VRAI - Wild Quarter Ends With Optimism

2023-04-02 09:00:00 ET

Summary

- U.S. equity markets concluded a wild first-quarter with their best week of 2023 as easing contagion concerns and further evidence of cooling price pressures lifted markets to a third-straight weekly gain.

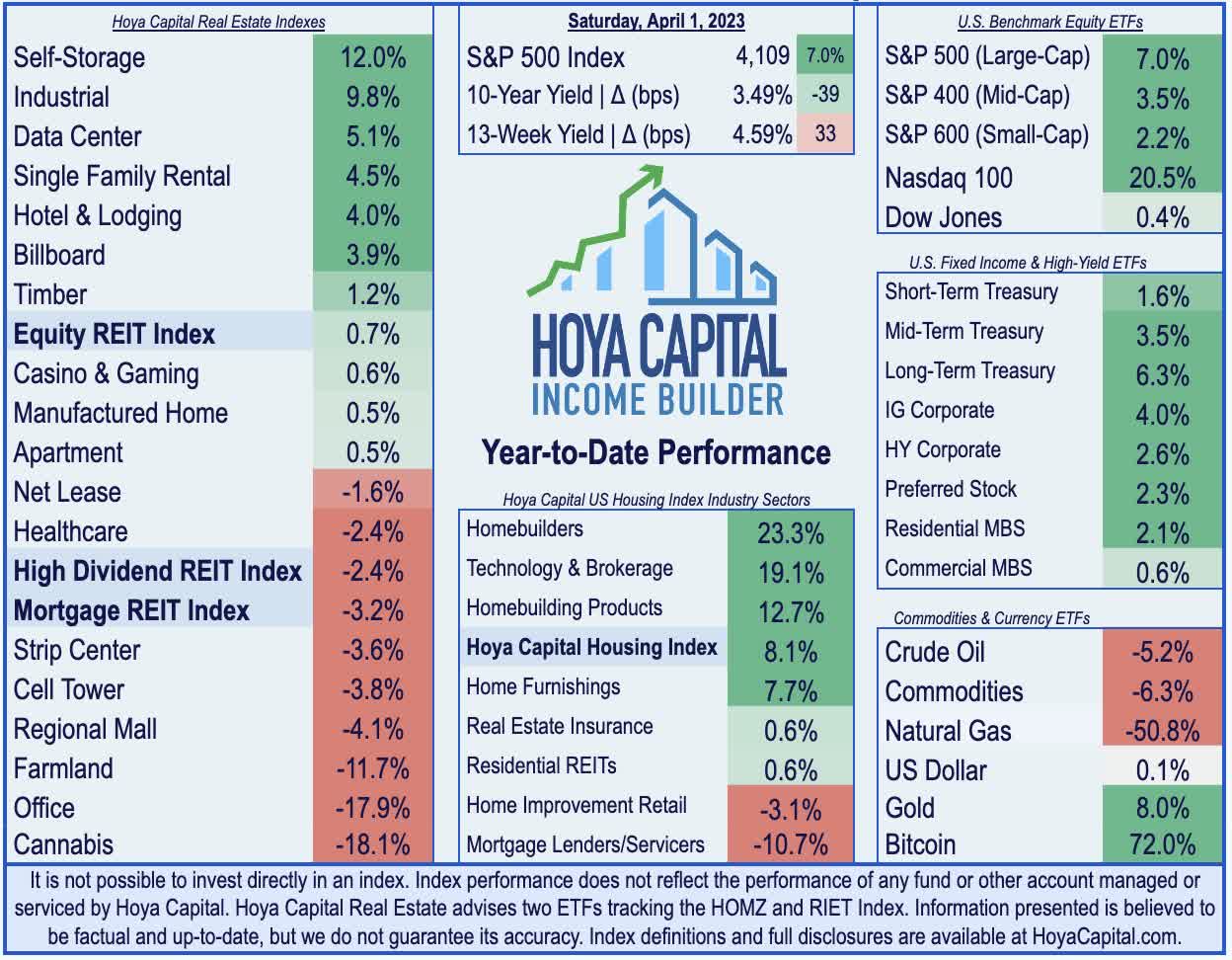

- Pushing its gains to 7.5% for the quarter, the S&P 500 posted its best week since last November with gains of 3.4%. The tech-heavy Nasdaq 100 climbed into "bull market".

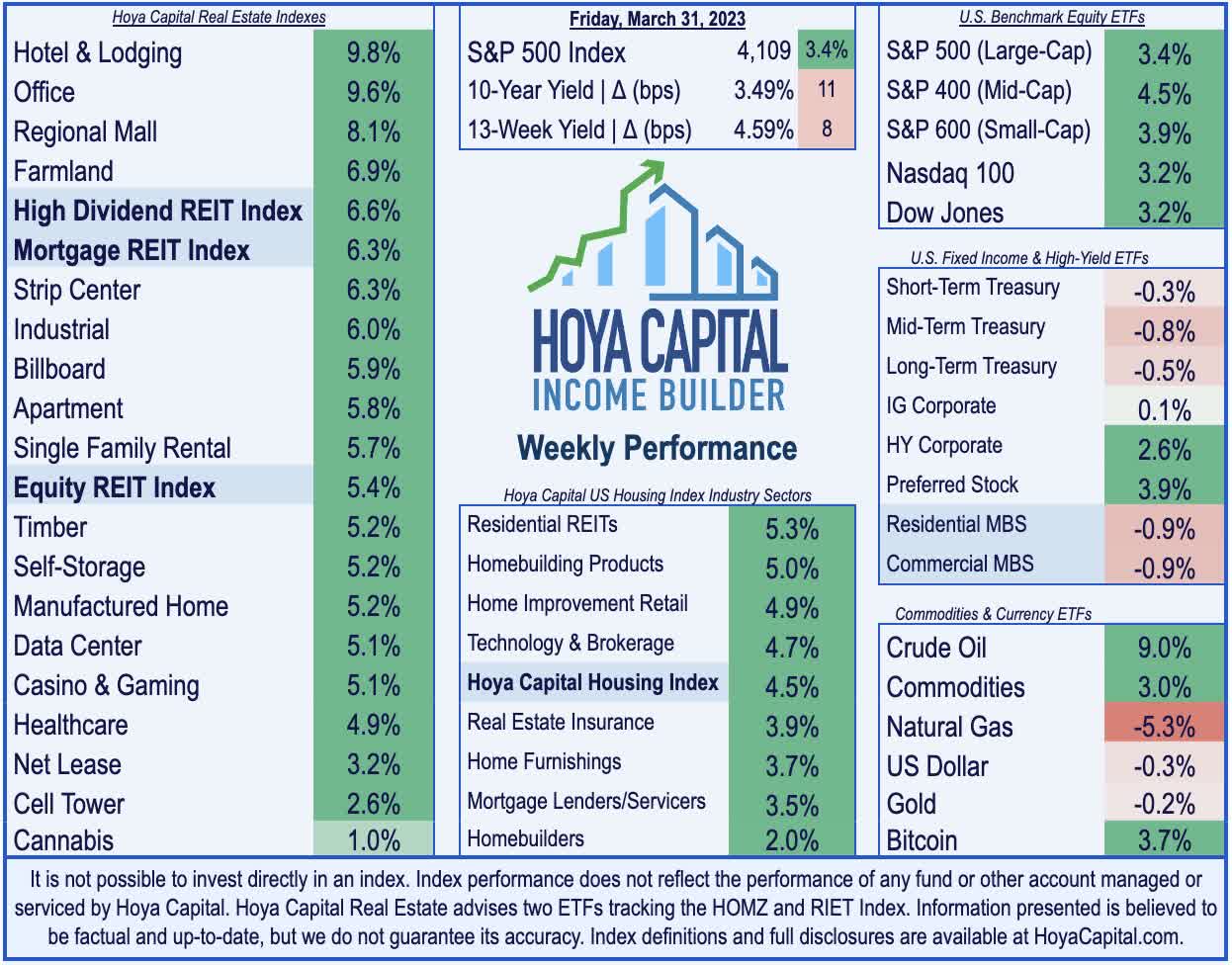

- Real estate equities - the sector with perhaps the most potential upside from easing inflation and interest rate pressures - were again among the leaders this week. Equity REITs rallied over 5%.

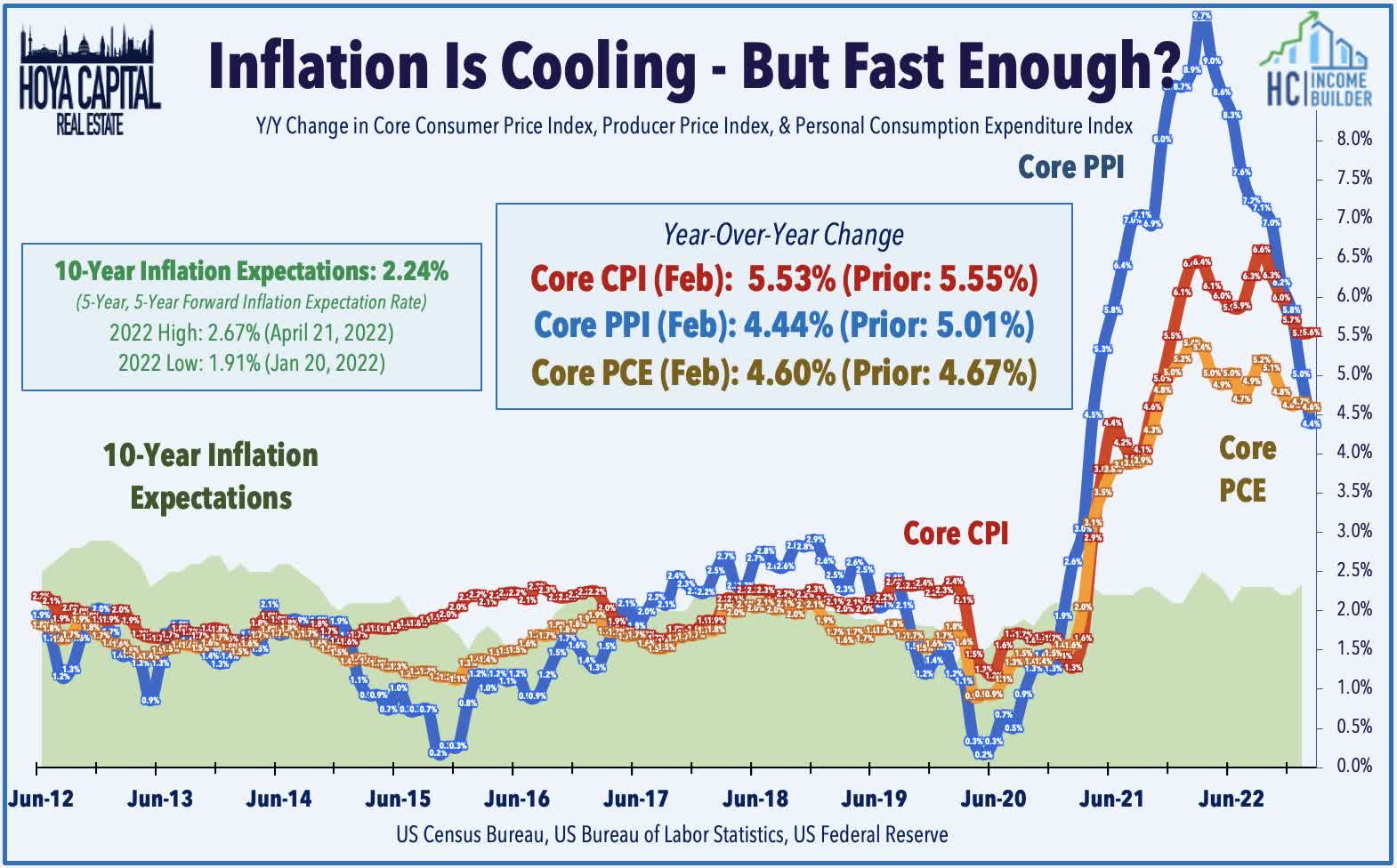

- Continuing the stretch of "good news" on the inflation front seen over the past several weeks, the closely-watched PCE Index provided further evidence that price pressures have cooled rather significantly in recent months.

- Hospital operator Medical Properties Trust rallied more than 9% this week after it announced that it will sell its Australian real estate investments and launch a counteroffensive against short sellers.

Real Estate Weekly Outlook

This is an abridged version of the full report and rankings published on Hoya Capital Income Builder Marketplace on March 31st.

U.S. equity markets concluded a wild quarter with their best week of the year as easing contagion concerns and further evidence of cooling price pressures lifted markets to a third-straight week of gains. After declining in three-straight quarters to start 2022 - which was the worst stretch of declines since 2009 - the major benchmarks notched a second-straight quarterly advance as a late-period rebound salvaged a quarter that was shaken for several weeks by tremors of financial instability following a pair of major bank collapses.

{kind=link}

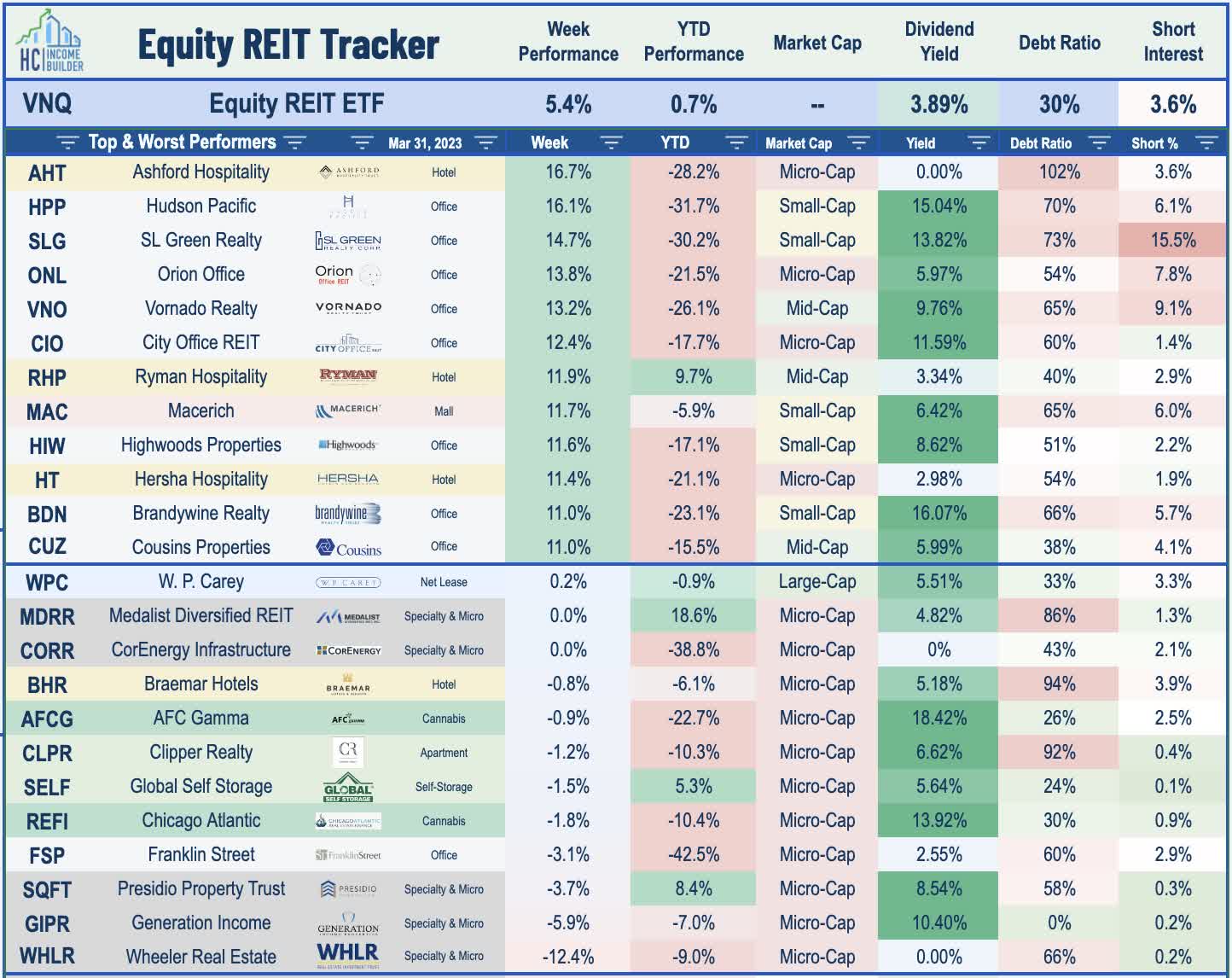

Pushing its gains to 7.5% for the quarter, the S&P 500 posted its best week since last November with gains of 3.4%. The tech-heavy Nasdaq 100 advanced another 3.2%, which pushed the benchmark into "bull market" territory with gains of over 20% since its late-2022 lows. While still lagging behind the large-cap benchmarks for the year, the Mid-Cap 400 and Small-Cap 600 closed the gap this week with gains of 4.5% and 3.9%, respectively. Real estate equities - the sector with perhaps the most potential upside from easing inflation and interest rate pressures - were again among the leaders this week, led by the most economically-sensitive segments. The Equity REIT Index rallied 5.4% on the week, with all 18 property sectors in positive territory, while the Mortgage REIT Index advanced more than 6%.

{kind=link}

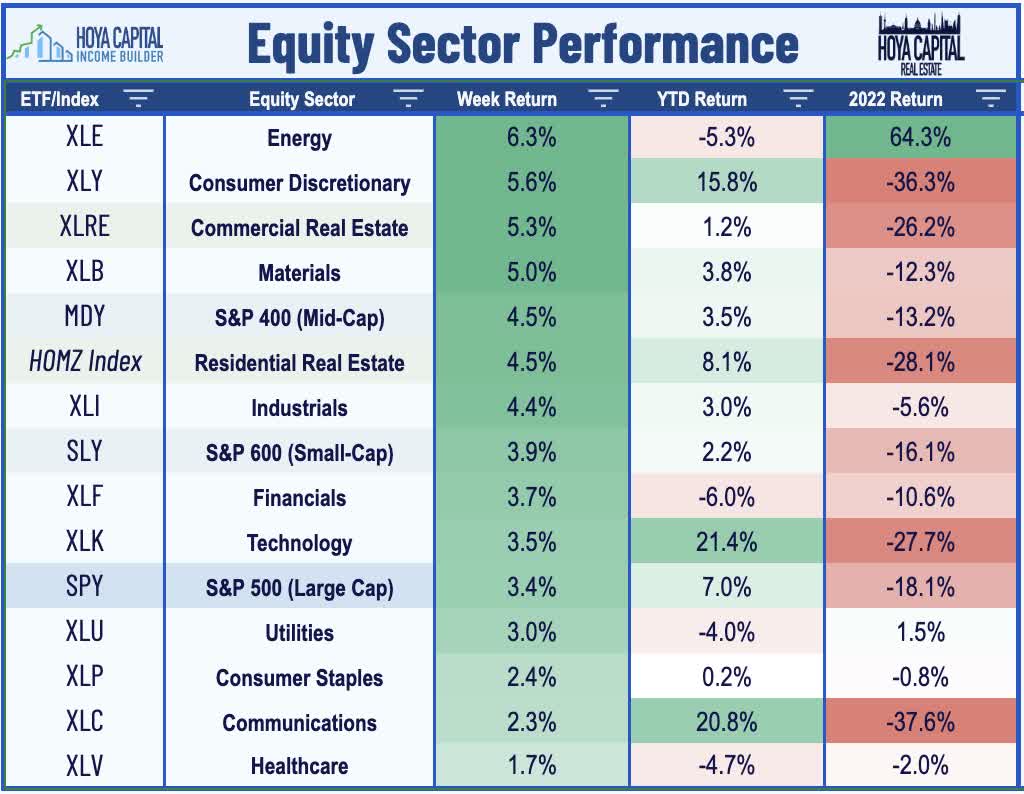

After surging to its highest-level since mid-November earlier this month, the CBOE Volatility Index ( VIX ) declined for sixth-straight sessions to end the week under 19 - its lowest level since March 6th before the SVB collapse. The MOVE Index - which measures bond market volatility - declined to its lowest level since March 9th after surging to its highest level since 2008 on March 15th. Bank stocks stabilized this week on calming contagion concerns following indications of regulatory support and the successful sale of large parts of Silicon Valley Bank and Signature Bank. After closing at its lowest-level in six months last Friday, the 2-Year Treasury Yield rebounded by more than 20 basis points to above 4.0%, while the 10-Year Treasury Yield rebounded by 11 to close at just shy of 3.50%. Commodities were mixed this week, with Crude Oil soaring by nearly 9%, but Natural Gas futures dipped another 5%. All eleven GICS equity sectors finished higher on the week, with Energy ( XLE ) and Consumer Discretionary ( XLY ) stocks leading the gains.

{kind=link}

Real Estate Economic Data

Below, we recap the most important macroeconomic data points over this past week affecting the residential and commercial real estate marketplace.

{kind=link}

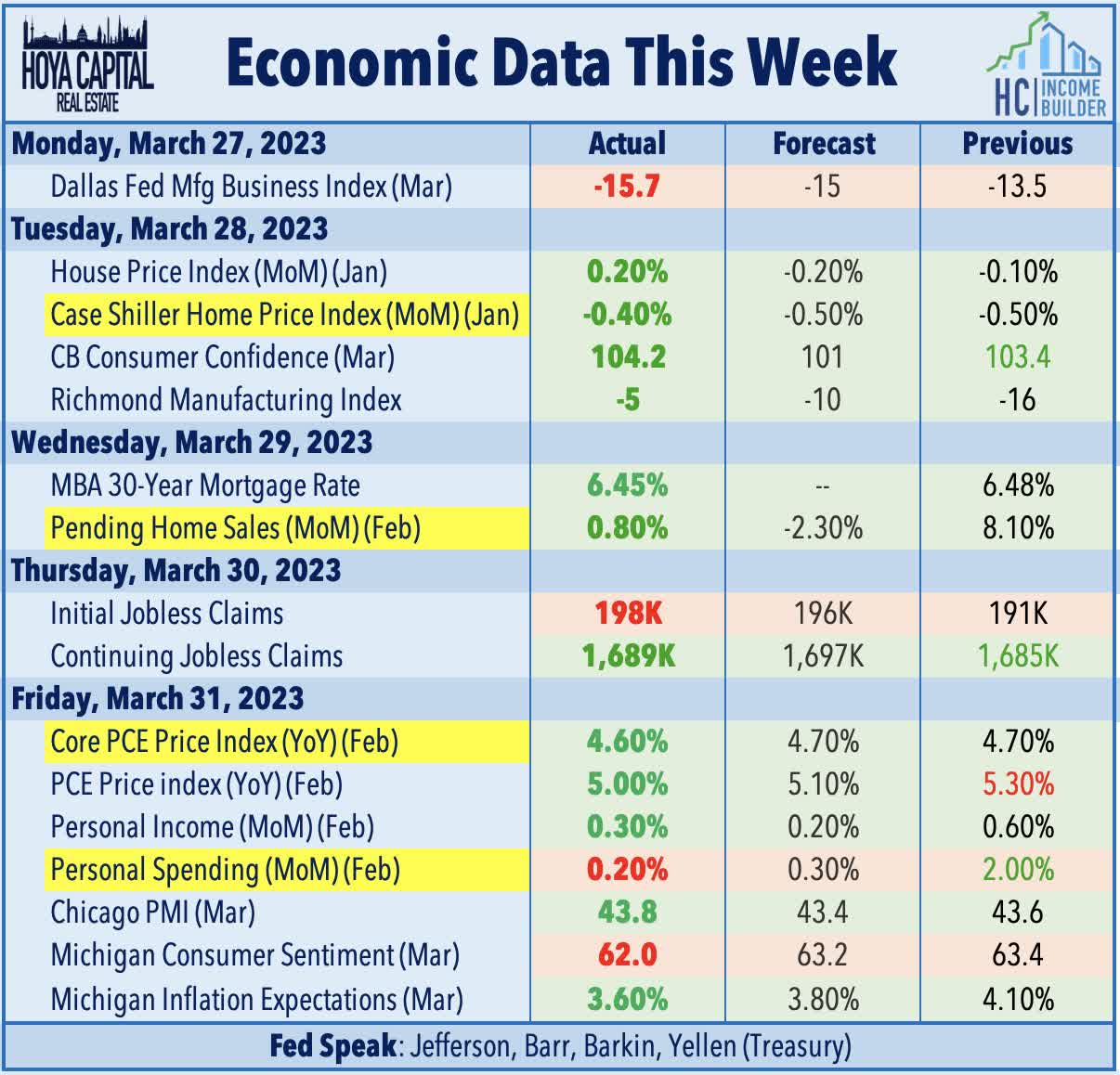

Continuing the stretch of "good news" on the inflation front seen over the past several weeks, the closely-watched PCE Index provided further evidence that price pressures have cooled rather significantly in recent months. The Core PCE Index decelerated to a 4.6% year-over-year rate in February, the lowest annual increase since October 2021 and below the 4.7% rate expected. As with the CPI Index, the PCE Index continues to significantly overstate real-time housing cost inflation due to lagged data collection issue, with the PCE Index showing an increase in housing costs of over 8% in this report despite recent market-based rent and home price metrics showing flat-to-negative increases over the past three quarters. As noted in the CPI report earlier this month, when the BLS Rent Index is replaced with the Zillow ZRI Rent Index, we observe a sharp decline in the CPI Index since mid-2022, with this "real-time CPI" averaging just 1.2% over the past eight months.

{kind=link}

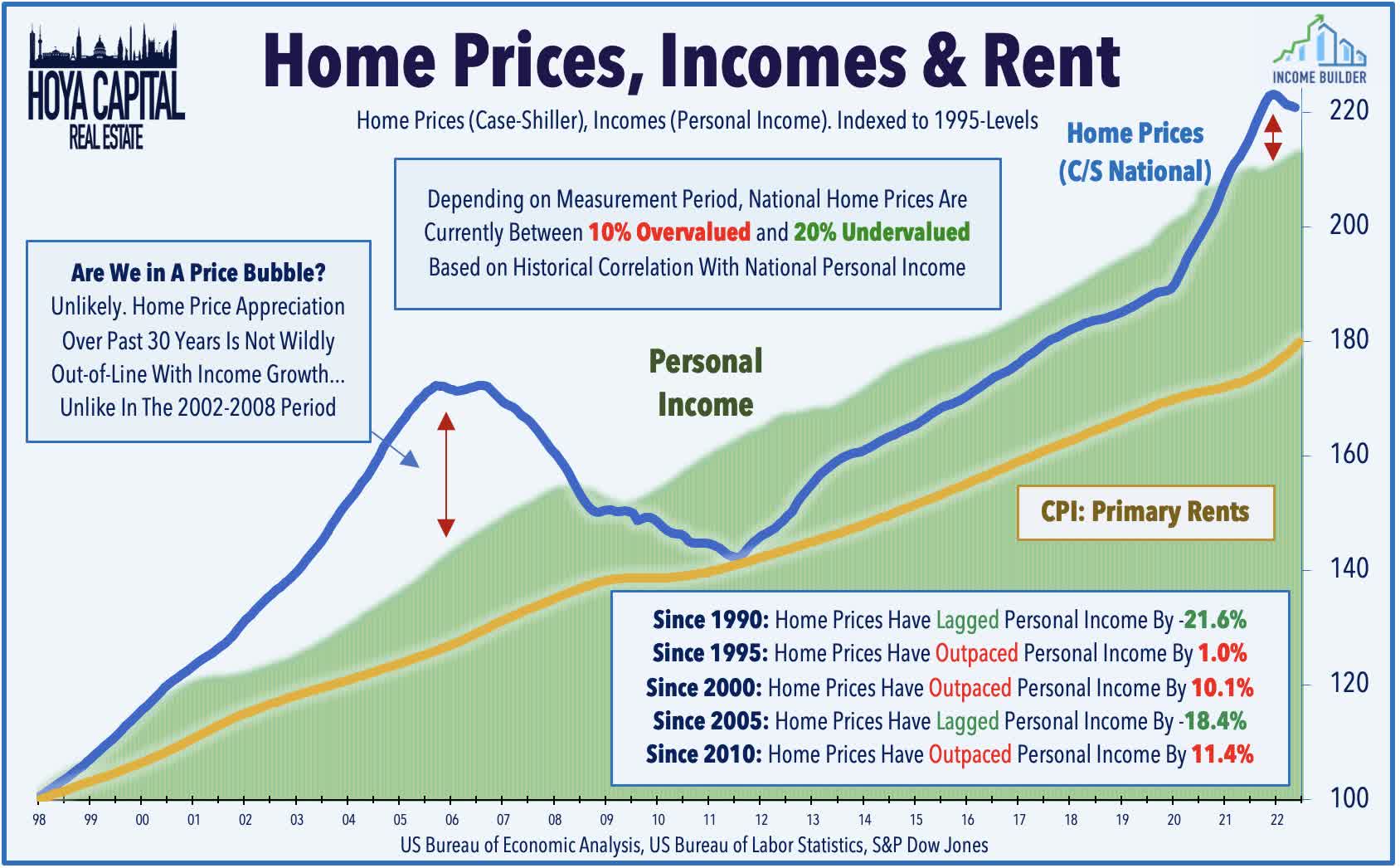

On that note, the Case Shiller Home Price Index showed that national home prices declined for a seventh-straight month in January, which pulled the index to over 5% below its peak in June 2022. While the pace of the home price declines slowed in January at the national level, home prices in West Coast markets remain under significant pressure with prices in Seattle now 16% below last year's peak, while prices in San Francisco have dipped by more than 12%. Strength in Sunbelt markets has offset the West Coast weakness, however, with home prices in Miami, Tampa, and Atlanta still within about 3% of the 2022 peaks. Importantly, while home price appreciation significantly outpaced income growth for a twelve-month period between mid-2021 and mid-2022, home prices are not wildly out-of-line with income growth over most long-term measurement periods. Since 1995, Home Prices have outpaced Personal Incomes by roughly 1%. By comparison, the "bubble" period in the early 2000s saw this disparity swell to over 30%.

{kind=link}

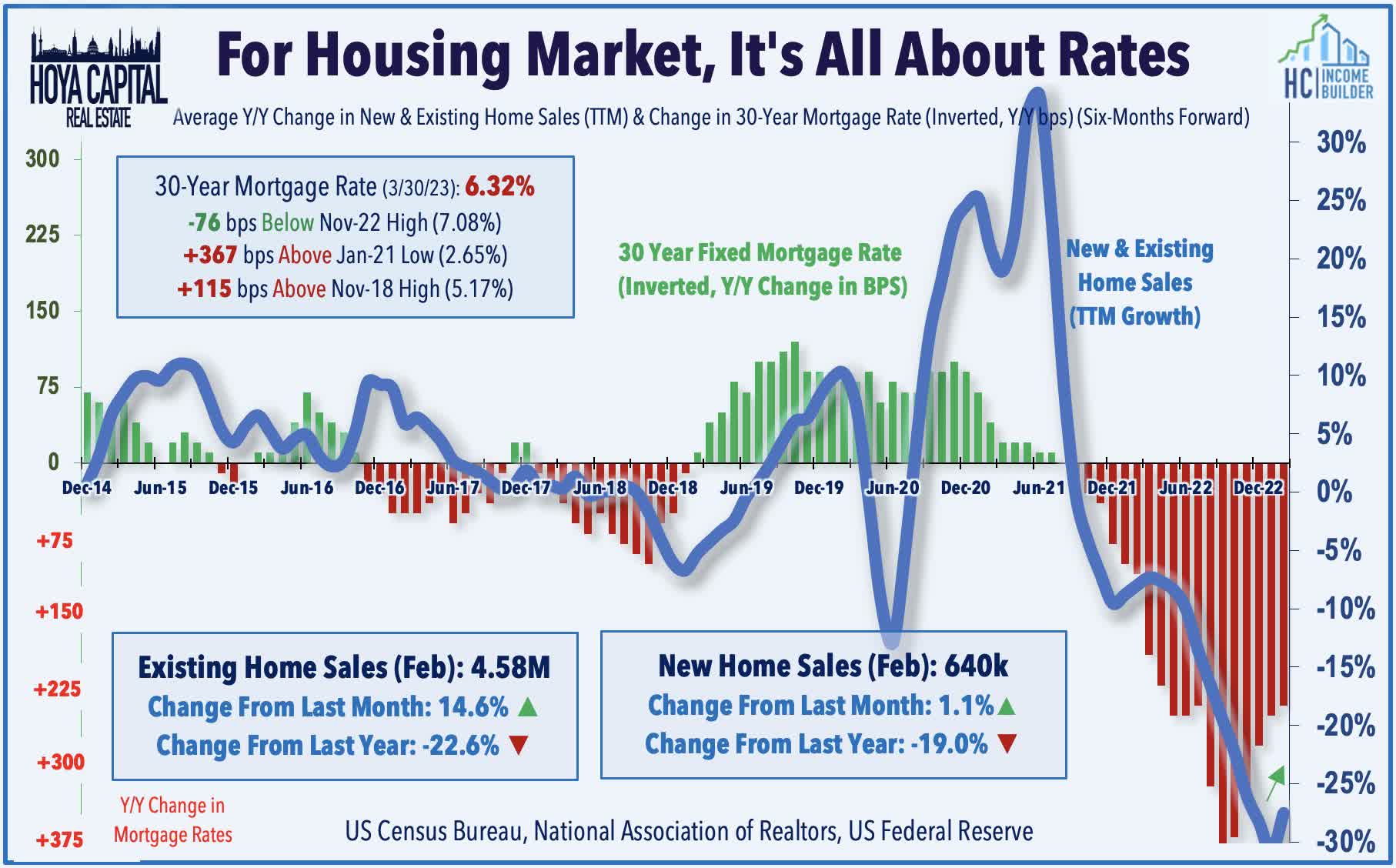

Concerns of further housing market deterioration have eased in recent months amid signs of life in housing demand, driven by a moderation in mortgage rates. Freddie Mac reported that the 30-year fixed-rate mortgage averaged 6.32% this past week, down another 10 basis points from the previous week and is now 76 basis points below the highs last November of 7.08%. Data this week showed that Pending Home Sales rose for a third-straight month in February, rising 0.8% from the prior month, but sales were still lower by over 20% from February 2022. Three U.S. regions posted monthly gains, while the West declined. Data last week showed that Existing Home Sales rose 14.5% in February compared with January to an annualized rate of 4.58 million units, which was the first monthly gain in 12 months and the largest increase since July 2020. New Home Sales data showed a third straight monthly increase to an annualized rate of 640k units - up 1.1% from January.

{kind=link}

Equity REIT Week In Review

Best & Worst Performance This Week Across the REIT Sector

{kind=link}

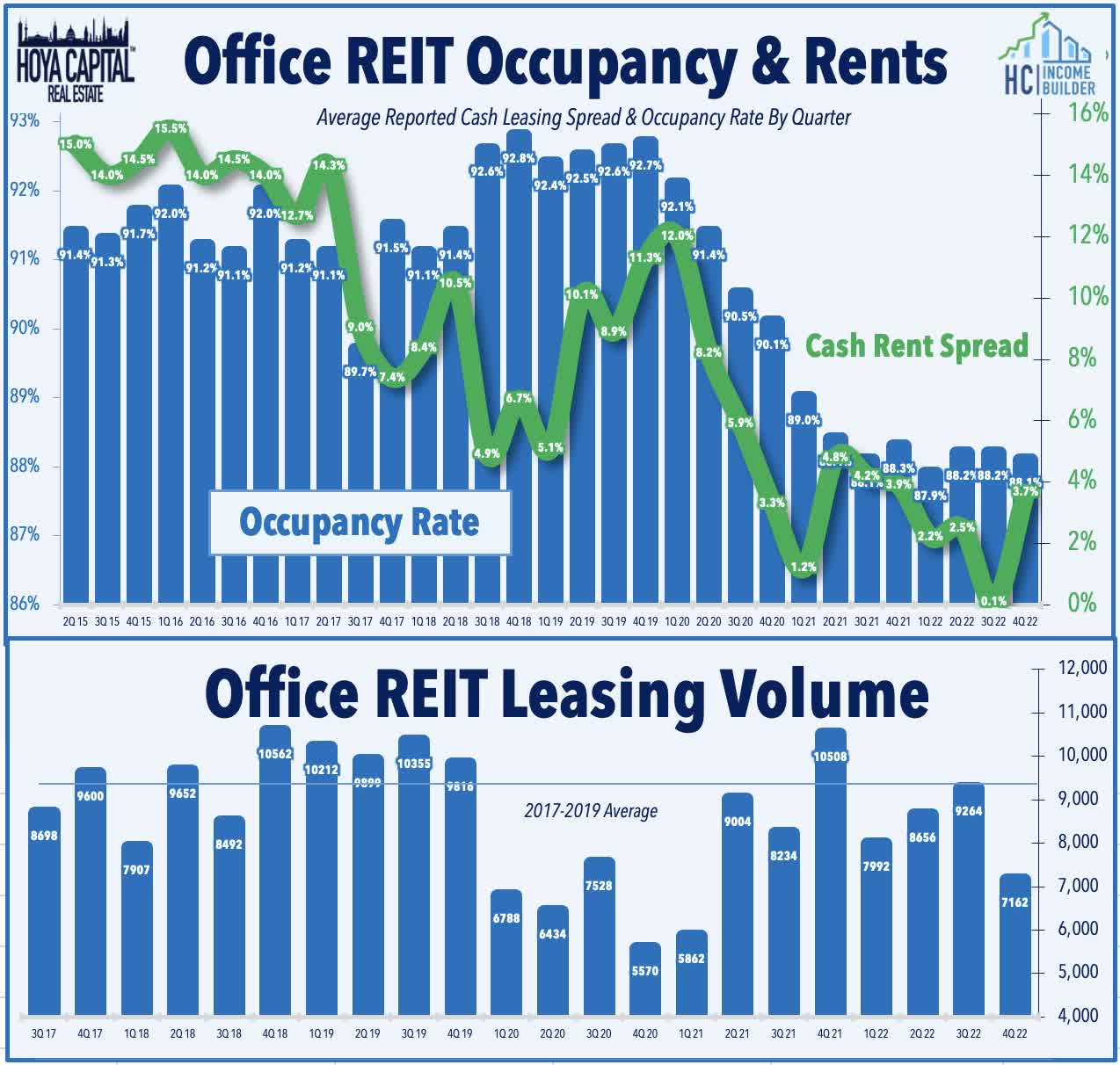

Office : The seemingly relentless selling pressure eased this week for office REITs, which posted their best week since April 2020 on easing contagion concerns following news that regulators tapped real estate specialist Newmark to help ensure an orderly sale of the roughly $60 billion of loans originated by Signature Bank, which failed earlier this month. NYC-focused were among the leaders this week, including SL Green ( SLG ), which rallied 15% this week after it announced that Palo Alto Networks signed a long-term lease covering a floor at One Madison Avenue, bringing the company's 2023 signed office leasing volume to 492K sq. feet - up from under 200K in Q4. Empire State Realty ( ESRT ), meanwhile, rallied over 8% after it announced that Claims Conference signed a 34K SF lease at 1359 Broadway. In our Earnings Recap last month, we noted that property-level fundamentals aren't as dire as the price action suggests, but there is concern that the gravity of private market distress will overwhelm any benefits of their comparative advantage.

{kind=link}

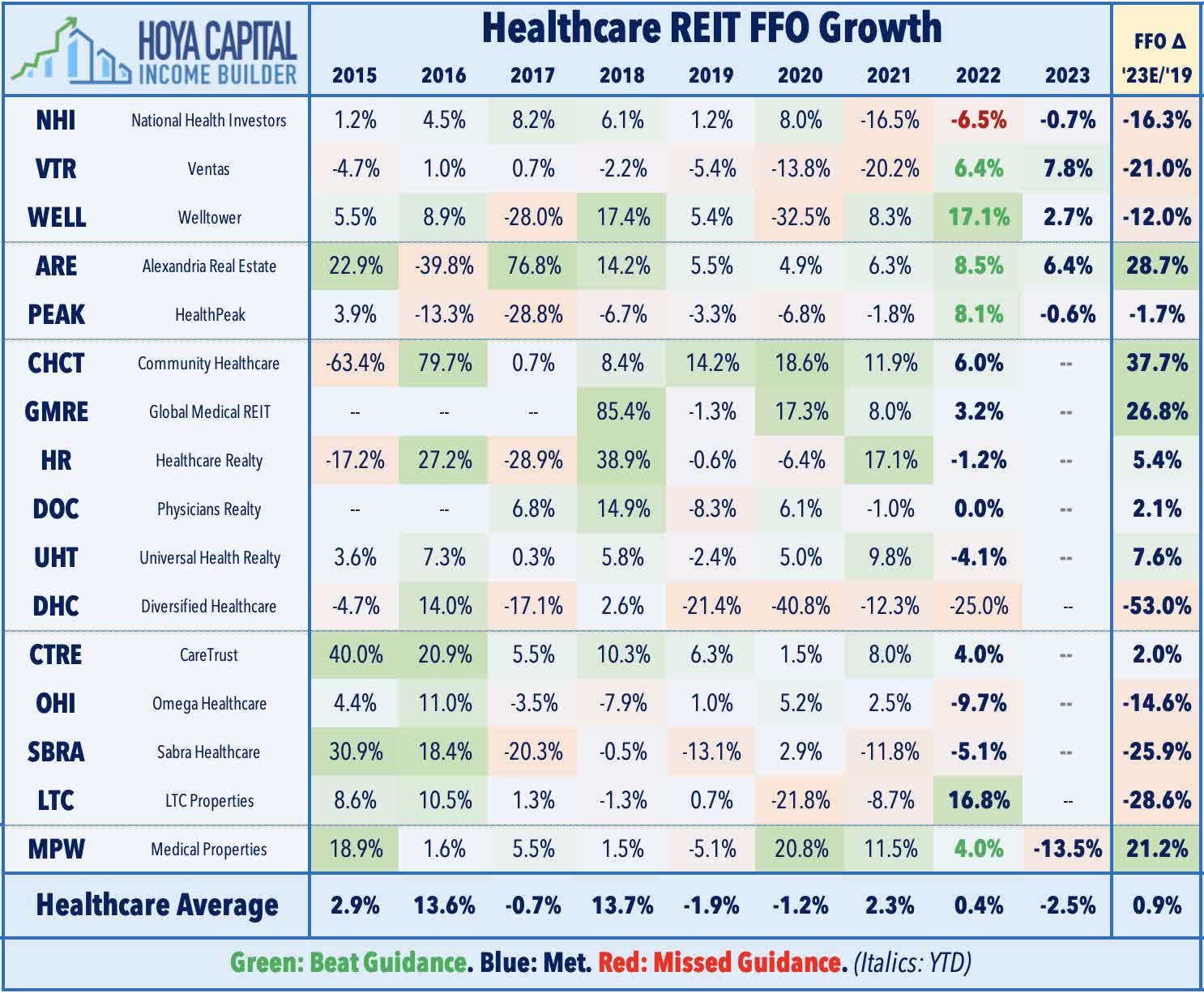

Healthcare : Hospital operator Medical Properties Trust ( MPW ) rallied more than 9% this week after it announced that it will sell its Australian real estate investments operated by Healthscope to affiliates of HMC Capital. Cash proceeds from the transaction are expected to cover the $810M (1.2B AUD) loan used to fund the 2019 acquisition of the 11 hospitals leased to Healthscope, according to a statement. The deal is expected to be completed in the second half of the year. MPW also announced that it has filed a lawsuit in federal court against Viceroy Research LLC, a short-selling firm that has "repeatedly published baseless allegations to drive down the Company’s stock price." MPW issued a letter to shareholders, "clarifying the facts underlying its strong and sustainable business performance and track record of value creation." While MPW had indeed been one of the better-performing healthcare REITs over the past decade, earnings results from MPW last month showed a downbeat outlook for 2023 with expectations of a 13.5% dip in its FFO at the midpoint of its range, impacted by rent collection issues from Prospect Medical - its third-largest tenant at roughly 12% of revenues.

{kind=link}

Sticking in the healthcare sector, Senior Housing-focused REIT Ventas ( VTR ) advanced about 2% on the week after it announced that it will take ownership of the portfolio backing its $486M loan to Santerre Health Investors, which has struggled to make interest payments over the past several quarters amid an ongoing "COVID hangover" that has pressured healthcare operators across the industry. The Santerre Portfolio includes 88 medical office buildings (“MOBs”), 16 senior housing operating portfolio (“SHOP”) communities, and 48 skilled nursing facilities and hospital assets. VTR's ownership will be subject to an existing $1 billion non-recourse senior loan secured by the portfolio which bears interest at LIBOR +1.84% and matures in June 2023. VTR expects to complete the process of taking ownership of the Santerre Portfolio in the second quarter of 2023. In Healthcare REITs: Life After The Pandemic, we discussed the outlook for each healthcare sub-sector, noting that the outlook for senior housing has brightened the most in recent quarters.

{kind=link}

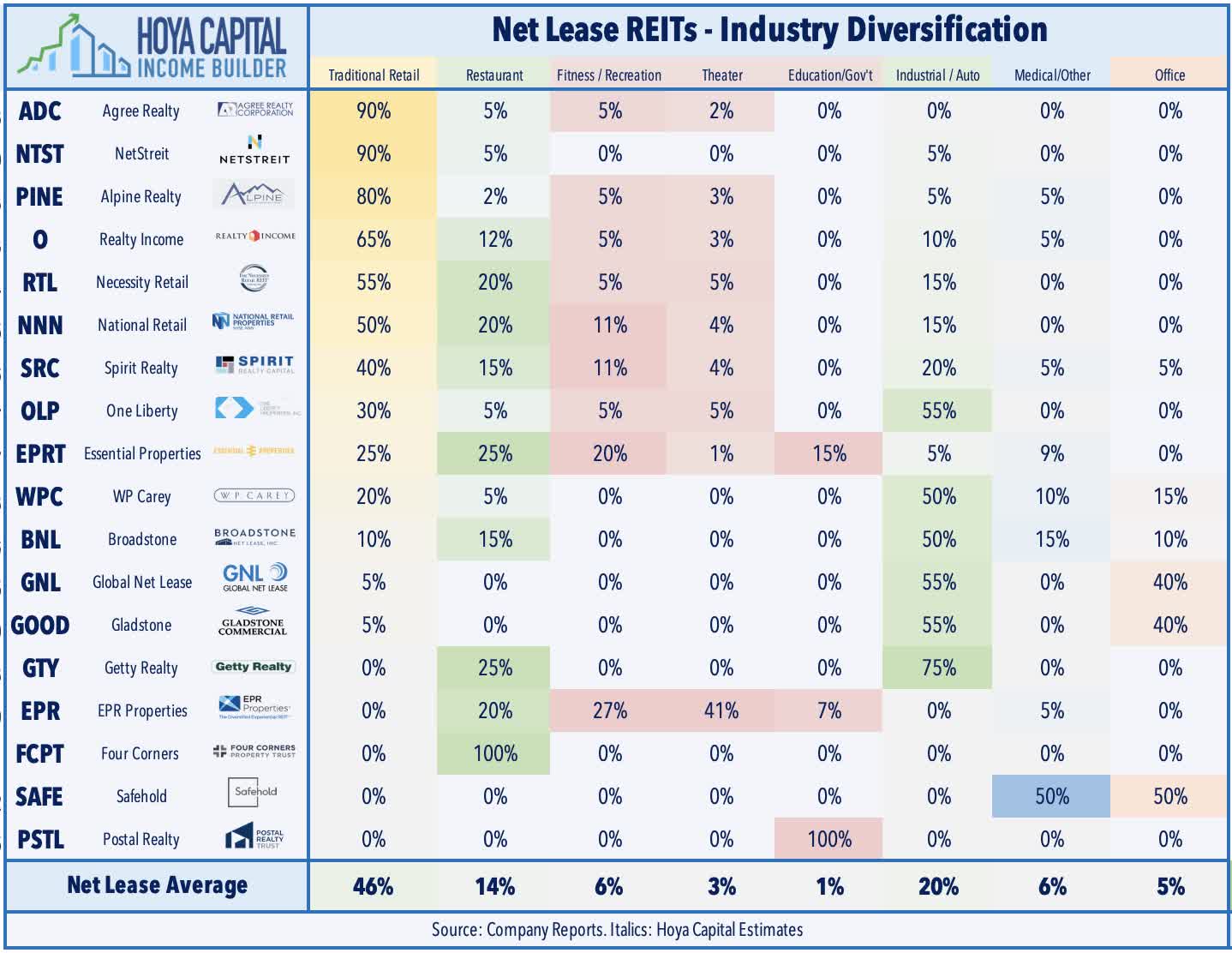

Net Lease : Movie theater-focused net lease REIT EPR Properties ( EPR ) rallied 8% this week after reports that Amazon ( AMZN ) is exploring the possibility of an acquisition of AMC Entertainment ( AMC ), the owner of a chain of nearly 600 movie theaters in North America and internationally. Separately, Bloomberg reported this week that Cineworld Group - the second-largest movie theater chain behind AMC - plans to exit bankruptcy after reaching a deal with creditors to trim billions of dollars of debt from its balance sheet. Last week in Net Lease REITs: Avoiding The Winners Curse , we noted that movie theaters were one source of potential credit risk for the sector, which represents roughly 5% of overall net lease NOI, but nearly half of NOI for EPR Properties . Box Office Mojo data shows that box office revenue plunged 80% in 2020 and has remained about 25% below 2019 levels in early 2023. A handful of other net lease REITs have between 1.5-5% of their rents coming from movie theater tenants.

{kind=link}

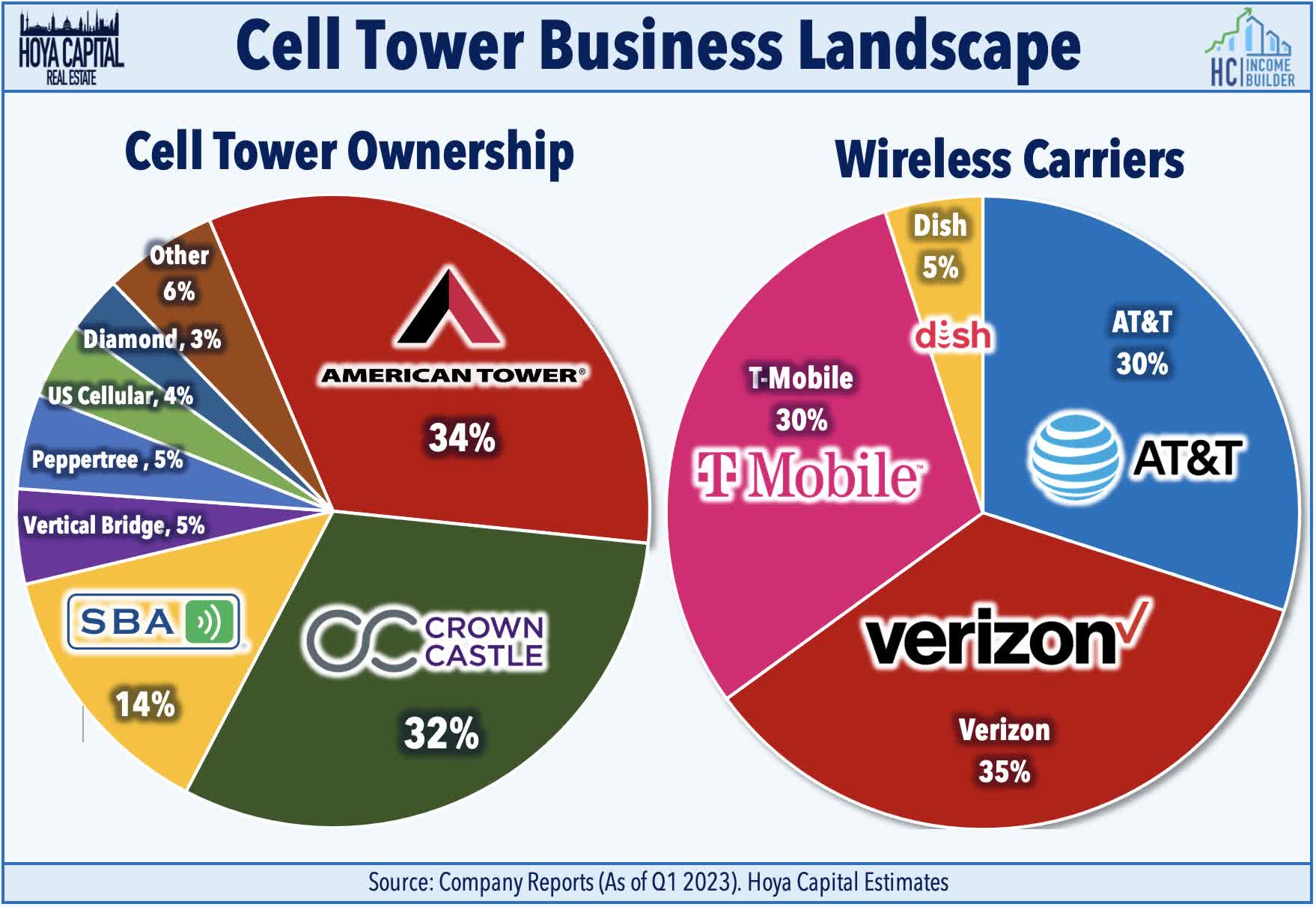

Cell Tower : One of several beaten-down small-cap REITs that led the rebound this week, Uniti Group ( UNIT ) - a REIT that owns fiber networks used to provide "backhaul" connectivity between towers and data centers - rallied more than 5% after it announced that it extended its $500M revolving credit facility to September 2027, the first of many steps needed to shore up its balance sheet. UNIT has been slammed over the past year due to its debt-heavy balance sheet, as the surge in benchmark interest rates has forced the company to refinance its recent debt maturities at substantially higher rates. Crown Castle ( CCI ) - which we named one of our three " Best Ideas in Real Estate " - rallied more than 3% this week following an analyst upgrade from MoffettNathanson and a credit rating affirmation from Fitch Ratings. This week, we published Cell Tower REITs: 5G's Killer App , which analyzed why the concern over the long-term competitive positioning of land-based cellular networks in the ever-evolving telecommunications industry is significantly "over-discounted" in current valuations. Awed by impressive rocket launches, the market has overlooked the more meaningful industry dynamic - the rapid growth of Fixed Wireless Access ("FWA") - which has further solidified the competitive positioning of land-based wireless networks - a market that is effectively "cornered" by the three major cell tower REITs.

{kind=link}

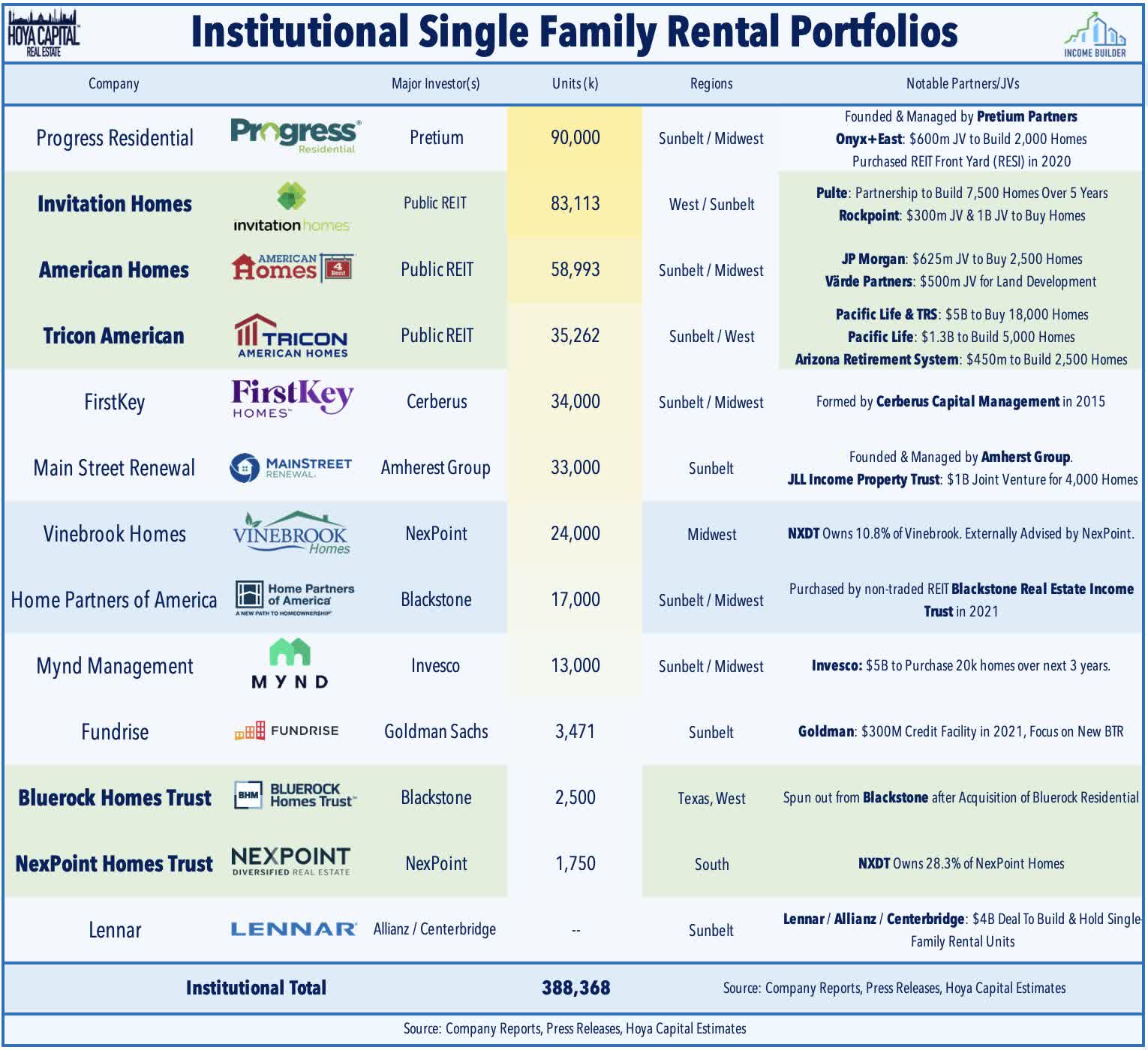

Single-Family Rental : This weekend, we'll publish an updated report on the SFR sector. One of the best-performing property sectors this year, SFR REITs have rebounded over the past quarter as the previously-sluggish U.S. housing sector has shown signs of life amid a moderation in mortgage rates. The dire predictions of a "hard landing" in rental markets have been rebuffed in recent months by stabilizing - and even reaccelerating - rent growth seen across the major rent indexes and in recent reports from SFR REITs. Data from Zillow last week showed that national rent growth in February posted its strongest month-over-month gain in six months, while the Apartment List National Rent Report this week showed that rents increased 0.5% in March - the second straight monthly increase and a slight acceleration over last month’s pace. That said, recent "start-up" entrants that pushed the leverage limits are learning the hard way that SFRs are a capital-intensive business that requires considerable scale to operate profitably over time. We believe that the "institutionalization" of the SFR market remains in the early innings and that elevated levels of interest rates will be a catalyst to drive further market share gains to larger institutions that have access to cheaper and deeper capital.

{kind=link}

Mortgage REIT Week In Review

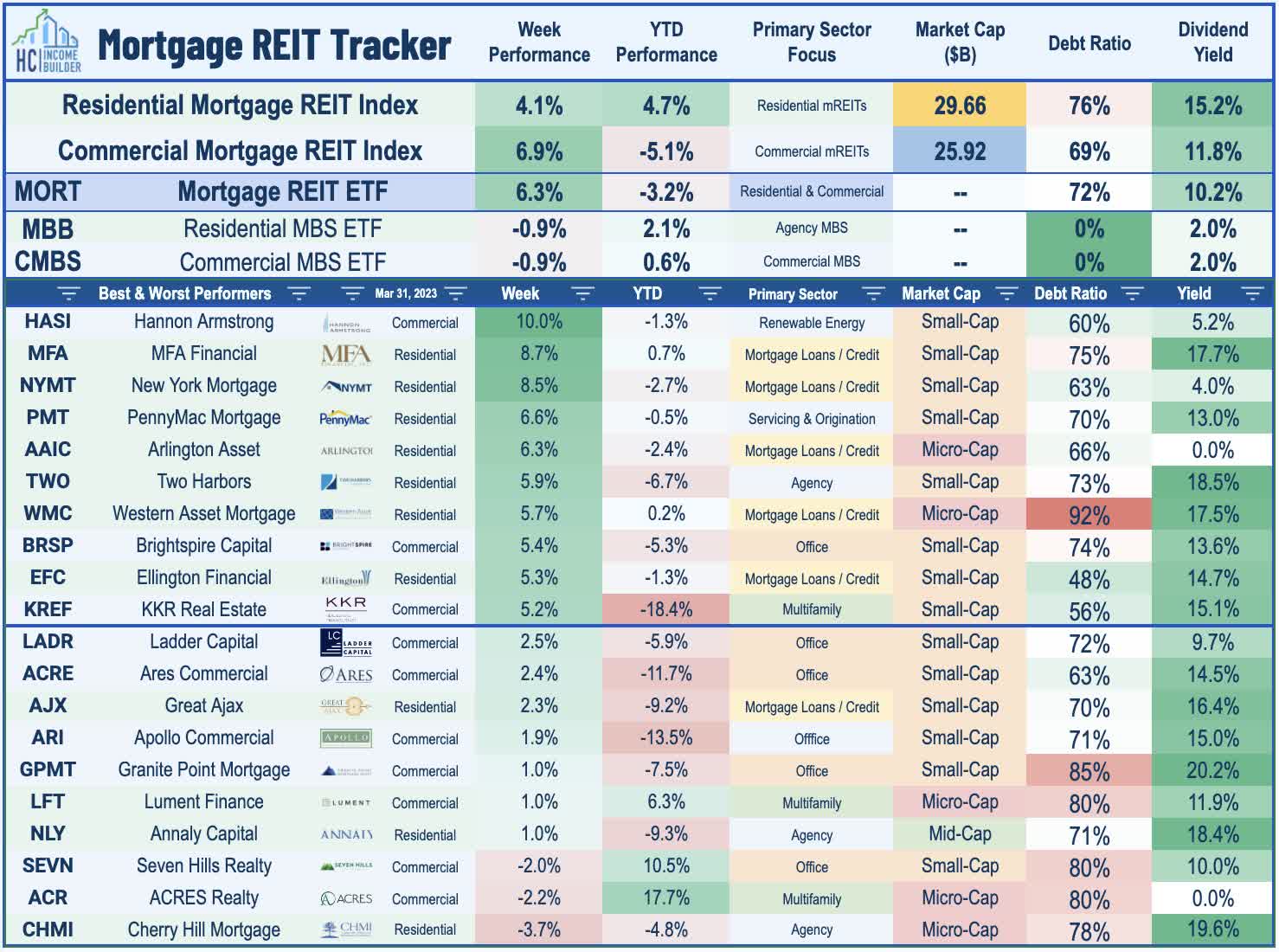

Mortgage REITs were among the best-performers this week, a second-straight week of solid gains following punishing declines earlier in the month. The iShares Mortgage Real Estate Capped ETF ( REM ) - which had dipped nearly 14% in the first two weeks of March - has erased half of those declines over the past two weeks with another 6.3% advance this week. A pair of micro-cap mREITs were among the leaders this week after rounding out earnings season with solid reports. Sachem Capital ( SACH ) rallied more than 4% after it reported full-year EPS of $0.46 - up from $0.44 in 2021. SACH noted that its adjusted EPS of $0.53/share for the year covered its $0.52/share dividends paid during the year. Arlington Asset ( AAIC ) rallied more than 6% this week after noting that its Book Value Per Share ("BVPS") increased about 2% to $6.59 in Q4 and stood at $6.48 as of February 28. Invesco Mortgage ( IVR ) advanced 2% despite reducing its dividend to $0.40/share - a 38.5% decrease from its prior dividend of $0.65 - representing a forward yield of 14.4%. IVR estimated that its Book Value Per Share ("BVPS") was $11.96-$12.44 as of March 17, a decline of roughly 5% since the end of Q4 at the midpoint of the range.

{kind=link}

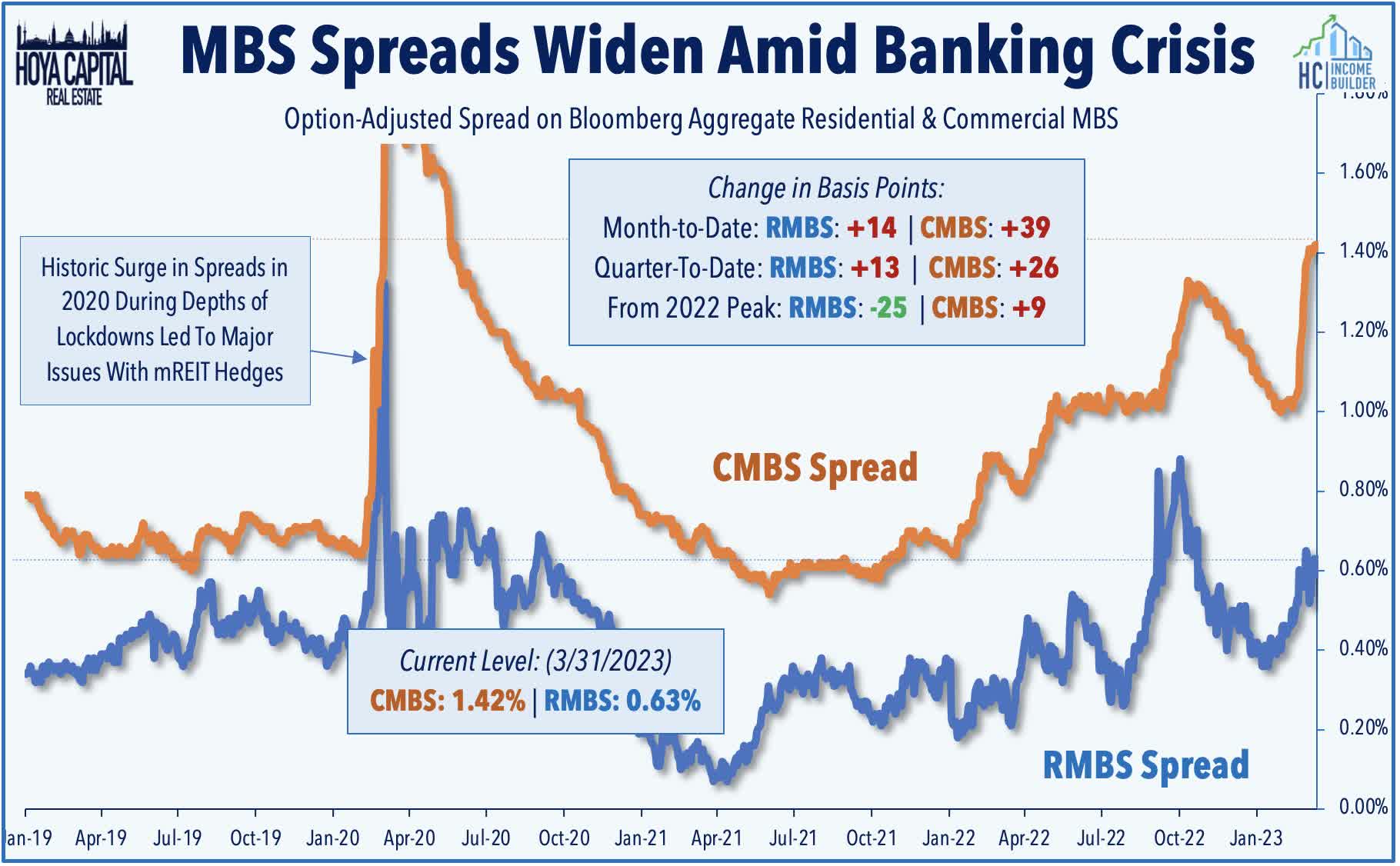

We've kept our eyes on the underlying Residential MBS ( MBB ) and Commercial CMBS ( CMBS ) markets throughout the recent banking crisis. These indexes remain in positive territory for the year - a surprise for some, considering the amplified media focus in recent weeks - as downward pressure from wider spreads has been more than offset by tailwinds from the decline in benchmark interest rates. CMBS spreads widened from 1.16% at the end of Q4 to 1.42% at the end of Q1 (26 basis points), while RMBS spreads widened from 0.50% to 0.63% during the quarter (13 basis points). We discussed in our Mortgage REITs report last week how sharp changes in benchmark rates and/or spreads in either direction can wreak havoc on mortgage REITs that are caught over-levered or improperly hedged - a risk that is particularly acute for agency-focused mREITs that typically employ more extensive hedging programs.

{kind=link}

REIT Capital Raising & REIT Preferreds

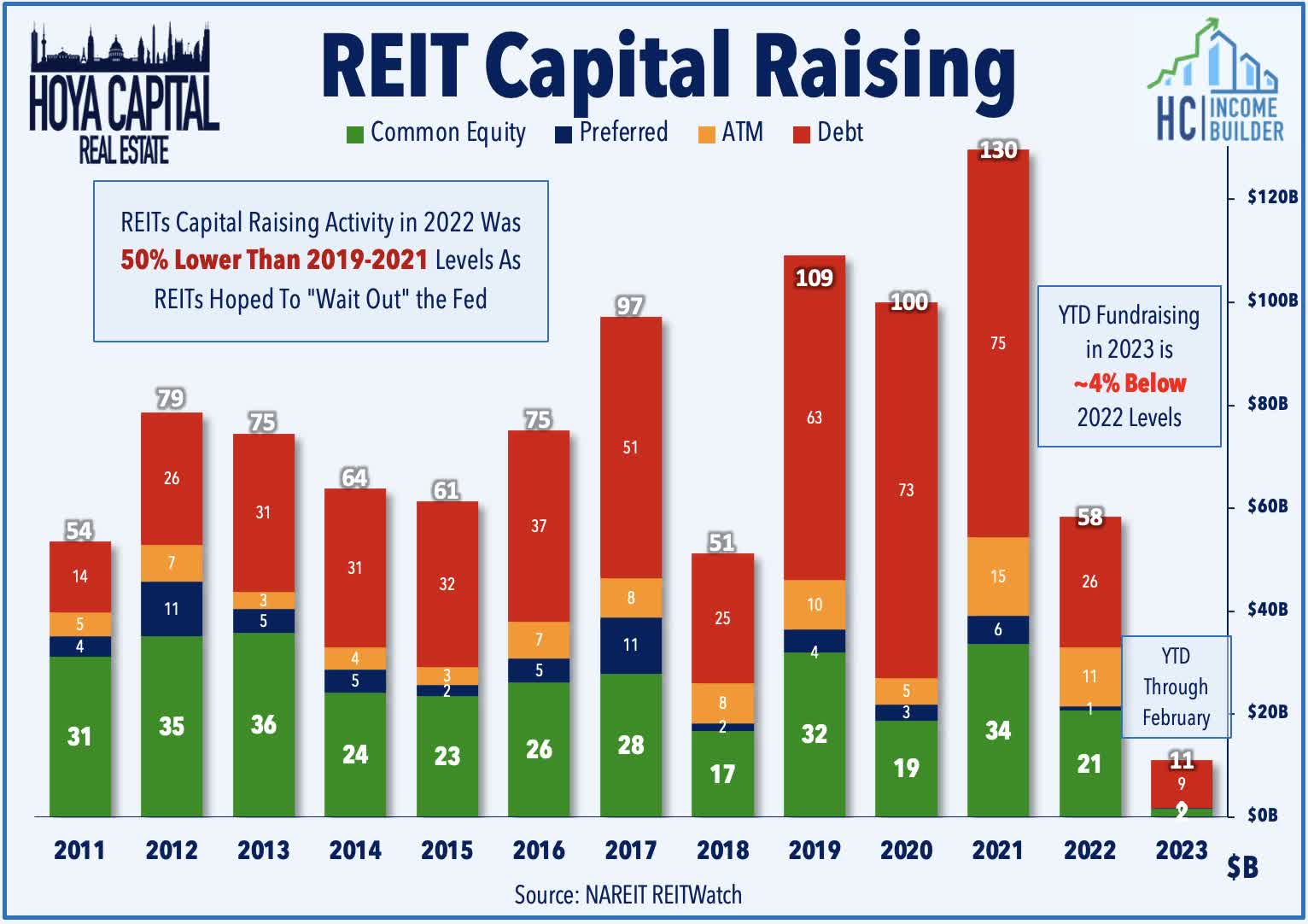

In our State of the REIT Nation report, we noted that after a historically quiet year of capital raising activity in 2022, REITs have returned to the primary markets in recent weeks with a common objective: reduce variable rate debt exposure. This week, office REIT Highwoods ( HIW ) announced that it obtained a $200M, 5-year secured loan provided by a life insurance company at a fixed rate of 5.69% secured by Bank of America Tower at Legacy Union in Uptown Charlotte and noted that proceeds have been used to reduce amounts outstanding on its revolving credit facility. Industrial REIT Rexford ( REXR ) priced $300 million of 5.0% senior unsecured notes due 2028 and intends to use proceeds to fund funding future acquisitions. S&P reported last week that REITs had raised $11B in capital year-to-date through the end of February, which is roughly 4% below 2022-levels over that period.

{kind=link}

2023 Performance Recap & 2022 Review

Through the first quarter of 2023, the Equity REIT Index is now higher by 0.7% on a price return basis for the year, while the Mortgage REIT Index is lower by 3.2%. This compares with the 7.0% gain on the S&P 500 and the 3.5% gain for the S&P Mid-Cap 400 . Within the real estate sector, 10-of-18 property sectors are in positive territory on the year (up from 2-of-18 last week), led by Self-Storage, Industrial, and Data Center REITs. At 3.49%, the 10-Year Treasury Yield has declined 39 basis points since the start of the year, which is nearly a full percentage point below its 2022 highs of 4.30%. The US bond market has stabilized following its worst year in history as the Bloomberg US Aggregate Bond Index has gained 3.0% this year.

{kind=link}

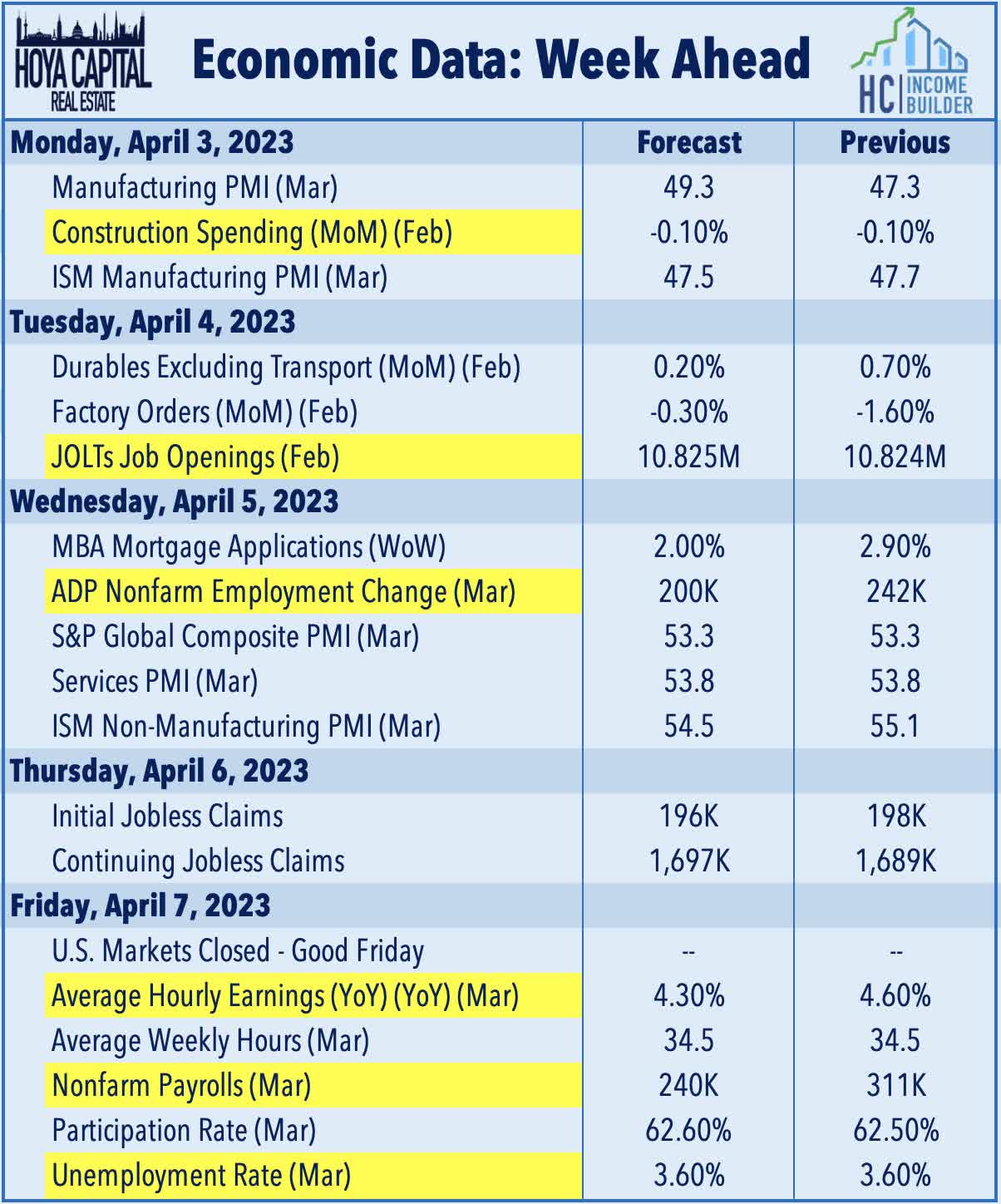

Economic Calendar In The Week Ahead

Employment data highlight a critical week of economic data in the Easter-shortened week ahead, headlined by JOLTS report on Tuesday, ADP Payrolls data on Wednesday, Jobless Claims data on Thursday, and the BLS Nonfarm Payrolls report on Friday. Markets will be closed on Friday in observance of Good Friday. Economists are looking for job growth of roughly 240k in March following the surprisingly strong reports in both January and February. 'Good news is bad news' will likely be the theme of these reports as investors and the Fed await the long-awaited cooldown in labor markets which has yet to fully materialize. The closely-watched Average Hourly Earnings series within the payrolls report - which is the first major inflation print for March - is expected to show a cooldown in wage growth in March to 4.3%.

{kind=link}

For an in-depth analysis of all real estate sectors, check out all of our quarterly reports: Apartments , Homebuilders , Manufactured Housing , Student Housing , Single-Family Rentals , Cell Towers , Casinos , Industrial , Data Center , Malls, Healthcare , Net Lease , Shopping Centers , Hotels , Billboards , Office , Farmland , Storage , Timber , Mortgage , and Cannabis.

Disclosure : Hoya Capital Real Estate advises two Exchange-Traded Funds listed on the NYSE. In addition to any long positions listed below, Hoya Capital is long all components in the Hoya Capital Housing 100 Index and in the Hoya Capital High Dividend Yield Index . Index definitions and a complete list of holdings are available on our website.

{kind=link}

For further details see:

Wild Quarter Ends With Optimism