TGNA - Why TEGNA Is A Buy Even As A Standalone Company

2023-10-23 17:57:36 ET

Summary

- TEGNA Inc. demonstrates potential as a media enterprise integrating traditional broadcasting with digital trends.

- Despite regulatory challenges, the company's strategic maneuvers highlight its dedication to shareholder value.

- Nevertheless, positive endorsements, such as that from investor Mario Gabelli, hint at a promising future with potential sector-wide M&A opportunities.

- TGNA's financial trajectory supports a positive outlook, and it appears to be undervalued, making it a "buy" with a target price of $17.50.

TEGNA Inc. ( TGNA ) demonstrates potential as a media enterprise adeptly integrating traditional broadcasting with evolving digital trends. Following a significant merger termination, the company's strategic maneuvers underscore its dedication to shareholder value, notwithstanding regulatory challenges. In my view, TGNA's financial trajectory supports a positive outlook regarding its future prospects. When assessed from a valuation standpoint, I believe TGNA appears to be notably undervalued, even under fairly conservative assumptions. This leads me to rate the company as a “buy,” with a target price of $17.50. I base this valuation on the company's demonstrated ability to navigate through industry challenges and its aptitude for adapting to digital advancements, which I infer will continue propelling its market position and financial growth.

Business Overview

TGNA holds a significant position in the media sector, owning 64 television and 2 radio stations distributed over 51 markets within the United States. They maintain a solid presence, particularly within the top 25 markets, as the predominant holder of the key four network affiliates: NBC, CBS, ABC, and FOX. Beyond traditional media platforms, TGNA has effectively transitioned into the digital era, establishing a robust online presence on various platforms, including Hulu, YouTube TV, and DIRECTV Stream.

Moreover, TGNA develops its own multi-platform news and entertainment programs and operates multicast networks. I believe TGNA's foray into the digital realm, especially the over-the-top ('OTT') streaming space, underscores its adaptability to evolving viewing preferences. This move has favorably impacted its subscription revenue. Also, this venture reflects TGNA's aims of capturing a broader audience base amid the digital shift. The ability to diversify its offerings across both traditional and digital media channels could potentially fortify TGNA's market standing and, in my opinion, set a precedent for other players within the industry to emulate.

Source: Investor Presentation August 2023

I believe TGNA's foray into the digital realm, especially the over-the-top streaming space, underscores its adaptability to evolving viewing preferences. This move has favorably impacted its subscription revenue . Also, this venture reflects TGNA's aims of capturing a broader audience base amid the digital shift. The ability to diversify its offerings across both traditional and digital media channels could potentially fortify TGNA's market standing and, in my opinion, set a precedent for other players within the industry to emulate.

Strategic Shifts After Deal Termination

Regarding corporate maneuvers, TGNA had a significant merger plan with Teton Parent Corp and others. Still, this plan hit a snag due to regulatory challenges, leading to its termination. This hiccup led to a $136 million termination fee from Standard General, the other party in the merger. After this termination, TGNA shifted gears by initiating a $300 million accelerated share repurchase program and amped its quarterly dividend by 20%, showing a proactive approach to keep shareholder value intact. Their financial performance has been noteworthy, too, with 2022 being a record year for them in terms of revenue and net income. Terminating the merger agreement had a notable impact, leading to decreased revenue and net income in a recent quarter. Despite these setbacks, TGNA maintained a steady course, with plans solidly outlined through the third quarter of 2023.

Source: Investor Presentation August 2023

Notably, TGNA experienced a modest uptick of 0.2% following a positive endorsement from investor Mario Gabelli. During a CNBC interview , he speculated that TGNA is positioned to earn $3.50 per share. He reiterated the potential of reaching a $24 share price in the near future despite regulatory hurdles, projecting a lucrative 50% return over the next 18 months. Moreover, Gabelli mentioned that the FCC may eventually relax restrictions to allow TV station operators to expand beyond the current 39% coverage cap. Also, I believe this could open up new avenues for growth and consolidation within the broadcasting industry, which may, in turn, create a favorable environment for TGNA to thrive. This hints at possible sector-wide M&A.

TGNA’s 2023 Q2 results showed a 7% YoY decrease in total revenues, mainly owing to the lower political revenue generated from the previous year's midterm election cycle. Despite this revenue contraction, TGNA reported a modest 2% YoY increase in subscription revenue, setting a new Q2 record. This increase, propelled by subscriber rate augmentations, hints at a favorable trajectory in both consumer retention and acquisition, which, in my view, corroborates TGNA's competitive positioning in its market. However, on the downside, TGNA’s Advertising and Marketing Services sector saw revenues shrink by 5% YoY, with core advertising trends also registering a slight decline into the low single digits. This suggests a possible area of concern or an opportunity for reassessment and strategy refinement in TGNA's advertising operations.

{kind=link}

Nevertheless, TGNA increased its dividend by 19.8% to $0.11375 per share, showcasing a sustained dedication to shareholder value return alongside its revenue growth ambitions. I believe this substantiates TNGA’s balanced approach to capital allocation and shareholder value maximization, which should bode well for long-term investors. Looking ahead, TGNA foresees a low double-digit percent decrease in total company revenue for Q3 2023, primarily tied to the absence of political revenue. But overall, analysts still expect TGNA’s revenues to continue growing, so as a whole, TGNA’s prospects remain promising.

Valuation Analysis

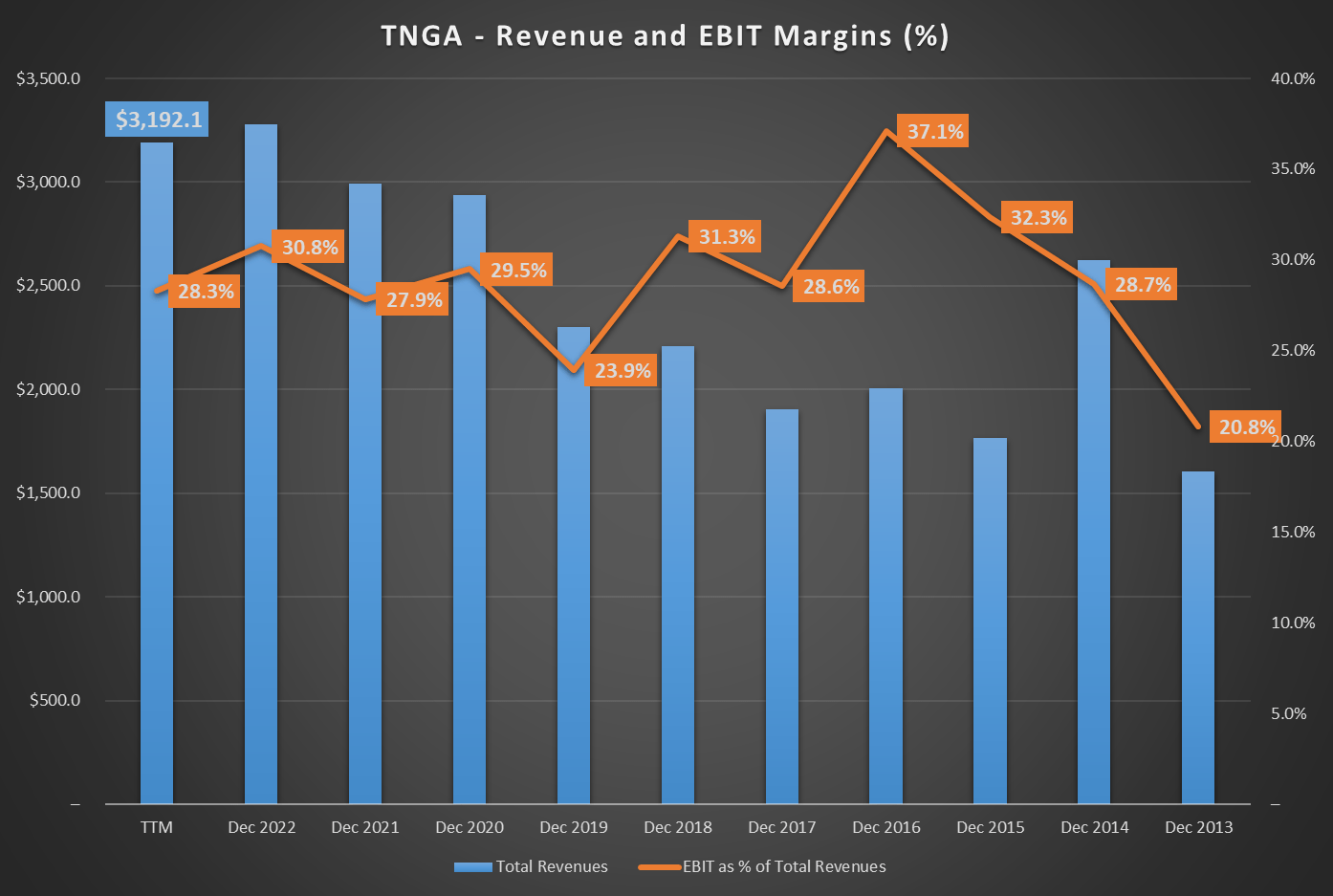

Over the past decade, TGNA has demonstrated a solid financial performance , with its revenues climbing from $1.60 billion in 2013 to $3.28 billion in 2022. This indicates a revenue CAGR of 8.3%, a notable figure among media companies, suggesting that TGNA's content successfully engages viewers. The substantial growth in revenue, alongside an upward trend in EBIT margins that reached 37.1% in 2022, highlights TGNA's proficiency in both market penetration and efficiency.

{kind=link}

In my view, these figures reflect a strong market position and a well-managed operational structure, which is crucial for sustaining growth and competitiveness in the fast-evolving media sector. However, it's worth noting that the EBIT margins have seen a slight dip from the 2016 peak, currently standing at 28.3%. I speculate this slight margin contraction could be attributed to increased market competition. Yet, TGNA’s margins remain robust, showcasing the company's competitiveness and well-managed business.

Author's elaboration.

As you can see, my valuation model is rooted in projecting a rough estimate of TGNA’s future prospects. The current revenue projections anticipate a decline of 9.7% in 2023 but growth in subsequent years, reaching $4.56 billion by 2027. This revenue drives the EBIT, which has historically been around 29% of revenues. After accounting for D&A, taxes, CAPEX, and NOWC changes, I estimate TGNA’s FCFFs. I then discounted these FCFFs and the terminal value of $5.8 billion by deriving TGNA’s WACC of 7.1% from its current EV, market cap, debt, and current credit rating yield . The result is a total present value of $6.18 billion. Thus, after accounting for TGNA’s cash and debt, I estimate TGNA's fair value at $3.5 billion. This means the stock is undervalued and has a promising upside potential of 24.4%. Therefore, I rate TGNA a “buy” with a $17.50 stock price target.

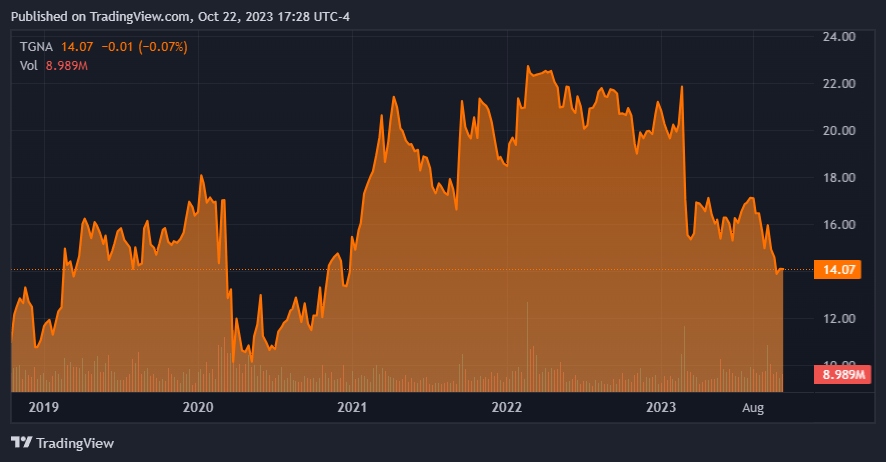

TGNA's recent pullback and current discount could signal a promising entry point for investors. (TradingView.)

{kind=link}

Conclusion

TGNA has undoubtedly marked its presence in media by successfully merging the strengths of traditional broadcasting with the nuances of modern digital innovations. Despite facing setbacks like the major merger termination, TGNA's unwavering dedication to enhancing shareholder value remains evident. This commitment and its resilience amidst regulatory hiccups set the foundation for a bullish outlook on the company's future. In my assessment, TGNA's valuation strongly suggests it’s undervalued. Thus, based on its proven adaptability, resilience against industry challenges, and forward-thinking approach to digital integration, I rate TGNA as a “buy” with a stock price target of $17.50.

For further details see:

Why TEGNA Is A Buy Even As A Standalone Company