SSNC - Why SS&C Technologies Is Misjudged And Underestimated

2023-07-18 08:59:25 ET

Summary

- SS&C has consistently been deleveraging its balance sheet, delivering strong margins and cash flows, enabling aggressive growth strategies.

- SS&C has created a moat with barriers to entry for peers through its reputation, industry position, client retention, diversification, and more.

- Street estimates for SS&C are highly conservative, and I predict SS&C will exceed expectations due to their scalable business and unrecognized synergies.

- The firm is repurchasing ~$700 million of shares by 2024, with a $0.20 dividend per share that is continuously growing.

- My 10-year DCF analysis, using a 10% WACC, and a blended average of valuations, gives me a 12-month price target of $80 for SSNC stock.

I would highly recommend putting SS&C Technologies (SSNC) on your investment radar, as I am initiating my coverage on this monopolistic fintech with a strong buy and a $80 price tag. I have been knee-deep into the financials of SS&C, a firm that has built quite an impressive moat for itself through its reputation, industry position, client retention, and more. Not only are they continuously deleveraging and expanding margins, but their valuation is extremely attractive to me.

Consensus estimates? I have reasons to believe they'll be smashed, and if not, the estimates for SS&C do not price in potential synergies from M&A and are highly conservative, making this a safe investment. Additionally, the management team suggests SS&C's stock price is cheap, as they have repurchased $305 million in shares this year, with $695 million more to come in the next 18 months and an all-time high dividend that is continuously growing on a YoY basis.

My Introduction to SS&C

SS&C Technologies has been in the finance world since 1986 (over 4 decades) and was founded by CEO Bill Stone. SS&C is one of the leading administrators for hedge funds (HFs), private equity ((PE)), ETFs, and Mutual Funds (MFs) transfers, with over 20k clients and 27k employees globally. The company went public twice, in 1996 and 2010.

Primarily servicing the financial industry, including insurance, SS&C offers a ton of services and software licenses for one-to-five-year contracts, differentiating itself with high client retention rates (>95%). The company's solutions cater to a varied client base, including multinational banks, credit unions, PE firms, HFs, insurance companies, and more.

Revenue streams are balanced across different sectors. About 40% of revenues come from institutional and traditional asset managers, 35% from alternative investments (HFs & PEs), and 25% from wealth advisory and other services.

SS&C's product range includes over 100 products across 8 businesses. Initial client relationships often start with software licensing and hosting services and gradually shift towards outsourcing services. SS&C's comprehensive outsourcing services offer clients enhanced experience through superior technology and dedicated expert staff familiar with international accounting rules, tax laws, and financial regulations.

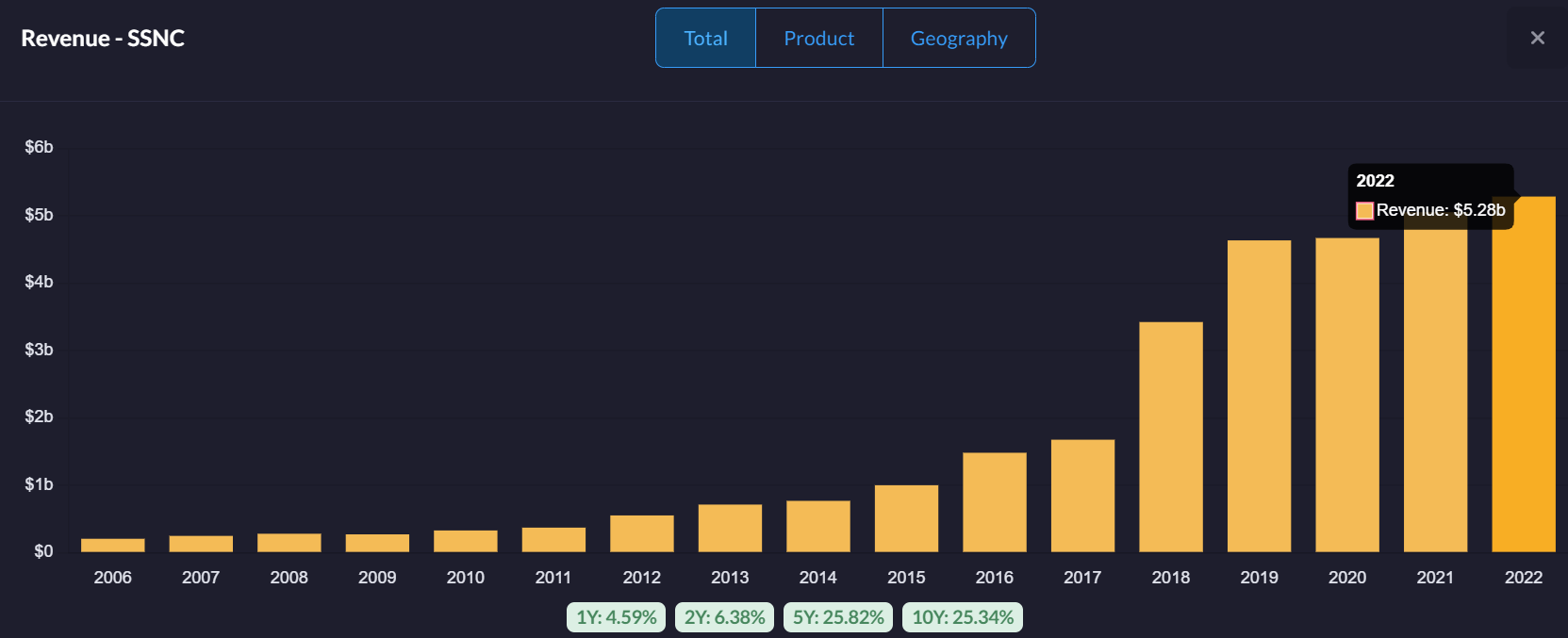

The company has shown consistent revenue growth, largely due to both inorganic and organic growth. Since its second IPO in 2010, SS&C's sales have grown at a ~26% CAGR. With about 2/3 of AUA (assets under administration) in alternatives, the company has shown a strong correlation between alternative AUA and revenue growth. AUA has grown at a 17% CAGR since 2010.

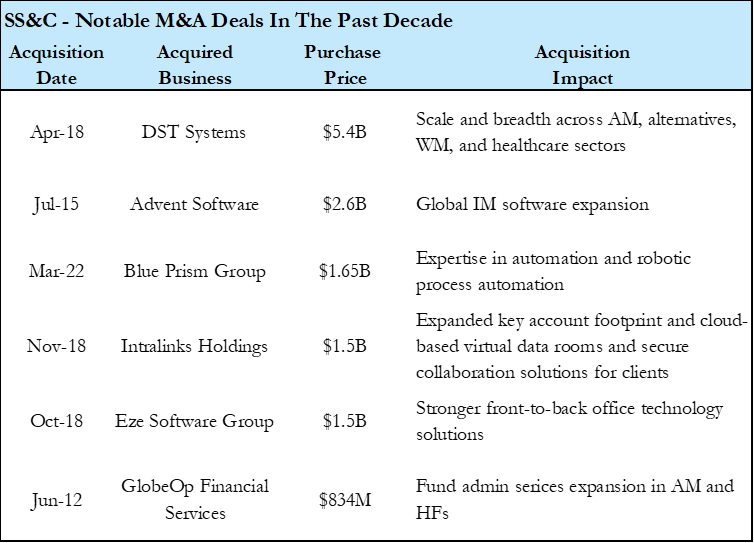

The company is known for its acquisitive nature, having acquired 65 firms since 1995, all different shapes and sizes. The acquisitions have significantly contributed to the scale and revenue growth of SS&C.

{kind=link}

SS&C's Products

SS&C Technologies has a ton of services, in all different sectors, with all types of clients, all over the world.

Outsourcing/Managed Services vs Software

Customers can choose to license SS&C's software solutions w/o outsourcing solely, or they can opt for a fully outsourced model. In the latter, SS&C takes over the client's middle- and back-office operational services, functioning like an outsourced IT department. This can reduce "key man risk" (wherein a company is overly reliant on a few key employees) and allows customers to reduce their IT footprint.

Revenue Breakdown

{kind=link}

Products/Applications Overview

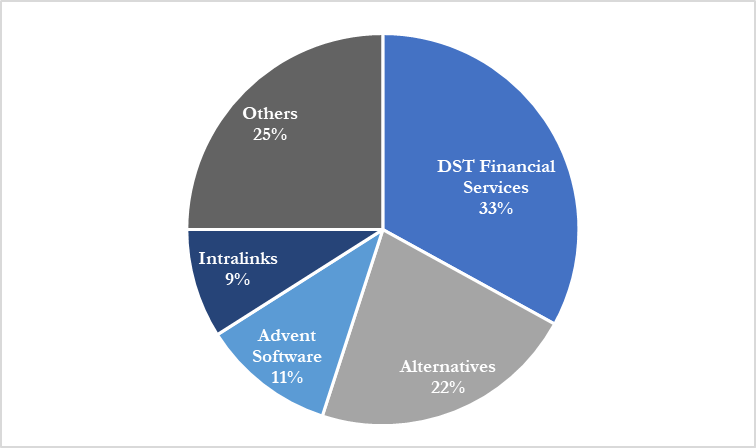

Intralinks - It's a SaaS application providing a secure environment for deal-makers to exchange sensitive documents and information, used primarily in M&A and alternative investments. Despite slower growth in 2022 compared to 2021 (due to the bear market), Intralinks still represents 9% of SS&C's revenue and will likely have much higher growth in 2023 due to higher inflows.

Eze/Financial Markets - A cloud-native end-to-end investment platform, Eze Eclipse is designed to streamline trading operations and minimize costs for investment managers (6% of sales).

Alternatives - SS&C is the world's largest HF and PE administrator through its GlobeOp operation. It provides a vast suite of solutions, including global regulatory compliance reporting, tax reporting, risk reporting, NAV calculations, valuation services, and more.

Advent - Acquired in 2016, SS&C Advent supports 4,300+ investment firms in more than 50 countries. The offering includes fully managed outsourced functions and pure SaaS solutions.

Institutional and Investment Mgmt. (I&IM) - Grew at 6% in 2022 and represented 6% of SS&C's sales. Key products include SS&C Singularity, cloud-based investment operations, accounting and analytics systems, and CAMRA, a portfolio accounting solution tailored for insurance investment operations.

In terms of competition, SS&C's Eze Eclipse is directly competitive with Enfusion. SS&C's client list reportedly includes larger AUM HFs like Balyasny Asset Management, Millenium Management, and Citacel LLC. Meanwhile, Enfusion appears to be winning more shares amongst smaller hedge funds.

My Investment Case for SS&C

Over the course of my experience and exploration of the financial services software industry, I've come across several fascinating and noteworthy companies. One such company that has consistently captured my attention is SS&C, a player that has been in the industry since 1986. What makes the company intriguing to me is the steadfast leadership of its founder, William Stone, who remains at the helm as the CEO to this day. His visionary mindset has turned SS&C into a global provider of software and software-enabled services for various mission-critical financial processes. What's particularly interesting about the company is its adaptive delivery model, offering its products on a license, SaaS, and even a hybrid basis to meet the needs of its clients.

Leadership Position

I am struck by the firm's growth trajectory and leadership position in the fintech space. With a top line exceeding $5 billion, the company has managed to secure leading positions across numerous verticals in this industry, with over 60 companies being integrated into SS&C since 1995. Of these, 8 significant deals in the last decade alone are estimated to be worth a combined ~$14 billion, demonstrating SS&C's aggressive growth strategy.

Well-diversified Client Base

Speaking about their global reach, as of the end of 2022, the firm's workforce exceeded 27k employees, spread across 90+ cities in 40 countries, with its HQ's nestled in Connecticut. The client list, which I have had the chance to review, shows that SS&C is a trusted provider for more than 20,000 finance and healthcare clients. Notably, these clients include some of the world's largest firms with more than $3.4 trillion in AUM. The customer base, in my view, is prudently diversified, guaranteeing a stable revenue stream.

Attractive R&D investments in product and technology

What further impresses me about SS&C is its commitment to product and technology development. The company boasts a portfolio of over 100 products and applicants spanning 8 business lines. Over the past four years alone, SS&C has pumped $1.6 billion into R&D. I think their approach to software licensing is quite interesting, too, with contracts ranging from one to five years, marked by high retention rates of over 95% in each of the last five years.

On the top-line growth front, SS&C presents a relatively unexciting outlook. The company's top 10 clients accounted for ~13% of total sales in 2022, and interestingly, no single client accounted for more than 5% of sales. Based on the firm's historical data, which shows a 4% sales CAGR between 2019 and 2022, I am hopeful for an organic growth acceleration with a projected 4% top-line CAGR over the next three years by the street.

Highly Profitable and Cash Generative

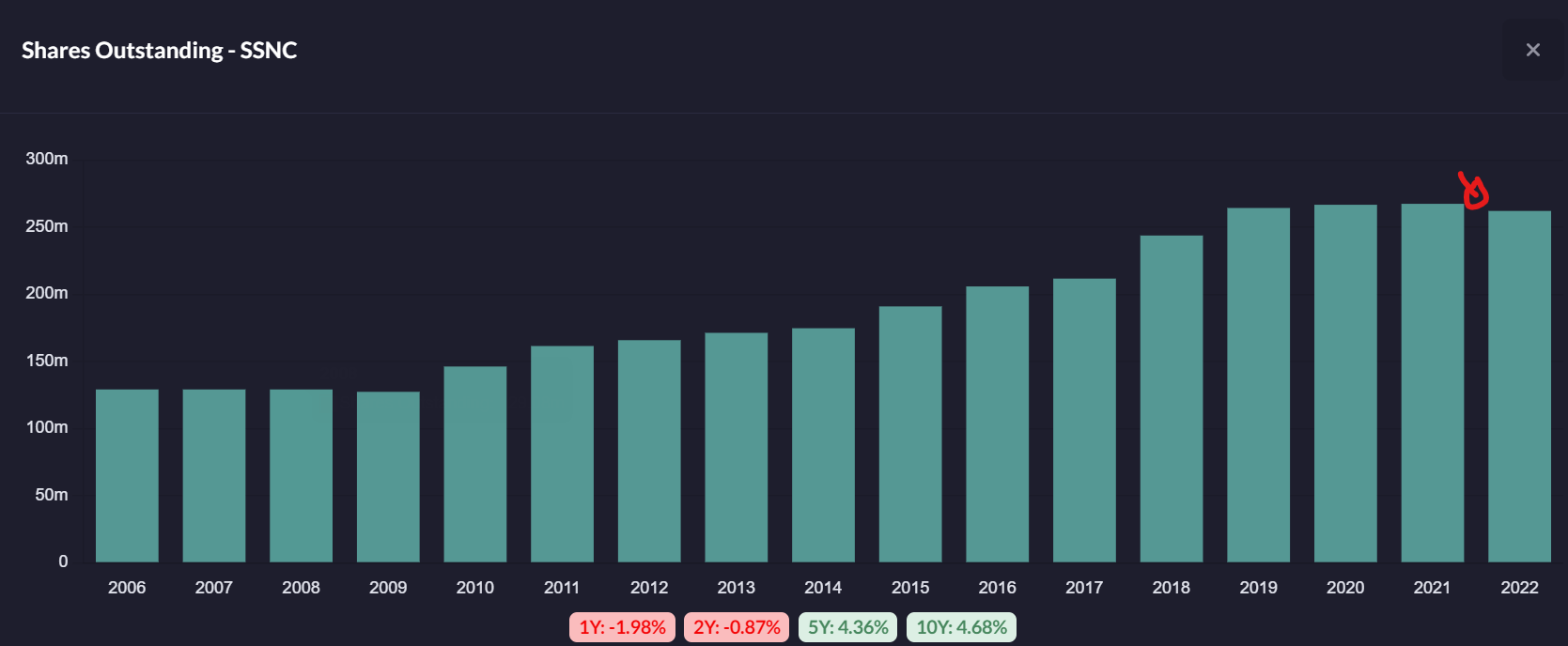

Most notable of all, I find it commendable that SS&C has been consistently delivering 60%/40% gross/EBITDA margins. Also, it is highly cash generative, enabling it to fund its acquisitive growth strategy, pay dividends, and execute share buybacks. At this point, I should also mention the liquidity of their stock. With well over 75% of the outstanding shares in free float, it has a high trading volume of ~$80 million per day on a three-month average.

SS&C Has A "Moat"!

Ok, so I have mentioned SS&C's industry experience, comprehensive product range, commitment to R&D, strong client retention, and diversified global presence. But my point on these factors is that they all combine to create a significant barrier to entry for potential competitors and, in turn, contribute to the stockiness of SS&C's platform.

The industry experience shows trust and reputation, which create barriers to entry for competitors. The diverse product portfolio keeps clients in its pipeline by being tied to the 8 different business segments within SS&C, and with its 100+ software apps and products, it is able to attract a wider range of clients than most. The R&D investments make its offerings more difficult to replicate, thereby fortifying its moat. Not to mention their 95% client retention to boost the moat further. Additionally, their global footprint and client diversity are barriers to entry for US competitors, among others. Then their M&A-drive growth strategy helps reduce the competition by gobbling up any companies that could pose a threat to SS&C. Finally, SS&C's 1-5-year contracts provide the company with a stable and predictable revenue stream which makes it challenging for new entrants to secure similar long-term contracts without a proven track record.

SS&C Technologies Financial Outlook

Street Estimates

Disclaimer: I use Capital IQ from S&P Global for the following street estimates on SS&C Technologies

SS&C charges fees on AUM for a range of services. There are 13 street analysts that give their predictions on SS&C, and their predictions are all very similar for the upcoming quarters. However, in terms of EPS (GAAP), there are only 4-6 analysts that have put in their estimates for the SS&C's FY23 Q2 earnings that are to be released on July 27th this year. See below for the consensus of these estimates:

{kind=link}

Now, I don't know what these analysts are thinking or saying about SS&C, but I certainly disagree with their FY23 estimates. Looking at Q2E for FY23, and looking at Q2A for FY22, there is little difference in the revenue and EBITDA outlook. However, SS&C grows its top and bottom lines through AUM/AUA growth. In Q1 of FY23, we have already seen massive inflows into ETFs. As of the end of June, the US stock market alone has already seen $200 billion of net inflows in 2023, according to ETF.com .

Something to remember about SS&C is that while they do not have the SS&C brand on any ETFs, they have 23 ETFs with the Alps brand (a company they acquired). These ETFs sum to ~$10.5 billion in AUM. But in total, SS&C serves nearly 70 ETFs through their Alps funds business line; these ETFs sum to be over $250 billion in AUM. My point is, as the whole industry is seeing larger inflows to AUM, and firms like SS&C charge fees on this AUM, with them managing over $250 billion in ETF AUM alone, it does not make sense to mee how there is no change from Q2 in FY22 to Q2 in FY23 in terms of top and bottom-line growth. Thus, I believe SS&C will have no trouble exceeding expectations this year and giving greater guidance for their future growth due to their scalable business model.

In any case, however, even if SS&C does not crush earnings estimates, the expectations are so low that I view SS&C as a safe investment with a very low chance of getting worse-than-expected earnings results.

Revenue Projections

{kind=link}

The revenue projections for SS&C indicate a growth trajectory of ~4-5% through the year 2025. That suggests an increase from the FY22 revenue of $5.4B to FY25 sales exceeding $6B. These estimates do not consider any potential top-line benefits from M&A. Since 2019, SS&C's organic sales growth contribution has oscillated between 1-6%. This is of course, affected by macro shifts and strongly correlated with AUM.

Operating Expenses

{kind=link}

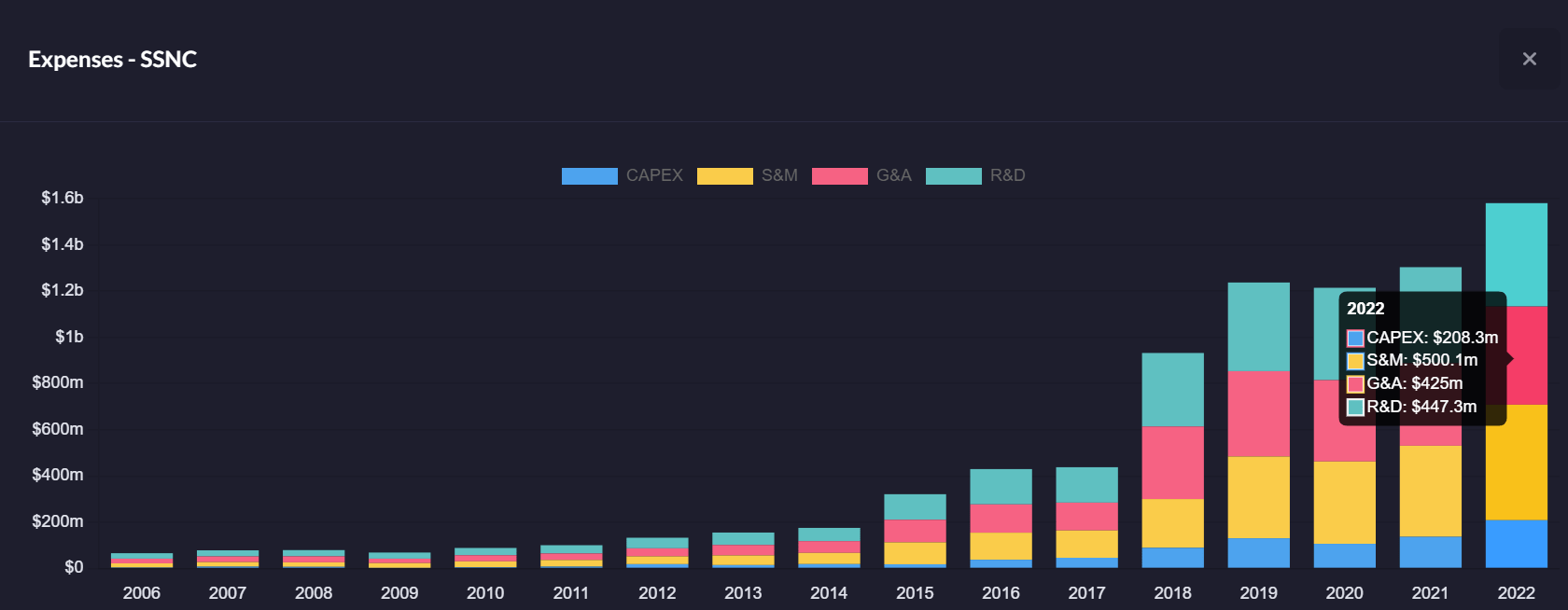

The forecasts do not anticipate significant changes to the key expense items as a % of overall sales. The gross profit margin is expected to hover around the 60% mark, which is slightly lower compared to more nascent SaaS companies, which may reach closer to 70%. When it comes to operating expenses, accounting for 8% of the overall revenue in recent years, this trend is expected to continue. Meanwhile, Sales & Marketing expenses are projected to remain relatively stable at ~7% of sales, while G&A expenses may see a modest decrease from 6% to 5%. These minor reductions in operating expenses led me to predict an expansion in the operating profit margin from 37% in 2022 to ~40% by 2025.

Cash Flows

SS&C's cash flow margin has fluctuated between 19% and 29% from 2016 to 2022. This does not suggest particularly high volatility, but I would note that the trajectory during this period hasn't been exclusively upward. The projections, however, show their margin increasing from 21% in FY22 to a more optimistic 33% in FY25.

Capital expenditures account for a small % of overall sales - around 4%, which aligns with industry standards for vertical software companies. I believe the majority of SS&C's capital spending will also be allocated to debt repayment, as per their management team has continuously done.

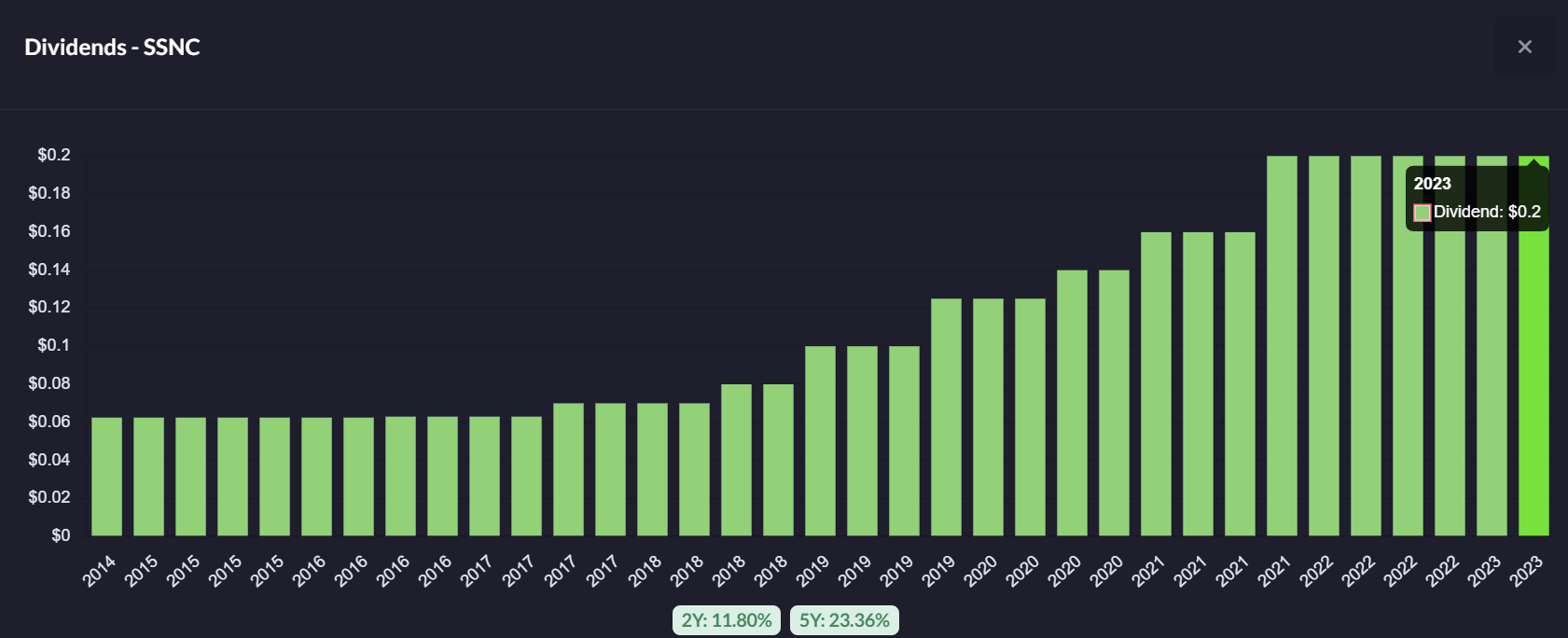

As for the return to shareholders, the firm plans to undertake a stock repurchase program, with a projected $695M of share buybacks forecasted over 2023 and 2024. $305 million of shares have already been bought back since their announcement in August of 2022.

{kind=link}

Also, SS&C has announced a $0.20 per share quarterly dividend, which amounts to just over $200M of annual dividend payment to its shareholders. A $0.20 per share dividend is awesome to see from SS&C if we look back to 2019, it was half of that, and in 2016 it was one-fourth of that. The dividend growth is on an upwards trend, and that is certainly pleasing to see.

{kind=link}

How I Believe SS&C Should Be Valued

SS&C Technologies is in the technology sector. According to Seeking Alpha Quant ratings, it is placed in the industrials sector. Companies in the industrials sector arguably have the lowest valuations. For that reason alone, Quant factor grades have SS&C's valuation grade at a D+. However, say you place SS&C in the information technology sector, Quant would likely have SS&C's valuation grade at an A! Or you could place SS&C in the financials sector - this would have Quant rating SS&C's valuation at an F because valuations are extremely low right now for financials. With this in mind, I would ignore the sector that SS&C is placed in, as I think that grading is not an accurate way to view SS&C's true value.

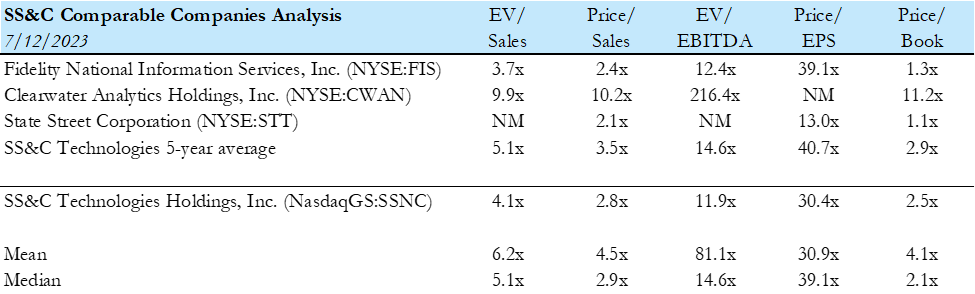

Instead, I believe it is wise to compare SS&C's value today with their 5-year average valuation metrics as well as comparing them to similar competitors:

{kind=link}

Taking a look at Fidelity National Information Services ( FIS ), Clearwater Analytics ( CWAN ), State Street ( STT ), and SS&C's multiples, there is no doubt to me that SS&C is undervalued. At this price, we are seeing SS&C on sale. Just even looking at the 5-year average for SS&C, it screams cheap - P/E 40.7x 5 yr avg vs 30.4x right now; or EV/EBITDA at 14.6x 5 yr average vs 11.9x today. Otherwise, we could compare to them all and look at the mean and median for the multiples, then compare that to what SSNC is trading at today; I would give SS&C's valuation grade an A+ as of writing. One last thing I want to mention is that SS&C has a 1.32% dividend yield, which is much higher than its 5-year average of 0.91%.

Discounted Cash Flows Analysis

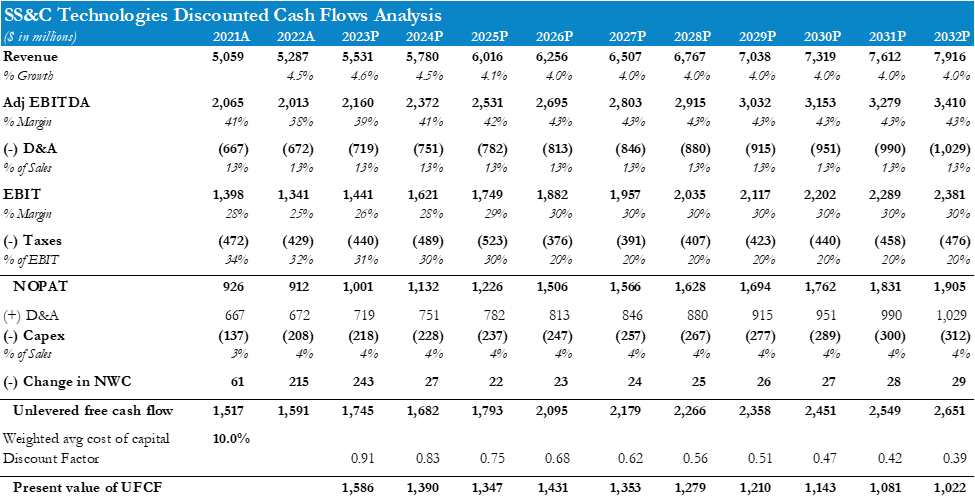

As previously mentioned in my financial outlook segment for SS&C Technologies, I have looked at what analysts are projecting SS&C to grow at and have given my opinions on it. To keep things simple, I kept the street estimates from 2023-2025 the same, then forecasted 2026 and beyond by keeping the same margins and growth rates the same. With this, I forecast SS&C on a 10-year DCF, as shown below:

{kind=link}

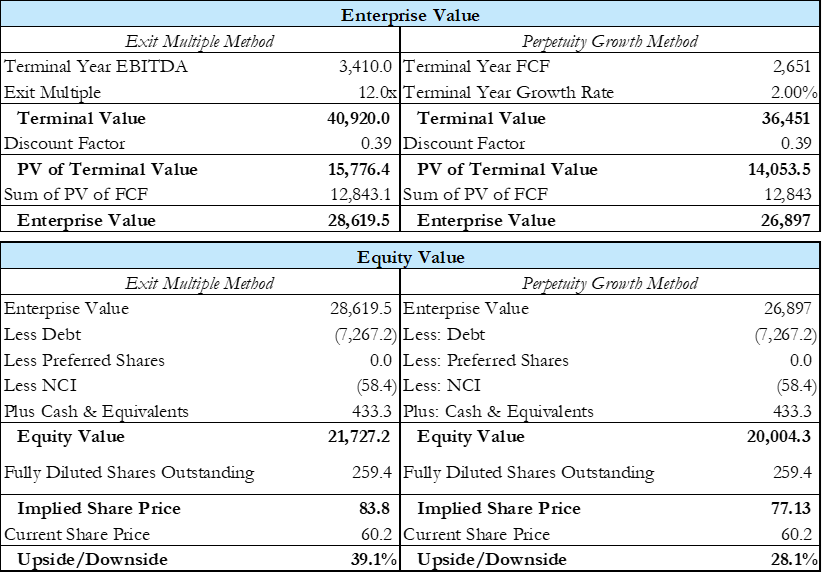

As shown in the figure above, I used a 10% WACC to discount the unlevered free cash flow to the present value. See below for the calculation of firm value:

{kind=link}

I use both the exit multiple methodology and the perpetuity growth methodology to get my implied share price for SS&C. For the exit multiple, I use SS&C's current EV/EBITDA multiple (also in line with 5 year average forward EV/EBITDA multiple), and arrive at an attractive, ~$84 implied share price. As for the perpetuity growth methodology, I assumed a 2% terminal growth rate as per industry standards and the nature and scalability of SS&C's business model; this methodology gives me another attractive implied share price of $77. I honestly believe the DCF forecasts, alongside the EBITDA multiple and terminal growth % are all near my bear case for SS&C, but I also think I may be biased due to my bullish view on SS&C. Anyways, I am setting a 12-month price target of $80 for SS&C, as that is a blended average of both valuations above, and implies a 33% upside to SS&C's current share price of $60.2, as of writing.

The share price is highly sensitive to the WACC, EBITDA multiple, and terminal growth rate, so I have provided a sensitivity analysis for all three of these metrics below:

Author's Data

Risks to Rating & Price Target

SS&C is known for its M&A-driven growth strategy - the company has an extensive history of growth through acquisition, dating back to the mid-200s when SS&C was private. From 2005 to 2010, the company gobbled up ~30 companies, spending close to $500 million in total. The average deal size during this period was $17 million, with valuations typically ranging from 3-7x EBITDA. This aggressive strategy significantly bolstered SS&C's capabilities and market positioning. However, as we have all experienced in recent years, the landscape has shifted. Valuations have risen, making it harder and harder to generate a return on ROIC through acquisitions. From 2012 to 2022, SS&C gobbled another 35 firms, including 8 sizable deals totaling over $14 billion in value. While M&A will likely continue to be a key part of SS&C's growth story moving forward, elevated valuation multiples, especially in tech, could slow down the pace of SS&C's business development.

SS&C has had some healthcare problems - In July 2021, SS&C ventured into a joint venture named DomaniRx, alongside other industry leaders, aiming to create a new cloud-native, API-driven claims platform. Sound cool and all, but the thing is, delays in the implementation of this platform will result in further outflows of Healthcare sales due to client losses beyond 2023.

Recessionary headwinds - as a software provider and outsourcing partner for finance firms, SS&C might face challenges in economic downturns. Recessions often lead to delayed IT budget spending or even cuts, which would adversely affect SS&C's sales. Also, a recession would lead to a market meltdown, leading to a decline in AUM and trading volumes, both of which are key drivers of SS&C's growth.

Bottom Line

I believe SS&C Technologies is a strong investment opportunity, considering its leadership position in fintech, diversified client base with best-in-class retention rates, continuous innovation, and highly scalable business model. Despite the slower top-line growth and potential headwinds, the firm's strong margins, successful M&A strategy, and undervaluation offer a safe bet at today's prices. All in mind, I am eager to give SS&C a strong buy rating with a 12-month PT of $80, suggesting a 33% upside.

For further details see:

Why SS&C Technologies Is Misjudged And Underestimated