WTW - Willis Towers Watson: Pricey For What Seems Like Poor Performance

2023-08-06 01:44:03 ET

Summary

- Willis Towers Watson's valuation is high compared to the sector average, leading to a decline in share price.

- The company's Q2 results showed declining margins despite a rising interest rate environment.

- The high price and unimpressive dividend yield make it a risky investment, leading to a sell rating.

Introduction

Willis Towers Watson ( WTW ) has seen its valuation go far above the sector's average and now sits at an FWD p/e of 15. For the financial sector, this is very high and it seems the market is noticing some of this premium is undeserved. The share price plummeted following the last report . YTD the share price is down around 13% despite other major financial institutions like JPMorgan Chase & Co ( JPM ) having seen solid returns so far into 2023. The very recent report from WTW showed declining margins despite a rising interest rate environment which, generally speaking, is beneficial to companies in the financial sector.

The price of WTW is too high for a buy case right now and with a not very impressive dividend yield there seems to be little in the way of investor value here right now. The only positive point from Q2 was the top line growing but all else seemed to show a YoY decline and that doesn't support a buy case here at all. I find there to be a significant downside risk here if coming quarters show similar results and a return to a p/e of around 9 - 10 might be likely. That indicates a target price of around $133, or over 30% less than today's prices. This is adequate to make a sell rating here possible, unfortunately.

Company Structure

WTW has a very rich history that dates back to 1828 and since then the valuation of the business has grown substantially and sits at over $21 billion today. The company is a part of the insurance brokers' industry and has its headquarters in the UK.

Operations revolve around advisory, broking , and providing company solutions to an international customer base. Within WTW two segments make up the company structure. These are Health, Wealth and Career, and Risk & Broking.

Specializing in strategy and design consulting, WTW has built up a solid reputation in the market and this has helped them make strategic customer acquisitions over the years.

{kind=link}

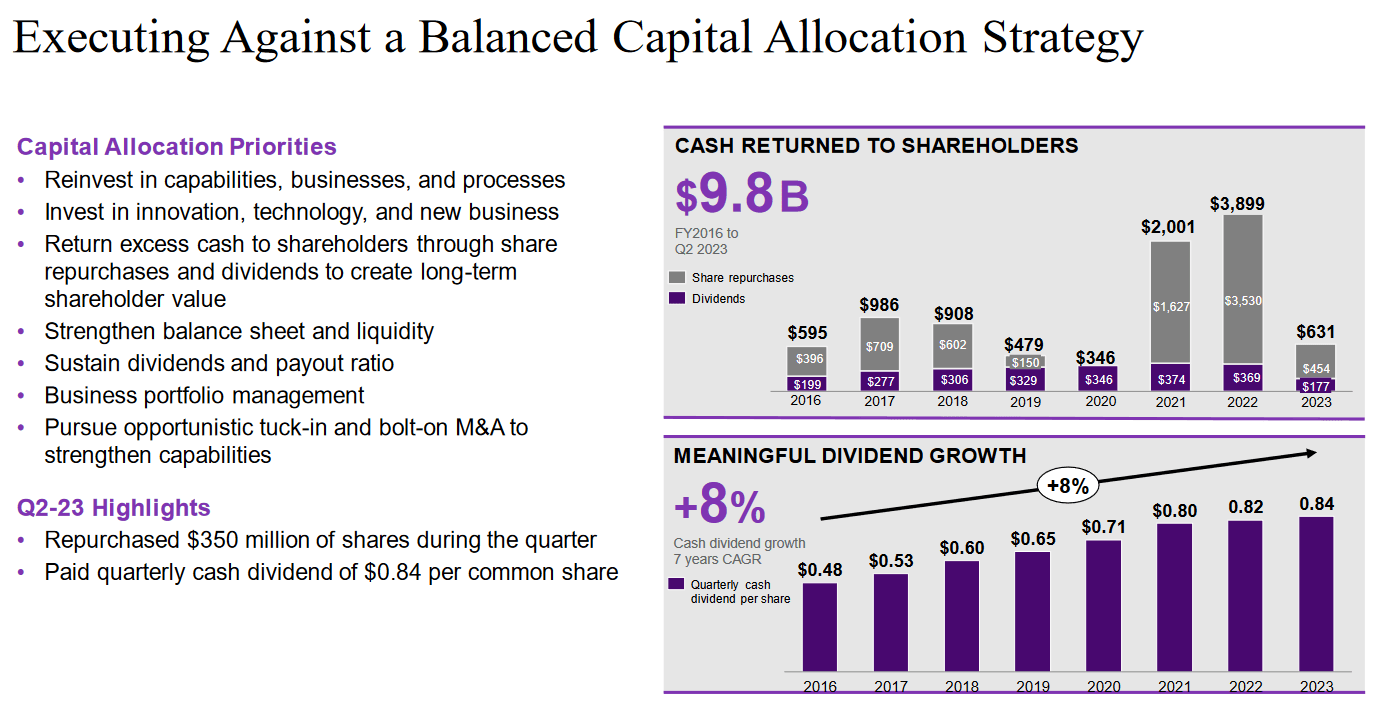

These days it seems that a lot of the priority of the management lies in returning large amounts of capital to shareholders through both dividends and buybacks. But given the high price you have to pay for WTW today, the yield is not that impressive. Besides, it seems like a poor capital allocation strategy to be repurchasing shares when the valuation is so high, and recent reports show struggling margin retention. During Q2 WTW spent $350 million in repurchases, which of course benefits shareholders, but I can't help to think that spending should have been delayed until a better buying opportunity appears. I don’t like it when I see overspending on share repurchases just to appease investors, which seems to be the case here.

Earnings Transcript

The last couple of weeks have been volatile for the share price of WTW. Following the report, the share price dropped from $232 to around $209. Looking at some comments from the earnings call there are some reasons for this drop I think. The CEO Carl Hess said the following.

-

“We faced margin headwinds from those investments as well as wage inflation in prior year book sales that limited our progress on driving margin expansion and earnings growth this quarter. The continued success of our transformation program, which exceeded our expectations yet again partially offset these headwinds. All in all, adjusted operating margin declined by 90 basis points for the quarter, which resulted in adjusted earnings per share of $2.05. Though we had a decline in adjusted operating margin this quarter, as we've said before, our progress in margin expansion won't always be linear. However, we don't expect margin declines in any full year period”.

This comment highlights the fact that WTW is still experiencing some of the impacts of inflation, especially as the UK inflation rate remains quite high. This is creating headwinds for WTW but as the CEO also mentioned, they don’t expect to see margin declines in FY2023 compared to FY2022. For me, it still doesn't seem certain and if WTW disappoints on that front I think we are heading to a p/e of 9 quite quickly.

Valuation & Comparison

GGM Model (Author)

Looking above here at my GGM model for WTW showcases the fact that buying right now seems to offer little in the shape of a strong return. The price is still a fair bit above where a 10% return would be achievable. I think that the dividend will continue to increase at a decent rate given that WTW is so shareholder-friendly and I think they can give up that front at all. With a target price of $164 for 2023 WTW remains too pricey for my liking and needs to drop a lot to get to where I want it. That also means that investors holding shares are introduced to some risk and that right now is too high to form a hold case around.

Risk Associated

Navigating the landscape of the sector poses significant challenges, and one of the most prominent concerns arises from macroeconomic risks. These external factors, including economic fluctuations, geopolitical tensions, and changes in government policies, can exert substantial pressure on short-term prices, creating uncertainties that may dampen overall demand.

{kind=link}

The volatile nature of the sector is underscored by the interplay of market dynamics and macroeconomic conditions. Fluctuations in global commodity prices, supply chain disruptions, and trade tensions can influence the sector's profitability and investment climate. As companies strive to maintain growth and profitability in such an environment, they must adopt agile strategies to adapt swiftly to market changes and capitalize on emerging opportunities.

Investor Takeaway

WTW has had some struggling couple of quarters and the margin contraction for Q2 FY2023 resulted in the share price dropping quite quickly. This has introduced a lot of risk with WTW right now, I think. The company seems vulnerable to wage inflation given its broad operations and it has impacted margins. Besides this, the p/e is at 15 which is far above the sector's multiples. I think we are likely to head far lower if Q3 and Q4 show the trend of margin contraction continuing. I don’t see a strong catalyst in sight to make the valuation make sense. All this concludes me rating WTW stock as a sell right now, unfortunately.

For further details see:

Willis Towers Watson: Pricey For What Seems Like Poor Performance