AYX - WingArc1st: Highly Profitable But Not Exactly Supersonic

Summary

- WingArc1st generates high cash profits and is the market leader in its domestic Japanese market for Business Document Services software.

- Its growth outlook looks pedestrian with its niche focus and the lack of cross-selling opportunities.

- Valuations are not demanding, but given the low pace of growth, we rate the shares as neutral.

Investment thesis

WingArc1st (WARCF) is a niche market leader in Japan for Business Document Services, with a challenger business in business analytics. The growth outlook is relatively low, due to its specialist nature and lack of cross-selling opportunities. The current outlook would mean its medium-term target EBITDA being missed. On undemanding valuations, we rate the shares as neutral.

Quick primer

Established in 2004 as a software development business and listed back in 2010, WingArc1st specializes in two areas of data analytics - BDS (Business Document Services, such as design, and tracking of business forms and applications such as purchase orders and invoices directed for the Japanese market) and DE (Data Empowerment - effective data analytics). It is said to have around 67% domestic market share in BDS, and 14% in DE. In Q3 FY2/2023, recurring revenues (from subscriptions) made up 58% of the total, with the remainder being license income.

In a competitive market, domestic peers include specialist software firms Change (3692) and OPTIM (3694), RPA-related players such as RPA Holdings (6572), and DX transformation service providers ranging from large IT consultancies such as NRI ( NRILY ) and NTT Data ( NTTDF ) to smaller specialists such as Rakus (3923). Other data analytics companies are making inroads in Japan, such as Domo ( DOMO ) and Alteryx ( AYX ).

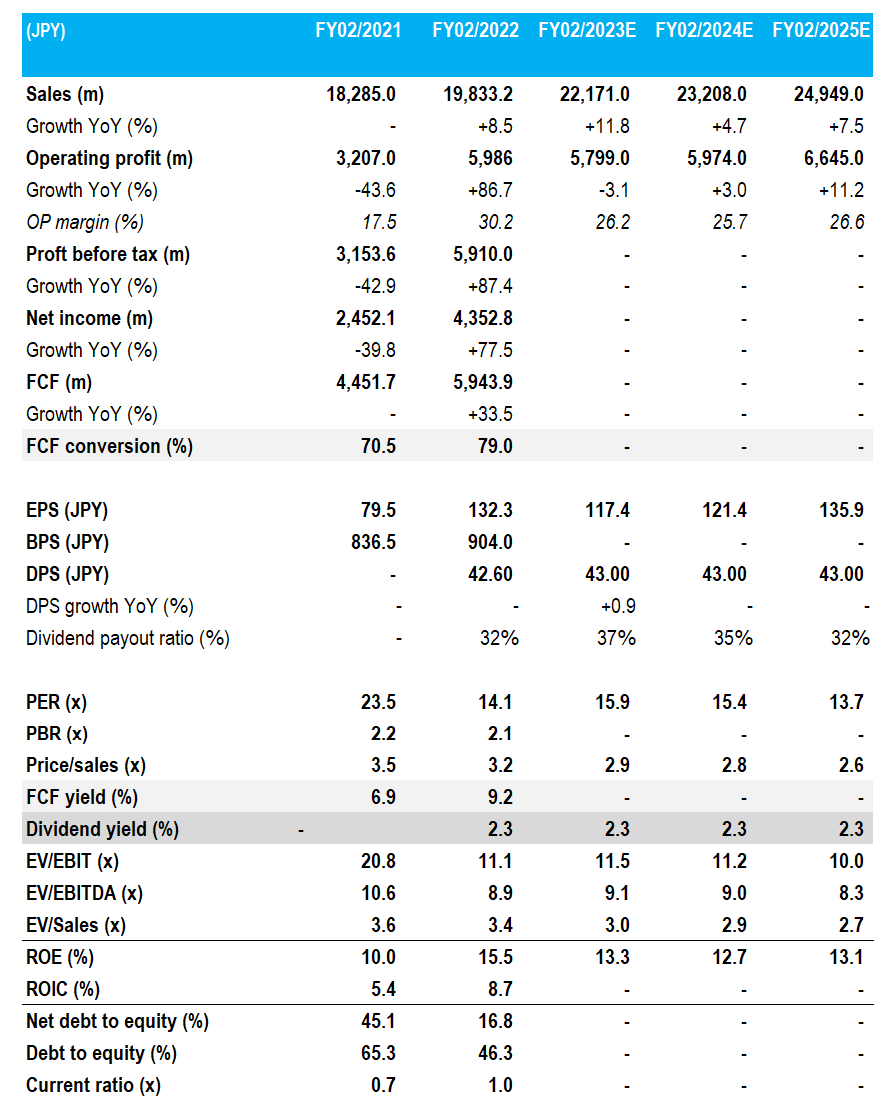

Key financials with consensus forecasts

Key financials with consensus forecasts (Refinitiv, Company)

{kind=link}

Our objectives

With IT capex in relatively good health in Japan, we see that digital transformation ((DX)) is a core driver. Both enterprises and the public sector are aiming to redesign business processes post-pandemic, with new business practices such as remote work, cloud, and greater use of data analytics.

Despite being a very competitive market, WingArc1st has established a strong position in BDS. We want to assess the growth outlook, and whether the shares are worth investing in.

Recent trading and outlook

Q1-3 FY2/2023 results highlight that the company passes the general 'rule of 40' test in terms of growth and profitability, with sales growth of 14.7% YoY and an operating profit margin of 30.7%. The company is seeing strong demand from larger enterprises for BDS software and has raised its FY guidance as a result. However, with consensus forecasts reflecting this uplift (see Key Financials table above), we note that operating margins are expected to fall YoY as the company has been spending on strategic investments such as new hires and marketing.

The outlook for the next two years appears to be steady single-digit growth, which is somewhat disappointing. We note that whilst niche Japanese software companies tend to be high margin and control their marketing costs well and report decent cash profits, topline growth is low for what is seen as a growth theme. We see two reasons for this. Firstly, despite the high and admirable market share the company has in BDS, it does not appear to have cost the business significant marketing dollars to achieve this, which leads us to believe that their product is niche and the total addressable market is small and limited. Secondly, the company has limited resources to expand its business to adjacent markets, which implies that growth potential is very finite.

The company has offices in Asian locations, but this appears to be more for offshoring development as opposed to cultivating new markets. Toshiba Digital Solutions Corporation (a subsidiary of Toshiba ( TOSBF )) has a 13.46% stake in the company, but this capital tie-up appears to have had a limited impact on business development thus far.

Medium-term plan

Driven by cloud service adoption, the company is aiming for an EBITDA of JPY12 billion /USD92 million by FY2/2027, from a current target of JPY6 billion/USD 46 million in FY2/2023. This implies a CAGR of 15% over the next 4 years, which look rather ambitious to us considering consensus as well as recent trading.

An obvious strategy for growth is to cross-sell BDS and DE products, but there is no company disclosure on this metric and we suspect there is not much success here. Other generic growth strategies include increasing distribution partners, but the company already has 535 of them which makes expansion difficult and susceptible to diminishing returns. Any overseas market expansion also looks unlikely given the Japan-centric offering.

Increasing pricing should be on the cards in the medium term given the inflationary environment, but versus large-cap customers, one feels that the company will have limited pricing power.

We conclude that as things currently stand, the company will make steady but finite progress over the medium to long term.

Valuation

On consensus forecasts, the shares are trading on PER FY2/2024 15.4x, EV/EBITDA 9.0x, and a dividend yield of 2.3%. On the surface, these valuations are not demanding, but then we should take into account a small cap discount, as well for limited trading liquidity.

Risks

Upside risk comes from a major push by enterprise customers to implement an accelerated digital transformation, resulting in steadily rising ARR and improving profitability.

The company is a specialist in a narrow field which could be attractive for other data-related services companies to acquire as a bolt-on asset. Capital tie-ups could also raise the share price, as the TAM could be seen as expanded via more cross-selling opportunities.

Downside risk comes from an increase in operating costs as the company needs to keep staff. Strategic investment costs may become more regular given rising competition as many software companies rebrand themselves in a digital transformation theme.

If the growth profile slows and margins do not improve, the business model will be seen as inferior to other SaaS-orientated growth names. Valuation multiples could contract as opposed to expanding.

Conclusion

WingArc1st is a highly profitable market leader in a niche space and looks fairly valued to us. We commend management's ability to generate cash profits, but we see growth limitations given the lack of cross-sell opportunities between their two core products, and the fact that the market already looks quite saturated. Whilst valuations are not demanding, our key concern stems from a pedestrian growth outlook that could result in valuation multiple contractions - the average PER multiple in FY2/2021 was 27.2x, and in FY2/2022 fell to 12.9x.

For further details see:

WingArc1st: Highly Profitable But Not Exactly Supersonic