Permian Basin exposure

{kind=link}

First, Sitio Royalties owns interests in production from the Permian Basin, one of the biggest & most prolific oil-producing regions in the United States. The basin is highly regarded due to its productivity, low production costs, and upside potential.

The Permian Basin is a huge oil producer and accounts for nearly 40% of the country's oil production and almost 15% of its natural gas production, as reported by the Federal Reserve Bank of Dallas.

Sitio owns over 260,000 net royalty acres ("NRAs"), over 180,000 of which are located in the Permian Basin. That equals approximately 70% of its NRAs, far exceeding any other county.

Warren Buffett is one of many investors bullish on the Permian Basin, demonstrated by his ownership of Occidental Petroleum, a large player in the region, which Buffett called out during Berkshire Hathaway's latest annual meeting .

Spanning approximately 250 miles in width and 300 miles in length, the Permian Basin encompasses more than 7,000 fields across West Texas. According to Chevron Corporation (CVX), the basin's unique rock characteristics contribute to its position as one of the world's most productive fields.

Also, investors should note that the Permian Basin is home to Enhanced Oil Recovery (“EOR”) techniques that are being operated by Occidental and other companies. These techniques can increase the recovery of oil while also reducing the environmental impact of oil production.

It’s bullish news for Sitio because it could increase production in the region, encourage future development and production in the region, and make Sitio a more viable long-term investment.

2. Extremely profitable company

Not surprisingly, Sitio’s profitability metrics are through the roof due to its low cost structure and higher oil prices. In particular, I’m blown away by its gross profit and EBITDA margins compared to the sector.

| Metric |

| STR |

| Sector Median |

| Gross Profit Margin |

| 99.12% |

| 46.48% |

| EBIT Margin |

| 63.05% |

| 23.41% |

| EBITDA Margin |

| 91.32% |

| 35.60% |

| Net Income Margin |

| 49.82% |

| 15.56% |

Last quarter saw Sitio's net income fall by 93%, but that was only due to one-time expenses related to its Brigham Minerals merger deal. Adjusted EBITDA still came in really strong at $93.1 million, despite a 17% drop in oil prices compared to the prior year's quarter. However, when including the impacts of the merger, its adjusted EBITDA would have been $169 million.

Those strong results led to Sitio declaring a Q4 2022 dividend of $.60 per share, which, at the time of the announcement, resulting in a dividend yield of 9.9%.

For 2023, Sitio expects to produce between 34,000 - 37,000 boe/d, and aims to reduce its G&A expenses. While there are still likely plenty of acquisitions it can evaluate in the current market environment, the company has indicated it will prioritize debt repayment for the remainder of 2023. Its debt is nearing $1 billion following the merger with Brigham.

Over the past 3 years, Sitio's adjusted EBITDA per boe has ranged from $20 to $70, depending on oil prices, and it's a highly profitable company at various oil price scenarios, so its debt doesn't worry me.

3. Efficient business model

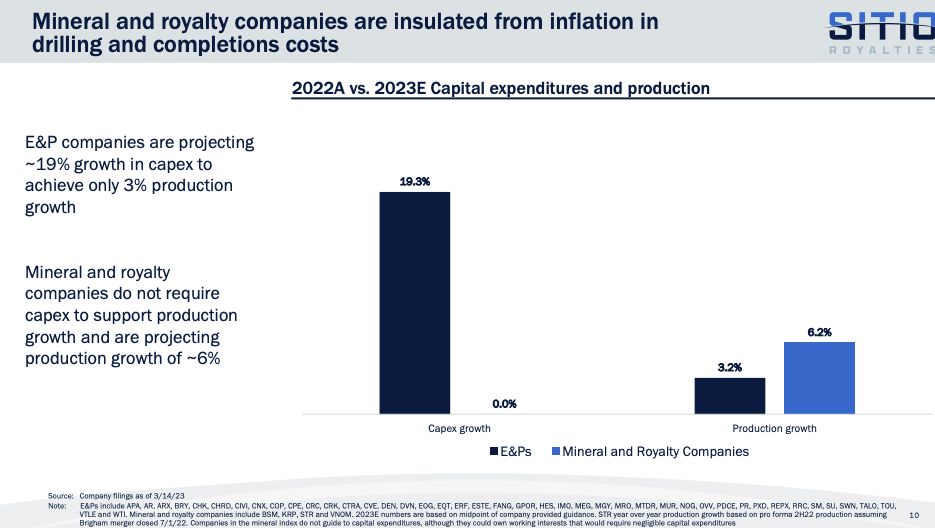

Related to profitability, this is an extremely efficient company, meaning it can operate and grow its revenues and cash flows without requiring much capital or human effort.

Although it may not be undervalued at the moment, it remains a high-quality firm with valuable royalty assets. Its non-operator business model allows it to minimize risk and achieve some of the highest margins in the oil and gas industry.

{kind=link}

{kind=link}

As a royalty holder, Sitio is not responsible for development capex and is largely shielded from the risks associated with being an operator. It does not have any physical operations. This leads to an extremely efficient business model.

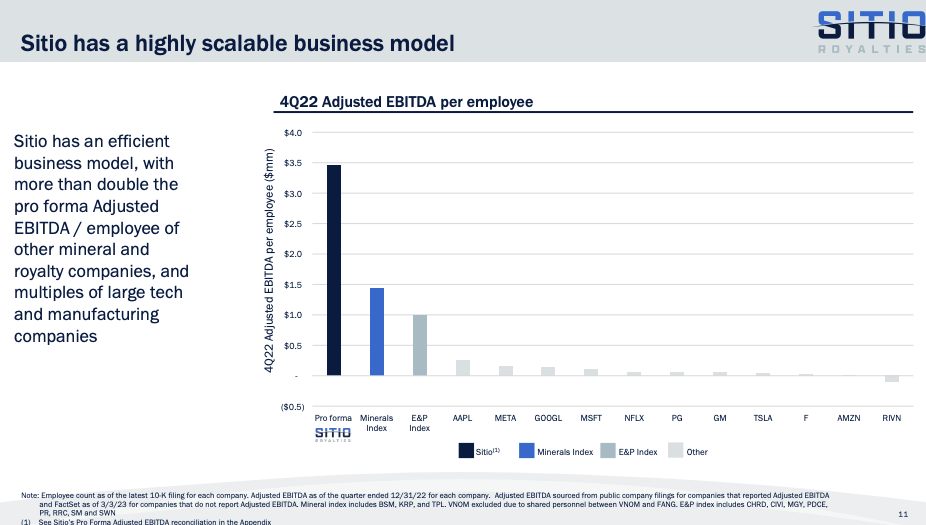

According to Sitio's corporate presentation (slide 11, pictured above), the company's adjusted EBITDA per employee is close to $3.5 million for each of its 49 employees. This figure is significantly higher than that of any tech company or energy producer, as it points out in its slide above, which further highlights Sitio's outstanding efficiencies and the potential for high cash flows and increased dividends in the future.

Sitio Royalties: The Bottom Line

Sitio Royalties is a very profitable and efficient oil royalty company that pays a substantial dividend (~10% yield) that is sustainable at spot oil prices. It owns prime royalties in the Permian Basin, which has the backing and support of Warren Buffett through his Occidental ownership stake.

But Sitio Royalties Corp. is arguably a better investment than any oil & gas operator in the Permian Basin for the reasons mentioned above. I believe the company can scale its business easily in the coming years and its higher production rates, along with higher oil prices, will lead to increased dividends to shareholders (along with a higher stock price). While Sitio Royalties Corp. shares don't appear to be undervalued at the moment, the stock is worth buying here for long-term investors.

For further details see:

Why Sitio Royalties Should Be On Warren Buffett's Radar