WPC - Why W. P. Carey Is My Top Pick For September

2023-09-06 08:30:00 ET

Summary

- W. P. Carey is a top pick for high yield in the current market, with a stable business model and mostly CPI-linked rent escalators.

- The company focuses on mission-critical properties and has a diverse tenant base, with international exposure for sourcing properties.

- Concerns include economic uncertainty and higher inflation, but WPC benefits from less competition for deals and a strong balance sheet.

Time flies, and with Labor Day marking the unofficial end of summer, it's time to take stock of one's portfolio with two-thirds of 2023 now in the pocket. With plenty of headline making financial events, including the regional banking crisis, the AI-led tech rally, and questions around a recession and interest rates, I continue to believe solid dividend paying stocks are the way to go as we look toward the last few months of 2023 and beyond.

This brings me to W. P. Carey ( WPC ), which I last covered here back in May with a Strong Buy rating. I wish I had my crystal ball, as WPC has given investors a -4% total return (including dividends) since then. However, I remain undeterred and in this article, discuss why WPC is a top pick in the current frothy market for high yield, so let's dive in!

Why WPC?

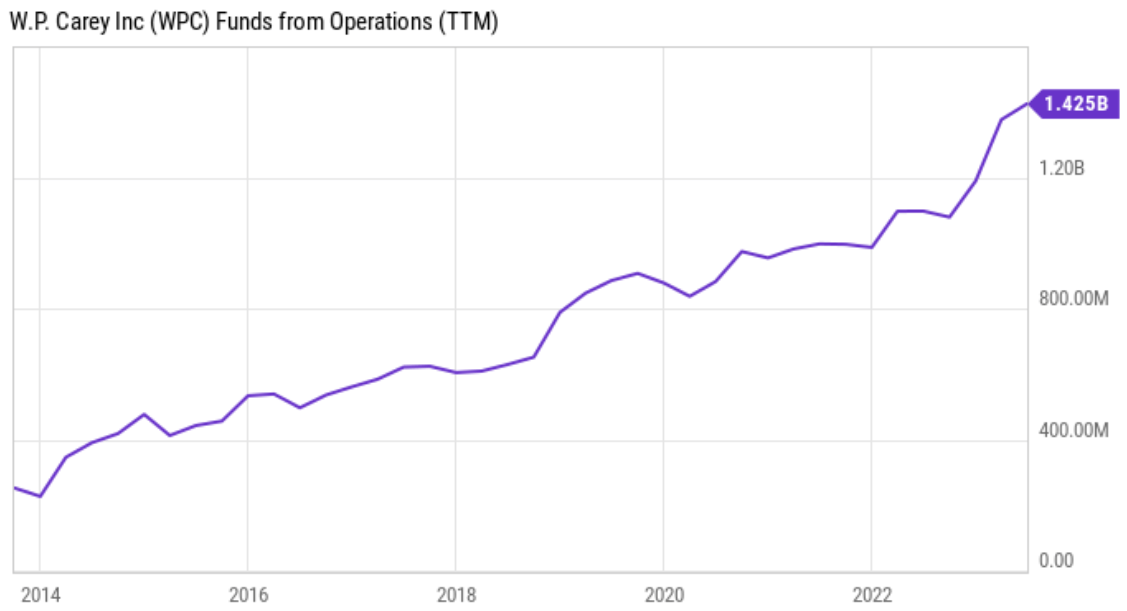

W. P. Carey is one of the premier net lease REITs with a long history of shareholder returns, and is often mentioned in the same breath as Realty Income Corp. ( O ) and NNN REIT ( NNN ). While O and NNN are certainly quality picks in their own right, their dividend yields simply aren't close to what WPC is currently offering. As shown below, WPC has a fairly strong record of growing funds from operations, with growth accelerating over the past 12 months.

{kind=link}

YCharts

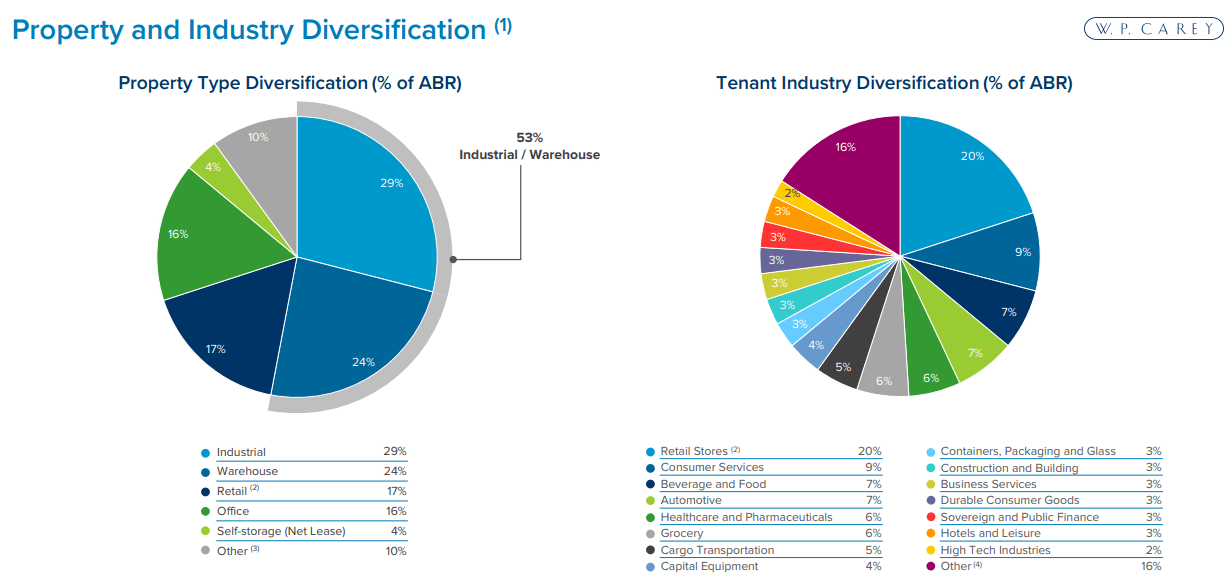

The company has been around for longer than some investors have been alive, with it having recently celebrated its 50th anniversary. What sets WPC from its net aforementioned net lease peers is its focus on mission-critical properties and retail properties makes up just 17% of its annualized base rent. At present, it holds 1,475 properties that are spread across 398 diverse tenants, and as shown below, Industrial and Warehouse property types make up just over half (53%) of ABR.

{kind=link}

Investor Presentation

WPC also has geographic diversification, as it sources 39% of its ABR from outside the U.S., primarily in Northern and Western Europe. Having international exposure opens up the playing field for WPC in that it has opportunities to source properties at attractive cap rates wherever they may be. It also opens up diverse sources of capital, particularly Eurobonds, which historically come with lower interest rates. This includes the recent entering of a three-year €500 million unsecured term loan and execution of an interest rate swap that fixed the rate at 4.34% through the end of next year.

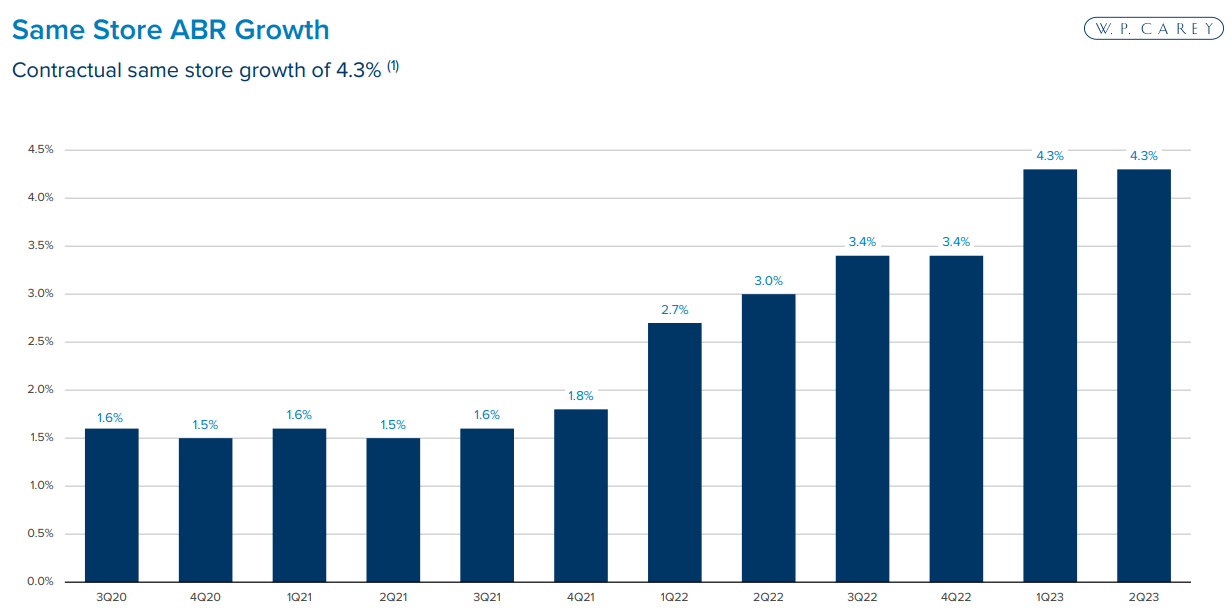

Meanwhile, WPC is benefitting from higher inflation, since 54% of its leases come with CPI-linked rent escalators. This, on top of strong 99.0% occupancy and net lease properties acquired under the CPA 18 merger contributed to 4.3% YoY same-store rent growth during the second quarter. Management expects to continue leading net lease peers in rent growth due to the lagged effect of CPI and rents and the strength of its fixed rent increases. As shown below, WPC's same-store ABR growth over the past 2 quarters has been at its highest over the past 3 years.

{kind=link}

Investor Presentation

Concerns around WPC include economic uncertainty, which could result in stress on tenants. Also, higher than expected inflation could outpace WPC's rent growth, considering that 43% of its leases have fixed rent increases, which were negotiated when interest rates were lower. Also, higher interest rates would raise WPC's cost of debt.

However, the silver lining for well-capitalized REITs such as WPC comes from less competition for deals, as higher leveraged players get priced out of the market due to their over-reliance on debt. WPC has been able to source properties in recent months at a 7.3% cap rate, which is 120 bps higher than what it was last year, and this translates into unlevered IRR in the 8s and 9s, when taking into account rent growth on the long-term leases.

While WPC's lower share price means that cost of equity is higher, it still had $385 million in unsettled forward equity at the start of the current quarter in progress, which was raised at the much higher share price of $83. This equates to a 6.3% cost of equity, based on forward FFO/share of $5.26, as it sits 100 bps below the cap rate on new acquisitions.

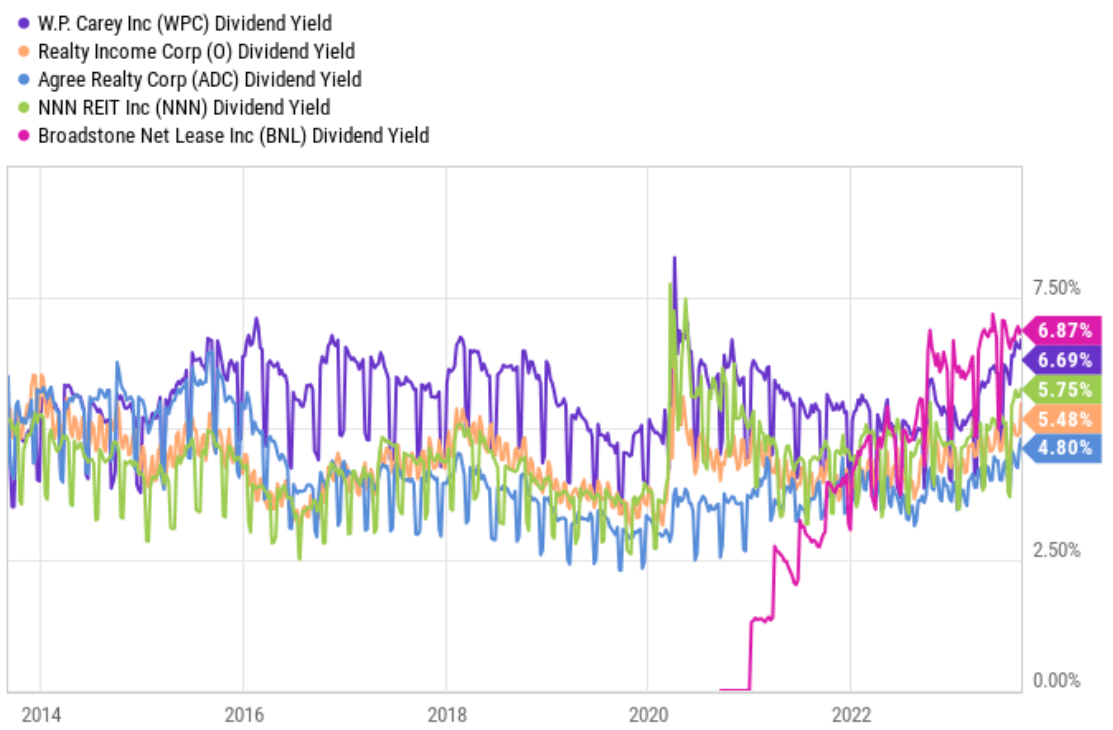

Importantly, WPC has the backing of a strong BBB+ with a net debt to EBITDA ratio of 5.7x and a strong fixed charge coverage ratio of 5.2x. The 6.6% dividend yield is covered by an 81% payout ratio and sits higher than most its net lease peers, with the exception of Broadstone Net Lease ( BNL ), which doesn't have the long track record of WPC.

(Note: The following chart shows TTM Yield. WPC's forward yield is 6.71%)

{kind=link}

Lastly, WPC represents solid value at the current price of $63.75 with forward P/FFO of 12.1, sitting below O's 13.4 and just slightly above the 12.0 of retail focused NNN. With stabilizing interest rates, low single digit rent growth and a 6.7% dividend yield, WPC could reasonably deliver 9-10% annual total returns even without a reversion to its mean valuation of around 15 P/FFO over the past decade.

Investor Takeaway

W. P. Carey is a premier net lease REIT and has been around for 50 years, having weathered through multiple interest rate cycles and economic downturns. It benefits from an asset base of mission-critical properties spread internationally. WPC is also seeing more attractive cap rates due to higher leveraged players being priced out of the market. With a high and well-covered dividend yield, a below average valuation, and a stable business model, WPC stock represents an appealing opportunity at its current valuation.

For further details see:

Why W. P. Carey Is My Top Pick For September