CCI - Why We Bought More SBA Communications

2023-03-28 17:55:29 ET

Summary

- Massive growth in mobile data requires continued investment in infrastructure.

- Interest expense guidance came in below my projections. That may be because management is looking at using free cash flow to pay down exposure to variable-rate debts.

- SBAC has a very low dividend payout ratio, resulting in a substantial amount of retained cash flows.

- Higher interest rates are bringing multiples lower and discouraging the big carriers from expanding their networks as they are still bloated with debt from bad ideas.

- SBAC is a strong buy for investors willing to wait for the scenario to play out. We're making a prediction over several years, not over the next month.

One of the REITs I'm bullish on is SBA Communications (SBAC). SBAC is one of three tower REITs. The other two are Crown Castle International ( CCI ) and American Tower ( AMT ). I'm invested in all three of these REITs.

This article is going to focus on the fundamentals.

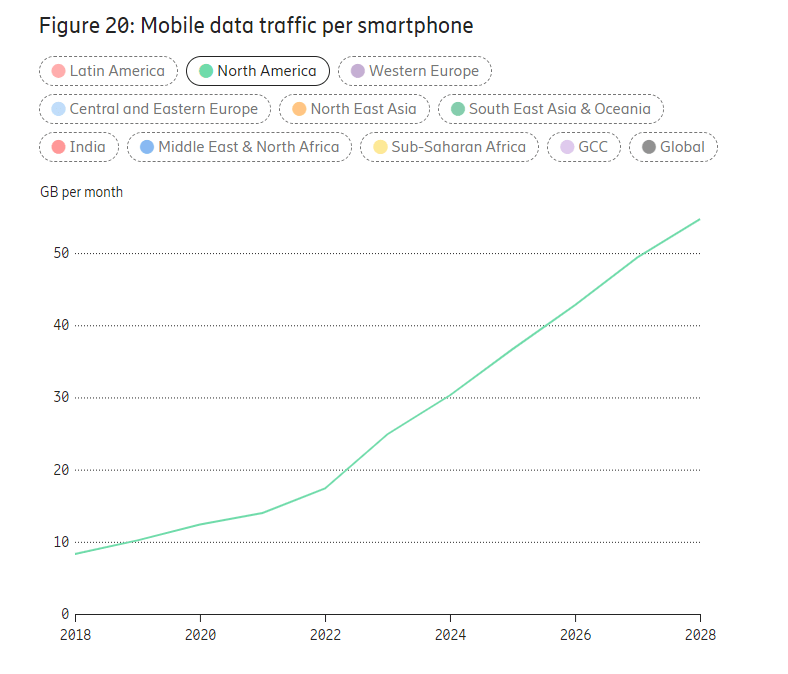

However, I need to touch on mobile data use briefly. It's always important when discussing tower REITs.

{kind=link}

I isolated the projected growth in data for North America. That's in GB per month per smartphone. The number of smartphones is increasing and the amount of data consumers demand is increasing.

Carriers can choose to build out the necessary bandwidth or their networks can become more congested. If they all stop building, maybe we can face the real oligopoly challenge of a few ancient companies failing to innovate and just using political pressure to prevent competition so they can remain relevant.

Pretty sure everyone knows that was about AT&T ( T ) and Verizon ( VZ ).

Remember when T and VZ produced poor returns for shareholders for the past decade while T-Mobile ( TMUS ) delivered more than 900%? That's today. It also was last month. And several other months. That's basically what a history textbook in investing would say.

Let's go back and review some words from a man who warned us it was going to happen. John Legere referred to Verizon and AT&T as "dumb and dumber." He claimed Verizon was going to achieve the status of "Dumber." For those who don't know, he was the CEO who brought T-Mobile to dominate the carrier market. He delivered enormous value to shareholders, as evidenced in the share price of TMUS.

He said Verizon invested billions to acquire junk. He was right. He said: "Millennials still will hate them." I think he was right about that also.

The smart move was building a better network and charging consumers a less obscene price. Verizon and AT&T spent billions on junk, when they could've been building that network.

Now, we're going to move over to the fundamentals.

Interest Expense

Almost all REITs are seeing increased interest expense in 2023. To be fair, the vast majority of stocks are also seeing an increase in interest expense.

I projected interest expense would increase by about $47 million. SBAC provided their guidance using "net interest expense." Since they will receive higher income on cash balances, this metric should grow a bit less.

Guidance predicted an increase of $36 million. I believe part of the difference comes from management's commentary about their plan for cash flows.

Cash Flow for Dividends and Debt

SBAC pays out a very small dividend at 27% of projected AFFO. They retain a large portion of cash flows (expected 73% retention in 2023) and suggested they would look to pay down variable rate debt using that cash flow. They already reduced their debts slightly.

If SBAC simply used all retained cash flows to pay off variable-rate debt, they would eliminate the vast majority of it within the year. AFFO attributable to SBAC remaining after dividend payments should be very close to $1 billion. I'm forecasting about $1.007 billion.

That's how SBAC can deliver better guidance on interest expense.

AFFO Per Share

For readers unfamiliar with AFFO, it's a metric that generally approximates cash flow. It's a bit more stable than using actual cash flows because AFFO doesn't care whether a rental payment was deposited on 12/29/2022 or 01/02/2023. It simply matches up with the period the rent covers, which is the treatment we want.

SBAC reports "AFFO per share" and "AFFO per share attributable to SBA Communications Corporation." I prefer to use the second, so when I say "AFFO per share," you'll know I'm actually talking about the part attributable to SBAC. The difference is pretty small (pennies or less), but it's one of the annoyances of having minority interests. Some sources will report a slightly different metric.

- SBAC's 2021 AFFO per share: $10.74

- SBAC's 2022 AFFO per share: $12.23 vs. $12.26 consensus estimate from early February.

- SBAC 2023 AFFO per share guidance: $12.59 midpoint ($12.41 to $12.77) vs. $12.84 consensus estimate from early February.

- SBAC's headwind from financing costs and foreign exchange per share: - $.425

- SBAC's 2023 Projected AFFO per share growth: 2.9% vs 6.4% without headwinds.

Note: SBAC significantly outperformed guidance for 2022. The original guidance for 2022 was $11.665 ($11.48 to $11.85). The huge growth in 2022 is creating a harder year-over-year comparison.

Further, on the earnings call , management stated:

We have been careful with our guidance and with our commentary not to get ahead of our customers.

The guidance certainly doesn't seem too aggressive.

History and Consensus Forecasts

I think the consensus AFFO forecasts for SBAC are within reason. The 2025 forecast may be a bit low.

{kind=link}

We expect to average at least high single-digit growth rates. There's a good chance for growth rates in the low double-digits on average. However, averages will include a few lower years.

Valuation

SBAC currently trades at about 20.5x forward FFO and 19.8x forward AFFO:

{kind=link}

Based on multiples, that's about where they were trading in late 2017. However, the share price is materially higher because FFO and AFFO increased dramatically. That ability to grow FFO and AFFO is why we want the REIT.

So what is weighing on tower REITs? Two factors stand out to me:

- Higher interest rates are hurting valuations for growth REITs. Tower REITs are a growth play and investors become impatient when they can get over 4% on cash. I don't think short-term rates will remain at these levels for very long. I'll be thoroughly surprised if there are no interest rate cuts by the end of 2024. I think interest rate cuts within 2023 would not be surprising.

- The big carriers in the United States took on vastly too much debt. That's a topic I plan to cover in more depth for another article. However, it's important to touch on it here. There are concerns about revenue growth because two of the major customers mismanaged their own cash flows. Somehow those carriers couldn't stick to the simple business of providing cell phone service and increasing speeds.

Dual Impact of Interest Rates

Both of these factors can be improved by a reduction in interest rates. Investors would be more interested in growth and the debt costs for the carriers would come down.

I expect rates to come down either in late 2023 or in 2024. That's a topic for another article because I don't want to derail this discussion.

Conclusion

Strong demand for mobile data means carriers will still need to spend capital on expanding their networks. They can divert some of it to uses that a CEO legend referred to as "dumb" and "junk," but it's a terrible move. The most useful thing for them to spend money on is a better network. That network runs through AMT, CCI, and SBAC. Leasing towers from REITs is significantly less capital-intensive than building their own towers.

It works for the tower business model because the tower can lease space to multiple tenants on the same tower. The only reason to build a tower for one tenant is because you believe there is a good chance that you can sign another tenant to the location. You don't need to get multiple tenants at every location, but you do need to do it often enough to keep shareholders happy.

SBAC has done that very well.

We increased our position in SBAC on 3/3/2023 at $259.56. We're slightly underwater on those shares (about 3%), but still confident in our choice.

Rating: Strong buy on SBAC. This is a long-term play. We can't predict the next month, but the long-term picture looks good.

For further details see:

Why We Bought More SBA Communications