VOLVY - Why Volvo's Order Decline Is Not A Problem

Summary

- Volvo Group reported earnings with 2022 revenues soaring YoY.

- Investors may be concerned about order decline, but it is part of a thoughtful strategy Volvo Group's management has undertaken to defend its margins.

- Electrified vehicle sales are climbing upward, making Volvo a serious player in this process.

- Most importantly, the company has a very high return on capital employed, which shows the quality of its management.

Introduction

The Volvo Group ( OTCPK:VOLVF , OTCPK:VOLAF , OTCPK:VOLVY ) recently released its Q4 and FY22 results . It has been a while since the company was among the first ones to adopt a restrictive order intake policy to manage its production and protect is margins. This strategy did pay off during 2022, as the company was the only European truck manufacturer able to keep its double-digit margins. To me, the company was an example of good management , where problems were anticipated and the right choices were made at the right time.

Let's go over the recent report to see how the company is performing and, in particular, what we should be expecting from the restrictive order intake policy in 2023.

Results

Before we start, let's keep in mind that Volvo Group is a Swedish company and, as such, it reports its earnings in SEK. For clarity's sake, I am using the conversion rate of 1USD=10 SEK, even though the current rate is 1:10,34.

Let's start with a few information about the recent results.

Here we see the main highlights for the quarter, with another net sales increase of 31% YoY excluding FX.

Volvo Group Q4 Results Presentation

{kind=link}

I really appreciate how Volvo Group always places next to its net sales its operating income performance, it is a sign the company wants investor to understand how profitable the company is. In this case, we are before a double-sided picture: while sales are increasing steadily, margins have somewhat flattened out and are actually trending slightly down. This is no big damaged as other peers experienced, but, still, I would like to see margins go up as volumes go up.

For the full year 2022, net sales amounted to $47.3 billion (vs. $37.2 in 2021). However, operating margins slightly declined as a percentage of total sales, coming in at $5.05 billion, a 10.7% margin - versus the $4.1 billion reported in 2021 which was equal to a margin of 11%.

Overall, here is how net sales are split by geography. We see Europe still accounting for 40% of total sales. Compared to last year, South America grew significantly, and this was no surprise for those who follow the industry in general (most truck manufacturer and construction and farming equipment makers have seen a huge growth in the continent).

Author, with data from Volvo Group report

If we break down the revenues by segment, we immediately spot the extreme importance trucks have for the company: the segment is three times larger than construction equipment, which is the second source of revenue for the company. Therefore, we have to pay attention to trucking in a particular way. On this, I will spend a few words in a moment.

Author, with data from Volvo Group report

Before we move on, let me highlight three facts before we look at two main points, that is the outlook for trucks and how Volvo's strategy of restrictive order intake is playing out.

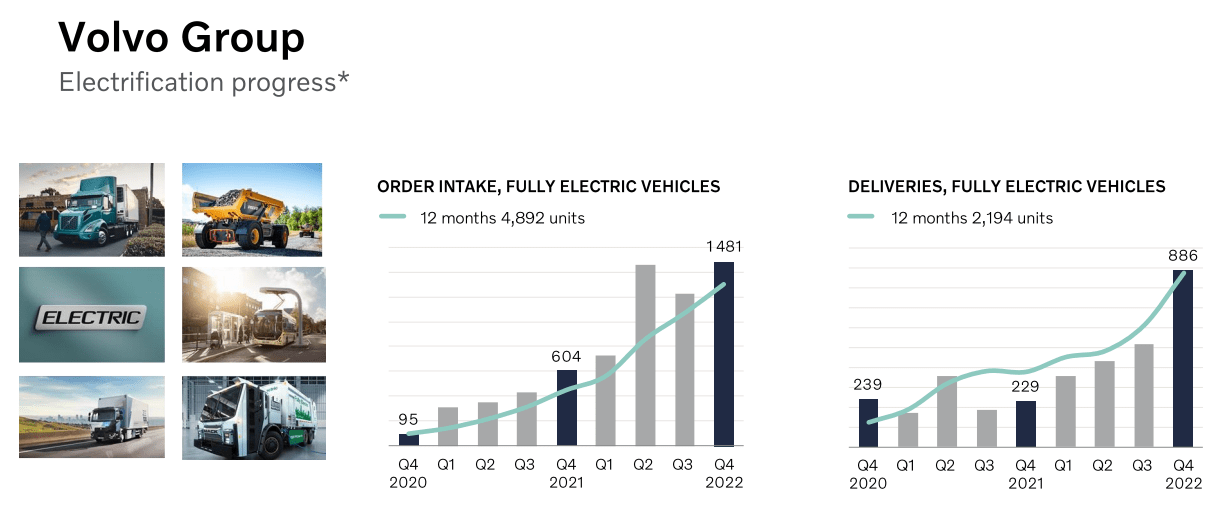

First highlight, Volvo is a major player in the electrification of trucks and construction equipment. In fact, I have it as my favorite pick among BEV trucks, as I outlined in this article . The Volvo Group is clearly able to manufacture electric vehicles and it is ramping up its production, which enables it to increase steadily its order intake, as shown by the two graphs below.

The company more than double the order intake, while almost achieving a fourfold on YoY deliveries.

Volvo Group Q4 Results Presentation

{kind=link}

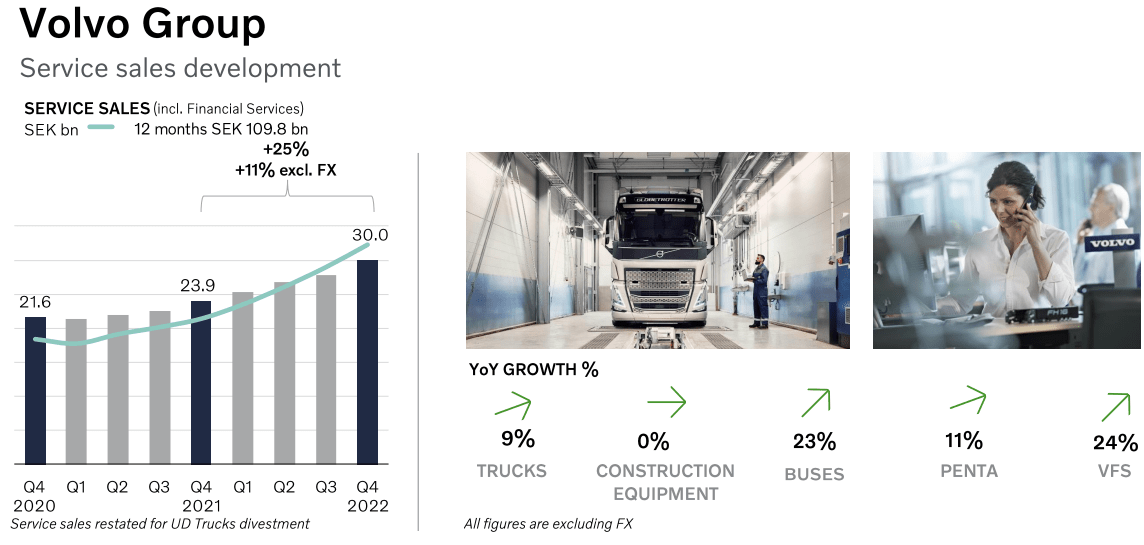

Second highlight. As most manufacturing companies are understanding, service sales are a key point for the health of the company. Companies selling consumer discretionary items, such as big vehicles, are much more exposed to economic cycles. However, there is a way to leverage the peaks of a cycle in order to smoothen the impact of the cycle's troughs: spare parts and assistance revenues. In fact, a company such as Volvo has to think that each vehicle it sells is not only a present revenue, but it is also a stream of future revenue as it will need maintenance and repair. During strong periods of growth, many vehicles are sold and this creates the perfect conditions for future spare parts and maintenance revenues.

As we can see, service sales are really moving in the right direction.

Volvo Group Q4 Results Presentation

{kind=link}

So, investors, be aware: as Volvo sells a lot of vehicles, future (high-margin) revenues are coming in, too.

Third and last highlight: Buses. This was the hardest-hit segment during the pandemic, for obvious reasons linked to travel. Now, the company reported that YoY net order intake increased by 70% to 1,781 units, primarily supported by coach orders in North and South America and important city bus orders in Europe. True, buses make up a small portion of total revenues, but, still, it is a business Volvo can achieve success. The only bad note was that margins, though improving, are still low at 3.4% (vs. -1% in Q4 21).

Restrictive order slotting

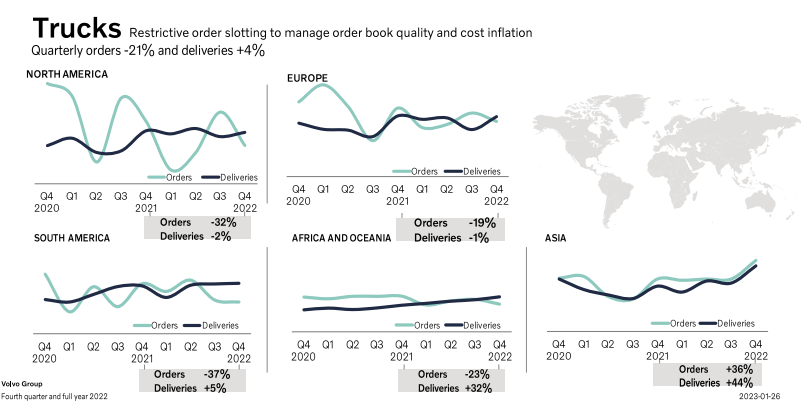

Let's talk about the strategy the company has been implementing for the past year: restrictive order slotting. For sure it has well defended Volvo Group's margins.

Let's see what is going on. Here we see orders and deliveries for trucks split by geographical market.

Volvo Group Q4 Results Presentation

{kind=link}

Now, while Europe seems to be stabilizing both in terms of orders and deliveries, some may be concerned about North America, where orders seem to be on a downward trend with lower highs and lower lows. However, deliveries are trending slightly upwards and this makes me think the company wants to reduce the big swings in orders to become more efficient in production and deliveries. Let's also notice how Asia is picking up thanks to China's easing Covid-policy.

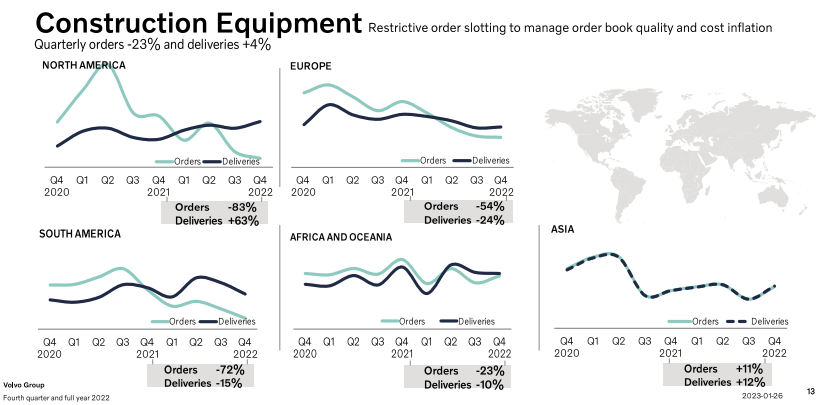

Let's also look at how construction equipment is performing. Here, the two main markets together with South America see orders go down since the peak of early 2021. I think this is partly due to the big effect across many Western countries government spending had on infrastructure, as part of a way to come of the Covid recession. Orders were very strong as infrastructure bills were approved which lead to a big order surge.

Volvo Group Q4 Results Presentation

{kind=link}

Truck outlook

I am not really worried about truck orders in North America. In fact, as I have shown in an article on PACCAR ( PCAR ), in the U.S. approximately 75% of public sector funding is going to highways and streets. This sets an argument to support a bull case for trucks, as we can see from the graph below, showing the amount of dollars spent on highway and street transportation.

U.S. Department of Transportation

{kind=link}

Secondly, according to the U.S. Department of Transportation , trucking contributed with $359.5 billion to the national GDP. This is the largest amount of all the freight modes.

Thirdly, trucking grew the fastest among the freight modes measured in the Transportation Services Index. It was also the most consistent freight mode in terms of steady growth.

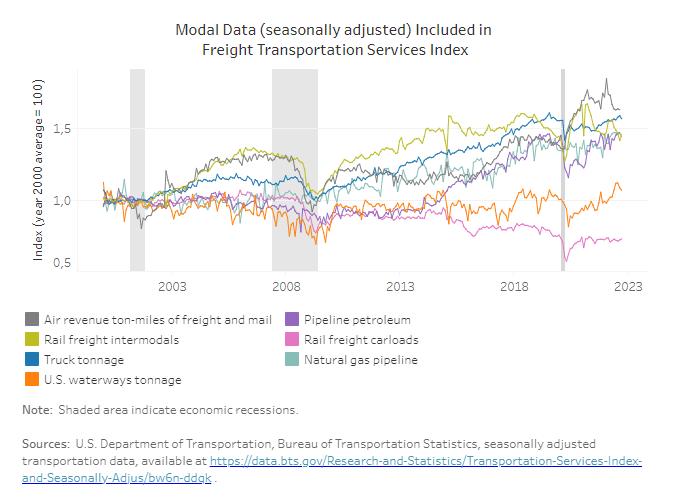

U.S. Department of Transportation

{kind=link}

Another reason why I am bullish on trucking, especially in North America, is shown in this last graph. Here we see how trucks carry the largest shares by value, tons and ton-miles for shipments moved less than 1,000 miles. Now, 82.9% of the value of goods moved in the U.S. travel a distance under 1,000 miles and this shows the need for trucks there is.

U.S. Department of Transportation

Return on capital employed

Looking at order intake, an investor may be concerned. However, I think I outline the whole context that shows from many point of views how demand for trucks is not going away anytime soon. In addition, Volvo has given up on purpose to increase its order books in order to gain better managing of its production while defending its margins. This led the company to a super result in terms of return on capital employed which is now at 27.4% vs 25.3 in 2021 and 14% in 2020. This is very smart management and extremely high results for a capital intensive business such as the one Volvo Group runs. I think this result is also due to the strategy of limiting order intake. This has led the company to use efficiently its production plants while being able to deliver accordingly new vehicles without having inventories to up dramatically, thus freezing working capital.

Valuation and conclusion

Based on these last results, I still think the Quant Valuation Grade is correct when it awards Volvo Group an A which goes along with an A- on Profitability.

The company currently trades at a fwd PE of 12 and a fwd EV/EBITDA of 8, not very high metrics in today's market. Volvo Group has proven many times it knows how to make money and be profitable and it has a growing service business that should defend it from downturns. This is why I still stick to my target price of $33, thinking the company has significant upside.

For further details see:

Why Volvo's Order Decline Is Not A Problem