WLMIF - Wilmar International: It's Premature To Be Bullish

2023-11-28 10:22:25 ET

Summary

- Wilmar International's shares are attractively valued with its forward P/E at the lower end of its historical trading range.

- The stock has potential catalysts associated with the new central kitchens business and margin recovery, but the catalysts will likely be realized at a later time.

- It is too early to be bullish on Wilmar International stock now, so I choose to rate WLMIF as a Hold.

Elevator Pitch

I rate Wilmar International Limited ( WLMIF ) [F34:SP] stock as a Hold. This isn't the right time to have a Buy rating for Wilmar International. The company's shares are cheap, but the catalysts relating to margin recovery and central kitchens are unlikely to play out soon. This means that a Hold rating for WLMIF is justified.

Readers should note that Wilmar International's shares are traded in Singapore and on the Over-The-Counter market. The average daily trading value for Wilmar International's OTC shares for the last three months was around $30,000 (source: S&P Capital IQ ). In comparison, the company's shares listed on the Singapore Exchange boasted a higher three-month mean daily trading value of $12 million as per data taken from S&P Capital IQ . There are US brokerages which allow for dealing in Singapore-listed shares such as Interactive Brokers.

Business Profile

In its media releases , Wilmar International describes itself as a "leading agribusiness group" that boasts "over 500 manufacturing plants and an extensive distribution network covering China, India, Indonesia and some 50 other countries and regions" with "a multinational workforce of about 100,000 people."

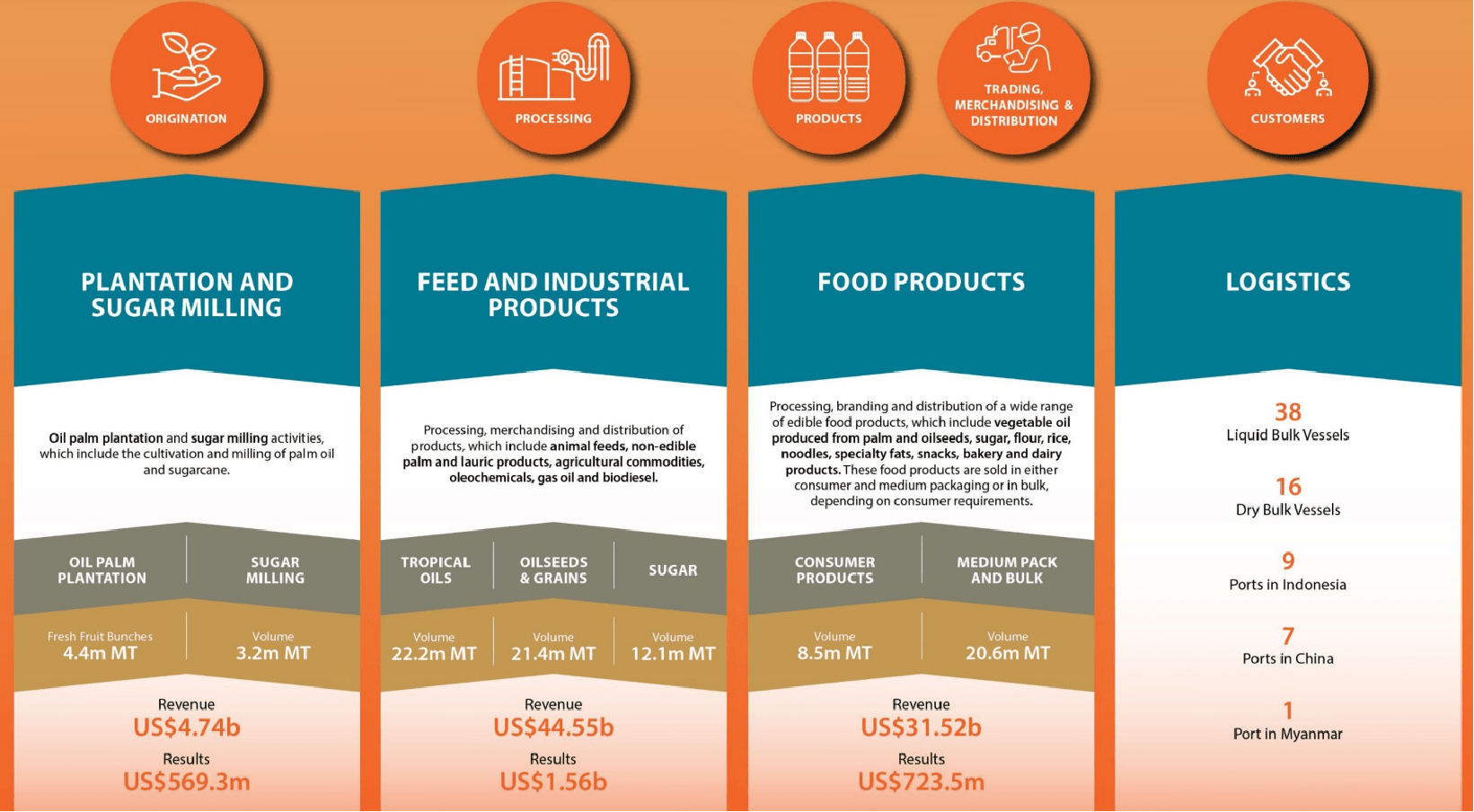

An Overview Of Wilmar International's Key Businesses

Wilmar International's 2023 Annual General Meeting Presentation Slides

{kind=link}

The company's key geographical markets are China, Southeast Asia, and Africa, which accounted for 51%, 19%, and 8% (source: S&P Capital IQ ) of its fiscal 2022 top line, respectively. None of the other geographical markets contributed more than 5% of Wilmar International's FY 2022 revenue.

Insider Buying And Valuations

Recent insider share purchases suggest that Wilmar International's current valuations are appealing.

After the company reported its Q3 2023 financial results on October 26, 2023, Wilmar International's CEO Kuok Khoon Hong engaged in a series of share purchases between end-October and mid-November. As such, Kuok Khoon Hong's interest in Wilmar International increased from 13.46% prior to the third quarter earnings release to 13.50% now. In fact, the company's CEO has been progressively acquiring shares in Wilmar International since October of last year when his equity stake at that time was much lower at 12.94% .

The insider buying for Wilmar International makes a lot of sense, when one considers the stock's valuations.

Wilmar International traded in the 8-12 times consensus forward next twelve months' normalized P/E multiple range between October 2022 and November 2023 as per S&P Capital IQ's valuation data. In contrast, the market used to value Wilmar International at between 10 times and 18 times consensus forward next twelve months' normalized P/E in the January 2018 to June 2022 time frame. The stock's consensus forward P/E ratio is 11.8 times (source: S&P Capital IQ ) now, which is at the lower end of what it used to trade at in the 2018-2022 time period.

In my view, there are two catalysts needed to spark a positive re-rating of Wilmar International's valuations. The first catalyst is profit margin improvement; and the second catalyst is building new businesses which are unaffected by commodity price volatility. I touch on these potential catalysts in the subsequent sections of this article.

Margin Recovery Will Take Time

Wilmar International's net profit margin was 1.79% for the first nine months of FY 2023. As a comparison, the company achieved relatively higher annual net profit margins of between 2.80% and 3.30% for FY 2018-2022. Similarly, the company's FY 2018-2022 EBITDA margins in the 5.94%-7.14% range were better than its actual 9M 2023 EBITDA margin of 5.33%.

The numbers presented above help to explain why Wilmar International was trading at a lower P/E multiple for the October 2022-November 2023 period as compared to the January 2018-June 2022 time frame.

There are signs suggesting that a recovery in Wilmar International's profitability to levels it achieved for 2018-2022 won't happen anytime soon.

Asian stock brokerage CGS-CIMB Securities issued a research report (not publicly available) titled "Slow Recovery In Profits, But Worst Is Over" on October 30, 2023. In this report, CGS-CIMB Securities cited the company's management commentary at the Q3 2023 results call indicating that "downtrading activities for its consumer products sub-segment in China and India in 3Q23 had somewhat impeded profit recovery."

Separately, the current consensus margin estimates for Wilmar International imply that the company's profitability won't return to prior highs in the next two years. As per S&P Capital IQ data, the consensus fiscal 2024 and fiscal 2025 EBITDA margins for WLMIF are 5.76% and 5.74%, respectively. The analysts also forecast that Wilmar International will deliver net margins of 2.46% and 2.63% for FY 2024 and FY 2025, respectively. These forward-looking margin projections for Wilmar International are still below what the company achieved between FY 2018 and FY 2022. It is also worth noting that the market's full-year FY 2023 consensus EPS forecast for Wilmar International remained unchanged at $0.22 after the company released its Q3 results on October 26.

In a nutshell, the margin recovery catalyst is less likely to be realized in the short term.

New Central Kitchen Business Will Help To Diversify Revenue And Earnings Mix In The Long Term

Another reason for Wilmar International's low P/E multiple, apart from weak profitability as detailed in the prior section, is the fact that the company is seen as a cyclical business that is affected by volatility in the prices of commodities such as palm oil.

As such, it is encouraging to see Wilmar International venture into new business areas which are less cyclical and not as susceptible to volatility in commodity prices. One key example is the company's central kitchen business in China.

The Operating Model For Wilmar International's Central Kitchen Business

Wilmar International's 2023 Annual General Meeting Presentation Slides

{kind=link}

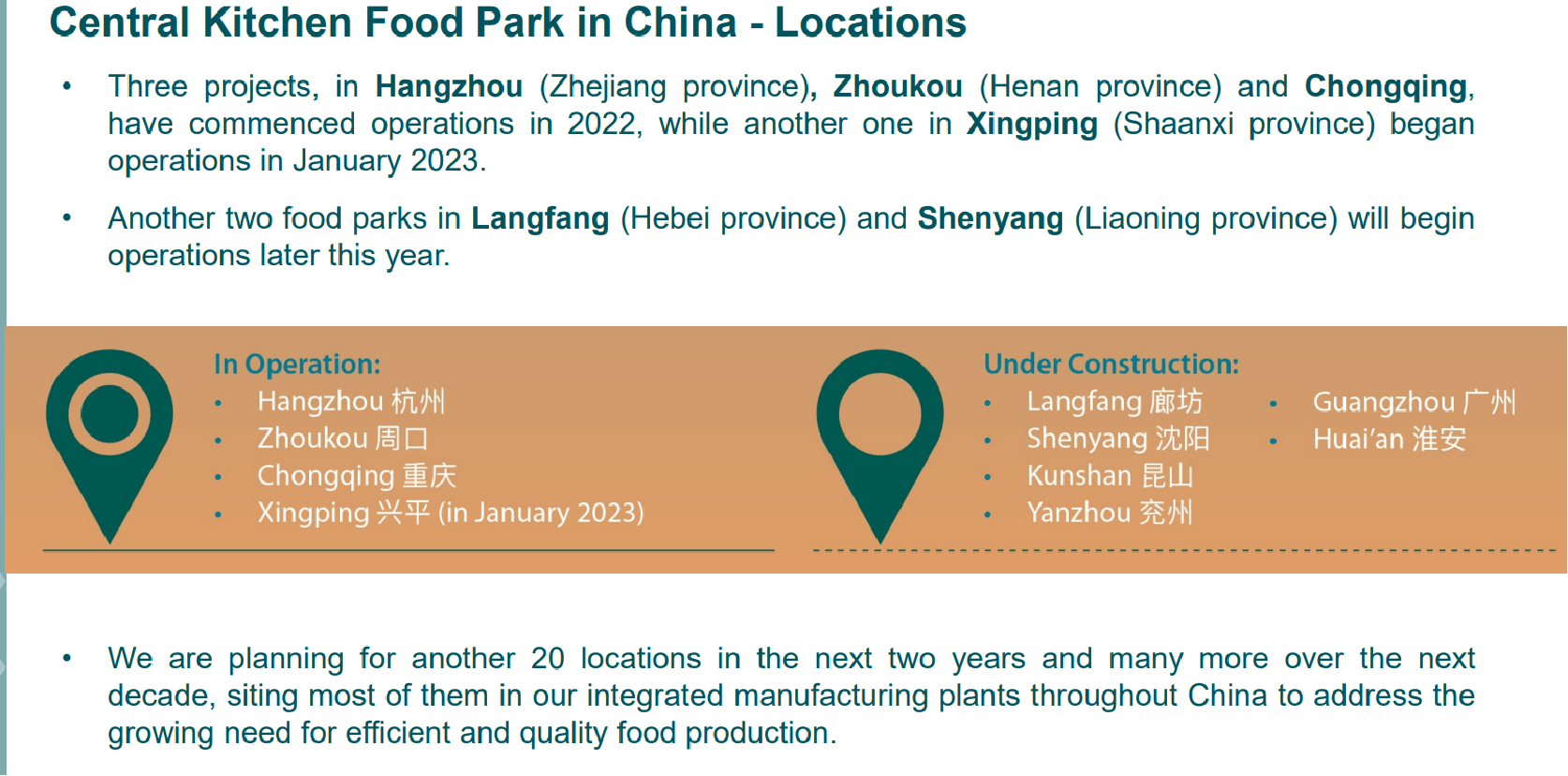

Wilmar International's first central kitchen is located in Hangzhou, China, which began operating last year. The company has plans to establish many more central kitchens in different parts of Mainland China as highlighted in the chart below.

Wilmar International's Central Kitchens In Operation And In The Pipeline

Wilmar International's 2023 Annual General Meeting Presentation Slides

{kind=link}

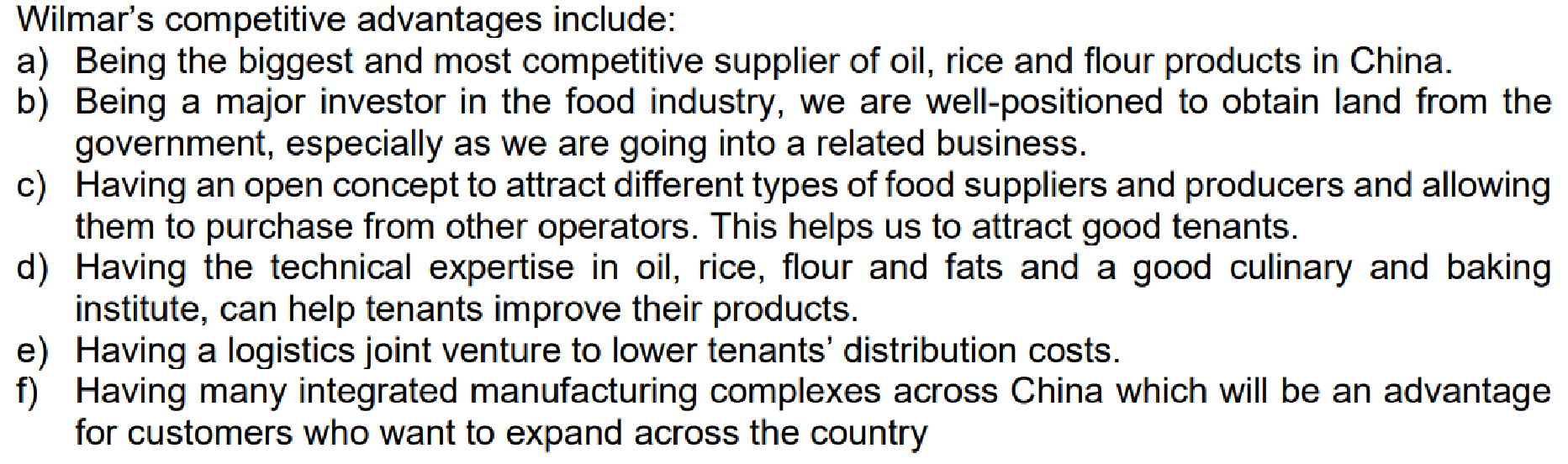

WLMIF does have an edge in the central kitchen business and this business is expected to provide multiple revenue streams for the company as detailed in the charts below.

Wilmar International's Edge In Operating Central Kitchens

Wilmar International's 2023 Annual General Meeting Q&A Session

{kind=link}

The Central Kitchen Business' Multiple Revenue Streams

Wilmar International's 2023 Annual General Meeting Q&A Session

{kind=link}

But the company didn't provide any specific financial numbers relating to its central kitchen business in its most recent fiscal year or FY 2022 annual report . In that respect, it is reasonable to infer that Wilmar International's central kitchen operations generate insignificant revenue and are still unprofitable.

At the company's Annual General Meeting this year, Wilmar International also acknowledged that "the take-up rate (for its central kitchens) has not been as strong as earlier anticipated", but it stressed that its "long-term plans for the CK (Central Kitchen) Food Park project remain unchanged."

In summary, new central kitchen operations will diversify the company's business mix in the long run, but the actual top line and profit contribution of the central kitchen business will be limited for now.

Closing Thoughts

I take the view that it is fair to assign a Hold rating to Wilmar International. The stock's valuations are undemanding, but it should take more time for its key catalysts to be realized.

For further details see:

Wilmar International: It's Premature To Be Bullish