CCI - Why You Should Look At Crown Castle Stock

2023-10-05 16:19:24 ET

Summary

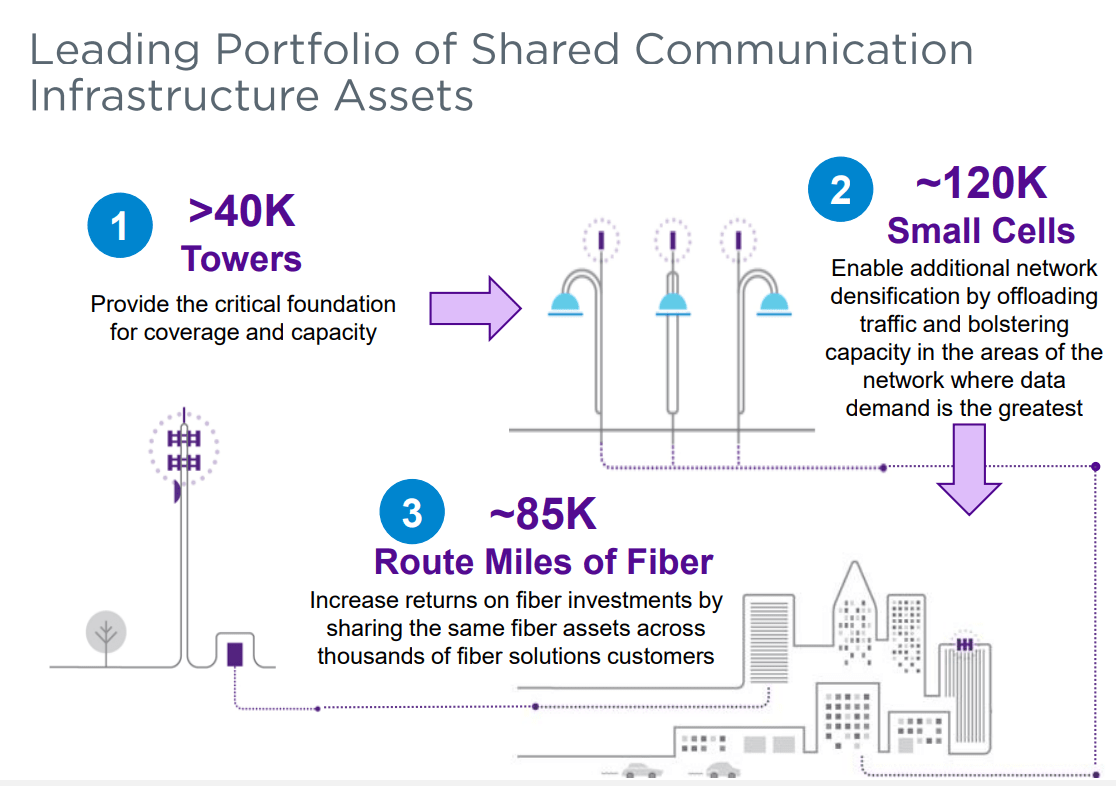

- Crown Castle is a US telecommunications infrastructure company, owning over 40,000 cell towers and 85,000 miles of fiber optic infrastructure. Its stock is down 35% YTD.

- The company reported strong Q2 FY2023 results, with increased AFFO, site billings, and adjusted EBITDA.

- Crown Castle revised downward its 2023 adjusted FFO guidance and implemented a restructuring plan to reduce costs and improve efficiency.

- The stock looks to me like an interesting oversold, undervalued, and high-yielding "Buy" with excellent development prospects.

Crown Castle ( CCI ) is a $38.4-billion market cap player in the telecommunications infrastructure industry, specializing in the ownership, operation, and leasing of a diverse range of communication assets across the United States. Their extensive portfolio comprises over 40,000 cell towers and approximately 85,000 miles of fiber optic infrastructure primarily designed to support small cells and fiber solutions. This expansive footprint ensures that Crown Castle has a substantial presence in all of the top 100 basic trading areas (BTAs) and maintains a strong foothold in major metropolitan areas nationwide.

As of Q2 FY2023 , site rental revenues accounted for 93% of their consolidated net revenues, with 63% and 37% attributed to their Towers and Fiber segments, respectively. Within the Fiber segment, 53% and 47% of revenue from fiber site rentals were generated by fiber solutions and small cells, respectively. This revenue stream is predominantly recurring in nature, driven by long-term tenant contracts.

{kind=link}

CCI's Q2 FY2023 AFFO increased by 14% YoY to $2.05 per share. Site billings also showed strong growth, rising 10% to $1.73 billion in the second quarter and 9% to $3.4 billion in 1H FY2023. Crown Castle, like other tower companies, experienced challenges due to Sprint cancellations following the T-Mobile merger but managed to achieve a net contribution of $100 million in site rental billings from Sprint in Q2, along with $57 million in prepaid rents. Adjusted EBITDA rose to $1.2 billion from $1.1 billion in Q2 FY2022. Total revenue, which includes site billings and services, increased by 7.7% from the previous year to $1.87 billion, while operating and administrative costs grew by less than 4% to $732 million.

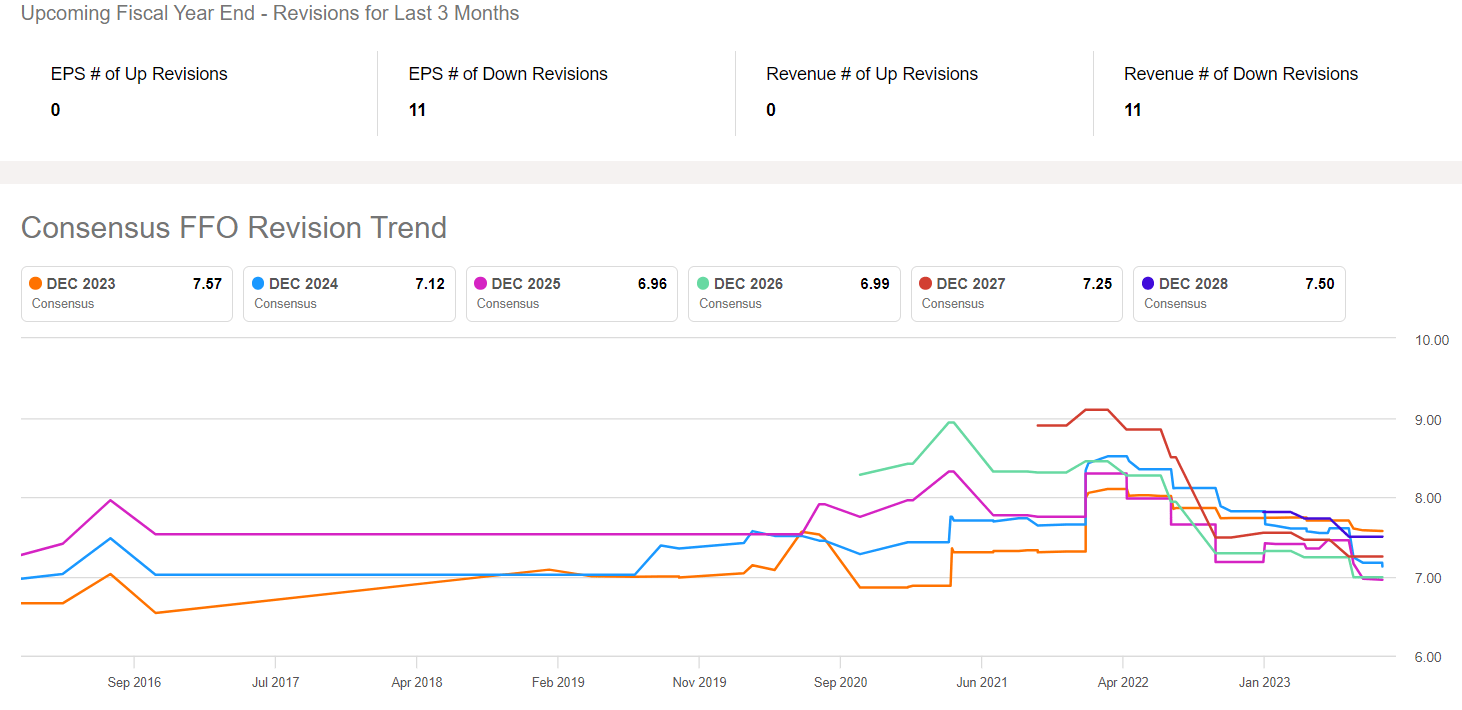

Following the second-quarter results, the company revised its 2023 adjusted FFO guidance to a range of $7.50 to $7.58 per share, down from the previous range of $7.58 to $7.68 per share. This 10-cent adjustment reflects expectations of slower tower activity in 2H FY2023. The expectations of the project site rental billings stayed in the range of $5.63 billion to $5.67 billion for the year.

A few days before lowering the guidance, CCI announced a restructuring plan to reduce costs, involving a 15% reduction in total employee headcount and discontinuation of installation services as a product offering within the Towers segment. The restructuring plan is expected to result in charges of ~$120 million, with $70 million related to employee severance and other one-time termination benefits. Additionally, office space consolidation will incur charges of ~$50 million. The reduction in headcount and the discontinuation of installation services will be completed by the end of Q3, while office space consolidation is expected to be finished by the end of Q4.

Against this backdrop, analysts hastened to lower their EPS forecasts for the coming years:

{kind=link}

A series of negative news stories drove CCI's dividend yield to unprecedented heights, while the share price continued to fall:

However, I would not rush to bury CCI's business prospects.

The ever-increasing demand for data traffic drives the industry where CCI operates. Research and Markets analysts wrote in April 2023 that the global mobile data traffic market is expected to expand significantly at a robust compound annual growth rate [CAGR] of 27.9% from 2022 to 2030. This surge in data demand is primarily due to the growing use of mobile devices and the need for more data to be transmitted. Carriers have 3 main options to meet this demand:

- utilizing existing spectrum more efficiently,

- incorporating new spectrum, and

- improving spectrum efficiency.

Based on the earnings call commentary by CCI , Crown Castle's growth hinges on the first two options, as carriers increasingly use spectrum more intensively and deploy new spectrum by adding antennas to existing assets, both of which drive growth for the company.

This approach helped Crown Castle experience robust growth in recent years, surpassing their typical target of 5-6% annual revenue growth. However, the transition to 5G has brought about a natural evolution in the generational upgrade cycle. The initial surge of 5G deployment has subsided, leading to a more stable and predictable growth trajectory. While the activity levels in their tower business for FY2023 are expected to be lower than in FY2022, Crown Castle anticipates growing at around 5% in FY2023, still within a favorable range for a business of its size, the CEO noted. This slowdown is part of the typical generational upgrade cycle, but the company remains optimistic about the industry's overall growth, driven by increasing data demand, potentially exceeding the 4G plateau.

Analysts at Argus Research recently initiated coverage on CCI with a "Buy" rating [August 2023 - proprietary source], stating that CCI's emphasis on small cells looks like a positive strategy to enhance communication in urban areas with high congestion and extend services to underserved rural regions. Argus has a price target of $140, seeing an upside potential of ~56.8% to the latest market price.

During the latest BofA Media, Communications, and Entertainment conference in mid-September , CCI's CFO Dan Schlanger stated that the firm's risk-mitigating Master Lease Agreement ((MLA)) contracts with carriers should ensure a minimum annual organic macro tower revenue growth rate of 3.75% through the year 2027. Schlanger also reiterated CCI's commitment to small cells, anticipating double-digit revenue growth in the coming year, highlighting the company's focus on diversifying its telecommunications infrastructure portfolio. By the way, BofA's analysts have a price objective of $115/sh., giving CCI stock an upside of ~28.8%.

In my subjective opinion, CCI was in a kind of perfect storm of various headwinds that led to panic selling and fears of dividend cuts. But from the information that came into my hands, CCI has no less growth drivers in the medium to long term.

On one hand, the market can be understood: CCI's leverage has risen significantly in recent quarters, increasing risk and uncertainty for the stock:

On the other hand, the firm has a Baa3 stable credit rating from Moody's and a BBB rating from Standard & Poor's with a stable outlook.

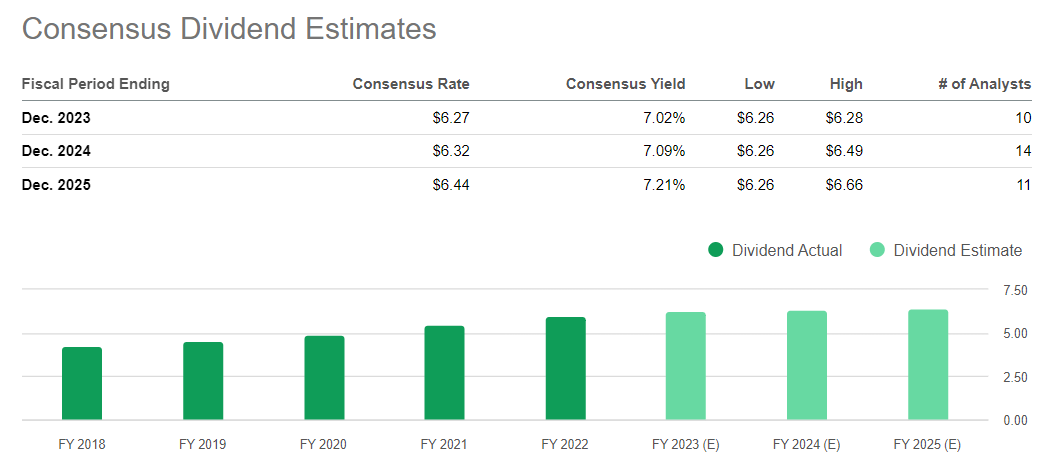

FFO per share is not the only thing affected by analysts' revisions. Forwarding CCI's dividend payout has been revised downward 5 times in the last 90 days. However, if you look at the projected yield , CCI's yield over the next 3 years is still north of 7%:

{kind=link}

What does it mean?

If you believe that the CCI has no more serious problems and the negative sentiment will soon subside, now is the right time to think about buying.

Aside from the unusually high dividend and good prospects in the industry where the company is a market leader, the stock is dirt cheap and trades at the largest discount to its historical EV/EBITDA metrics:

The skeptic in me explains this by the fact that the company’s leverage has also increased - more credit risk, less EV/EBITDA. But if we take 6 peer companies, CCI's discount to average EV/EBITDA [FWD] is about 20%, while the debt to equity ratio has no premium (it's about average):

Of course, investors in Crown Castle stock confront some risks that I should mention. As 5G availability continues to expand in the U.S., CCI may face long-term saturation concerns. Additionally, there's the risk of customer concentration, particularly with wireless network operators, which has been heightened by industry mergers like the T-Mobile/Sprint combination that could lead to tenant losses. However, CCI's focus on small cell development helps mitigate this risk. Other potential risks include government regulation, international expansion, and the impact of rising bond yields, which could exert pressure on the dividend or increase borrowing costs, potentially affecting CCI's performance, as REITs tend to correlate with interest rate movements.

But despite the whole galaxy of risks, to which can be added the risk of continued panic selling without a proper explanation from the fundamental part of the business, CCI stock looks to me like an interesting, high-yielding "Buy" with excellent development prospects. Given the current discount to its valuation, as well as the excessively high dividend yield [in a historical context], I think CCI should trade 20-30% above current levels.

Thanks for reading!

For further details see:

Why You Should Look At Crown Castle Stock