LVMUY - Why You Should Aim For $2 Million For Retirement

2023-11-11 09:00:00 ET

Summary

- Retirement goals should be set based on individual situations and factors like your pre-retirement earnings, place of retirement, and spending needs.

- $1 million used to be a good goalpost for retirement savings. However, $1 Million is not the same as it was two decades ago.

- We believe folks in their 40s and early 50s would need between $1.5 to $2 million to retire comfortably. We also discuss a few strategies to achieve the same.

By most estimates, a vast majority of Americans are ill-prepared for retirement. The median retirement savings of American households in 2022 was $87,000. According to the data from the Federal Reserve, in the year 2022, the median savings for folks in the age group of 45-54 years was $115,000, while the same for the age group of 55-64 years was $185,000. However, the mean savings are much higher due to some high earners and high net-worth individuals. Needless to say, the figures are not encouraging.

So, the question is how much should you target for a reasonably comfortable retirement. There is no single answer for this because it depends on several factors, including your place of retirement, your earnings (and expenses) at retirement, your eligibility for Social Security and Medicare at the time of retirement, and any debt that you may be carrying into retirement. There may be several other factors in play based on individual situations.

The Negative Impacts of Inflation

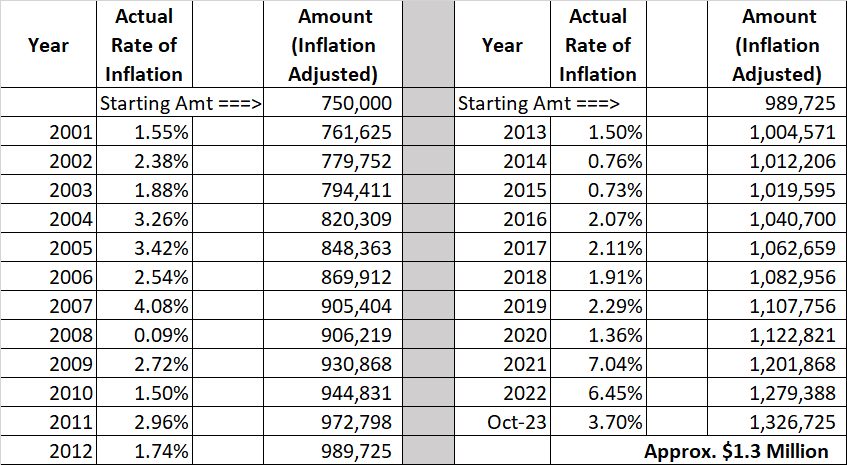

Back in the early 2000s, the retirement goalpost for a couple used to be $1 million for a very comfortable retirement. However, that has been steadily increasing due to inflation. We have had almost two decades of low inflation since 2000, but that has changed since the pandemic in 2020. Let's see the impact of inflation starting from the year 2001 until Oct. 2023. Also, we think a target of $1 million in the year 2000 was a little over the top for a vast majority of people, so we will tone it down to $750,000.

Table 1: Inflation Impact

{kind=link}

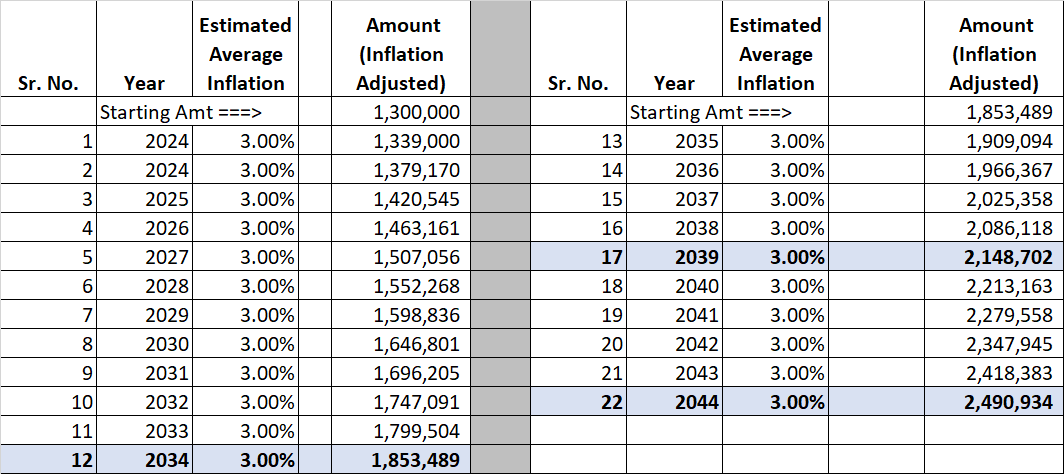

As you can see from the above table, due to inflation, the buying power of $1.3 million today is the same as $750,000 in the year 2001. This is based on the actual official rate of inflation during the last 23 years. Now, let's calculate the retirement target amount for today's 40-year, 45-year, and 50-year-olds, assuming they retire at the age of 62. We will assume an average rate of inflation at a constant 3% (some years it will be more, but some other years it may be less).

Table 2:

{kind=link}

We have provided emphasis (color-coded) on lines nos. 12, 17 and 22. These are the years when today's 50-year, 45-year, and 40-year-olds will get to age 62, respectively. So, as we can see, depending on their current age group, these folks would need anything between 1.8 million to $2.5 million when they reach the age of 62, assuming they wish to retire at 62.

- Today's 50-year-olds should require $1.85 million at age 62.

- Today's 45-year-olds should require $2.15 million at age 62.

- Today's 40-year-olds should require $2.5 million at age 62.

In summary, we can say that most folks above 40 years (but less than 55) of age today should target at least $2.0 million.

How To Get To $2.0 Million In 15 Years

Obviously, there are many ways to reach the same goals. However, there are certain prerequisites to reach an ambitious target. First, you have to give the retirement savings a top priority. Second, depending on how much you have already saved, you need to save a minimum of 15% to 20% of your gross income on auto-pilot. Last but not least, you need to invest in stocks of large, relatively safe, and growing companies. Depending upon the life stage, at least half of the companies should be dividend-paying.

Let's assume that our investor couple is in the age group of 45-50 years and starts with an initial capital of $250,000. Going forward, they will save 16% of their annual gross income of $140,000. We will also assume that their employer matches 70% of the first 6% of the contributions.

We will discuss two strategies our hypothetical investor could invest in over the next 15 years.

Strategy 1: High Growth Strategy

Allocation: 30% to 50%, depending upon the life stage.

Since our investor still has 15 years (or more) before they plan to retire, they should devote a portion of their portfolio in high-growth stocks so their capital can grow at a rapid pace. Earning dividends may not be a top priority during the first half of 15 years.

One strategy that we can recommend is to utilize a stock screener and select stocks based on the following criteria. We recommend that this process is repeated at least on an annual basis (or bi-annually) and see if any of the existing stocks need to be replaced with new ones.

List of Criteria:

- Market capitalization is at least a billion dollars. But the majority of stocks should be selected above $5 Billion.

- Forward EPS (estimated for the next 3-5 years) is > 10%

- EPS Growth (3-Year History) >=7%

- Revenue Growth (3 Yrs) >=12%

- Revenue Growth (TTM vs. Prior TTM) >=9%

- Price Performance (52 Weeks)>=15%

- Operating Margin ((TTM))

- Operating Margin (5 Year Avg)

- P/E (Price/TTM Earnings)

Some of the above criteria (last three) are applied just to display the data, but there are no minimums set in the filter. After applying these criteria, we get 36 names. We apply some weights to each of the above factors and sort the list on total weight. As expected, we get a lot of names from the Computer, Software, and Semiconductor industry segments. But we will try to select stocks from many sectors and segments.

( ANET ), ( NVDA ), ( VRTX ), ( AXON ), ( ADBE ), ( V ), ( SNPS ), ( LVMUY ), ( VEEV ), ( OKTA ).

Table 3: High Growth Stocks (Selected from Screener process)

{kind=link}

Strategy 2: DGI (Dividend-Growth Investing) portfolio

Allocation: 30% to 50%, depending upon the life stage.

So, why a DGI portfolio? It is a well-established fact that in the past four decades, over 70% of the market returns have come from dividends. So, if you are a long-term investor, you should not ignore the power of dividends. There are many ways that you can construct a DGI portfolio. It can be constituted from individual stocks, ETFs (Exchange Traded Funds), or a combination of both. If you are a passive investor, you can constitute solely from ETFs.

Some examples of decent dividend ETFs are:

- Schwab U.S. Dividend Equity ETF ( SCHD )

- ProShares Dividend Aristocrats ETF ( NOBL )

- Vanguard High Dividend Yield ETF ( VYM ),

- Vanguard Dividend Appreciation ETF ( VIG ),

- iShares Core Dividend Growth ETF ( DGRO ).

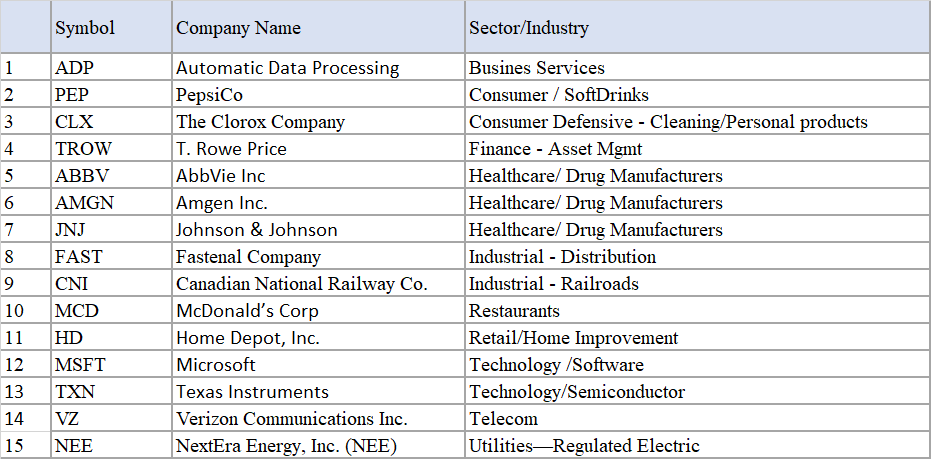

Now, for those who like to own individual stocks and also have the ability to trade individual stocks inside their retirement accounts, we will present a list of 15 stocks that will form a reasonably conservative but dividend-growth portfolio.

Stocks in the Model Portfolio (sorted on sector):

Automatic Data Processing ( ADP ), PepsiCo ( PEP ), Clorox ( CLX ), T. Rowe Price ( TROW ), AbbVie ( ABBV ), Amgen ( AMGN ), Johnson & Johnson ( JNJ ), Fastenal ( FAST ), Canadian National Railway ( CNI ), McDonald's ( MCD ), Home Depot ( HD ), Microsoft ( MSFT ), Texas Instruments ( TXN ), Verizon ( VZ ), and NextEra Energy ( NEE ).

Table 4:

{kind=link}

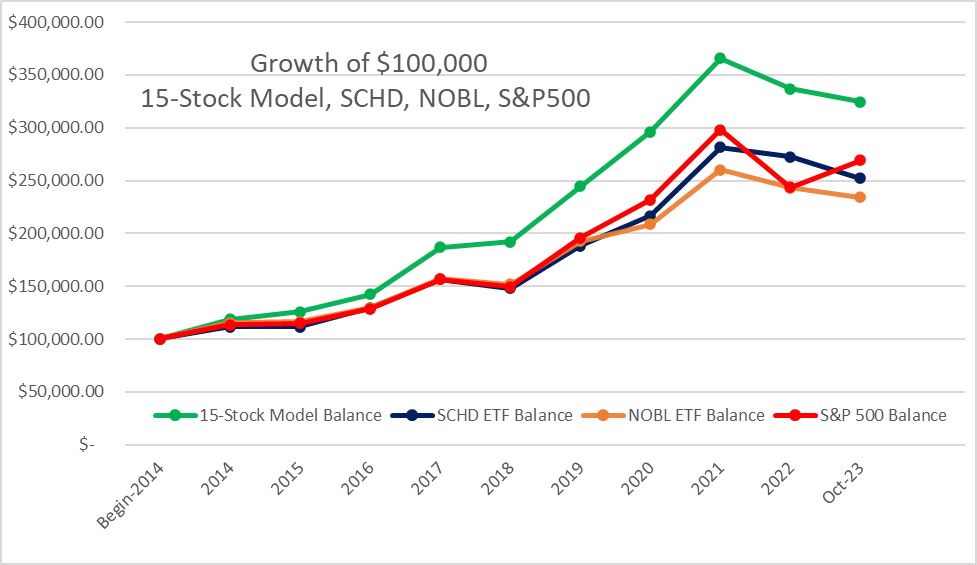

Even though, for most folks, dividend ETFs can do a good job of compounding capital as long as they are buying both in down markets and up markets. However, a portfolio of carefully selected individual stocks can beat the market as well as the best dividend ETFs. Here is some back-testing of a portfolio of above 15 stocks in comparison with the S&P500 and two dividend ETFs, namely, SCHD and NOBL.

Chart 1:

{kind=link}

Growth of Capital in the Next 15 Years:

Now, with their money invested in the above strategies, we will assume that our investors are able to get an average annual growth rate of 10% over the next 15 years. Sure, it will not be a constant 10% every year; it will be up and down from year to year. But we are talking about the average annualized growth rate. We will also consider lower returns (from 7% to 9%) in the next table.

Let's see, with $250K in starting capital, a 10% annualized growth rate, and 16% (of gross income) contributions to their retirement funds, how much will they have at the end of 15 years? Our calculations also assume that our investor's gross annual salary increases at a 2.0% rate annually.

Table 5:

Author

We can see that with a 10% average annualized growth, we can comfortably meet our goal of $2 million in 15 years. With the strategies discussed above, it seems reasonable to expect 10% annualized growth. Sure, as stated earlier, some years it will be less, but other years it will be much higher. But it is also reasonable to doubt and feel that 10% may be too high to achieve. So, let's see what happens with a lower growth rate of 9%, 8%, or even 7%.

Table 6:

| Annualized Growth Rate |

| Ending Capital in 15 Years. |

| 10% |

| $2.05 Million |

| 9% |

| $1.84 Million |

| 8% |

| $1.65 Million |

| 7% |

| $1.50 Million |

Now, if somehow markets do not perform as well in the next 15 years, and we get a growth rate that is less than 10%, we are going to have some shortfall in our targets. There are a few ways to deal with such a situation.

- Contribute more (than 16%) in the year when markets are in a downturn, and your expected growth rate is likely to be low. This will do two good things. First, you will be buying more shares at lower prices. Second, higher contributions tend to compensate for lower returns in a down year. However, do not get tempted to decrease your contributions when the markets are doing good.

- You may like to think of ways to reduce your discretionary spending. This will not only help increase your savings rate but also have an impact on your budget when it is time to retire.

Concluding Thoughts:

It is obvious that due to consistent inflation, cash loses its value day in and day out. More recently, the rate of inflation has been highly pronounced, which has a devastating impact on everyone's savings. We agree everyone should have some amount of cash (usually six months of living expenses) to be able to deal with life situations. But beyond that, most of the money should be invested in long-term investments. Once you are in your 40s or 50s, there is nothing more important (financially) than to have a retirement savings plan. There are usually three factors that are going to decide how successful you are going to be in meeting your retirement goals. Fortunately, you control two of them directly. There is only one factor that you do not have control over. These three factors are:

- Start saving early and invest in long-term investments. This determines how many years your money will have to grow and compound.

- How much you save each year. This will determine directly how big the retirement capital you are likely to have. We recommend saving a minimum of 15% to 20% of your gross income.

- Future market and economic conditions. As someone famous said, "It is hard to predict, especially about the future." But we can change our strategies to deal with both up and down markets.

In the article above, we have attempted to provide a basic blueprint on how to set your goals and adopt strategies to reach those goals.

For further details see:

Why You Should Aim For $2 Million For Retirement