OSTK - Williams-Sonoma: A True Retail Market Beater

Summary

- WSM has continued beating the market through multiple headwinds.

- The company has managed the transition to omni-channel more or less flawlessly.

- Given the solid growth opportunities, pristine balance sheet, smart capital allocation, and fair valuation, I think WSM continues to beat the market.

I've been covering Williams-Sonoma ( WSM ) for quite a while on this site. My first article, in 2017, was part of a series on retailers bucking the retail apocalypse brought on by Amazon (NYSE: AMZN ), when it felt like the prevailing wisdom was that brick and mortar was going the way of the dinosaur. Well, some of them have, or are on the way. WSM won't be joining them, however. The company has transformed itself into an e-commerce company with a brick and mortar footprint, and has smashed the market while doing so. Look at the returns since the last time I wrote on them, just before Covid:

Seeking Alpha Company Presentation

{kind=link}

{kind=link}

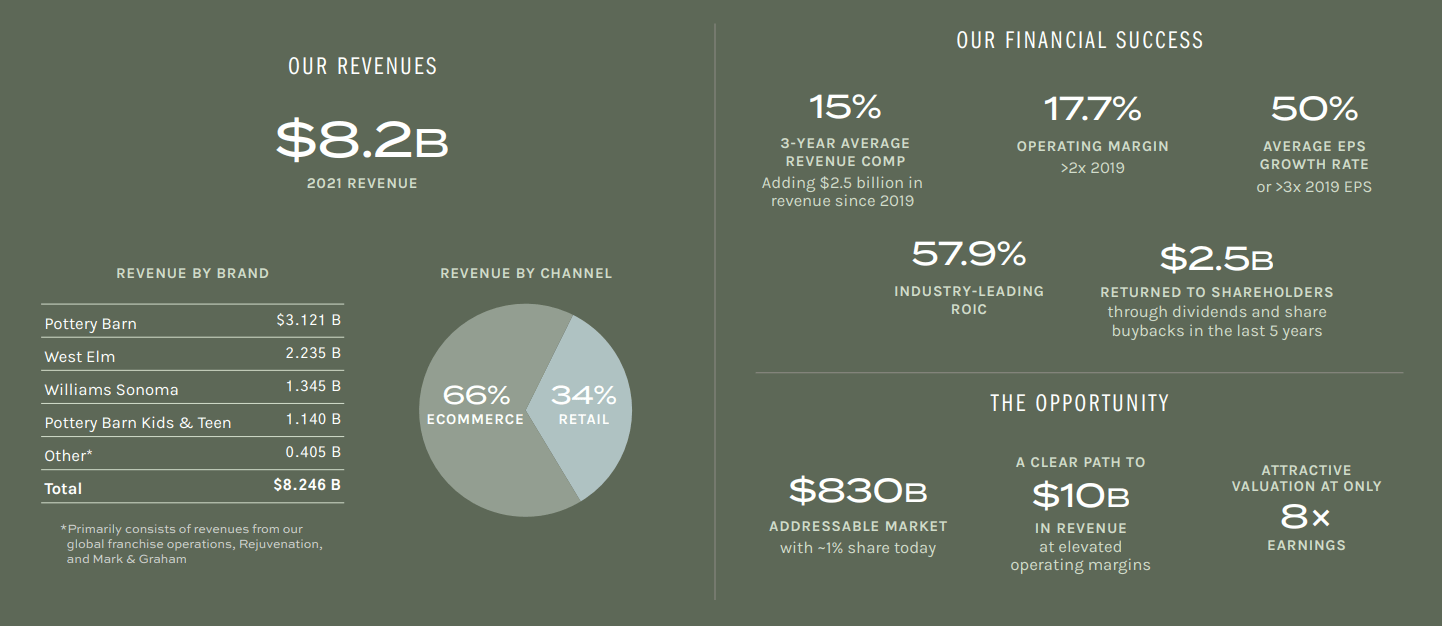

WSM covers home furnishings, assorted home goods, and more across the higher end consumer landscape. The different brands are specifically targeted at every age demographic, and despite the name of the company, Pottery Barn and West Elm dominate the revenue makeup now more so than Williams-Sonoma. The company has leveraged its 12M member cross-brand loyalty program, the Key, to build a significant understanding of its target consumer and used that to great effect in driving high returns on invested capital.

WSM stands up to online-only competitors in a few ways. Firstly, companies like Wayfair ( W ) and Overstock ( OSTK ) lack the operating history. WSM has done so well over time using targeted marketing and a data-driven knowledge of its target consumer. This has allowed the company to spend less on marketing than some competitors per dollar of revenue, improving profitability. Additionally, many retailers like Lowe's ( LOW ), Home Depot ( HD ) and others have succeeded in the new environment by leveraging their store footprint. WSM anticipates closing many of its poorer-performing locations, and utilizing the remaining for ship-to-store. Cross-brand or multi-line items can be part of one purchase and conveniently shipped to a store vice a person's house to improve customer flexibility.

Although WSM faces economic pressures from a downturn in housing or the general economy, there is validity to the argument that its target consumer is somewhat less affected than others. Pottery Barn, specifically, targets more affluent consumers who may be less affected by downturns.

In the most recent quarter, the company reported earnings growth of 12% on 7% sales growth. However, management pulled guidance for FY24, and is holding off on FY23 guidance until the next quarterly report based on uncertainties around the macro environment. Although it's never great to hear, if management doesn't feel they have a good finger on the pulse, we will just have to wait and see what happens. All that being said, these are short-term problems, and WSM has stood the test of time through plenty of difficult economic environments.

A little perspective from CEO Laura Alber from the recent call:

So you can clearly see, even by looking at the net comps, how strong Pottery Barn was. They've really been outperforming. The rest of the brands are kind of in a similar range. But remember, you got to look at more than just one year. So when you look at West Elm on a three-year, it's really, really strong and not as far off as you might think.

So, in terms of what we see in the demos, it's really -- I'm careful not to draw any big conclusions from it because the data is very sensitive. It looks like the only thing we can see is lower income being more affected. We don't see necessarily an age issue. We just see lower income being more hurt than higher income, which is consistent with what you'd probably expect out there. The good news is, in total, our core customer is pretty affluent. And we also know that a lot of this is just uncertainty because there's really nothing that's happened. They still have a lot of home appreciation, and we have more savings than they did before the pandemic. And so, depending on what happens with the macro, this could be short. But if the macro gets worse and wage loss happens, and the Fed continues to do what they are tasked to do, which is to stop growth, it could impact those customers more than it even has already. And so, that's the reason we've been hesitant to give guidance out into '24. It's not that we're not confident in our business, it's that it's really hard to tell what's going to happen in the macro. If that was even just going to be as it is today, we would predict it. But it's changing so rapidly.

If you don't typically read earnings transcripts for the companies you invest in, you'll miss out on some of my favorite exchanges, like the one below:

Adrienne Yih

Great. Thank you very much. Good afternoon, everybody. I'm sorry if I missed this, but…

Laura Alber

Hi.

Adrienne Yih

Hi. How are you?

Laura Alber

Good. How are you?

Looking a little deeper, inventories were up pretty significantly from last year, but the last 2 years of supply chain mayhem have likely lead to a slow normalization for the company. Management discussed an order backlog and difficulties with getting multi-line (across more than one brand) to the right place as they right-size their inventory. This is something to keep an eye on moving into next year.

{kind=link}

Looking at growth vectors for the company, there is plenty to be excited about. WSM is expanding its company-owned stores into Canada. Based on Target's (NYSE: TGT ) past issues, this definitely bears watching, but it's likely the easiest market to tack on to the company's US operations.

Separately, the company is partnered with India-based Reliance Group and has opened franchise Pottery Barn and West Elm stores in Mumbai and New Delhi. It's difficult to overstate the opportunity India represents. The sheer population and growing middle class would be a boon to the company if it's able to penetrate the market in any meaningful way. I like to see the partnership with a local conglomerate. It's unlikely WSM could make the juice worth the squeeze to attempt crossing cultural barriers themselves. This bears watching as a small segment of the business now, but one that could pay off in the long run.

Lastly, the business to business segment has made some solid strides. Its growth is impressive, and most recently partnered with Starbucks (NYSE: SBUX ) to furnish the company's flagship Empire State Building roastery. Some additional perspective from the call:

A key B2B customer of ours for over three years now is Starbucks. We are thrilled to publicly announce that our team was able to assist Starbucks with the build-out of their gorgeous three-storey flagship reserve store in the Empire State Building. In addition to incorporating furniture from Brooklyn-based West Elm, our B2B team had the opportunity to work with Starbucks to create custom furniture solutions to meet their unique needs. We look forward to growing our existing relationship with Starbucks.

As SBUX revamps its locations, it could lead to meaningful revenue for WSM if its furnishings are used. I'd look for additional partnerships moving forward, as the company looks to ink deals with major hotel and restaurant brands for what could be a management-projected $80B TAM opportunity. Revenues in this segment currently project to be about $1B this year.

Looking at SG&A expense to revenue, the company is riding the correct trendline I'd look for of flat to down over time. This shows the company is growing effectively with an eye to keeping its expenses in line. ~25-27% is a good figure to see over the longer term for the company.

WSM carries no debt, and continues to drive meaningful and growing free cash flow. The dividend is sitting at a generous 2.46%, well covered, and with zero liquidity concerns. Management has committed to returning free cash flow to shareholders via dividend hikes and share buybacks.

{kind=link}

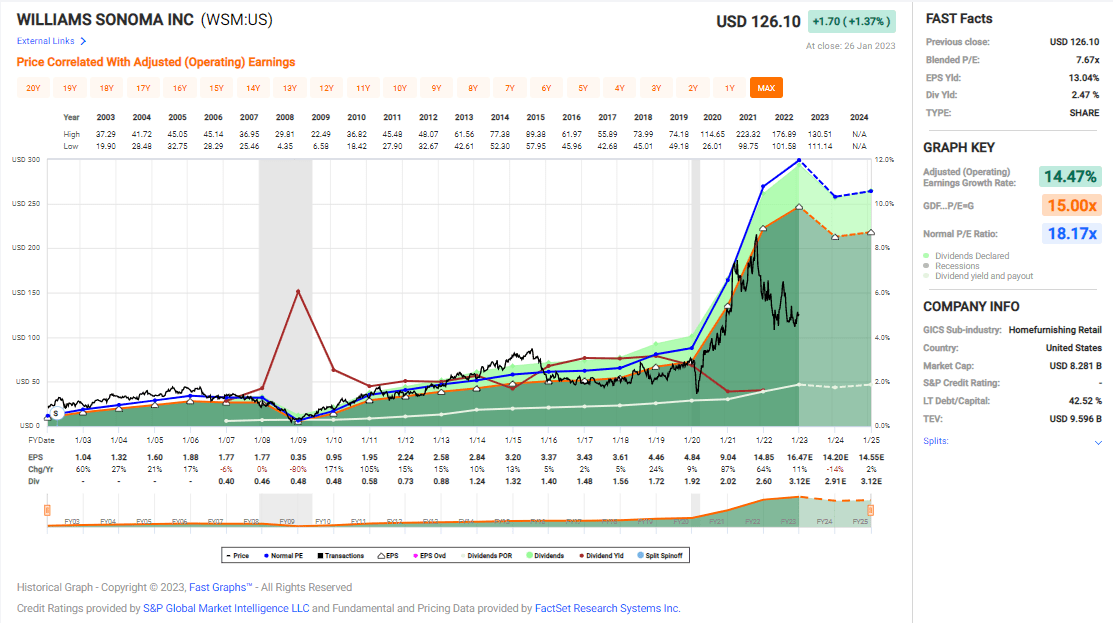

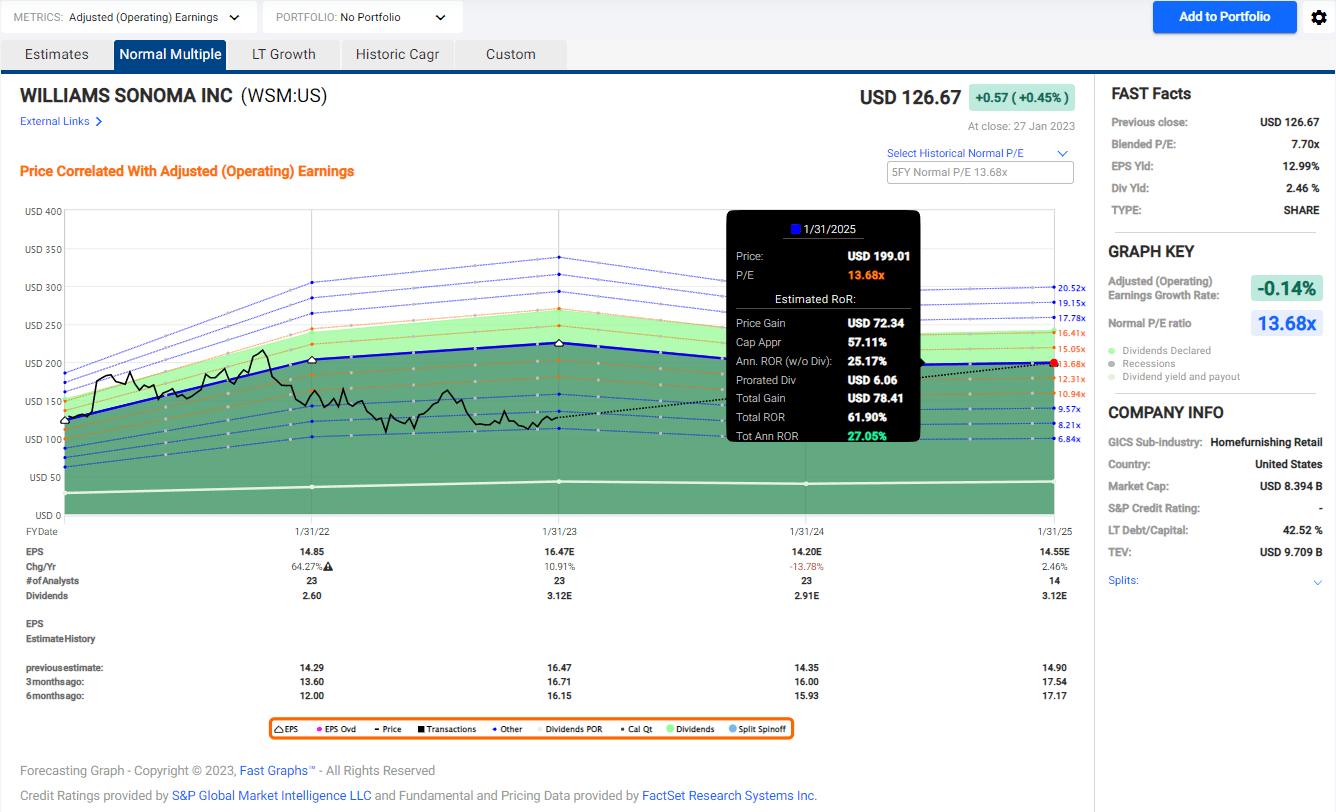

Looking at valuation over time, it's pretty obvious when the company embraced the omni-channel. Earnings shot up like a rocket, and are now growing in the low double digit range. Supply chain pressures and economic climate may pose short-term risks, but the company's share price is well in-line with earnings, and priced at about 13-14X.

{kind=link}

Based on analyst estimates, a return to the company's long-term valuation could yield an annualized rate of return of 27%. That number isn't a projection, but it can show relative valuation against likely earnings outcomes.

Based on management performance, strong capital allocation, a pristine balance sheet, and a truly impressive shift to omni-channel, WSM remains one of my top retail stocks to continue beating the market. Every time I dive in to the company's reports, I come away with few things to worry about other than self-inflicted wounds that allow competitors to claw away market share. It's important to keep an eye on the company's growth initiatives I discussed above, returns on invested capital, and revenue growth across the segments. That being said, I'm rating WSM as a buy. As always, do your own due diligence.

For further details see:

Williams-Sonoma: A True Retail Market Beater