VGSH - Why You Should Aim For $3 Million For Retirement (Gen X'ers And Millennials)

2023-07-15 09:31:00 ET

Summary

- We discuss how millennials and GenX'ers in their late 30s or early 40s should aim and accumulate a relatively large sum that should afford them a comfortable retirement.

- Saving early and regularly, investing wisely, budgeting expenses, and keeping them less than your income are keys to a wealthy retirement.

- We will discuss multiple investment strategies for retirement accounts like 401K accounts as well as IRAs (Individual Retirement Accounts).

- We also discuss how regular savings on a monthly basis and deploying some smart investment strategies can lead to large capital over the next 20 years.

Retirement is the farthest thing that most young folks think about. After all, there are plenty of distractions, and life's priorities are entirely different. But it's easiest for young folks to accumulate wealth over time if they start early. They have something wonderful on their side, that is time that can help compound their savings. After all, Albert Einstein termed compounding the eighth wonder of the world for no small reason. They can compound their savings and investments into sizable wealth as long as they invest with some discipline. As you get older and keep delaying retirement savings, meeting retirement targets gets tougher and tougher.

This article's focus is on folks between the age group 35 to 50 years, which would include Gen X'ers and Millennials, though not all of them. That said, the principles and methodology described here would apply to anyone in any age group.

When to retire?

So, how much is good enough to retire?

This is more of a subjective question. However, we can generalize at some level. Mostly, it will depend upon your basic living expenses. Your living expenses could vary based on several factors, including your pre-retirement income, the place where you choose to retire, your hobbies, and the kind of lifestyle you want in retirement. There are many ways to determine your expenses in retirement. One common method is to calculate a specific percentage of your pre-retirement income. Another method would be to subtract from your pre-retirement income expenses that you would not need to incur in retirement. For example, you would not need to contribute to your 401k account, not there would be any social-security taxes to be paid. You also would be spending less on transportation and any other upkeep related to work.

Why saving early and saving enough is critical

We have stated before, and we will stress this again, that the earlier you start saving and investing, the better it is. It will have more time to compound, and the net impact can be dramatic. A dollar saved today and invested can be worth much more than a dollar saved five years later. We will explain this by way of an example below. Two friends, Mark and Joe, start working at the same age, but one of them starts saving at the age of 30 while the other one starts at 40. Even though they save the same amount (after age 40), Mark accumulates almost double the amount that Joe would accumulate. This is because of the fact that Mark's savings for the extra ten years got plenty of extra time to compound.

The table below presents the savings by the age of 62 with an assumed annualized rate of return of 8%.

Table-1:

Author

You are 40. Do you have an investment plan?

Let's assume you are already 40-years-old. It's probably high time that you should have some kind of savings and investment plan. We have stated before and want to emphasize again the importance of time that you have to grow and compound your savings. There are some other factors that you must keep in mind:

- You will need to take into account the impact of inflation on your savings. It's difficult to predict the rate of inflation in the next 20 years, even though historically, in the last 30 years, we had a low inflation rate of 2% to 3%. However, recently in the last couple of years, inflation spiked to much higher levels. For the planning purpose, it may still be prudent to account for a 3% average inflation.

- The second factor that younger folks need to consider is the sustainability of Social Security benefits in the future. Anyone who is already 55 years or more probably need not worry about it as they would be protected from any future cuts or changes in the law. We know that the Social Security trust is likely to run out of money in about 10 years and will either have to cut benefits or will need some changes from Congress. Since the matter is highly sensitive politically, lawmakers will probably keep pushing it down the road as much as possible, but at some point, it will need to be dealt with. The most likely scenario would be a combination of delayed eligibility, some cuts for future retirees, and some form of tax increases. So, anyone who is only 40 years today should only account for 50% to 60% of benefits (compared to current levels), though these calculations can change over time.

Retirement Targets:

We will make certain assumptions to calculate our retirement targets:

- Let's assume you need $1 million today to retire reasonably well, along with the Social Security benefits. Though this is highly debatable and subjective, as some folks will need more, and some others may need less. But for the sake of our example, it should work as it is somewhere in the middle.

- Now, we should account for inflation over the next 25 years, and a rate of 3% annual inflation should be a reasonable assumption. Some years it will be more, but some others, it may be less. $1 million in today's dollars would be equivalent to $2.1 million 25 years later.

- For our calculations, for a 40-year-old, we will assume that Social Security benefits would reduce by 40 from current levels. So, our investors should plan for the gap by means of additional savings. For rough calculations, we estimate that we would need another $500,000 to fill this gap in Social Security benefits. The way we calculate is that if we were to put $500,000 (future dollars) in an annuity, it would generate roughly $2,500 per month with a 3% annual increase (or $1,200 in today's dollars). This should be sufficient to fill the gap in Social Security benefits.

- From the above calculations, we can see that we will need roughly $2.6 million ($2.1m + $0.5m) to retire comfortably in 25 years. Sure, these are rough calculations based on certain assumptions, and they are as good as assumptions. If you do not agree with our assumptions, you should modify these figures.

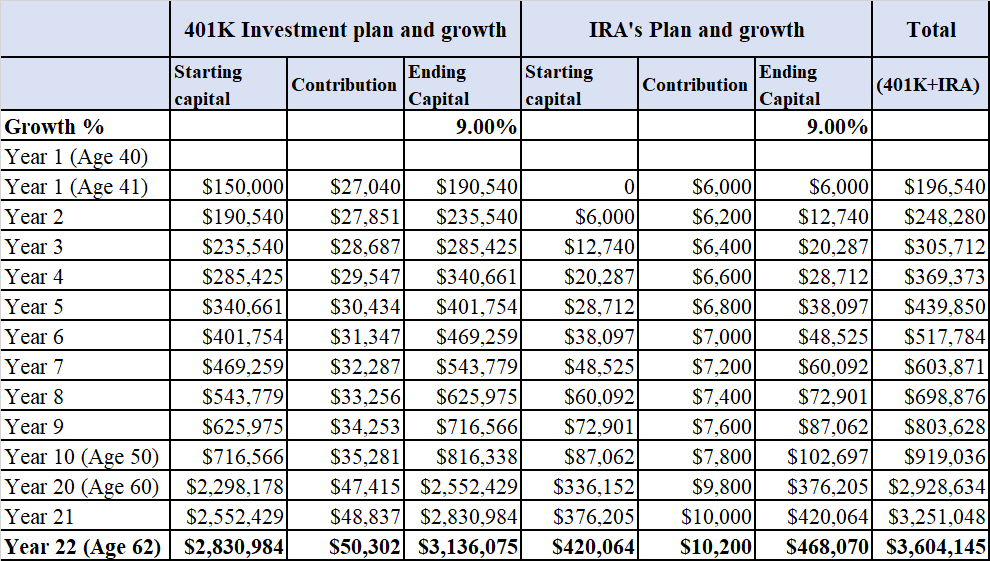

We will now calculate how you would need to save on a monthly basis to reach the above target in 20 years. We will show two examples, the first with a 9% annual growth rate and the second one with a more conservative estimate of a 7% annual growth rate.

Other assumptions made:

- For our example, let's assume our investor makes $130,000 annually (as family income).

- We also will assume that you have already saved roughly $150,000, and this would be your starting capital at age 40.

- Our investor commits to saving at least 16% of their annual income by way of contributions to 401K accounts.

- They will put another $6,000 into IRA accounts, also resulting in some tax savings. This amount will be increased by $200 every subsequent year.

Table-2:

{kind=link}

Author

Now the next table will show similar calculations with a very conservative growth rate of 7% annually.

Table-3:

{kind=link}

Author

You can see from the above tables that, even with a very conservative 7% average annual growth (assuming 3% inflation), you will meet your target retirement goals with relative ease. But saving and investing consistently with discipline and commitment is a must.

Investing For Success: Retirement Planning Part-II

Now, we will put ideas into an actionable plan that's actually workable and practical.

We believe there are multiple paths to achieve anything. However, we would try to follow a path that's easy to navigate, cause the least stress, and has a high probability of achieving our goals. We recommend the following multi-basket strategy:

Summary of investments:

Table-4:

| Type of funds |

| Strategy |

| Type of Strategy |

| 401(k) accounts |

| Strategy-1 |

| ETFs or Mutual funds from the available pool as per the allocation (if individual stocks and securities are not permissible). |

| 401(k) accounts |

| Strategy-2 |

| Rotation strategy suited for 401(k) using equivalent funds like S&P500, International fund, and Treasury or Bond fund. |

| 401(k) accounts |

| Strategy-2B |

| Rotation strategy (if individual securities trading allowed). This can be in addition to Strategy-2. |

| IRA funds |

| Strategy-3 |

| DGI portfolio of 20 stocks. |

Investment Portfolios

Strategy 1: 401K Funds strategies:

This can vary from person to person. If you work for a large corporation, you probably have many options inside your 401k account as they may be managed by well-known brokerage firms. Most of the time they also would include a brokerage account where you can also trade individual stocks. However, that may not be true for small companies, which normally offer only a select set of mutual funds. Even then, it would include many types of funds like S&P 500 funds, large-cap, mid-cap, and small-cap funds, as well as a couple of bond funds. They should generally include one or two international funds as well. Also popular are the age-targeted funds that change the investment mix as you grow older and get closer to retirement.

You should compare the fee structure of each available fund before determining the best set of funds for you.

Generally, you could choose the following types of funds if you only have mutual funds available.

- S&P 500 fund (or Large-cap fund) 25% allocation

- Mid-cap and small-cap fund 20% allocation

- International (developed markets) 15% allocation

- International (developing countries) 5% allocation

- Real estate fund (if available) 10% allocation

- Bond funds 15% allocation

- Treasuries or money market funds 10% allocation

Strategy-2A: Risk-hedged rotation strategy for low drawdowns (for 401K accounts)

If your 401K does not allow individual stocks or ETFs, it means you can only use mutual funds. So, in that case, our strategy needs to be simple and easy to implement.

One of the strategies we usually recommend for 401k accounts is as follows. At every month's end, we will compare the performance of four securities over the last three months and select only the best-performing security for investment for the following month. The strategy rotates on a monthly basis. We select the following four securities because they're the most common types of funds, and they should be available in some form or the other.

- A fund equivalent to S&P500, i.e., Vanguard 500 Index Fund Investor ( VFINX ).

- A fund representing the international (developed) markets, i.e., Vanguard Total International Stock Index Fund Inv ( VGTSX ).

- A fund that represents Long-term (20 years) Treasuries, for example, Vanguard Long-Term Treasury Fund ( VUSTX ).

- A fund that represents short-term (1 to 3 years) Treasuries, for example, Vanguard Short-Term Treasury ETF ( VGSH ).

VUSTX and VGSH are two of the Treasury funds, one long term and the other one short term. These two would play the role of hedging assets and limit the drawdowns during recessions or panics.

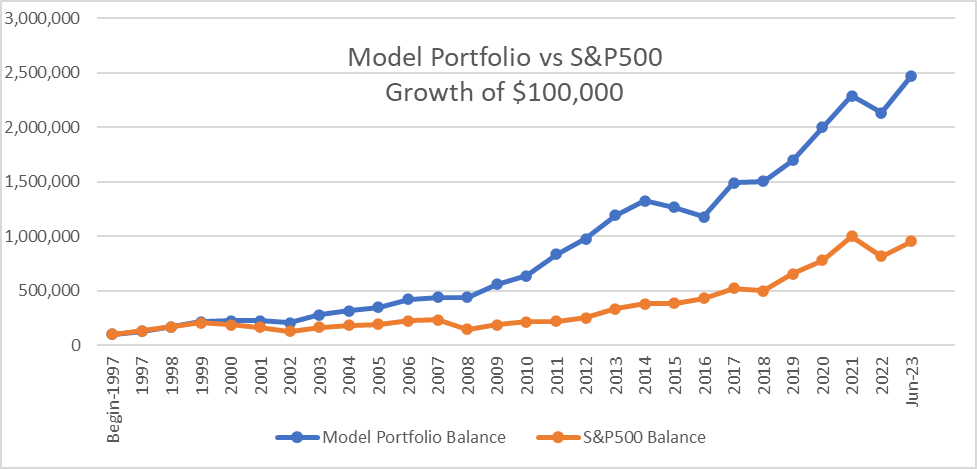

This strategy has resulted in a 13% annualized return over the last 26 years (since 1997). This compares very well with only about a 9% return from the S&P 500 during the same period. More importantly, the max drawdown for the strategy is -20%% compared to -50% for the S&P 500.

Please be aware that backtesting results cannot provide any guarantee of similar results in the future, but they do provide some historical perspective.

Note: In our backtesting, we used the short-term Treasury fund SHY in place of VGSH from 2003-2023. Prior to that period, SHY was not available.

Table-5: Equivalent or similar ETFs that can be used for the above mutual funds

Below are the backtesting results since January 1997. You can see theta model outperformed the S&P 500 by a wide margin over 26-year period with a drawdown of less than half of the S&P 500.

Chart-1:

{kind=link}

Author

Strategy-2B: Risk-hedged rotation strategy (for IRA or Brokerage accounts) for Income Investors

Most younger folks do not need income from their investment accounts, especially if they're working in steady jobs. But in some situations, you may like to have an option where your portfolio can generate and provide some sort of income. Here is one such portfolio.

Note: This strategy is not suitable for accounts where trading in individual securities is permissible. Not all 401K managers allow brokerage trading. However, almost all IRA accounts allow individual securities.

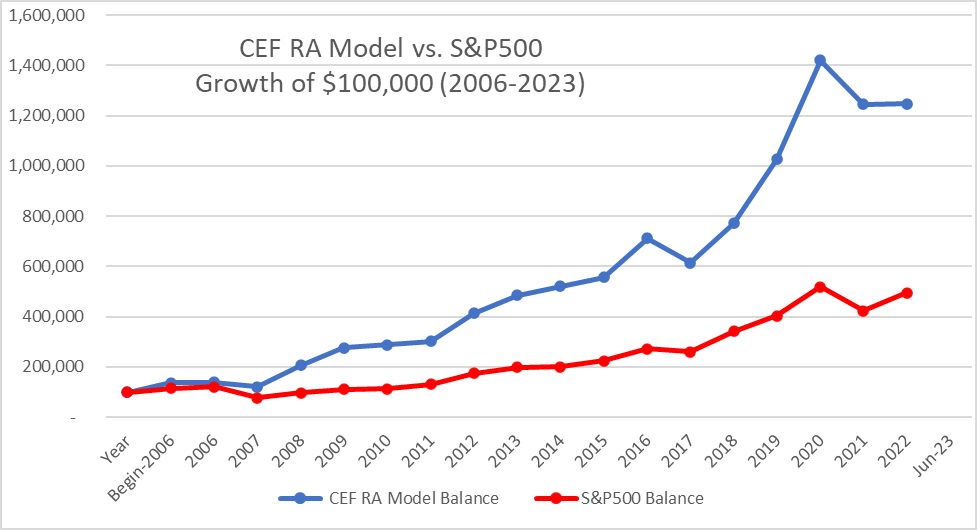

This Rotational model uses SIX closed-end funds along with a Treasury fund, though we would invest in only two of them at any point in time. At the end of each month, we will compare the total returns/performance of each of the seven securities over the previous three and seven months (average of two). We will select the top two and invest for the next month. If none of the securities had positive returns, we would stay in cash.

This model also generates roughly 6% of income due to the fact that it is invested in CEFs for the majority of the time.

The seven CEF securities and a short-term Treasury fund are:

- EV Tax-Advantaged Dividend Income ( EVT )

- Flaherty & Crumrine Preferred and Income Securities ( FFC )

- Kayne Anderson Energy Infrastructure ( KYN )

- Nuveen Muni High Inc Opp ( NMZ )

- Cohen & Steers Qty Inc Realty ( RQI )

- BlackRock Science & Technology ( BST )

- Tekla Healthcare Investors Fund ( HQH )

- iShares 1-3 Year (Short-term) Treasury ETF ( SHY )

Note: SHY is the hedging security, while we have included BST for growth.

Chart-2:

{kind=link}

Author

Note: While performing backtesting, BST was replaced with QQQ from 2006-2015 since BST did not have a history prior to 2016.

Strategy-3: DGI Portfolio for the IRAs or Brokerage Accounts

We believe everyone who is invested in stock markets should have a core DGI (Dividend Growth Investing) portfolio. A DGI portfolio could have as few as 10 stocks or as high as 25 or 30 stocks, depending upon your capital size. If carefully chosen, a DGI portfolio can add 2% to 3% of annual growth over and above the returns of the broader market. It may sound like a small number, but an annual alpha of 2% or 3% will result in thousands of additional dollars to your retirement savings. Further, a DGI portfolio usually requires the least maintenance on an ongoing basis with practically zero fees (for individual stocks).

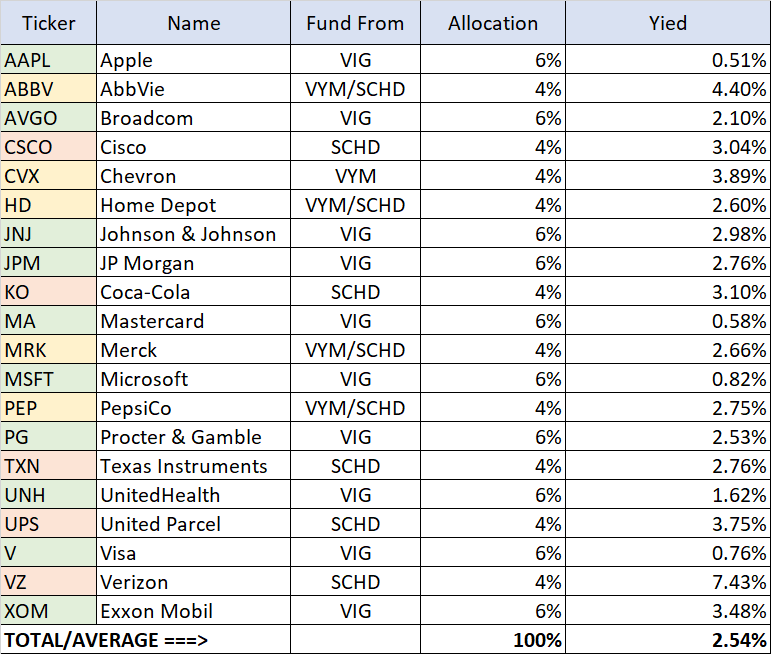

So, all that said, how do you select stocks for a DGI portfolio? Sure, there are many ways, but we will describe one simple method here. We will look at three of the most popular dividend-focused ETFs, namely, VYM, VIG, and SCHD. We know that VIG is more growth oriented than the other two. We will take the top 10 holdings of each of the three funds and remove the duplicates among them. If we do this exercise today, we get the following list.

Apple ( AAPL ), AbbVie ( ABBV ), Broadcom ( AVGO ), Cisco ( CSCO ), Chevron ( CVX ), Home Depot ( HD ), Johnson & Johnson ( JNJ ), JPMorgan ( JPM ), Coca-Cola ( KO ), Mastercard ( MA ), Merck ( MRK ), Microsoft ( MSFT ), PepsiCo ( PEP ), Procter & Gamble ( PG ), Texas Instruments ( TXN ), UnitedHealth ( UNH ), United Parcel ( UPS ), Visa ( V ), Verizon ( VZ ), and Exxon Mobil ( XOM ).

Now, since we are forming this portfolio for a typical 40-year-old, we will assign a little more weight to stocks that are part of VIG (a growth-oriented fund). So, we will assign 6% to each of the ten stocks that came from VIG list and 4% to the rest of the 10 stocks that were included in VYM or SCHD.

Table-6:

{kind=link}

Author

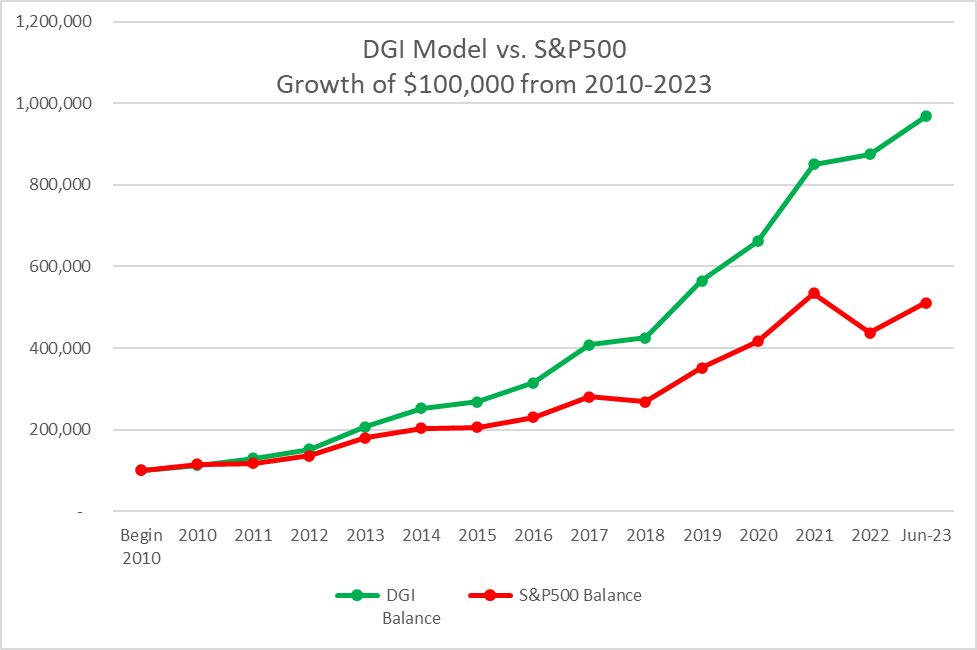

Chart-3: Growth of DGI portfolio

{kind=link}

Author

Conclusion

How wealthy you are going to be in retirement will depend on several factors, for example your current savings, rate of savings on a regular basis, time left to compound your savings (time left to retire), and the rate of growth of the capital. Most of these factors are directly controlled by the investor; however, the rate of growth depends on your investment decisions as well as on market conditions.

In this article, our focus was on investors in the age group of 35 – 50 years. However, the underlying principles and investment strategies could be used by anyone, irrespective of age. They may be the first group that is likely to see some form of changes in social security benefits and thus need to save extra to fill any such gap. Also, the low rates of inflation that we have seen in the last two decades may not repeat, and average inflation is likely to be higher in the next 20 years.

We have also presented several investment strategies, some of which are specifically suited to 401K type of accounts. We also have presented a DGI portfolio for long-term growth and two Rotational strategies that will help in lowering drawdowns and volatility.

For further details see:

Why You Should Aim For $3 Million For Retirement (Gen X'ers And Millennials)