SRVR - Why The Fed's Call For A Housing Bottom Means Hawkish For Longer

2023-07-07 07:18:31 ET

Summary

- The Federal Reserve has noted a bottoming out in the housing market, with improvements in home sales, builder sentiment, and new construction since the start of the year.

- Despite a recent moderation in housing services inflation, the Fed has expressed concerns about potential risks due to low inventories of homes for sale, solid housing demand, and slower-than-expected deceleration in rent measures.

- The resilience of the housing market could lead the Fed to maintain a hawkish stance for longer, even after the rate hike cycle ends, with affordability issues potentially impacting worker mobility and labor markets.

The Federal Reserve's minutes for the June 13-14 meeting contained important commentary on the resurgent housing market. Most importantly, there appears to be a sense that the housing market has bottomed:

"Some participants remarked that the effect of high interest rates on the housing sector appeared to be bottoming out, with home sales, builder sentiment, and new construction all having improved a little since the start of the year."

"Improved a little" is an understatement for the year. Here are the numbers:

- Single-family new home sales are up 12.4% year-to-date (through May) versus -16.1% at this same time last year.

- Single-family existing home sales are up 6.7% year-to-date (through May) versus -11.2% at this same time last year.

- Builder sentiment is up 77.4% year-to-date (through June) versus -20.2% at this same time last year.

- Single-family housing starts are up 12.4% year-to-date (through May) versus -12.3% at this same time last year.

Accordingly, the iShares U.S. Home Construction ETF ( ITB ) was up 20.7% year-to-date through the end of May versus -26.5% at that same time last year. (ITB is up 34.9% year-to-date at the time of writing).

The iShares U.S. Home Construction ETF (ITB) has had a strong year despite high mortgage rates. (TradingView.com)

{kind=link}

This fresh strength in the housing market has the Fed worried about risks to expectations for a continued downward trend in housing services inflation:

"Some participants noted the recent moderation in housing services inflation and expected this trend to continue. However, a few participants pointed to upside risks to the outlook for housing services inflation associated with near-record low inventories of homes for sale, solid housing demand, and less-than-expected deceleration recently in measures of rents for leases signed by new tenants."

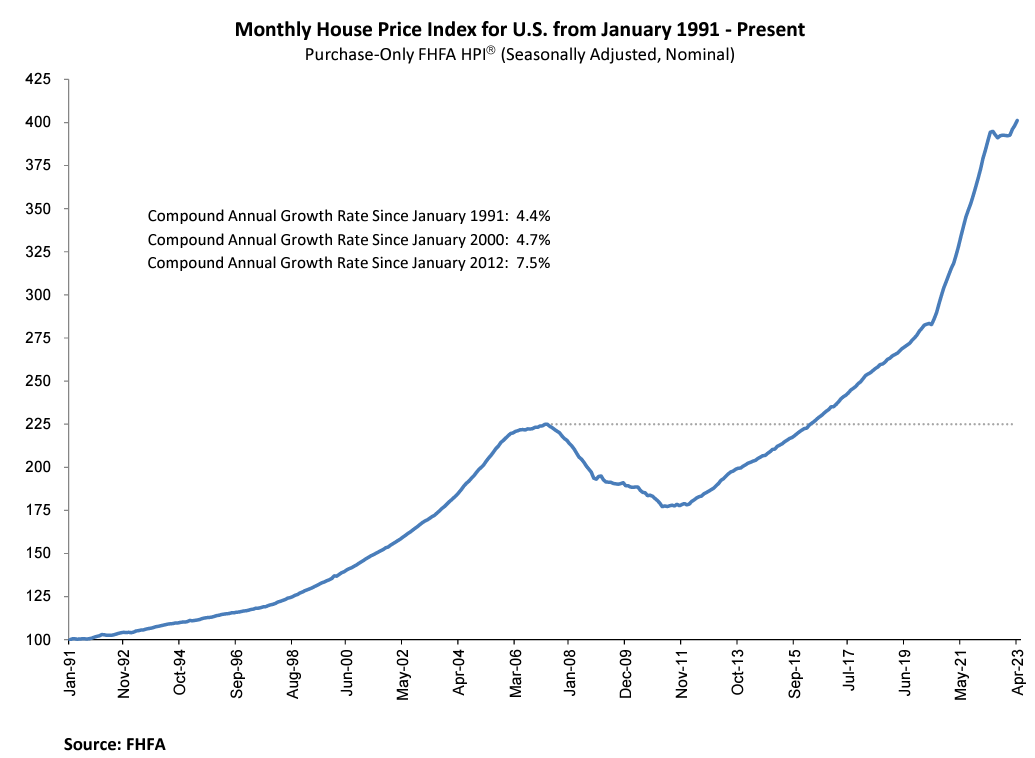

A bottom in housing would be just the catalyst to deliver the upside risk. Already, national price indices are showing a bottoming. For example, the latest FHFA Housing Price Index ((HPI)) Monthly Report shows that nationally aggregated prices are on the move again and back to setting all-time highs.

National housing prices barely rested before the latest move higher. (Federal Housing Finance Agency (FHFA))

{kind=link}

On a market-by-market basis, it is possible to see the moderation some participants are yearning for. Per the FHFA:

"For the nine census divisions, seasonally adjusted monthly price changes from March 2023 to April 2023 ranged from +0.1 percent in the Pacific division to +2.4 percent in the New England division. The 12-month changes ranged from -3.8 percent in the Pacific division to +6.1 percent in the East South Central division."

The FHFA even pointed out that "on a year-over-year basis, house prices in some regions of the country continued to decline." Still, if enough markets continue to experience rebounding prices, the Fed will have yet one more reason to be hawkish for longer.

The Lure of the New Normal

The Fed's understatement belies what must be a sense of bewilderment at the resilience of the housing market in the face of soaring rates. However, the 30-year mortgage rate rushed so much to price in Fed rate hikes that it peaked in November, one month after core inflation itself peaked . Subsequent rate hikes have only applied marginal upward pressure to mortgage rates. As a result, buyers have had all of 2023 to get acclimated to the new normal of higher rates and adjust buying preferences accordingly.

Ditto for home builders who have proven remarkably nimble in providing incentives and pricing flexibility to continue tapping into demand pent-up by limited (existing home) inventories. The lure of the new normal means that the Fed will need to stay hawkish for longer, otherwise it could risk unleashing even more robust, inflation-inducing housing activity.

The Affordability Issue

Plunging housing affordability still looms as the most likely potential brake on a resurgence in housing inflation. I wrote about affordability issues in my last housing market review . I included references to the Federal Reserve Bank of Atlanta's Home Ownership Affordability Monitor (HOAM) and Harvard University's Joint Center for Housing Studies (JCHS) 2023 annual report on The State of the Nation's Housing . Resilient prices could not only dampen demand at some point but also negatively impact worker mobility. Per the Fed minutes:

"A couple of participants conveyed that they heard at a recent Fed Listens event that, in various parts of the country, the lack of affordable housing in the area was preventing some lower-income workers from relocating to accept jobs."

If housing distorts labor markets, an aggregate inflation number may mask the cooling in markets where lower-income workers are "stuck" with lower opportunities while expensive markets face more inflation pressures through the higher wages required to incentivize moves. How these dynamics resolve will play an important role in how much longer the Fed will need to remain hawkish.

Hawkish for Longer

The resilience of the housing market is setting up conditions for the Fed to remain hawkish for longer even after the rate hike cycle comes to an end. Once the Fed feels it has pushed rates as high as it dares, I will look to the Fed to promote the reduction of the balance sheet as proof of its ongoing tightening. Given the March crisis in regional banking temporarily stalled balance sheet reduction, the Fed still has a lot of runway to stay hawkish for longer.

The Fed still has a LOT of work to do to "normalize" its balance sheet. (Board of Governors of the Federal Reserve System (US), Assets: Total Assets (Less Eliminations from Consolidation): Wednesday Level (WALCL), retrieved from FRED, Federal Reserve Bank of St. Louis; fred.stlouisfed.org, July 6, 2023.)

{kind=link}

Under these conditions, I am still comfortable declaring an end to the seasonally strong period for the stocks of home builders . I also suspect that the outsized gains of the latest season pulled forward gains from the next season. As a result, I will likely be more muted than usual when the next season kicks off in October or November.

In the meantime, ITB remains well-supported by uptrends in all its major moving averages. The most critical test will come when ITB next tests its 200-day moving average ((DMA)). At the current pace of trading, that test could conveniently come right before the next trading season begins…and the stock market resumes its anticipation of imminent rate cuts.

Be careful out there!

For further details see:

Why The Fed's Call For A Housing Bottom Means Hawkish For Longer