UPMMY - Why UPM-Kymmene Is Fully Valued And A 'Hold' Going Into 2023

Summary

- I haven't written about UPM in some time - but the time has come to revisit this, one of the most attractive Finnish forestry companies out there.

- The company has seen a more than doubling of the S&P 500 return since my last article - and that was even buying the business at a relatively expensive valuation.

- As we go into 2023, we face a company with a valuation that's relatively expansive already.

Dear readers/followers,

Remember UPM ( UPMKF )? It's one of those Scandinavian companies that are larger than you expect it to be. It's a combined forestry, fuel, and timber company, with appealing segments in multiple sectors and geographies, and one that also pays a very attractive overall dividend.

It's a company I've been long in for years, and it's also a business that has seen some very impressive amounts of overall outperformance, the least of which is during the period since my last article. Take a look at how things have gone.

Seeking Alpha UPM (Seeking Alpha)

As you can see, I did not even "time" the lowest level here, which means that total overall returns for my own average position in the time are almost up 15% in a time when the market is down close to double digits.

How is this possible and what should we expect from UPM going forward?

Let's take a look.

UPM - Why the company is richly valued for 2023E

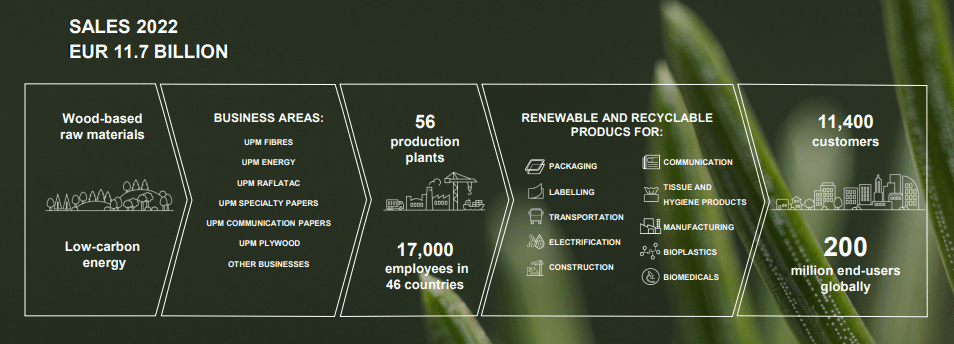

UPM was formed by a merger between two large Finnish forestry, combining it with the NA-based United Paper Mills in 1996, which means about 26 years' worth of overall history - and technically a very good history. In my initial article here , I pointed to the company's sales mix as a very good argument for appeal. Unlike most carton, timber, or energy companies, UPM does it all and does it all in an attractive mix that generates upwards of €10B in sales revenues on an annual basis.

2022 was a superb year for UPM - that's a big part of why the company outperformed. Why was it such a great year?

A few reasons. 4Q22 Sales increases of over 20%, EBIT increases of 42%, sales price increases successfully pushing and offsetting any macro impacts the company saw, an energy-impacted incoming operational cashflow of triple the amount of 4Q2021, leaving the company at the liquidity of over €6.4B at the end of the fiscal of 2022.

The company also saw advances in its various, global projects. The growth project in Uruguay is getting ready for start-up and the new pulp terminal in the port of Montevideo is operational since October.

The company now works, thanks to this, at a net debt/EBITDA ratio of under 1x, at around 0.94x.

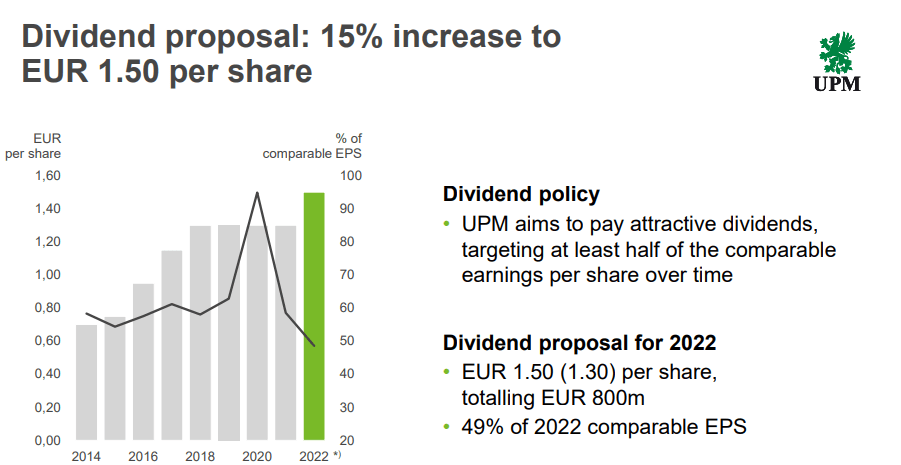

The company has also changed its dividend policy, and adopted a 100% earnings-based dividend policy, leading to a double-digit increase in the company dividend to €1.5/share.

As with most other companies, UPM has suspended everything having to do with Russia. It no longer delivers, purchases, or works with Russia, and the Chudovo plywood mill that the company owns is suspended in terms of operations. The company also decided and proceeded to sell the Steyrermühl site in Austria to secure competitiveness and adapt newsprint production to long-term market development - in that newsprint is only going one direction, that is down.

So, this is UPM for 2023 .

{kind=link}

The company is in every single attractive end-user segment out there, from pulp to raflatac, to fuels, to chemicals like lignin and glycols, to things like biocomposites. At the right valuation, this business is good enough to where I believe you should make it 3-5% of your portfolio.

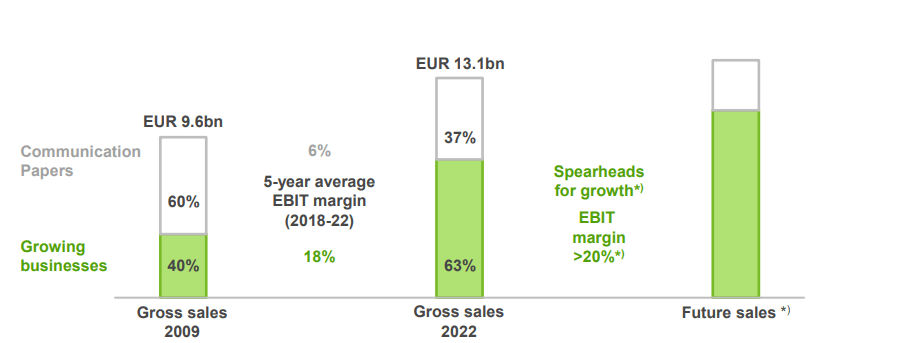

The company's focus on fibers, specialty, and biorefining is exactly in line with where the industry is currently headed. Take a look at how sales have changed in around 10 years, and how the mix has gone from papers to growing business.

{kind=link}

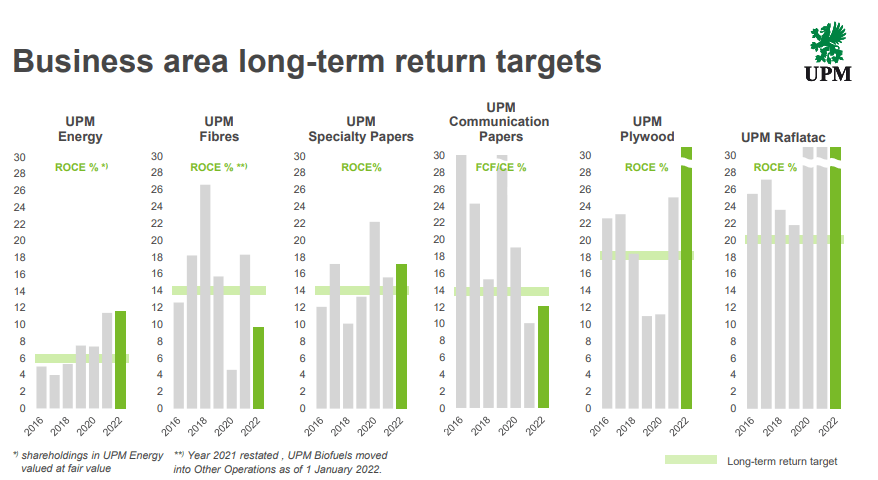

With records in annual earnings and results, as well as RoE, the company is in a very good position to "beat", going forward. All of the company's segments, with the exception of communication papers and Fibres, are currently within their ROCE targets.

{kind=link}

The company's overall capital allocation policy is split between a very attractive dividend, and high-return investments , at around a 40/60 split, while maintaining a below 2x net debt/EBITDA. Going forward, the company wants to size this at closer to 50/50, and allow for the debt to grow to 2x where necessary, but maintain a headroom.

This latest bump in the dividend represents the first real bump in several years, and it's a relatively big one.

{kind=link}

The latest few years represent some of the most transformative in this business's history, and the 2023E period is estimated to still consume about a billion euro worth of CapEx, including a majority spent on the growth projects for pulp in South America, and biochemicals in Germany.

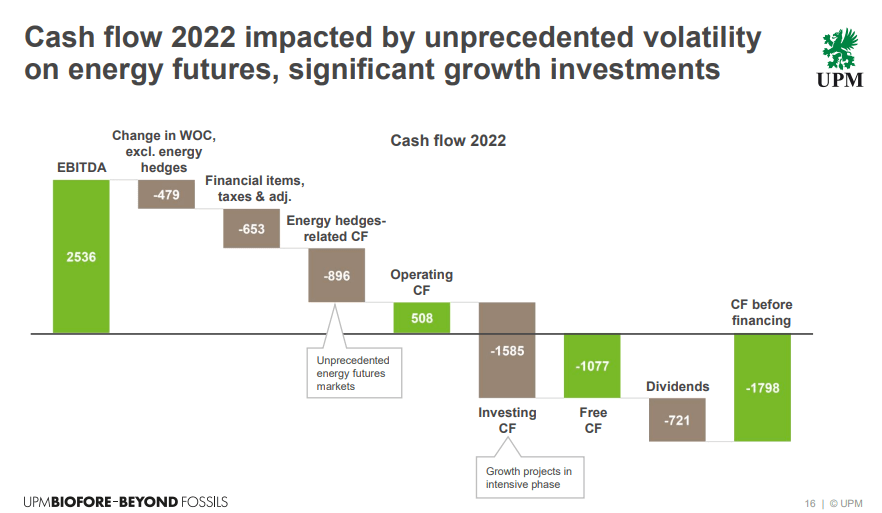

That is not to say that UPM has been without risks or impacts from the situation in 2022. Take a look at the cash flow bridge and how it has looked for the year.

{kind=link}

Maturities for the company are extremely well-laddered. Nothing major is coming until 2025, and most are well beyond 2024. Outlook for the coming year is a relatively positive one. This is due to increased delivery volumes as operational ramp-ups in Paso de los Toros, as well as the opening in China, which is expected to increase demand. Headwinds come in the form of a very high input cost level, while we've seen a slowly reverting demand situation, pushing product prices down. The combination of these two factors isn't necessarily positive, but several of these inputs have conceivably reached their peak here, and are set to start dropping again.

Significant uncertainties remain. Ukraine and Russia are only one of them, but it's one of the larger impacts due to its effect on energy prices, regulation in Europe, and the ramp-up of the company's nuclear power plant unit OL3. The company also owns a significant amount of forest that it manages effectively, and since 2008, a considerable amount of Southern American forest assets have been added to the mix here, to where 49% is now in Finland, 7% in the USA, and 44% in Uruguay. The trends for these are very different, with Uruguay being a fast turnover, but low inventory, but Finland being the exact opposite. The new Paso de los Toros will grow the Pulp output by over 50% at a highly competitive cash cost, with a scheduled start this quarter.

The investment also comes with some of the most modern logistical setups for this type of operation in the world.

{kind=link}

Remember, this is not the only thing where the company is "the best" or "the largest". UPM-Kymmene is the largest paper company in the world. The second-largest EU competitor, European Stora Enso ( OTCPK:SEOAY ), is a distant second with around half the capacity. I own both of these companies in my portfolio, and I will say that I'm well-versed in the ups, downs, and specificities of the Scandinavian and European paper, timber, pulp, and forest market. It's a segment I've invested in for the past 10-15 years, though more professionally for the past 5.

UPM is one of the most attractive names in this entire segment, and at the right price and valuation, I rate this as a must-"BUY".

That is not the case at this time, however.

Valuation for 2023 - the metrics are somewhat stretched

Now, I preface this by saying that I might be wrong here, and the company may go the exact opposite direction, shooting up even further on the back of increased deliveries, volumes, and solid pricing. However, whenever things are as positive as we've seen here, there's the risk of over-assuming the positive side of things.

UPM, while a great business, is not the super-stable investment you might be looking for. For over 10 years, the company's share price went absolutely nowhere . This is why the valuation when you do invest is so crucial, and why it's even more important than the specific qualities of the company - which might be great.

UPM is currently trading at €35/share. This represents a marked premium towards the latest 10-15 years. There are extremely good reasons, underlying ones, for why UPM is now worth more per share than 10 years ago. You will not find me disagreeing with this one obit.

However, I would not be doing my job if I did not say that compared to closer peers such as Enso, Metsä, and other international paper and forest product comps, UPM is now more expensive both in terms of EBITDA, revenues, book, and other metrics than these.

That's a warning - and it's a warning you should potentially heed. It's not that I believe the company might decline massively from today's level - no. I just believe UPM won't go much further than this.

The proof is in the pudding, as they say. A DCF assuming a double-digit discount range going to around 10.5% at the low point and a terminal growth rate of as high as 5-6%, comes to an overall valuation range of €32 on the low side to €38 on the high side. This comes to a conservative midpoint of €35, at the highest. That's also currently where UPM is actually trading.

Analyst targets mostly confirm this conservative picture. Remember that analysts tend towards being positive, so the current average of €37.5 isn't a vote of confidence that the company is going to rise those 7-8% - I would call this to be in the range of the margin of error. We can confirm this by being down in terms of analysts - less than half are now at a "BUY", compared to more than half when the company was below €30/share.

So, you can see how logical the appeal of the company is - or isn't - when a certain valuation presents itself. It's not that UPM is unattractive, it's that the price is.

I will be happy to buy more UPM once it hits closer to €30/share again. I believe this will happen as we see the results for 2023, impacted by pricing and input pressures, start to impact the company. I'm not selling my stake in UPM here though, and if it goes differently, I'm happy to hold my position at a great 6%+ yield here.

This is a great stock, and I don't see a reason to easily rotate it unless it starts getting clearly overvalued - which I see starting to happen at €40-€45/share.

Therefore, my UPM thesis is as follows here.

Thesis

- UPM is one of the world's best and most appealing, Finnish-based forestry and pulp/chemical companies with a good energy arm. It also has a great yield. At the right price, this company goes from being lukewarm to a full-fledged must-"BUY" - that's my view, at least.

- However, this requires the "right" valuation, and I want to see at least a €30/share price or below for that stance to materialize. It's not that it's not attractive at €35/share, I just don't think it's going much higher than that. My previous PT was €36/share.

- This still represents where I believe the company will go, but not far above it - so I stick to my target of 1 year ago because everything here was already included in what I expected there.

- UPM is a "HOLD" here.

Remember, I'm all about:

1. Buying undervalued - even if that undervaluation is slight, and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

2. If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

3. If the company doesn't go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

4. I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

The company, because of this, does not fulfill my valuation-related criteria, and therefore needs to be considered a "HOLD" at this time.

For further details see:

Why UPM-Kymmene Is Fully Valued And A 'Hold' Going Into 2023