VNOM - Why We Are Loading Up On This Big Yield: Viper Energy

2023-08-28 07:35:00 ET

Summary

- Viper Energy Partners LP plans to change from a partnership to a corporation by year-end to increase valuation and stock price.

- The company's royalty interests in oil and gas properties in the Permian Basin have resulted in rapid production growth.

- The company's base distribution has been rising rapidly, and it expects continued growth in cash flow and income.

Co-authored with Long Player

Viper Energy Partners LP ( VNOM ) is a mineral royalty corporation formed by Diamondback Energy ( FANG ). This company owns and acquires mineral and royalty interests in oil and natural gas properties, primarily in the Permian Basin in West Texas.

VNOM has long been a growth and income play. The income part is a variable income. Recently, oil prices have begun to strengthen, so there is likely to be some appreciation potential ahead. However, management is adding their own plans to that potential because management will be changing the partnership to a corporation by year-end in the hopes of a higher valuation throughout the business cycle. That should add an extra bounce to the coming price recovery while assuring a higher stock price valuation throughout future business cycles.

Note: Although currently structured as a partnership, VNOM previously elected to be taxed as a C-Corp and therefore has been issuing Form 1099 to investors (rather than a K-1).

There will not be any change to how the company functions. The payout ratio and acquisition strategy will remain untouched. Shareholders will get to vote as they do with any corporation. But FANG will continue to own the majority of outstanding shares. Therefore, Diamondback will continue to control the company.

Royalty Company

The fairly rapid growth of VNOM is expected to continue. The company has royalty interests in some very good acreage because management does not purchase a royalty interest unless it expects the acreage to be developed. This differs from other companies that purchase a royalty interest in a broad area and then wait for someone to develop the area. Even though management does not control the rate of development, it attempts to control whether or not the acreage will be developed. This has resulted in fast production growth.

Royalty companies bear none of the exploration or development risks of upstream companies. Instead, they simply collect a percentage of oil produced while paying for the cost of that production. As a result, the company has no capital costs other than the royalty purchased for the production received. The downside is that the royalty company does not control the development of the leases in which it owns an interest. This management tries hard to minimize the risk of non-development during the evaluation process of the leases before purchasing a royalty interest.

Second Quarter

Production increased from the first quarter by about 5%. Production is expected to increase in each quarter for the foreseeable future. Diamondback is the main operator as well as the controlling company. This gives Viper Energy Partners unusual visibility into future development plans. Many of the other operators in the royalty holdings are likewise well-known names with excellent reputations. Diamondback is the most material.

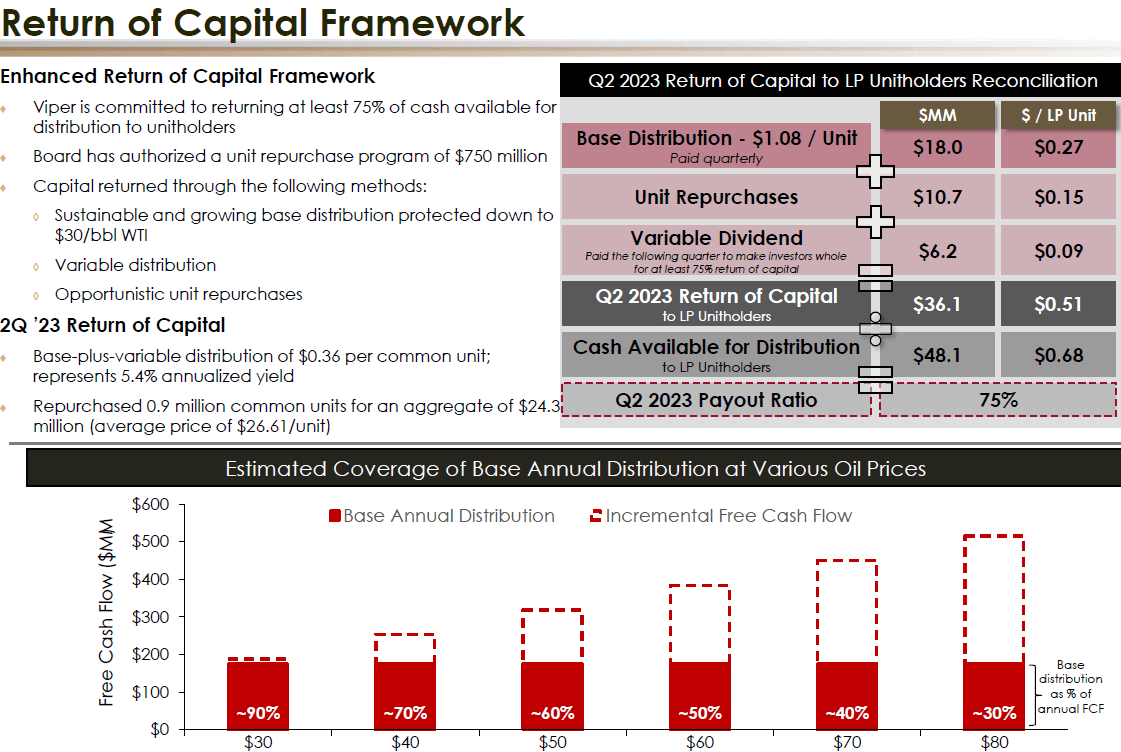

At the same time, management increased the base distribution to $1.08. The base distribution has been rising rapidly, and this part is expected to be paid even at the bottom of the industry cycle unless that bottom is unusually low (or sustained for an unexpectedly long amount of time). This differs from the past when the distribution was totally recalculated each dividend.

The payout model has changed from 100% payout to the current 75% payout. The current model allows for debt repayment along with some opportunistic royalty acquisitions from time to time. In this organization, debt ratios remain a priority. In light of this, management aims to have cautious debt ratios under far more conservative assumptions than is the case now.

Part of the 75% payout to shareholders includes a variable distribution of $0.09 per share for the quarter and the repurchase of shares of common stock. The stock purchase program ensures that per-share growth exceeds the already substantial production growth posted by the company. It is also another sign that the company believes its shares are relatively cheap. This is the second indication the shareholders have received this quarter after the notice to convert to a corporation.

It is a relatively new idea for royalty companies to live within their means. Before, just like the midstream industry, this industry would make periodic trips to the capital market to make royalty acquisitions or any other balance sheet needs. But the stock market and the debt market have essentially put an end to that practice. Now, these companies, like midstream, have higher valuations if they live within their means.

Return of Capital Guidance

The underlying assumption is that the wells that Diamondback drills have unusually low breakeven points. Therefore, it takes an unusually severe downturn for production growth to stop. Because the partnership does not own an interest in all Diamondback acreage, the growth rate can be (and usually is) different. Source

VNOM Aug 2023 Investor Presentation

{kind=link}

As can be seen above, this company expects to be able to pay a base distribution under some rather extreme industry conditions. Even the variable distribution and stock purchases can take place under some hostile conditions. All of this testifies to the low cost of a royalty interest. Diamondback has very low production costs. Therefore, Viper has low costs as well.

The reason for considering the purchase of the stock now is that with rising oil prices, the variable distribution is likely to grow over time as well. Income investors need to consider that the Diamondback organization overall is an opportunistic repurchaser of shares of stock. Therefore, if management sees an unusually low stock price, they will not hesitate to redirect some cash to stock repurchases for a quarter at the expense of the variable distribution. Nonetheless, fewer shares outstanding will mean more cash outstanding for distributions in the future.

Summary

The rapid growth of production combined with the share repurchase plan ensures that the amount of cash per share will grow at a good clip at various oil prices. Even if an acquisition would result in Diamondback dropping an unusually large royalty interest that would require stock, that situation would likely be accretive as well to shareholders. It is also less likely to occur in the future than in the past, though it is still a possibility.

VNOM Aug 2023 Investor Presentation

{kind=link}

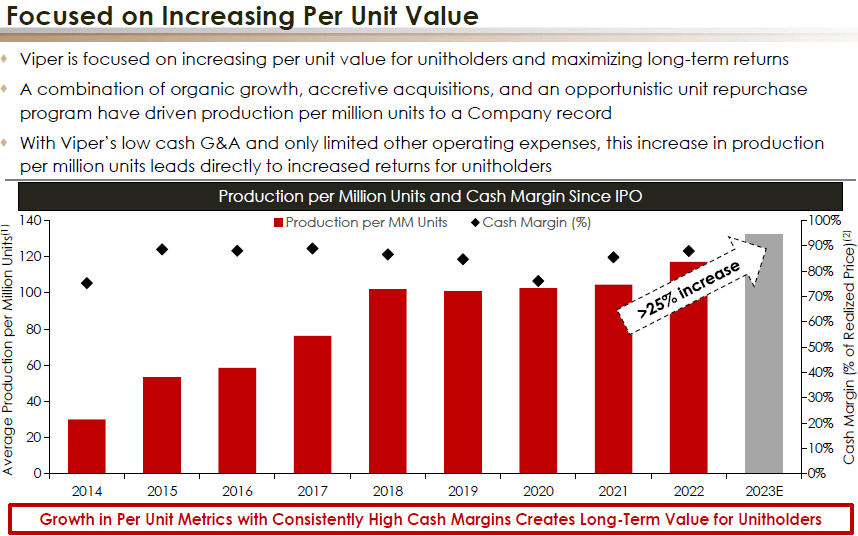

Obviously, growth has slowed in recent years as the company has become larger. However, at least one year, fiscal year 2020, was due to the pandemic challenges. Even so, the performance shown above was better than many upstream companies during the pandemic times.

There has been an emphasis on balance sheet repair after debt market requirements changed quite a bit. This partnership was no exception. However, the choice of acreage has allowed production to continue to climb while debt ratios have become more conservative. Many upstream companies cannot do that.

Since there are no maintenance requirements in a royalty interest, much of the cash that is collected can be used in the calculation for shareholders. This is strongly implied by the margin shown before. There are not many expenses (relatively speaking) for a company like this.

The rapid growth in production and hence the rapid growth of the base distribution should continue long into the future. The current 5% sequential quarterly growth implies a more than 20% compounded annual growth. Just a little bit faster growth would allow for a 25% compounded return which would triple the production per share every five years. That implies a lot of income growth ahead. For investors that can handle the variable distribution and stock repurchases, an investment in this equity should produce outstanding cash flow for years to come.

The yield in the second quarter was ~5.4%. They increased the base distribution to $0.27 quarterly and then had another $0.09 variable in the second quarter while repurchasing 900,000 shares of common stock. That was the second quarter of 75% cash flow available to shareholders. Oil prices have strengthened since the second quarter. With one month to go, if that trend remains, there will be more money to be returned to shareholders. This is why we are loading up on this great yield!

For further details see:

Why We Are Loading Up On This Big Yield: Viper Energy