FTDS - Why The Bank Of Japan Blinked

Summary

- The Bank of Japan shocked the market by increasing the band on their Yield Curve Control policy.

- The policy change was necessary because the BOJ has maintained an accommodative monetary policy despite surging inflation and a weakening yen.

- The policy change has not had the desired effect of smoothing the yield curve or improving liquidity in Japanese Government Bonds.

For all of 2022 the developed world has been dealing with the problem of excessive inflation. To combat this trend, the G7 central banks, with the exception of Japan, have reversed their Quantitative Easing policies of the prior decade by raising interest rates and implementing Quantitative Tightening (QT.)

The Bank of Japan ((BOJ)), however, led by Governor Haruhiko Kuroda, has been steadfast in maintaining their accommodative monetary policy. Kuroda has insisted that monetary easing is appropriate to support Japan’s economy.

Until last week, when the Bank of Japan blinked.

A week ago, Monday, the BOJ shocked the financial markets when they announced a modification to their Yield Curve Control ((YCC)) policy by widening the band around their target yield of 0.0% on the 10-year Japanese Government Bond (JGB.)

The prior band had been +/- 25 basis points around the 0.0% target, and the new band was increased to +/- 50 basis points. This was couched as a technical move to improve market functioning, but it was so much more.

The BOJ has been behind the curve for some time, which has created problems that they are still figuring out how to deal with.

Kuroda, whose 10 year term ends in April 2023, introduced the policy of Quantitative and Qualitative Easing ((QQE)) in 2013 to achieve the price stability target of 2% in a sustainable and stable manner. He is the architect of the largest monetary easing program in the world, and is determined to ride the policy to the end. But the market has changed, and so must BOJ’s policies.

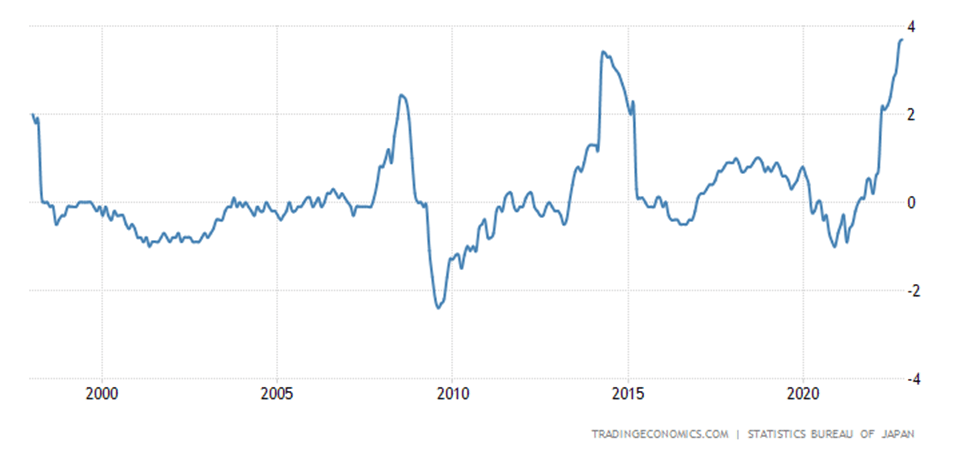

Inflation Exceeds 2%

Inflation is a global phenomenon, and Japan has not been immune. The CPI for November hit 3.7%, a forty-year high. The main culprits have been the rising costs of oil and imports due to the depreciation of the yen. The BOJ’s shift is an acknowledgement that the persistence of higher prices can no longer be ignored.

Japan Annualized CPI

{kind=link}

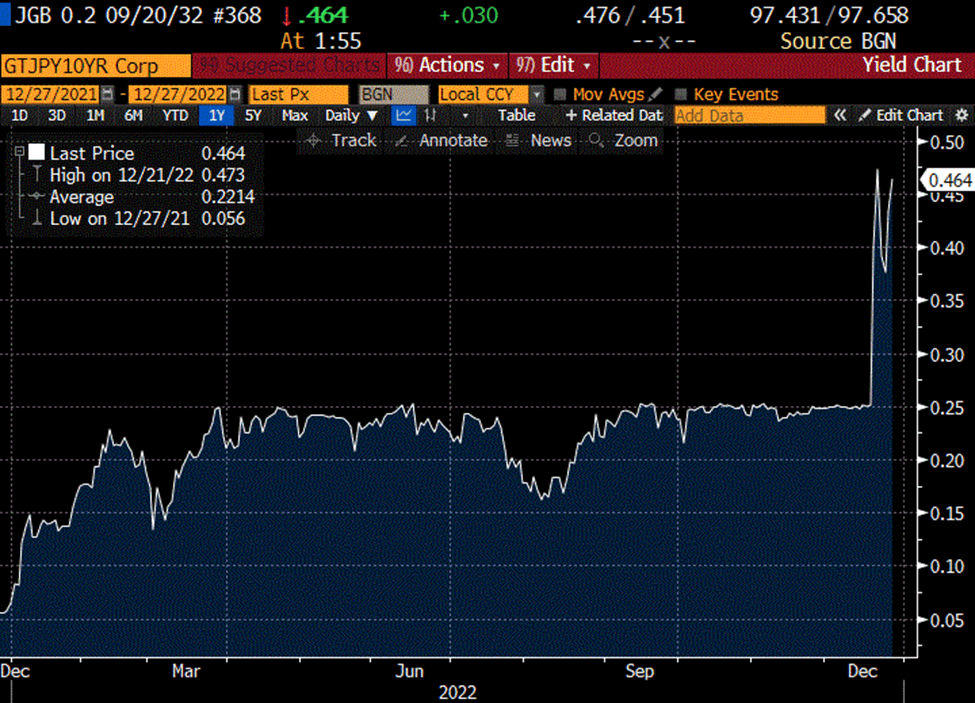

The Yield Curve Control Policy is Not Working

YCC was instituted in 2016 as a way to stabilize long rates around zero percent when Japan was experiencing deflation and short rates were negative. Combined with QQE the goal was to continue purchasing massive amounts of JGB’s until inflation returned to the 2% target in a stable manner.

The YCC policy established a +/- 25 basis point band around the target 0.0% rate on 10 year JGB’s with a commitment to purchase whatever amount of JGBs was needed to stay within the band.

That commitment has been tested on numerous occasions earlier this year by foreign speculators who shorted JGBs, forcing the BOJ to defend the band.

{kind=link}

While the BOJ’s policy under QQE has been to buy 7.3 trillion yen of JGBs per month, under YCC they have been pressed to purchase larger amounts.

During the current quarter, the BOJ has bought 14 trillion yen, per month, of 10-year JGBs, double the target, to protect the band, thereby expanding QQE when the rest of the world was implementing QT.

This position was untenable, hence the policy shift. The market response was for the 10-year JGB yield to immediately jump to the new band. The BOJ’s commitment to the new upper limit may soon be tested, as well.

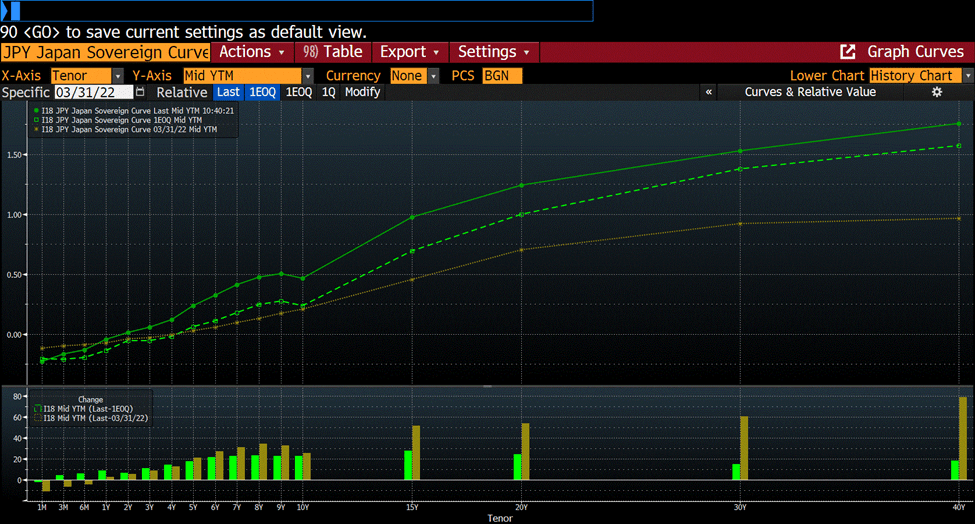

Goal of Smoother Yield Curve is Not Working

Kuroda rightly noticed that the functioning of the yield curve has been impaired by YCC. YCC is committed to only 10-year JGBs consequently yields at other maturities move more freely. With pressure across the yield curve, it has attained an artificial shape with a kink at the suppressed 10-year.

{kind=link}

The above chart shows the yield curve at three time periods. The yellow line represents fiscal year end, 3/31/22. This curve shows a normal, smooth shape. The dotted green curve is from 9/30/22 and indicates the pressure that has been felt on yields. All yields beyond one year have risen, but the artificial cap of YCC has created a kink. The final solid green line is the most recent yield curve, following the BOJ policy adjustment. Again, all yields rose, but the kink at the 10-year remains. Therefore, the BOJ goal of smoothing the curve has not been met.

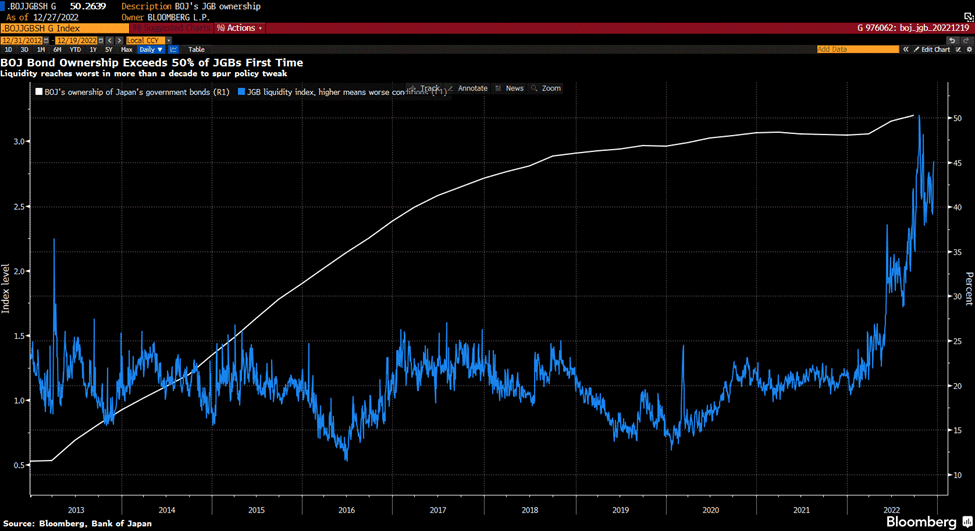

JGB Market Liquidity Remains a Problem

Kuroda’s main reason for widening the band on 10-year JGBs under YCC was to improve liquidity in JGBs. He observed deterioration in the functioning of Japan’s bond market. As shown in blue on the below chart, the Bloomberg JGB Liquidity Index has risen sharply, with a higher number representing less liquidity.

{kind=link}

One reason for this decline in liquidity is the fact that such a large portion of the market is owned by the BOJ. The white line in the chart shows the BOJ’s ownership of the market, which recently exceeded 50%. Consequently, there are not many bonds that are traded freely which, of course, weakens liquidity.

Interestingly, when Kuroda implemented QQE in 2013 the BOJ only owned 11% of the JGB market. As QQE continues and more bonds are removed from available float, it will be difficult for this situation to improve.

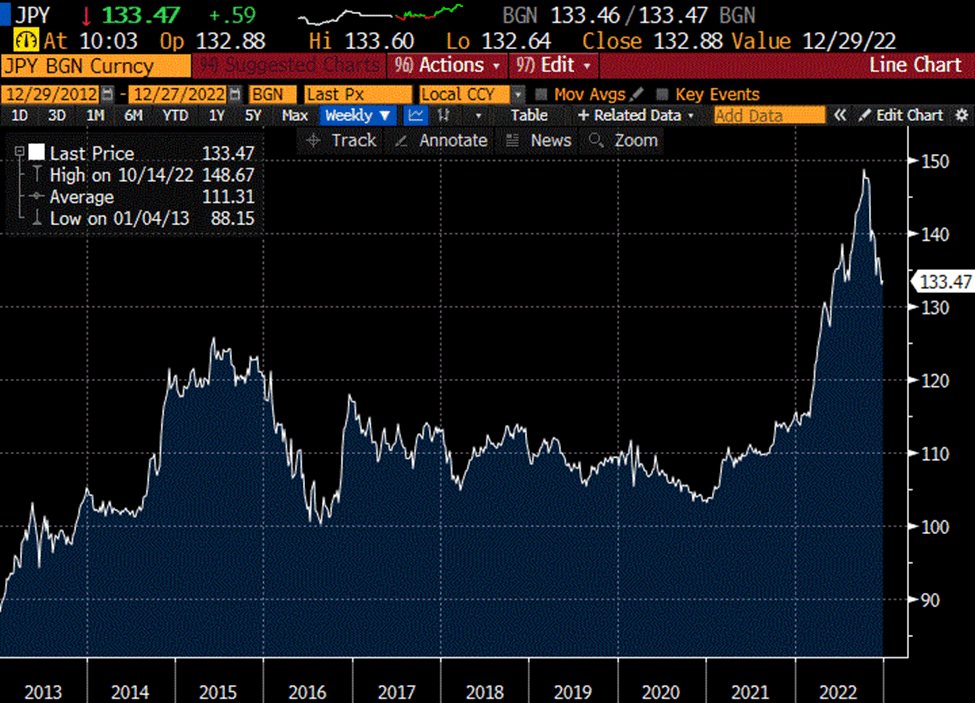

The Yen Weakens

A major consequence of Japan’s continuation of monetary accommodation while the rest of the world is enacting QT is a severe deterioration in the yen. The widening global interest rate differentials have made the yen unattractive. From the beginning of the year to the yen’s weakest moment in October, the currency was off 22%. It rebounded somewhat and had a positive 5% move on BOJ’s announcement of their policy shift, but the sustainability is unclear.

{kind=link}

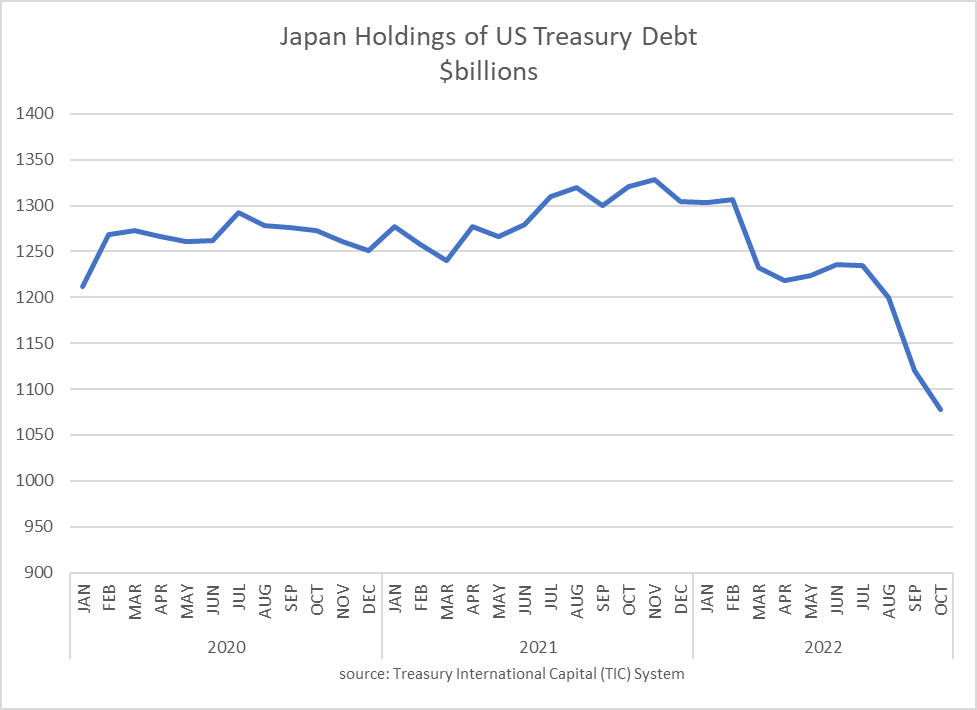

The BOJ was forced to take action in support of the yen, and one such step was for them to reduce their holdings of US Treasury debt. Japan has been the largest foreign owner of Treasury debt, and their holdings peaked in November 2021 at $1.3 trillion. Since then, they have regularly cut their position and as of the most recent release, they only held $1.08 trillion. Altogether, they sold 19% of their Treasury bonds. The BOJ actions of selling dollars to buy yen has only slowed the decline.

{kind=link}

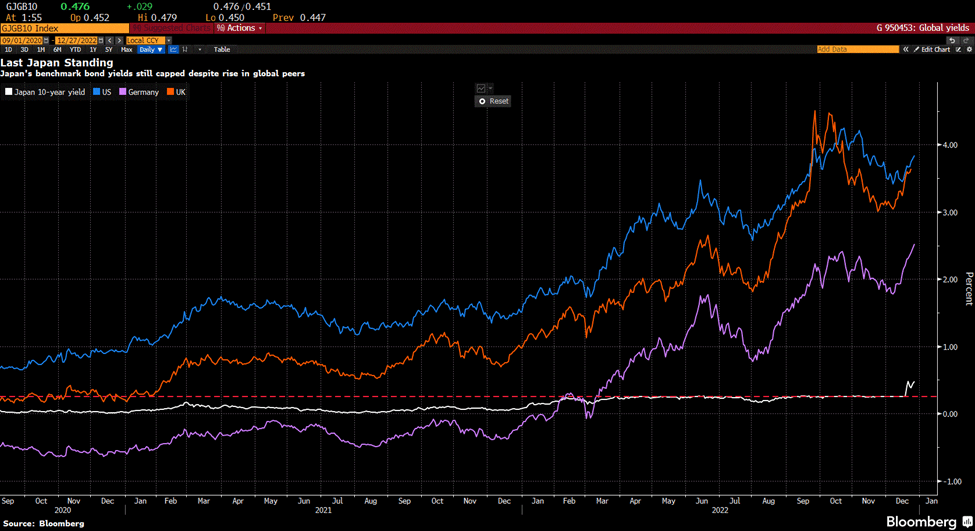

The Problems with Rising Rates

Interest rates across the globe have risen significantly this year to combat inflation. The BOJ has been late to the game.

{kind=link}

The impact this rise in rates has had on central bank balance sheets is significant. The BOJ is now experiencing this effect. As of 9/30/22 when the BOJ reported their financial statements for their half year fiscal results, the BOJ revealed an unrealized loss of 874.9 billion yen in their JGB portfolio.

This is the first time in 16 years that the BOJ has had such a loss. As rates continue to rise, this loss will only get bigger.

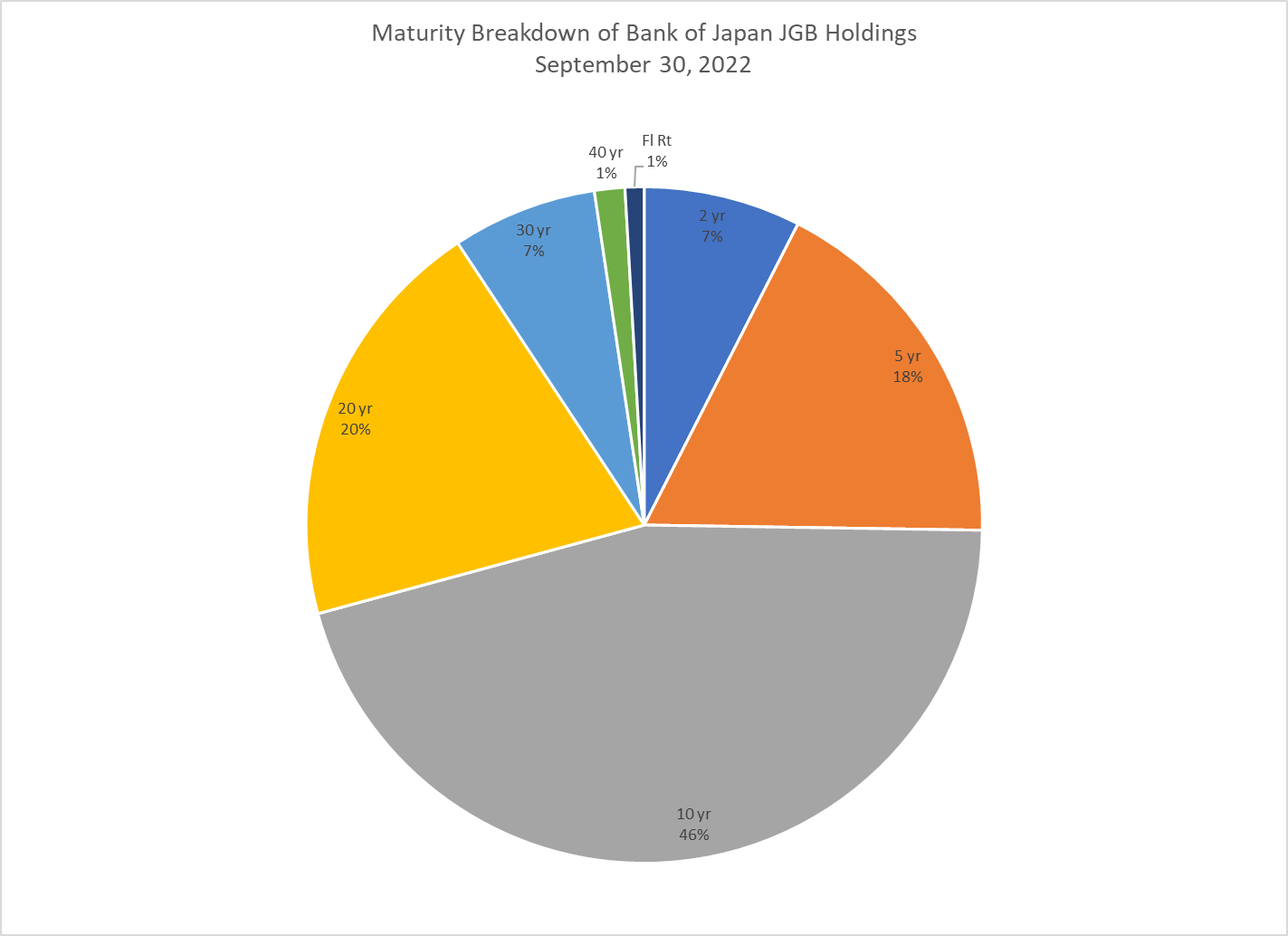

The JGB portfolio at BOJ is comprised of mostly longer-term securities. The largest position, mainly due to YCC, is the 10-year, which represents 46% of the portfolio, while the 20-year is 20% and the 5-year is 18%. Altogether, the average maturity of the JGB holdings is 12 years. This maturity leaves the BOJ exposed to a significant amount of interest rate risk.

{kind=link}

With the large purchases in the current quarter to defend the upper band, the average maturity of the portfolio has increased to 16 years. Due to the overall rise in rates following the policy shift, we project that for the current quarter, the BOJ will increase the unrealized loss on their JGB portfolio by more than 16 trillion yen.

The cumulative unrealized loss is three- and one-half times the BOJ’s total capital of 5 trillion yen.

The BOJ has emphasized that unrealized bond losses won’t undermine their ability to guide monetary policy.

The impact of higher interest rates also ripples through the economy. Banks, the second-largest owners of JGB debt, are also experiencing balance sheet losses.

The extreme exposure to interest rate risk complicates any BOJ push to normalize rates.

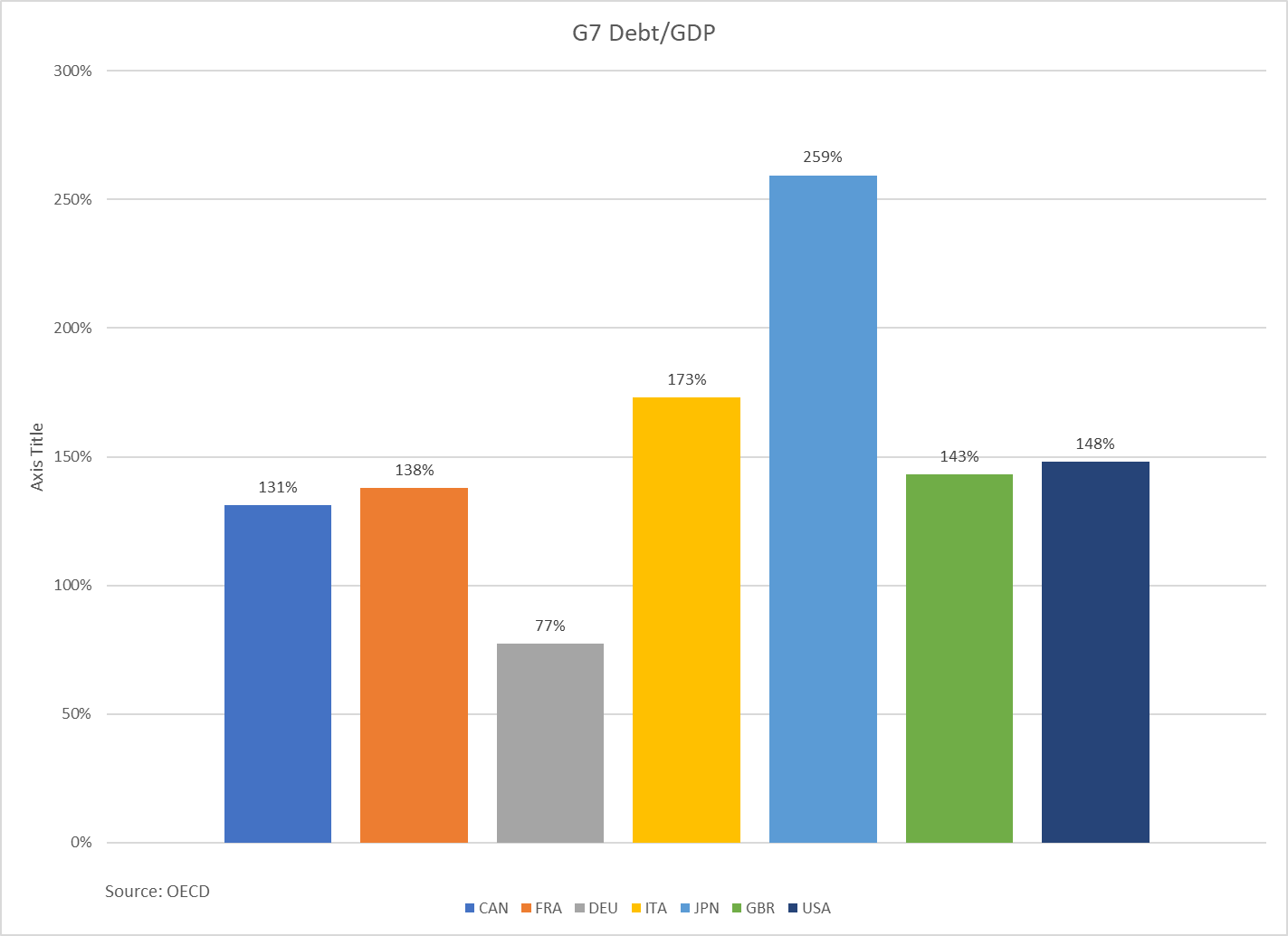

Another complication is that Japan is the most indebted country in the world. The government has borrowed heavily for over twenty years to stimulate the economy, with only questionable results. The net of this, though, is that Japan has the highest debt/GDP ratio in the world.

{kind=link}

This wasn’t a problem, however, because the bulk of the borrowing has been under a zero-interest rate policy. It doesn’t matter how much you borrow when it doesn’t cost you anything. As rates rise, though, the cost of the borrowing can become an overwhelming burden.

The BOJ is facing a conundrum. The policies it must implement to control inflation and strengthen the yen create huge problems for the government’s fiscal situation and their own financial position.

For further details see:

Why The Bank Of Japan Blinked