AL - Willis Lease Finance: Attractive Business With Huge Potential

2023-11-07 10:34:54 ET

Summary

- Willis Lease Finance Corporation has shown higher returns than the general market, with a 3.2% appreciation in stock.

- The company's exposure to aircraft engines, which have high residual value, makes it an appealing investment.

- The stock has significant upside based on EV/EBITDA valuation.

In September 2023, I commenced coverage for Willis Lease Finance Corporation ( WLFC ) and I marked shares of the engine lessor and management specialist a buy. Though not huge (yet), the stock has shown returns higher than what the general markets were able to generate with a 3.2% appreciation for WLFC stock versus a slightly negative market return. In this report, I will be discussing the most recent results and revisit my price target for the stock.

Why Willis Lease Finance Might Be Interesting For Investment

The reason why I like Willes Lease Finance is specifically their exposure to aircraft engines. I consider commercial airplanes to have a very appealing value retention profile, and that is one of the reasons why I am also bullish on names such as AerCap Holdings N.V. ( AER ) and Air Lease Corporation (AL). Generally, at the end-of-life of an airplane, meaning airframe plus engines, the engines are the components with the highest residual value. So, if you consider airplanes to have a strong value retention, engines in a relative sense do even better. That is not only driven by the complex propulsive technology and components, but also because the life-limited parts that need to be changed after certain intervals or hours have price escalations in excess of CPI. Whether above CPI escalations are sustainable will depend on how airplane pricing develops, because at some point the value locked in the engines could limit the overall economic life of the airplane.

Willis Lease Finance provides services to keep airplanes flying as engines initially installed under the wings of an airplane come off the wing for shop visits. Airlines can, of course, also acquire their own spare engines to rotate airplanes back to service faster, but generally we are seeing trends where airlines are more inclined to use aftermarket sales solutions from specials than having to carry and account for a pool of spare engines to keep airplanes in service. Furthermore, the company provides end-of-life solutions, spare parts, engine financing, aircraft maintenance and activities related to aircraft redelivery and transition supporting airlines and lessors to redeliver airplanes to lessors at the required state and prepare them for service for the next lessee.

In the current supply chain-constrained environment from OEM side but also the constraints on MRO capacity, lease extensions provide a positive background for airplane values as well as the engines used on those airplanes. So, I would say that the current environment is certainly a positive for Willis Lease Finance.

What I Like A Bit Less About Willis Lease Finance

While I certainly do like the exposure to commercial airplane engines, there are also elements that I am less thrilled about. The most prominent one is that management does not host earnings calls or provide detailed breakdowns of their engine exposure, nor are there discussions, for instance, during conferences about their business. So, it is a difficult business to analyze and perhaps an even more complex business to invest in. I would have loved to hear management comment on how the current issues with the Pratt & Whitney GTF are affecting the company, not just from engine value retention perspective but more so from direct customer demands for GTF-powered operators and whether the current supply chain constraints are also putting a pressure on delivery of new engines to Willis Lease Finance and whether the company has the capacity to support an acceleration in shop visits.

Willis Lease Finance Revenue Growth Outpaces Cost Growth

{kind=link}

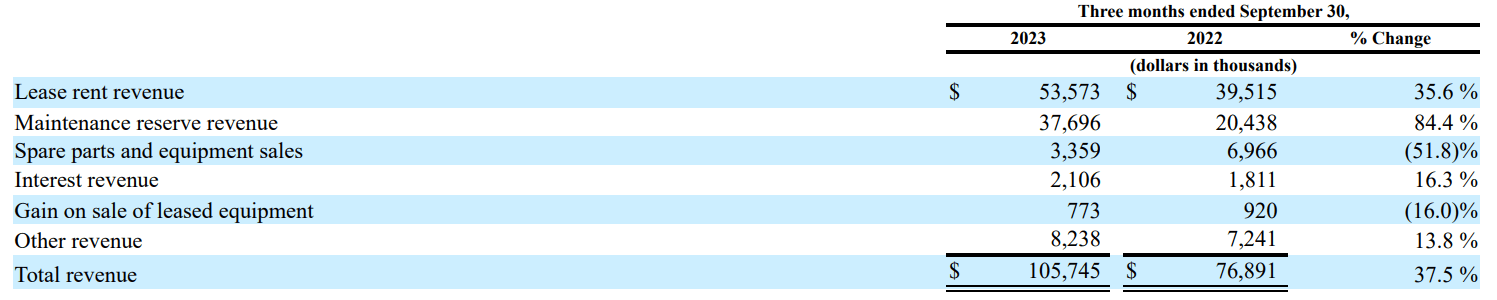

The third quarter showed a 37.5% increase in revenues from $76.9 million to $105.7 million. While spare parts and equipment sales might seem like a huge opportunity given the nature of price escalation of spare parts, it is not a big business for Willis Lease Finance with a lot of variability year-over-year and quarter over quarter. The biggest driver of growth was the 35.6% growth in lease rent revenues driven by more engines placed on lease and better utilization and the higher maintenance reserve revenues driven by short-term leases which include maintenance reserve revenues charged by flight hour.

{kind=link}

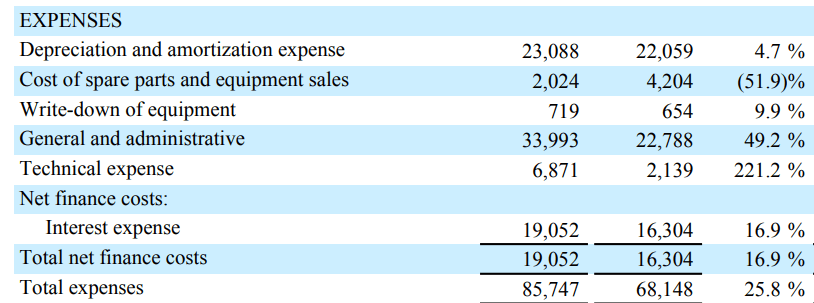

What I do like about lessors is not just the underlying value of the leased equipment, but also the scalability of the business. Costs increased by 25.8% indicating that there was a margin expansion as revenue growth exceeded cost growth despite higher depreciation and amortization, higher interest costs, and higher technical expenses and general and administrative expenses. With the exception for the cost of spare parts and equipment sales, costs rose across the board, but not enough to weaken margins leading to a nearly 150% rise in net income attributable to shareholders.

What Is Willis Lease Finance Stock Worth According To Book Value Principles?

| Valuation Willis Lease Finance |

| Shareholder's equity in $ millions |

| $ 431.93 |

| Shareholder's equity attributable to preferred shareholders in $ millions |

| 50 |

| Common shareholder's equity in $ millions |

| $ 381.93 |

| Common shares outstanding in millions |

| 6.45 |

| Book value per share |

| $ 59.25 |

| Implied share price (5-year price-to-book) |

| $ 37.86 |

| Upside |

| -16% |

| Implied share price (5-year price-to-book (pre-pandemic)) |

| $ 43.34 |

| Upside |

| -4% |

| Implied share price (median) |

| $ 43.85 |

| Upside |

| -3% |

Using the shareholder's equity corrected for the preferred shareholder's redemption value, the common shareholder's equity is around $382 million which boils down to a book value per diluted share of $59.25 implying 30% upside from current levels. Alternatively and possibly more appropriate, one could apply the price-to-book value multipliers. The 5-year price-to-book value would imply the stock is currently overvalued by around 16% while the 5-year figure pre-pandemic would suggest a 4% overvaluation and the long-term median would imply 3% overvaluation. So, with typical price-to-book values in mind, I would say that the stock is fairly valued.

What Is Willis Lease Finance Stock Worth According EV/EBITDA Valuations?

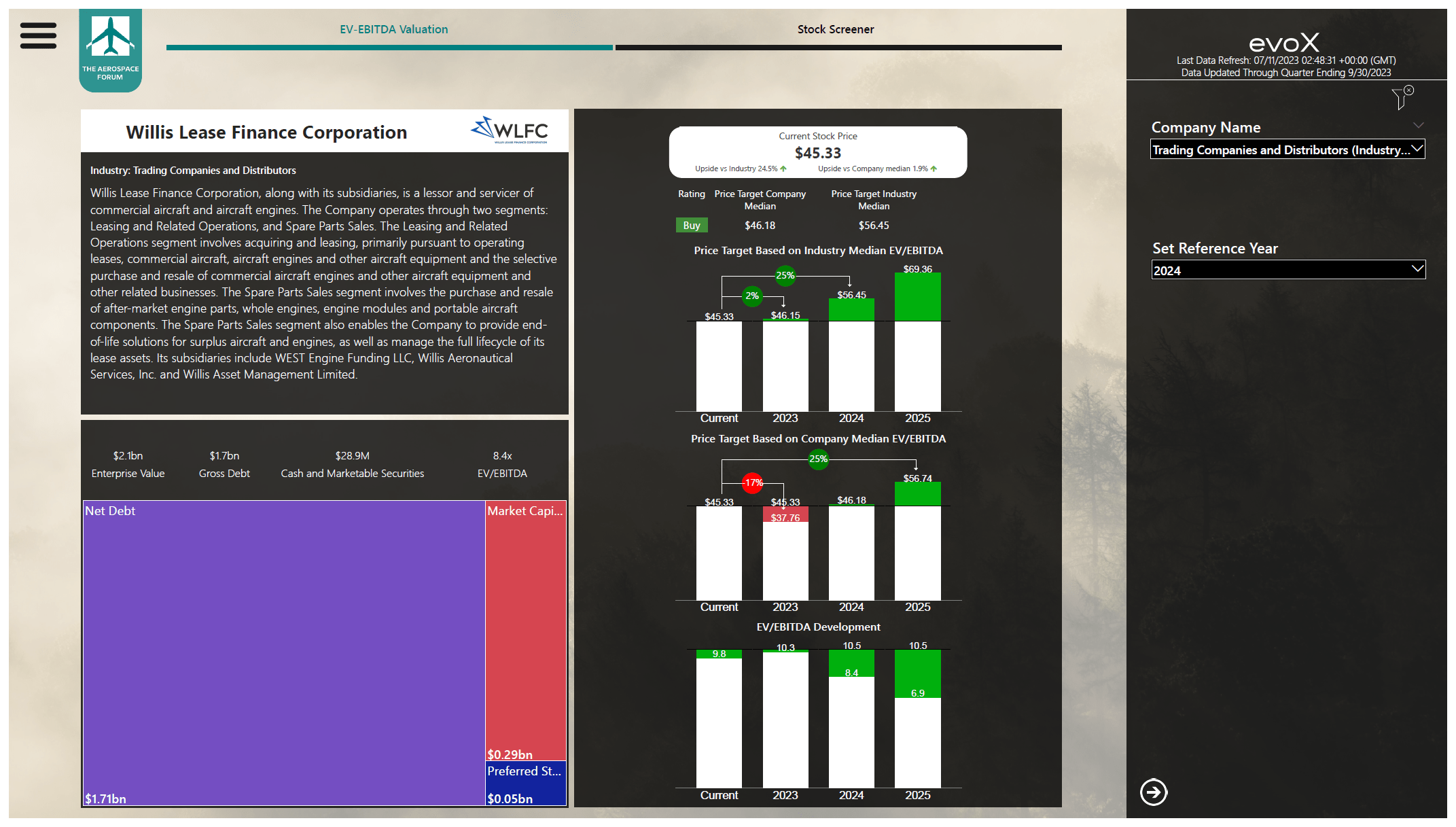

{kind=link}

I previously put a buy rating on Willis Lease Finance stock, and the most recent processing of balance sheet data and forward estimates, made me increase my price target to $56.50 implying an attractive 25% upside. Using the company EV/EBITDA targeted multiple, the company is somewhat undervalued with 2023 projected earnings in mind and has 25% upside for next year. With the year nearing its conclusion in less than two months, I think factoring 2024 earnings into the stock price is appropriate. The company EV/EBITDA median more or less suggests the same, but with a one-year shift in the targets. So, while the book value adjusted by a multiplier does indicate slight overvaluation, I believe the forward earnings do provide a solid base for a Buy rating.

Conclusion: Willis Lease Finance Remains Attractive

I believe that Willis Lease Finance remains highly attractive for investors. The company will likely add to its debt pile to continue financing its expansion, but that is inherent to the cash-intensive leasing business for airplanes and airplane components, and likely that is not just limited to airplanes or parts but just a consequential requirement for acquiring long-life assets. Engines have an appreciable value retention profile, so combined with continued expansion and MRO activity increasing in the coming years driven by longer-term timing of shop visits and a combination of the current market environment including the PW1000G turbofan issues and shortage of airplanes, I do believe that Willis Lease Finance provides a highly compelling investment opportunity and that is without factoring any upside based on a possible take-over scenario as we have seen in the past.

For further details see:

Willis Lease Finance: Attractive Business With Huge Potential