REVG - Winnebago Industries: Still Worth Consideration Despite Tremendous Industry Pain

2023-03-23 21:49:48 ET

Summary

- Winnebago has been negatively impacted by a great deal of pain in the industry in which it operates.

- This pain is likely to ease as the year progresses, but the overall picture for the firm should worsen relative to what it was last year.

- Even with this pain taking place, shares of the business look attractively-priced and likely offer investors at least some upside.

For the most part, the economy continues to perform quite well. But as I highlighted in another article, we are starting to see some signs of weakness. One space that has been particularly impacted by high inflation and rising interest rates is the motor home / RV market. What data is available today shows a significant decline in shipments. Naturally, this is having a negative impact on the companies that operate in this space. But some of these firms have been beaten up more than what is warranted. One great example of this can be seen by looking at Winnebago Industries ( WGO ), an enterprise that is famous for producing and selling recreational vehicles and other related products and services. Despite plunging sales, profits, and cash flows, the stock still looks cheap. This includes not only on an absolute basis, but also relative to similar firms. So long as the fundamental condition of the company does not deteriorate far more than what it has already, I would make the case that some additional attractive upside still exists for investors from here.

Significant industry pain

Because of the high cost of production, combined with the reliance on financing that has, undoubtedly, been made less attractive by rising interest rates, the recreational vehicle market is one of the first to show meaningful deterioration in response to interest rate hikes aimed at combating inflation. The latest example of this weakness can be seen by looking at data covering January of this year. That's the most recent month for which data is available. According to one source, the number of recreational vehicles shipped during the month totaled only 20,405. That's down 61.8% compared to the 53,351 reported the same month one year earlier. The biggest pain for the industry came from the towable segment, with revenue plunging 66.8% compared to the 10.1% decline experienced by motor homes.

Although January started off rather rough, industry experts believe that the space will show some leveling off as the year progresses. For 2023 as a whole , for instance, the expectation is that wholesale recreational vehicle shipments will come in at between 324,300 and 344,000. Although this sounds like a significant number of vehicles, it would actually represent, using the midpoint figure of 334,100 units, a 32% decline compared to the 493,300 wholesale shipments reported for 2022. These industry experts cited an uncertain economy, high inflation, and rising interest rates as the primary drivers behind this weakness. In addition to that, however, an inventory glut at the retail level (a glut that is improving) is also responsible.

With weakness like this, I can understand why some investors may prefer to stay away from companies in this market. However, I have long believed that the best time to buy is when the companies in question are already experiencing pain. And what better prospect to consider than Winnebago Industries, one of the largest players in the market? The last article that I wrote about Winnebago Industries was published in early December of last year. In that article, I acknowledged that short-term risks could cause sales and cash flows to weaken in the short run. But all things considered, I believed the company to be a healthy business with shares that looked cheap, both on an absolute basis and relative to similar firms. This led me to rate WGO stock a ‘buy’, but results since then have not been particularly great. At a time when the S&P 500 is down 1.6%, shares of Winnebago Industries have outperformed, but only marginally with a decline of 0.7%.

Fundamentals have weakened as well

{kind=link}

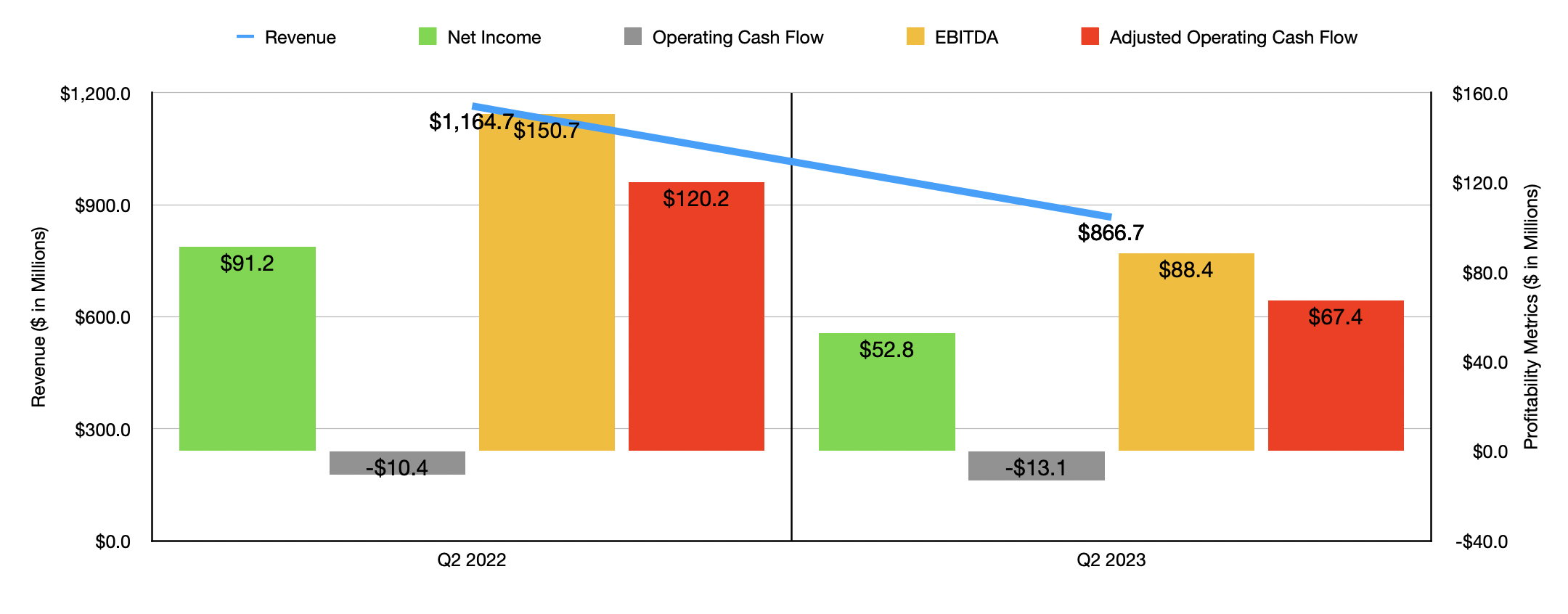

Interestingly, this outperformance has come even at a time when the fundamental condition of the company has shown signs of deteriorating. I think we can chalk up the outperformance then to the fact that, while performance is weaker than it was a year ago, it is still higher than what analysts anticipated. Consider results covering the second quarter of the 2023 fiscal year. These were just reported on March 22nd. Revenue for the quarter came in at $866.7 million. That's 25.6% lower than the $1.16 billion the company reported the same time one year earlier. Despite the plunge in sales, management exceeded expectations that were set by analysts to the tune of nearly $83 million. The biggest pain for the company came from a significant downturn in the number of unit deliveries reported by management. Under the Towable segment, deliveries came out to 7,436. That's 51.4% lower than the 15,294 units that were sold the same time one year earlier. Under the motor home segment, shipment volumes declined a much more modest 23.5%, with the number declining from 2,831 to 2,165. This is not to say that everything reported by management was weak. There was one really great spot for the firm. This involved the much smaller Marine segment. Even though the number of units declined by 4.2%, dropping from 1,322 to 1,266, overall revenue managed to rise from $97.3 million to $112.9 million thanks to higher pricing.

{kind=link}

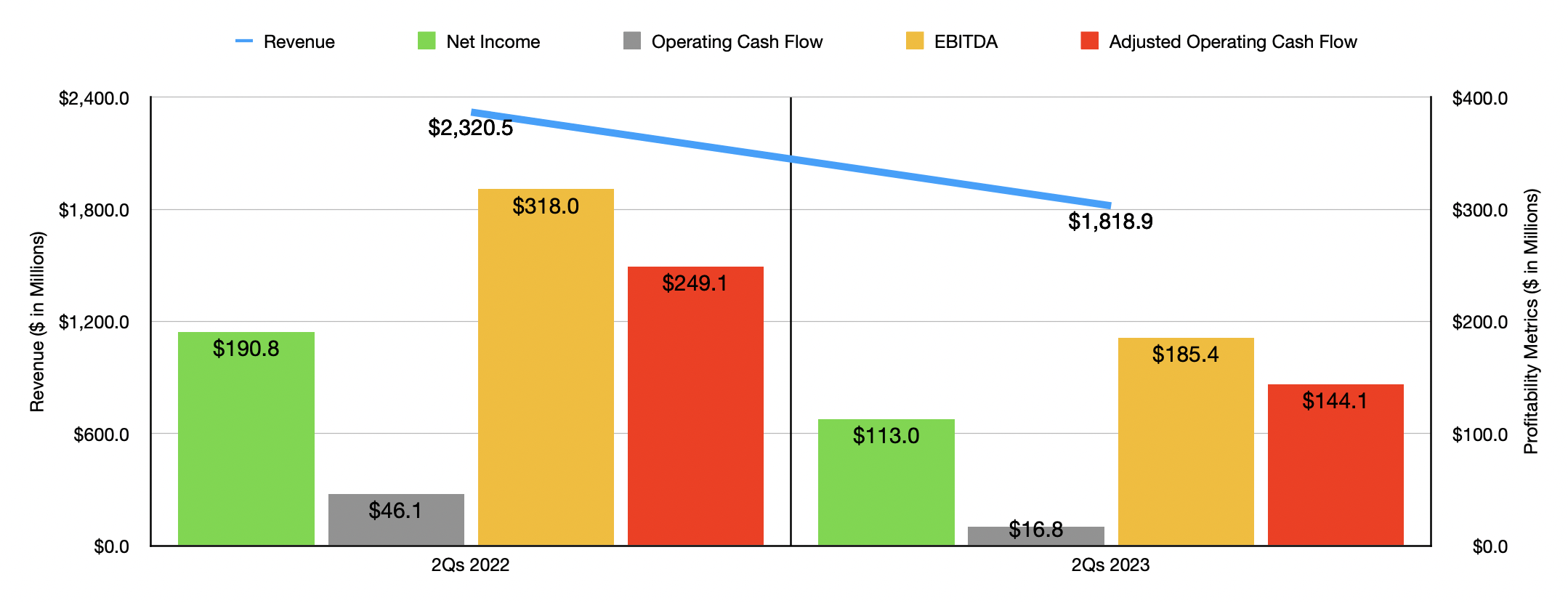

The drop in revenue for the company brought with it a decline in profits. Net income totaled $52.8 million. That's nearly half the $91.2 million reported the same quarter one year earlier. On a per-share basis, earnings totaled $1.52. At the same time, the 2022 fiscal year resulted in earnings per share of $2.69. Even though this plunge looks painful, it's important to note that the earnings per share reported by management actually came in higher than what analysts anticipated to the tune of $0.45. Other profitability metrics also weakened during this time. Operating cash flow, for instance, went from negative $10.4 million to negative $13.1 million. On an adjusted basis, it declined from $120.2 million to $67.4 million. And finally, EBITDA for the company fell from $150.7 million to $88.4 million. In the chart above, you can see how the second quarter was not a one-time event. The first half of the 2023 fiscal year as a whole has shown signs of worsening. More likely than not, this trend will continue through at least this year.

{kind=link}

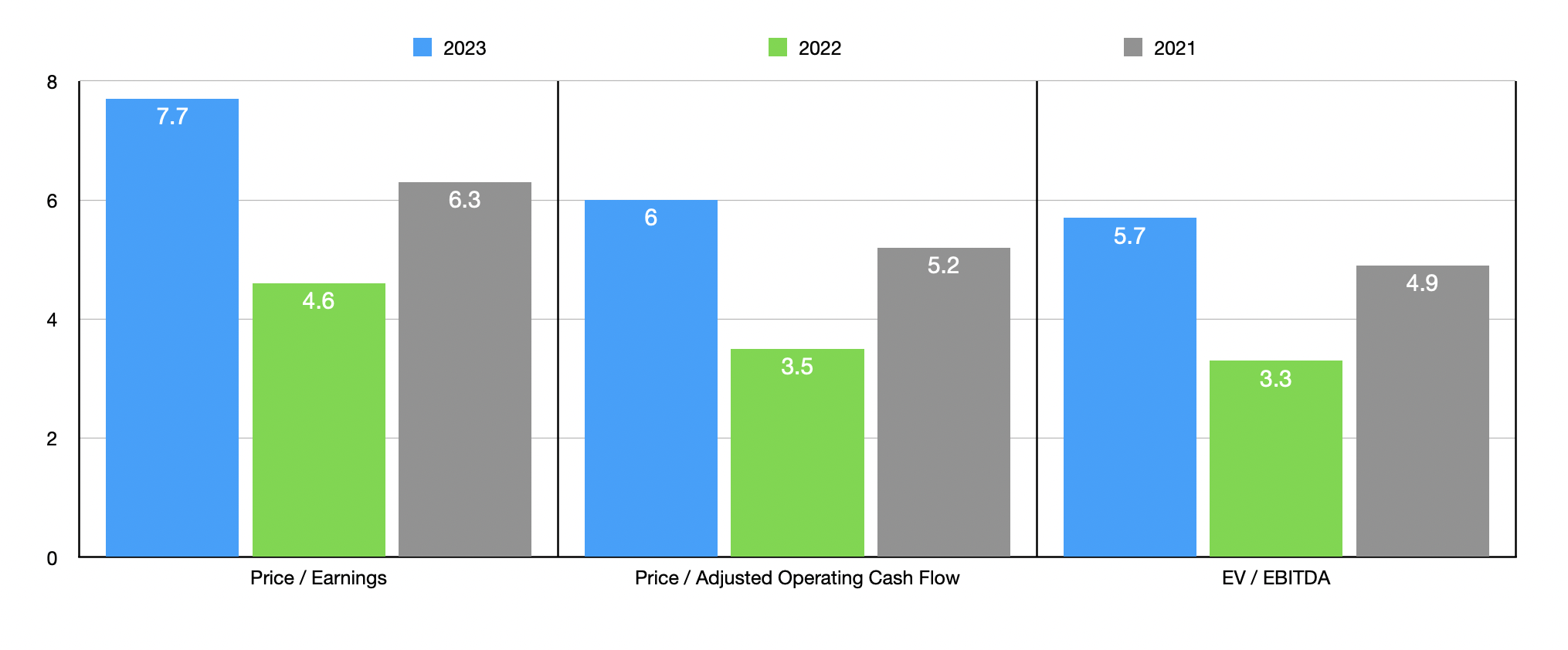

If we project out the financial performance achieved so far for the year, we would get net income of $231.3 million, adjusted operating cash flow of $296.5 million, and EBITDA of $378.3 million. Based on these figures, the company is trading at some pretty cheap multiples. The forward price to earnings multiple, for instance, is 7.7. That compares to the 4.6 reading that we get using data from 2022. The price to adjusted operating cash flow multiple should be even lower at 6, a number that is up from the 3.5 reading that we get using data from the year prior. And finally, using the EV to EBITDA approach, we get a reading of 5.7 compared to the 3.3 from the year prior. As part of my analysis, I also compared the company to five similar firms. Using the data from 2022, since it is the most recent completed fiscal year, I actually calculated that Winnebago Industries was cheaper than any of the five firms I looked at. If, instead, we were to use the valuation from 2023, then we end up with for the five firms being cheaper than Winnebago Industries when it comes to the price-to-earnings approach, and three of them being cheaper using the other valuation metrics.

| Company |

| Price / Earnings |

| Price / Operating Cash Flow |

| EV / EBITDA |

| Winnebago Industries |

| 7.7 |

| 6.0 |

| 5.7 |

| Lazydays Holdings ( LAZY ) |

| 6.0 |

| 110.3 |

| 4.2 |

| THOR Industries ( THO ) |

| 5.5 |

| 5.0 |

| 4.2 |

| LCI Industries ( LCII ) |

| 7.0 |

| 4.6 |

| 5.6 |

| Camping World Holdings ( CWH ) |

| 6.4 |

| 4.7 |

| 5.8 |

| REV Group ( REVG ) |

| 294.9 |

| 8.0 |

| 17.3 |

Takeaway

At this moment, the recreational vehicle and motor home market is facing a great deal of pain. It looks as though the picture will ease up later this year. However, that doesn't change the fact that Winnebago Industries is experiencing some discomfort at this time. Fortunately for investors, even with the assumption that fundamentals will worsen before they get better, the company still looks to be a solid opportunity. Because of this, I've decided to keep it rated a ‘buy’ for now to reflect my view that it should outperform the broader market moving forward.

For further details see:

Winnebago Industries: Still Worth Consideration Despite Tremendous Industry Pain