WTW - Willis Towers Watson: Slightly Overvalued Needs To Prove Itself

2023-05-03 20:35:57 ET

Summary

- I wanted to take a look at the company’s prospects in the future while looking at the broader sector outlook.

- The company may benefit from strong sector growth if it manages to innovate and become the dominant player.

- The balance sheet is nothing to write home about; however, it seems to be somewhere in the middle of the competition.

- With no huge revenue catalysts in the near future, and with conservative margin improvements, the company is still slightly overvalued. I give a hold rating.

Investment Thesis

With somewhat improving margins and the positive sentiment about the industry in the long-term by the management, I wanted to take a look at what would be a good price to pay for Willis Towers Watson ( WTW ). I will briefly cover the sector outlook, delve deeper into the company’s financials, and come up with some reasonable growth assumptions for a 10-year DCF model to see what the company is worth to me.

The company has a positive outlook for its sectors but lacks real growth catalysts on the horizon. The only positive I see is that they can improve efficiency and profitability through margin expansions. In my opinion, WTW stock is slightly overvalued at the moment. I would wait for a slight correction during the next 6-12 months of economic volatility.

Briefly on the Company and Latest Results

WTW is an insurance broker, an advisory, and a solutions company that is based in the UK. The management recently updated the company’s reportable segments, of which there are only two now; Health, Wealth, and Career ((HWC)), and Risk and Broking ((RB)). The company provides its services to other organizations. Provides advice, data solutions, consulting services, investment management, and many other services within the insurance umbrella.

Revenue was up around 4% y-o-y, with 8% organic growth. The adjusted operating margin increased by 140bps to 18.6% from the same period last year, which suggests that the company’s initiatives are coming to fruition while adjusted EPS was up 7% at $2.84 for the quarter. Net income attributable to WTW increased 65% to $206m while adjusted net income, which includes items like Amortization, Transaction and transformation, and certain tax adjustments, was down 3% to $306m.

Looking at the ’23 outlook, the management expects to deliver mid-single-digit returns in '23 and further margin expansion from their Transformation Program and some currency headwinds of around 5 cents a share.

Overall, the numbers are decent. It is good to hear that the management is focusing on margin health in the long run as there will be further headwinds going forward as we are on a verge of a supposed recessionary period, which will weigh on companies like WTW.

Broad Sector Outlook

We have been hearing quite a lot about the upcoming recession since the end of ’22. It’s already May and we still have not seen too much happening that we haven’t seen in ’22. Inflation is still very high; the unemployment rate is still at record lows. It seems like the Fed’s plan is taking slightly longer than expected. I would like to look at the broad insurance sector outlook in ’23 and beyond to give me a sense of where the company might be headed in terms of growth.

The macroeconomic risks are the biggest challenges in the sector as they weigh on short-term prices, which will put a strain on demand. The management still expects to grow at around 5% for ’23, whereas in FY22, the company lost around 2% in revenues y-o-y. This seems like a very positive outlook because, during the last 5 years, the company has not reached over 5% y-o-y growth since jumping over 100% from '15 to '16.

Digitization in Insurtech seems to have a very positive and strong growth outlook for the next 5-10 years. With the advancement of AI tools and other technologies, this area of insurance is poised to see a 52% CAGR over the next 7 years. It is quite a small market right now, but with such growth, it'll grow to around $100b and will continue to grow the more advanced the technology gets. Another benefit of this sector is that more people are working remotely from home, which requires all kinds of protection like cybersecurity. Companies are actively switching to the cloud which in turn makes these companies much more efficient, profitable, and very scalable.

The much bigger health insurance sector is predicted to grow at around 9.5% CAGR to well over $3T by ’28. If the WTW can capture some similar growth numbers, it would do well in the long run.

It won't be easy for the company to capture numbers like these because the competition in the insurance broker space is also growing at a very decent pace, which means WTW may start to lose its competitive advantage to new brokers, or current brokers that are taking an initiative to evolve and bring something new to the table that other companies are not able to. Insurance broker and the market size is predicted to grow almost 9% CAGR by ’28. The good news is that WTW is still one of the key players.

If the company harnesses the power of technology more, in terms of adapting AI and other efficiency tech tools, it can cement itself as a leader in its sector. I see a bright future for insurance brokers, we just need to wait to see how well WTW can adapt to rapid changes in technology.

Financials

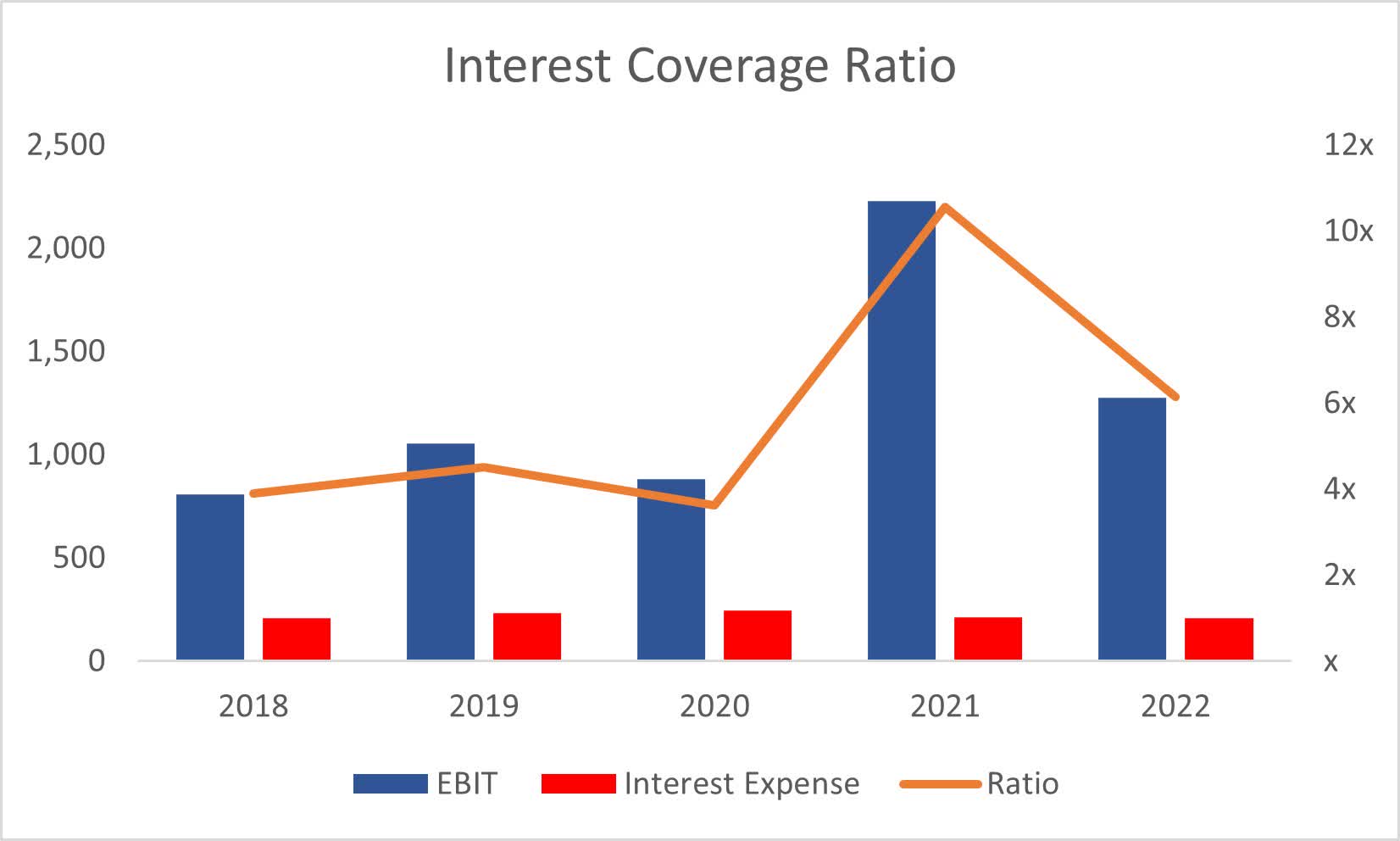

I will be focusing on full-year metrics on the graphs below as a single quarter doesn’t tell me much about the company in the long run. I will briefly mention the quarterly numbers if I think they’re relevant. The company had a little over $1.2B in cash at the end of FY22 and slightly less in Q1 ’23 ($1.13B). Long-term debt is at $4.47B, which is quite high, however, I don’t think it is an issue because the interest coverage ratio is over 6 as of FY22, which means that the company's EBIT can cover interest expenses 6 times over. This is a healthy ratio to have, although it is on my lower-end threshold.

Interest Coverage Ratio (Own Calculations)

{kind=link}

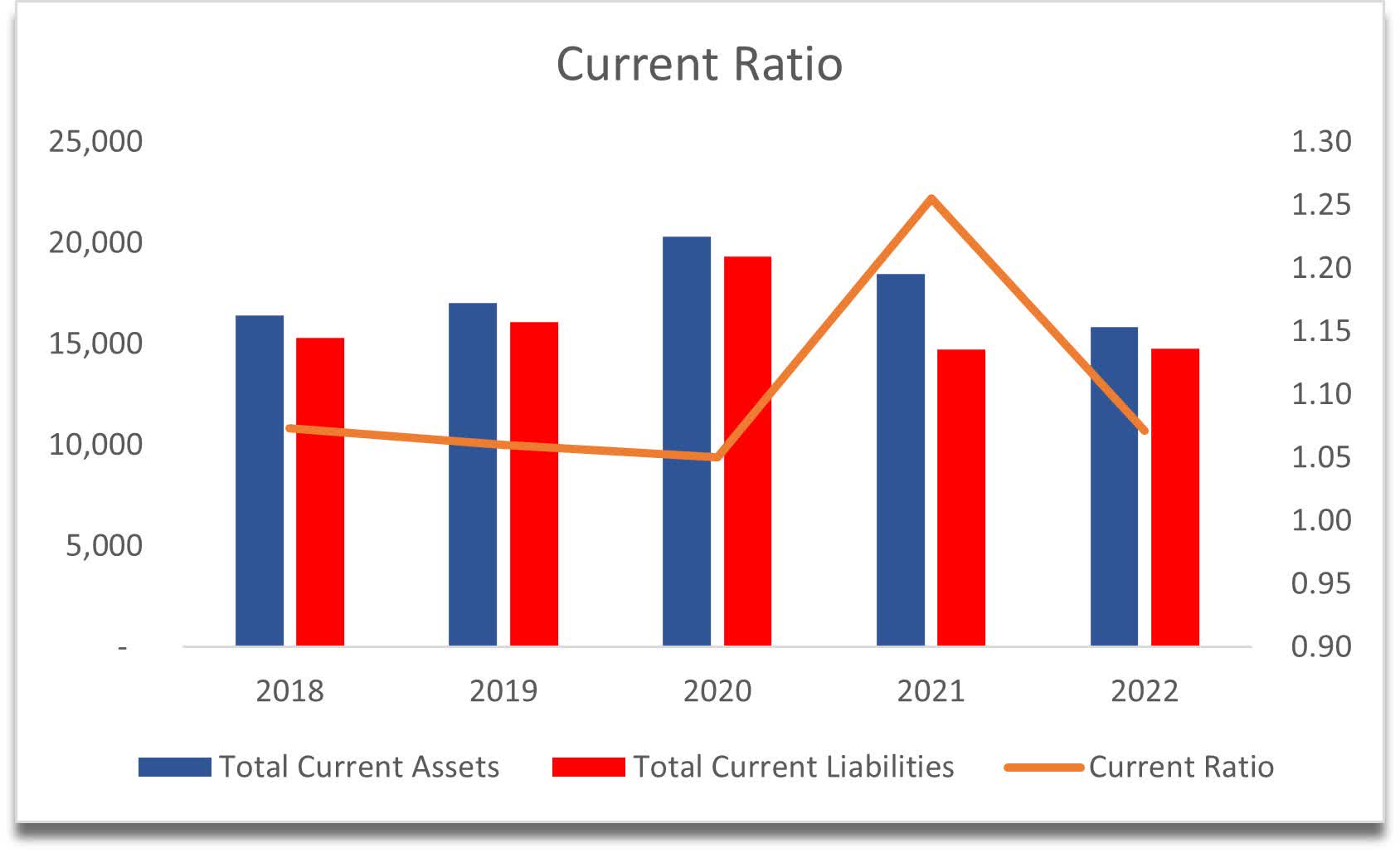

Continuing with liquidity, the company’s current ratio is just over 1 both at the end of ’22 and Q1 ‘23, which is about the minimum I’d like to see. I prefer a company to have 1.5 -2.0, which then suggests the company will not have any liquidity problems any time soon. It still doesn’t have any liquidity problems right now as it can pay off its short-term obligations, but I’d feel better with a higher ratio.

Current Ratio (Own Calculations)

{kind=link}

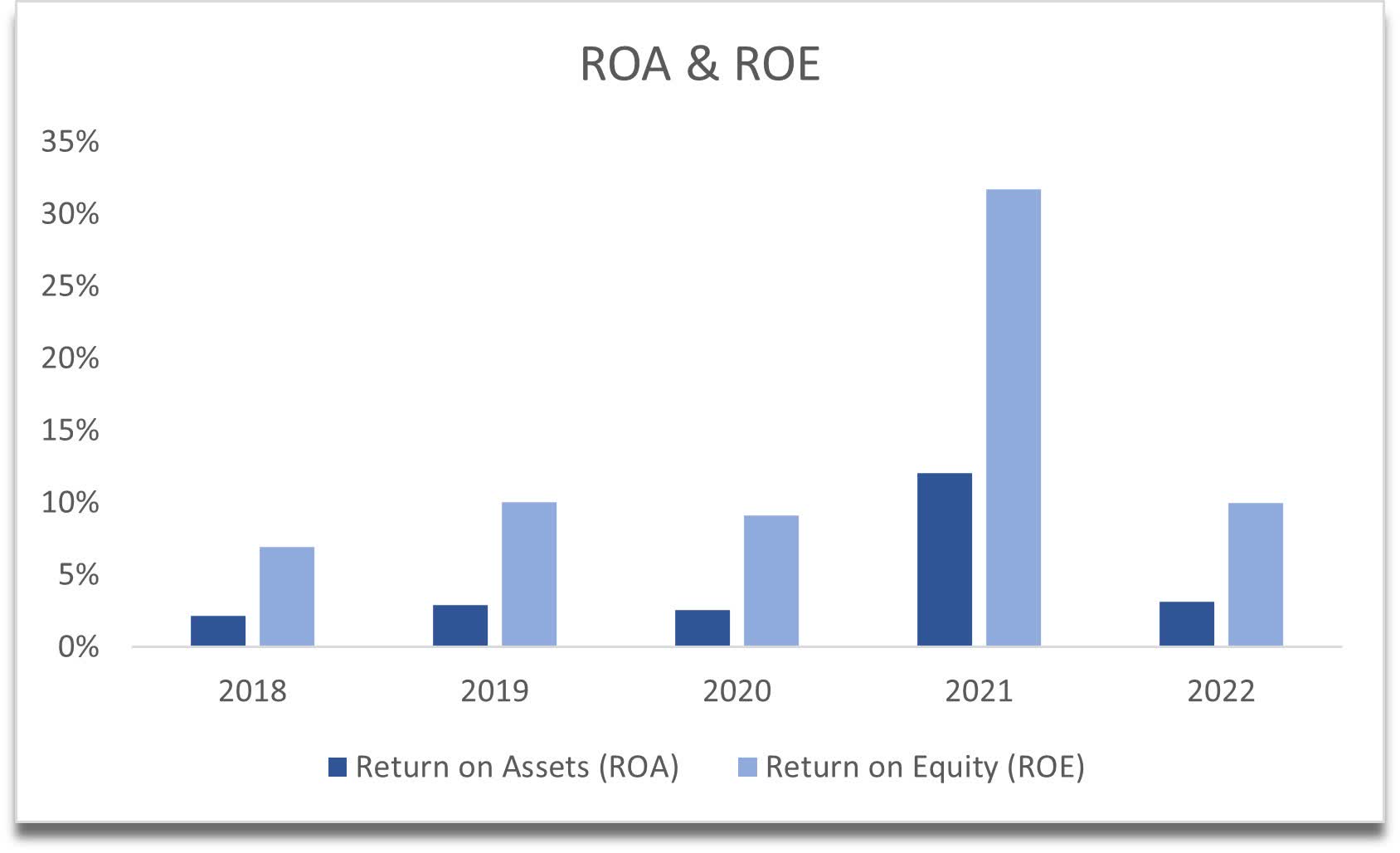

Looking at profitability and efficiency, the company is not very outstanding in these metrics either. In terms of ROA and ROE, the company has just about the minimum I would look for in a company. The management needs to find a way to be much more efficient with their assets and shareholders' capital to make for an attractive investment in my opinion.

ROA and ROE (Own Calculations)

{kind=link}

The same story can be said for return on invested capital, which has been around mid-single digits for the last 5 years. It does look slightly low, however, if we look at the competition, it is somewhere around the middle, with the bigger players in the industry ([[MMC]], [[AON]]) displaying much higher returns on capital.

Return on Capital (Seeking Alpha)

{kind=link}

Overall, the financials seem quite average, with no big warnings and nothing outstanding in a good way either. I’ve seen many better balance sheets with greater profitability and efficiency metrics.

Valuation

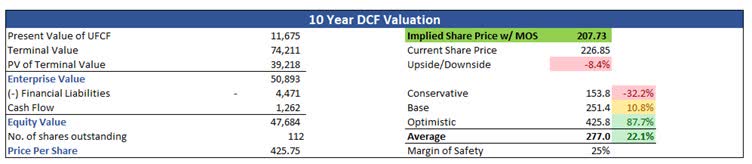

I will use a simple DCF model to calculate what I would like to pay for a company that is looking to improve its margins, that seems to have very little growth potential if the company continues chugging along as it has, and a positive outlook of the sectors in the next 5-10 years.

For growth assumptions, I decided to anchor my base case to 5% growth, which I think is even a little more optimistic, unless the company manages to land some outstanding growth catalysts in the future because, in the last 5 years, the company has seen low-mid single-digit growth. I cannot assign higher growth numbers without the company proving to us that it can achieve them somehow, and from reading the transcripts, there were no indications of such potential.

For the optimistic case, I went with 7% CAGR, and for the conservative case, 3% CAGR to give myself a range of possible outcomes.

In terms of margins, I am positive that the company can achieve better efficiency and profitability without the need for some revenue catalysts, however, I will still approach margins conservatively. Gross margins and operating margins will see a 200bps improvement over the next 10 years, which I believe is quite conservative as the company managed to improve by around 300bps in the last 5 years.

Furthermore, I would also like to add a 25% margin of safety to the intrinsic value calculation to be on the safer side even more.

With that said, and with the above growth potential and financial health of the company, I would be happy paying around $207.73, which means there is around an 8% downside from current valuations.

10-year DCF Valuation (Own Calculations)

{kind=link}

Closing Comments

I could easily see the company coming back down to around my intrinsic value and even further down, because of the volatility that is not going to go away anytime soon. This is the price I would be ok with owning the company; however, I will be more patient and see if it can go below $200 and more toward $190. At that point, I believe the risk/reward ratio is much more favorable in the long run. I have a price alert at $200 a share and will reassess once the company hits it, and if it hits it in the next year or so. My analysis may change if the company comes out with great results and some revenue catalysts that will propel its revenues. At that point, I will go back and adjust accordingly, but for now, the company is a hold in my opinion and I'd like it to come back down slightly.

For further details see:

Willis Towers Watson: Slightly Overvalued, Needs To Prove Itself