WRB - Willis Towers Watson: Secular Tailwinds Manifest In A Strong Q3

2023-10-26 11:47:02 ET

Summary

- Shares of Willis Towers Watson Public Limited Company rose 9% after a strong earnings report, driven by secular tailwinds, cash generation, and reasonable valuation.

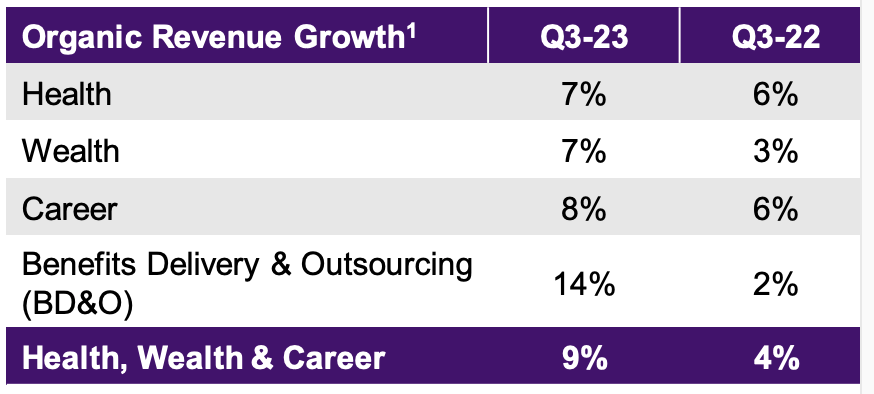

- The company's Health, Wealth, and Career unit saw 9% growth and expanded margins, with strong demand for health insurance services and retirement consulting.

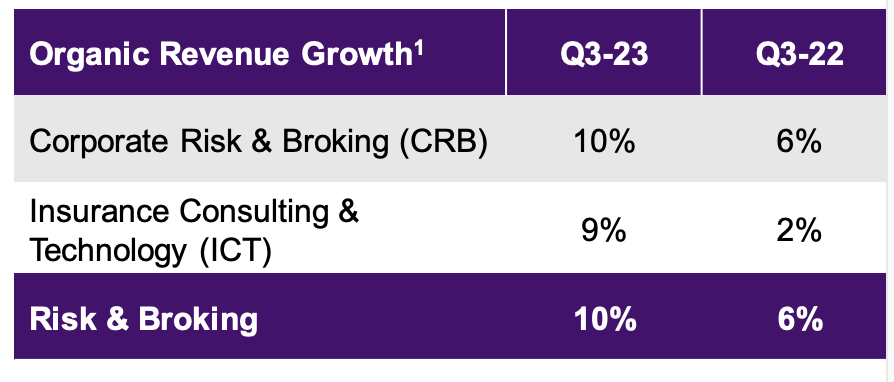

- Willis Tower Watson's Risk & Brokering unit had 10% revenue growth, benefiting from higher client retention and rising premium rates in the insurance industry.

- Its cost savings program is improving cash flow, and at 14x 2024 earnings, Willis shares are attractive.

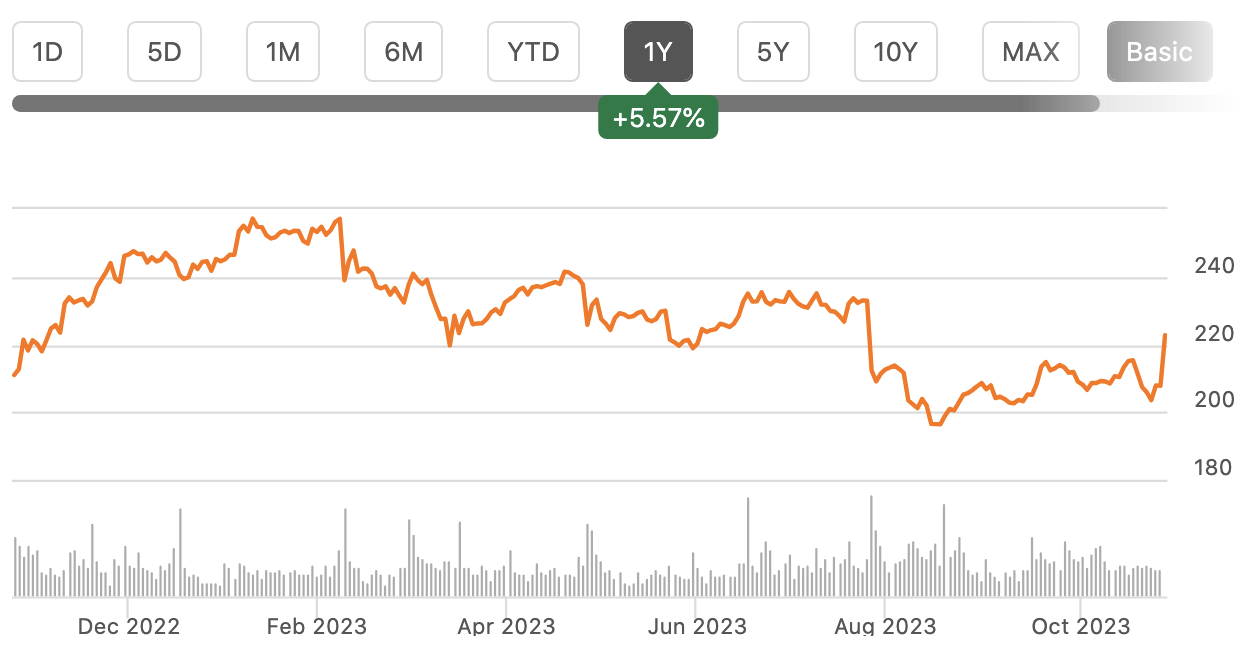

Shares of Willis Towers Watson Public Limited Company ( WTW ) have been a mixed performer over the past year, trading essentially flat even as the broader market has rallied. However, shares popped about 9% on Thursday morning in response to a strong Q3 earnings report . Its business has some secular tailwinds, is increasingly cash generative, and has a reasonable valuation. I see further upside.

{kind=link}

In the company’s third quarter , Willis earned $2.24 in adjusted EPS, beating estimates by $0.20 as revenue came in at $2.2 billion, rising 9% on an organic basis. Adjusted EPS rose by 2% from last year; there were $0.24 of year over year tax headwinds which is why EPS growth was slower than revenue growth. Excluding tax, earnings were up about 13%. WTW delivered 170bp of operating margin expansion to 16.2% as its transformation program has resulted in $300 million of cost savings to date.

WTW is an insurance broker and consulting firm. As such, by and large it does not take on risks like an American International Group ( AIG ) or Chubb (CB), and it does or manage client money like BlackRock (BLK); rather it helps clients pick the right insurer or asset manager for their needs, collecting a fee for this service. Its primary competitor is Marsh & McLennan Companies, Inc. (MMC). Right now, the business is performing quite strongly, and there are tailwinds that make this likely to continue.

Its Health, Wealth, and Career ((HWC)) unit generated 9% growth to $1.28 billion with outsourcing particularly strong. Margins expanded 350bp thanks to cost cuts and increased operating leverage. Operating income rose 29% thanks to this margin expansion. As you can see below, growth was broad-based, accelerating across the board from last year. BD&O continues to win client, in particular with strength for life insurance services.

{kind=link}

These sub-units provide a range of services that have several tailwinds. Its health unit helps companies determine what benefits to provide employees, brokering agreements with health insurers like UnitedHealth ( UNH ) or Cigna (CI). With health insurance increasingly expensive and benefits an important way to compensate and retain employees, these services help business optimize costs and ensure their plans are competitive with peers.

Wealth provides consulting services to retirement plans. Pension plans and company 401(k) plans have fiduciary responsibilities to their plan participants, meaning they must act in their interest when determining what investments to offer or how to allocate assets. Many companies rely on consultants to choose managers, ensuring expertise and impartiality in selecting managers to meet this legal obligation. This unit saw new client flows, and because its fees can be tied to asset levels, it benefited from higher market levels.

With an aging population across the developing world, retirement services should see ongoing demand strength. Its career unit works on executive compensation, which is an increasingly hot button issue. It also provides surveys and data on pay transparency. With companies increasingly focused on issues like pay parity between men and women, these surveys and data are seeing strong demand. I would expect that tailwind to persist. While this is the smallest category at 12% of HWC revenue, I see particular growth opportunities here.

WTW’s other unit is Risk & Brokering, and it had 10% revenue growth to $855 million. About 89% of the business comes from insurance brokerage. Here, medium and large companies hire Willis to find the best insurer for their needs. Big enough companies can craft specially-written polices to cover their exact needs, and Willis assists in determining the right policies to seek as well as finding the best insurance rate for their needs. Willis is seeing higher client retention, which has boosted revenue. Moreover, its fees are generally tied to the cost of the insurance policies, capturing a portion of the insurer’s economics. So far this earnings season, a constant theme for insurers has been rising premium rates as insurers recapture pricing after lagging inflation in recent years. Chubb , W. R. Berkley (WRB), and others have said this. These higher premiums mechanistically translate to stronger revenue levels for WTW. This should continue to be a tailwind through 2024.

Alongside these services to companies seeking insurance, Willis has technology and consulting services for insurance companies themselves to assist in their actuarial modeling, client management, etc. This unit is seeing increased software sales, which should drive ongoing, high-margin revenue through next year. This combination of revenue tailwinds and cost control meant that R&B’s operating margins expanded 200bp to 15.7%.

{kind=link}

While WTW is categorized as a “financial” company, it is really more of a services company to the financial industry and products. It is benefitting from secular tailwinds and higher pricing, helping to drive substantial revenue and profit growth. WTW has generated $707 million of free cash flow year to date, more than double last year. It also reaffirmed guidance for mid-single digit organic revenue growth with a 12% free cash flow margin from 8% last year even as it spends $150 million to deliver cost savings. It has a long-term goal of 16% free cash flow margins. It will be at 14% just by not having to spend more on its cost savings program next year.

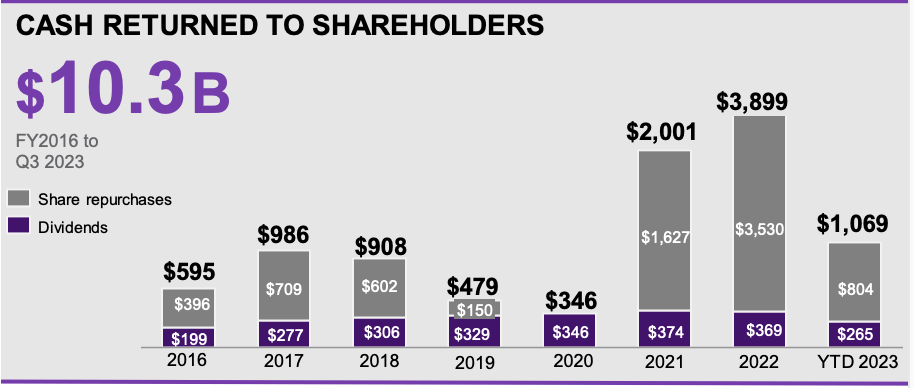

With strong cash flow, WTW has been steadily returning cash to shareholders, including a $350 million buyback last quarter. In September , the board authorized an open-ended $1 billion share repurchase program, which could reduce the share count by 4-5% over time. Over the past year, its share count has fallen over 5%. WTW has $1.25 billion of cash on hand, essentially flat this year while it carries just $5.2 billion of debt for 2.2x debt to EBITDA leverage. This solid balance sheet will enable WTW to continue to direct free cash flow to shareholders.

{kind=link}

Alongside this quarter, management stated a target of $10 billion in revenue next year and $15.4-17 in EPS. Based on this, WTW should be able to generate about $1.35-1.4 billion in 2024 free cash flow, enough to essentially complete its $1 billion buyback authorization while also paying its dividend. Given the growth we are seeing, I view these targets as reasonable.

Even after its strong rally Thursday morning, Willis shares are just 14x 2024 earnings with a 6%+ free cash flow yield. For a company with very little economic sensitivity (after all, companies still need insurance, to offer benefits, and have investment options in 401(k) plans in a recession) that is seeing strong growth, and which is increasingly generating free cash flow due to its cost program, this is an attractive valuation. If anything, the legal, insurance, and benefits landscape are growing more complex, increasing demand for its services

In my view, WTW will be a high-single digit growth company for several years as it benefits from these tailwinds, allowing it to meaningfully reduce share count and grow EPS at a double-digit pace. It also has limited cyclical risk given the nondiscretionary nature of many of its services. I can see shares rising to a 16x multiple or $264, providing over 15% of upside.

At that level, Willis Towers Watson Public Limited Company shares would have a 5% free cash flow yield, which I view as appropriate as WTW is well positioned to grow free cash flow at least 5%/year over the medium term, providing a 10% ongoing return potential. WTW shares are finally starting to perform after a quiet 12 months, and it is not too late to buy.

For further details see:

Willis Towers Watson: Secular Tailwinds Manifest In A Strong Q3