NLY - Why The Agency MBS Sector Is Worth A Look Now

2023-09-04 22:06:38 ET

Summary

- Agency MBS is an attractive asset class for income investors due to its cheap valuation, high quality, and diversification benefits.

- The option-adjusted spread for Agency MBS is elevated compared to corporate credit spreads, making it an appealing investment.

- There are various ways to invest in Agency MBS, including through mortgage REITs, leveraged CEFs, unleveraged ETFs, and mREIT preferreds.

In this article we revisit the Agency MBS sector as well as the different types of securities and investment vehicles that focus on this sector. Agencies are often overlooked by investors due to their middling level of yield. However, there are ways to allocate to the sector at high single-digit yields. Beyond the yield there are several other compelling reasons for taking a renewed look at the space.

Why Agencies

Agency MBS is an attractive asset class for income investors at the moment for three main reasons. One, it remains fairly cheap - almost uniquely so - in the broader fixed-income space. Two, it is one of the highest-quality sectors in an environment where a medium-term recession remains a toss-up. And three, it provides much-needed diversification in income portfolios that are typically overweight corporate credit risk.

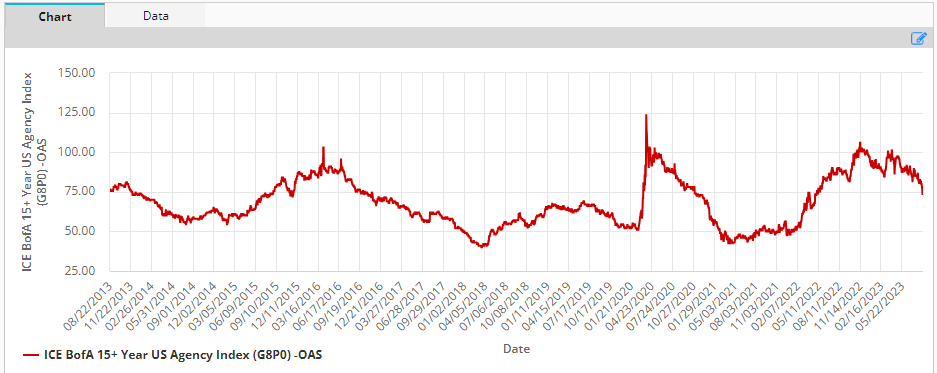

The credit landscape is mixed at the moment. We have a situation where interest rates (both nominal and real) are high, which is good (for income) but credit spreads are fairly tight which is bad. However, spreads in the Agency sector remain unusually elevated.

The Agency option-adjusted spread is well above its median level of the past decade. This is in contrast to corporate credit spreads which remain at very tight levels.

{kind=link}

This is obviously not because of any actual credit concerns since Agencies don’t have credit risk and is more due to a combination of elevated interest rate volatility (making Agencies more negatively convex) as well as technical pressure from FDIC sales and the Fed’s balance sheet runoff.

Once the FDIC is done, the technical pressure should recede. Interest rate volatility is also likely to subside once the Fed moves to a more permanent pause.

Some Ideas

Agencies in their pure form are not super compelling income securities at yields of 5-6%. However, there are other higher-yielding ways to hold them.

The highest-yield / highest-beta option would be Agency mortgage REITs at low double-digit yields. Any rally in Agencies would also translate most directly to capital gains there as their leverage is in high single-digits. The downside, of course, is the usual forced deleveraging and locked in economic losses - something that has happened repeatedly.

Lower-beta options are something like the BlackRock Income Trust ( BKT ) which is a leveraged Agency CEF with leverage comparatively low versus mREITs. BKT trades at a 9.1% yield and a 5.4% discount. There are also a number of unleveraged ETFs. Among these, the First Trust Low Duration Opportunities ETF ( LMBS ) looks the most interesting.

The final option and best in our view are the mREIT preferreds which provide decent yields of 7-10% but without explicit leverage. Here we continue to hold the Annaly Series I ( NLY.PR.I ) as well as the AGNC Series G ( AGNCL ).

Another attraction of preferreds (particularly for those investing in tax-sheltered accounts) is that they allow investors to do relative value rotations. This is a strategy that we have used with the Annaly Capital Management ( NLY ) trio of preferreds.

Systematic Income Preferreds Tool

The chart below shows our switches over the past year or so with the series name we were holding added. The chart shows normalized total returns of all the series as well as the rotation strategy (in blue) which has outperformed the individual stocks.

Systematic Income

The strategy has also outperformed the broader mREIT preferred sector over the same period as shown below.

Systematic Income

Since our recent rotation to NLY.PR.I from NLY.PR.F, it has outperformed NLY.PR.F despite having a significantly lower stripped yield. The reason for this is that the stock's yield will step up to the highest level on its call date in 2024 and as that date approaches the prices of the two stocks should converge as they have a nearly identical spread over the base rate. If the stock is redeemed that will only be a windfall for holders as it trades below "par".

Systematic Income Preferreds Tool

Takeaways

The Agency MBS sector is worth a look for income investors in the current environment. Its valuation remains cheap even as the broader credit market is fairly expensive. It also provides an important diversifier in income portfolios which often lean heavily on corporate credit risk. Its high-quality profile also means it should perform well if markets hit a bump in the coming months.

For further details see:

Why The Agency MBS Sector Is Worth A Look Now