VGSH - Why You Should Aim For $2 Million For Retirement

2023-04-01 09:00:00 ET

Summary

- What should be your retirement goals? Obviously, the answer depends on many factors that we explain in the article.

- The key to a successful retirement is always keeping your expenses significantly lower than your income. We recommend expenses to be no more than 80% to 85% of your after-tax income.

- In this article, we discuss why folks in their 40s and 50s would need $2 million or more to retire comfortably. We also discuss the strategies that can help them to achieve these goals even if they are starting late.

Retirement planning is not overly complicated. But it does require strong will, some effort, discipline, and due diligence. Due to rampant inflation in the last couple of years, retirement goals have been moving up. No longer is $1 million the dreamy goalpost as it used to be back in the early 2000s. The younger you are, the higher will be your goal post.

This is mainly because of two reasons. The first reason is obviously the impact of inflation in the coming years. It is unlikely that we are going to see an under 2% inflation rate any time soon. The low rate of inflation that we saw in the late 1990s and the first two decades of the 2000s was the direct result of the wide adoption of globalization. More recently, to some extent, what we are seeing is the reverse of globalization, especially after facing supply chain issues after the pandemic. This trend is likely to continue.

This is not to say that globalization is over for good, but the benefits of globalization are going to be less and less impactful. We feel there are much higher chances that the new normal for the average rate of inflation would be in the range of 3% to 4% for quite some time rather than under 2%. So, this would have a far-reaching impact on your retirement savings goals. There is a second factor that is more relevant to younger folks. The Social Security benefits that we have today for current retirees (or near-term retirees) are on an unsustainable path. Since this is such a hot-button issue for both political parties, we are not going to see any type of reforms until the end of this decade. Eventually, Congress and a future President will have to find some workable reforms.

So, one can draw some likely scenarios. For folks between 40-50, they would probably see the benefits eligibility age moving up by a few years. For folks, who are under 40 currently, they will likely see some combination of delayed eligibility, reduced benefits, higher taxes, and possibly some kind of means testing. Sure, we can't see the future; we can only try to make educated guesswork. But the conclusion is that younger folks should prepare for higher savings and for longer.

Table-1:

| Age-group |

| Likely Preferable Retirement Goals |

| Age group: 20-35-Year-Olds |

| $4 million |

| Age group: 36-45-Year-Olds |

| $3 to $3.5 million |

| Age group: 46-55-Year-Olds |

| $2 to $3 million |

| Age group: 55-Year-Olds and above |

| $1.5 million or higher |

When to retire?

As people are living longer and staying healthier into their 60s and 70s, the retirement age is gradually moving up as well. In fact, many people do not want to retire early, as they think a 9-5 routine keeps them younger, healthier, and engaged in meaningful work. That said, it would vary based on many factors, including personal situation. Finally, it comes down to your spending needs and if your expected income can meet those expenses. Obviously, there is no one answer, and it can vary from person to person.

So, the first step is to estimate in realistic terms what your expenses would be in retirement. Many financial advisors overestimate it by using standard formulas, for example, 80% of your gross income prior to retirement. We do not believe in these methods as they are too generic and leave out the individual factors entirely. So, it is best to estimate this on an individualized basis.

Why saving early and saving enough is critical?

We believe one of the most important factors that determine how wealthy you are going to be later in life has to do with how soon you are willing to start saving and paying yourself first. In other words, start saving for retirement. The easiest way to save is by means of setting up auto-deduct or auto-transfer. The amount that you never see in your regular account usually does not get spent.

Why Bank deposits or CDs are bad for long-term retirement Goals?

It is also important to know how you invest your savings. Keeping your savings in cash or a bank savings account does not do much good. Even today, when you can get much higher interest rates on Bank CDs compared to two years ago, they can barely match the rate of inflation. So, essentially you are losing money every day that you postpone an investment plan. It is not to say that you need no cash savings. You need an emergency cash fund worth six to nine months of your living expenses, but that's all you need to have in cash or short-term deposits. Also, they may serve a useful purpose for short-term cash or for older investors.

How to determine your retirement goals:

Back in early 2000, most financial planners agreed on $1 million as a standard goalpost to be able to retire comfortably. We will keep these goals a bit more conservative and assume that retirement savings of $750,000 were good enough back in the year 2000. If we calculate the inflation-adjusted value, the same $750,00 would amount to $1.3 million today. Inflation was quite low for most of the first two decades; however, more recently, the inflation rate has picked up. In spite of the Fed's effort now to bring down the inflation rate to under 2%, we believe inflation could linger on a bit higher between 3% to 4% for some time to come. So, for a 50-year-old today, $1.3 million would be roughly the same as $2 million in the year 2038 (in terms of buying power).

Let's do some planning:

Let's work out our retirement targets in the following manner:

Your current age: Between 45 - 50 years.

Earliest Retirement: In 15 years, the year 2038.

Table-2:

| Retirement Target as of 01-JAN-2001 (Ideal target in the year 2001 used to be $1 million, but we will assume a bit conservative figure). |

| $750,000 |

| Retirement Target on 01-Jan-2023, in inflation-adjusted dollars (based on actual inflation from 2001-2022). |

| $1.28 million |

| Retirement Target on 01-Jan-2038, in inflation-adjusted dollars (assuming 3.0% average inflation for 15 years). |

| $2.0 million |

Additional considerations :

If your retirement is 15-20 years away, we can only hope that the Social Security benefits are the same as they are for the current retirees. Hope should not be the only recourse, but we should be prepared for a slightly worse scenario. It is quite likely that there would be some changes, either in the form of higher eligibility age or some reduced benefits. So, you should plan to work a bit longer or accumulate even higher savings than $2 million.

You should plan to save some extra amount for some kind of annuity that would provide benefits somewhat similar to the current Social Security and fill the gap. For example, you could plan to save enough extra amount that could provide you with $1,000 per month in today's dollars, or $1,500 in inflation-adjusted dollars (in 15 years). Though we do not like annuities as a form of investment and believe that there are better alternatives. But, just for the sake of calculation, we will see how much capital one should accumulate for an annuity that would generate $1,500 a month. From our rough estimates (based on some annuity calculators), one would need an initial annuity capital of roughly $400,000 to generate $1,500 with a 3% annual adjustment for 30 years.

This means that your retirement goal in the year 2038 would be $2.4 million that could afford the same living standards as was afforded by $750,000 in the year 2001.

Now, with the above estimates, and assuming your current annual income of $140,000, the below table will show how much you should save on a monthly basis.

Assumptions made:

- Annual income $140,000

- To save at least 16% of gross income in pre-tax savings. These savings should go to tax-deferred plans like 401Ks. Additional savings will be contributed by the employers' match (assuming 80% on the first 6%).

- Additional savings of $5,000 in individual retirement savings accounts (IRAs or Roth IRAs).

- Current initial savings of $200,000.

- The average long-term growth rate of 9% in a realistic scenario. However, we will also calculate results based on a more conservative 7% growth rate.

Note: The discussion about the pros and cons of using traditional IRAs vs. ROTH IRAs is rather a complex topic and is outside the scope of the current discussion.

We will present two tables below to demonstrate that even with a modest growth rate of 7%, retirement goals can be within reach as long as someone is committed to savings and investing. However, we believe, with some prudent planning, a 9% to 10% total average return is quite realistic and achievable.

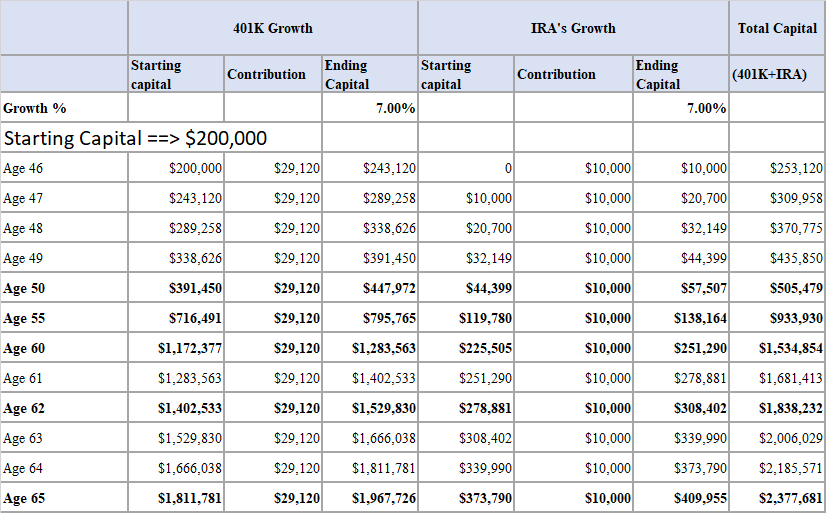

Table-3:

{kind=link}

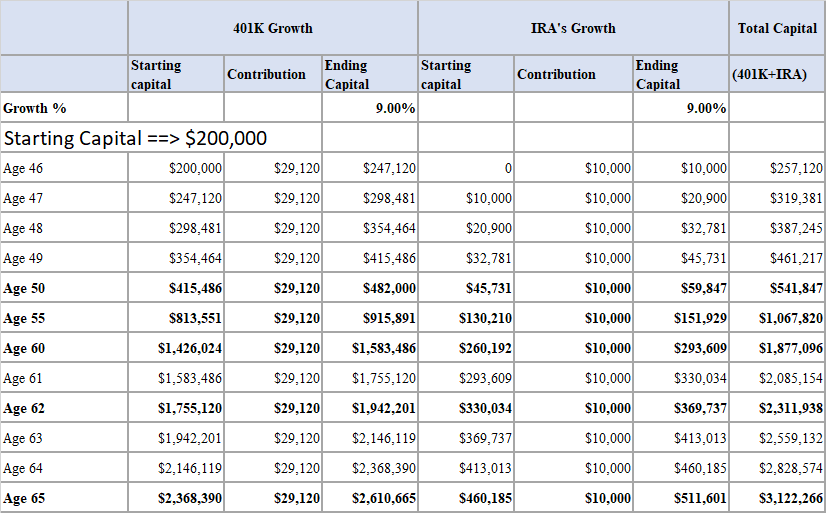

Now let's be more optimistic and recalculate the above table with the average annual growth rate of 9%.

Table-3B:

{kind=link}

Retirement Planning Part-II: Investing Successfully

There are two most critical concepts to retirement planning:

- Save early and save enough

- Invest wisely and relatively safely.

As we have talked about earlier, saving at least 20% of your income on a regular basis is the key to a wealthy retirement. The saving of 20% can be in any form, but it helps in two ways. First, it adds a substantial amount to your investment capital every month that can grow over time. Secondly, saving 20% of your income inculcates a habit of spending less than your income. In fact, once you have saved 20%, the rest can be spent guilt-free. We cannot emphasize enough to the younger folks how important it is to get into a habit of paying yourself first.

The second part of achieving a wealthy retirement is to invest your savings wisely and meaningfully. It is best to make a plan in writing rather than adopting a haphazard or spontaneous approach. Making good and sound investments and leaving them alone to compound for a long-time can do wonders for the growth of your capital.

Strategy-1 for 401K Accounts

In the first option, we assume that your 401K accounts do not permit buying individual securities. But they allow certain mutual funds and ETFs (exchange-traded funds).

Note: Most 401(k) accounts do not permit trading in individual stocks, but some 401K managers do. Some brokerage houses (managing 40K accounts) do allow a certain percentage of the account in individual stocks/securities.

If your 401K sponsor does not allow individual stocks, you are restricted to a select list of funds (usually mutual funds). In such a scenario, we would suggest the following combination of funds for wide diversification and long-term growth. We can hope to get a minimum growth of about 8%-9% annualized on a long-term basis.

- 25% in the S&P 500 fund

- 25% in the Total Stock Market fund or the Equal-weighted S&P 500 fund

- 15% in high-growth Technology funds

- 15% in the Developed International fund

- 10% in Emerging Markets fund

- 10% in Bonds and Treasury funds.

Strategy-2 with the 2-Basket approach:

Though there are many ways to achieve the same goals , we recommend the following multi-basket strategy.

In this option, we are assuming here that you have the option of investing in individual stocks or at least in ETFs (Exchange Traded Funds). We recommend deploying a two-basket strategy.

Basket-1: Risk-hedged rotation strategy (suited for 401(k) accounts)

Since this strategy is being implemented inside 401(k) accounts, it needs to be simple and easy to implement. Most 401(k) accounts offer a limited number of funds that one can choose from. This strategy rotates on a monthly basis.

The strategy will involve four securities (or equivalent funds), which are:

- Vanguard 500 Index Fund Investor ( VFINX ) or SPY

- Vanguard Total International Stock Index Fund Inv ( VGTSX )

- Vanguard Long-Term Treasury Fund ( VUSTX ) or ( TLT )

- Vanguard Short-Term Treasury ETF ( VGSH ) or iShares 1-3 Year (Short-term) Treasury Bond ETF ( SHY ).

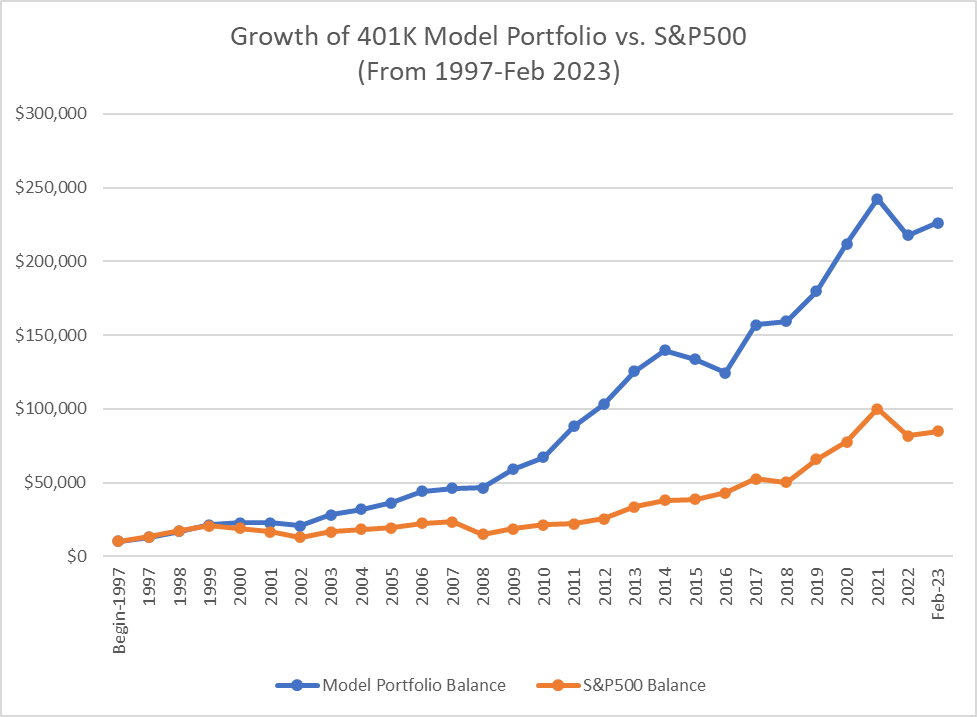

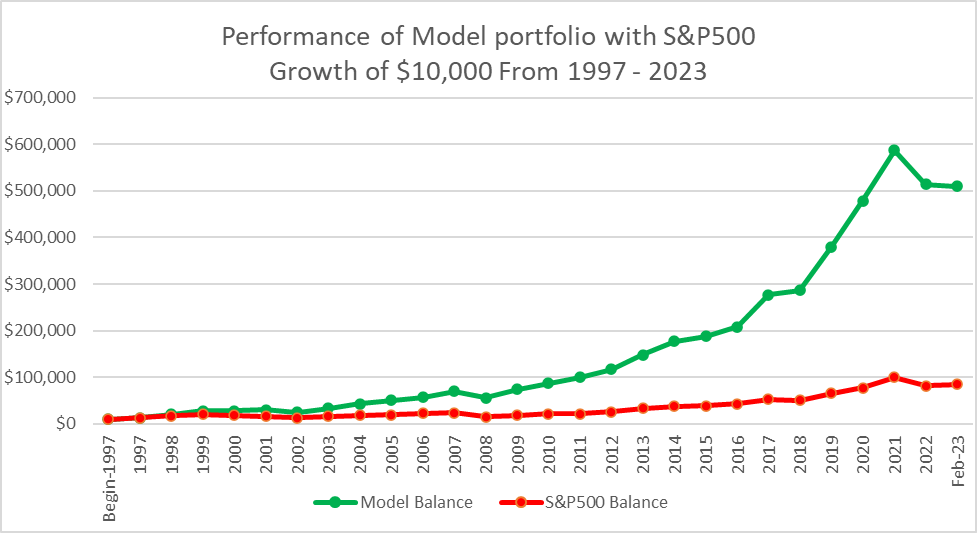

Out of these four securities, two of them (TLT and SHY) are the hedging assets and will come into play only when the other two main assets are not doing well, or there is some kind of correction or panic situation. For someone who would have used this strategy since 1997, it could have produced a very significant alpha over the S&P500. The strategy has generated a CAGR (Cumulative Annual Growth Rate) of over 13% compared to 8.5% from Jan. 1997 to Feb. 2023. A difference of nearly 4.5% percentage points is huge over a 25-year period. This is not all. The biggest benefit was the much lower drawdowns during the corrections and bear markets of 2000-2002, 2008-2009, and 2020.

Note: We have used the short-term Treasury fund SHY instead of VGSH, which are similar securities. Also, in the back-testing model, we did not use SHY prior to Jan. 2003 since it did not have a history prior to 2002.

Equivalent or similar ETFs that can be used for the above mutual funds:

Table-4:

The methodology: The strategy is pretty simple. On the last trading day of every month, we will calculate the performance (total return, including the dividends) of each of the four securities over a period of three months and select the top one. We will invest in the selected security for the next month. The process will be repeated every month.

Chart-1:

{kind=link}

Basket 2: DGI (Dividend Growth) Portfolio

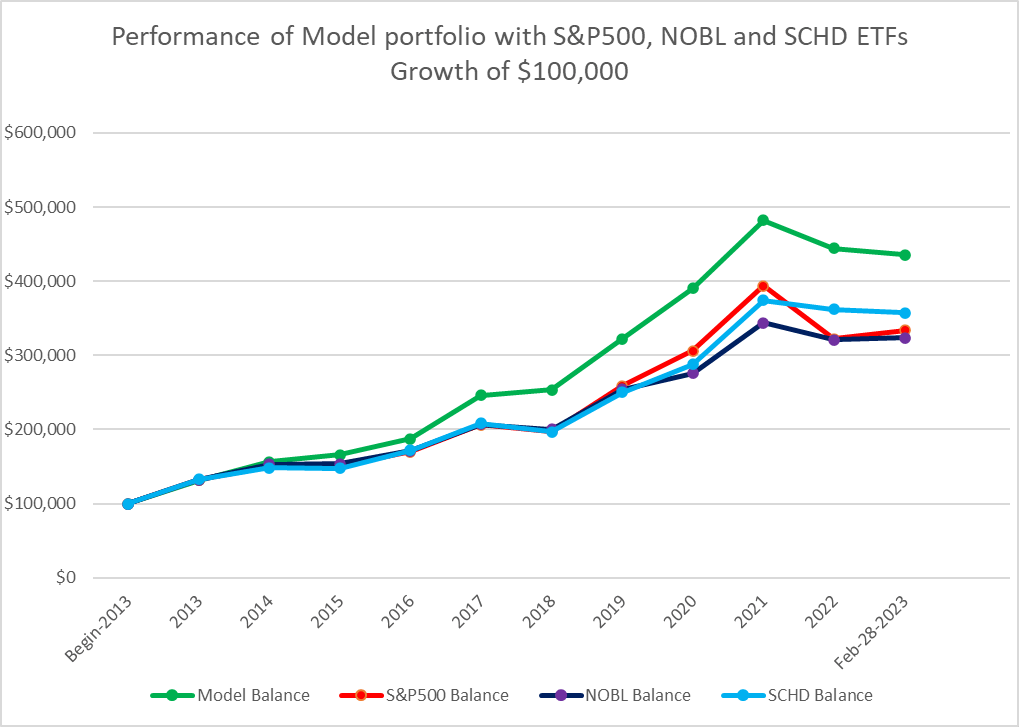

A simple DGI portfolio can be constructed by using some of the dividend ETFs. Some examples are Schwab U.S. Dividend Equity ETF (SCHD), ProShares Dividend Aristocrats ETF (NOBL), Vanguard High Dividend Yield ETF (VYM), and Vanguard Dividend Appreciation ETF (VIG). You can just select a couple of them for more than enough diversification. Please note that some of them may be concentrated in growth stocks (for example, VIG), while others may be in value stocks (for example, VYM). For most folks, this can produce reasonably good results over the long term. However, the dividend yield may be a bit on the lower side. However, if you are an active investor and like to own and pick individual stocks, there can be many advantages. First, you will save on the ongoing fees; however low they may be. Secondly, by selecting only the good stocks and buying them at reasonable (or cheaper) valuations, you can create some additional alpha leading to higher returns. So, let's compare a sample portfolio of 15 DGI stocks with the S&P500 and two of the best dividend ETFs, namely SCHD and NOBL.

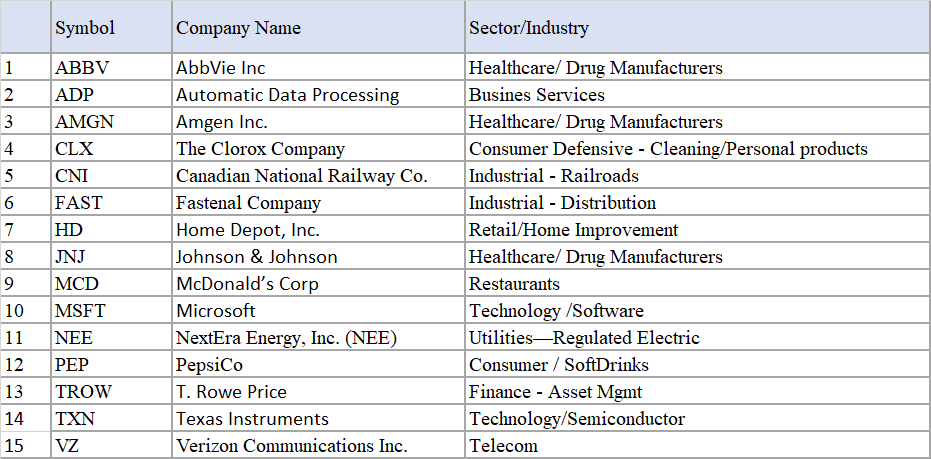

Stocks in the Model Portfolio:

AbbVie ( ABBV ), Automatic Data Processing (ADP), Amgen ( AMGN ), Clorox ( CLX ), Canadian National Railway ( CNI ), Fastenal ( FAST ), Home Depot ( HD ), Johnson & Johnson ( JNJ ), McDonald's ( MCD ), Microsoft ( MSFT ), NextEra Energy ( NEE ), PepsiCo ( PEP ), T. Rowe Price ( TROW ), Texas Instruments ( TXN ), and Verizon ( VZ ).

Table-5:

{kind=link}

Chart 2: Performance Comparison with S&P 500 and Dividend ETFs, NOBL and SCHD:

{kind=link}

Chart 2B: Long-term growth of Model Portfolio and S&P500 (from 1997 to Feb-2023)

{kind=link}

(Note: The stock ABBV was replaced by ABT prior to year 2013).

Conclusion

There are three factors that can lead to success in retirement planning and achieving retirement goals. Importantly, we control the first two factors directly.

- The amount and the rate of regular savings,

- The time for those savings to grow and compound,

- The market conditions and the investment returns.

While we do not have control over the market and economic conditions, we can have an investment plan that can withstand the ups and downs of the market. This can also help us prevent us from making wrong decisions due to fear or greed.

We believe there are many paths that can lead to financial success in retirement. The stock market has broadly provided an average of 9% to 10% annual growth over the last five decades. Sure, that growth has involved so many ups and downs, various crises and recessions, and deep corrections and drawdowns. In the above article, we have outlined an investment thesis that can provide the same (or better) long-term growth while limiting the downsides and drawdowns. We may like to add that the past performance cannot guarantee similar returns in the future but still provides a track record of outperformance.

For further details see:

Why You Should Aim For $2 Million For Retirement