VRE - Winners Of REIT Earnings Season

2023-11-10 09:00:00 ET

Summary

- Beneath the "Rates Down, REITs Up" whipsaw effects, REIT earnings results were stronger than expected across most property sectors, particularly from retail, hotel, and technology REITs.

- Among the equity REITs that provided updated guidance, 82% increased their forecast, while only 18% lowered their full-year NOI outlook - a beat rate that significantly exceeded the S&P 500.

- As predicted, mergers and acquisitions were a major theme, with several small and mid-cap REITs being acquired by larger peers - a trend that we expect to continue into 2024.

- Retail REITs have enjoyed an under-discussed revival over the past 18-24 months as store openings have considerably outpaced store closings, driving occupancy rates to record highs and fueling impressive double-digit rent growth.

- Unlike the second quarter, which saw a handful of truly poor reports and unexpectedly steep guidance and dividend cuts, there were no major 'bombshells' this earnings season. In Part 1 of our Earnings Recap, we discuss the Winners of REIT Earnings Season.

Real Estate Earnings Recap

{kind=link}

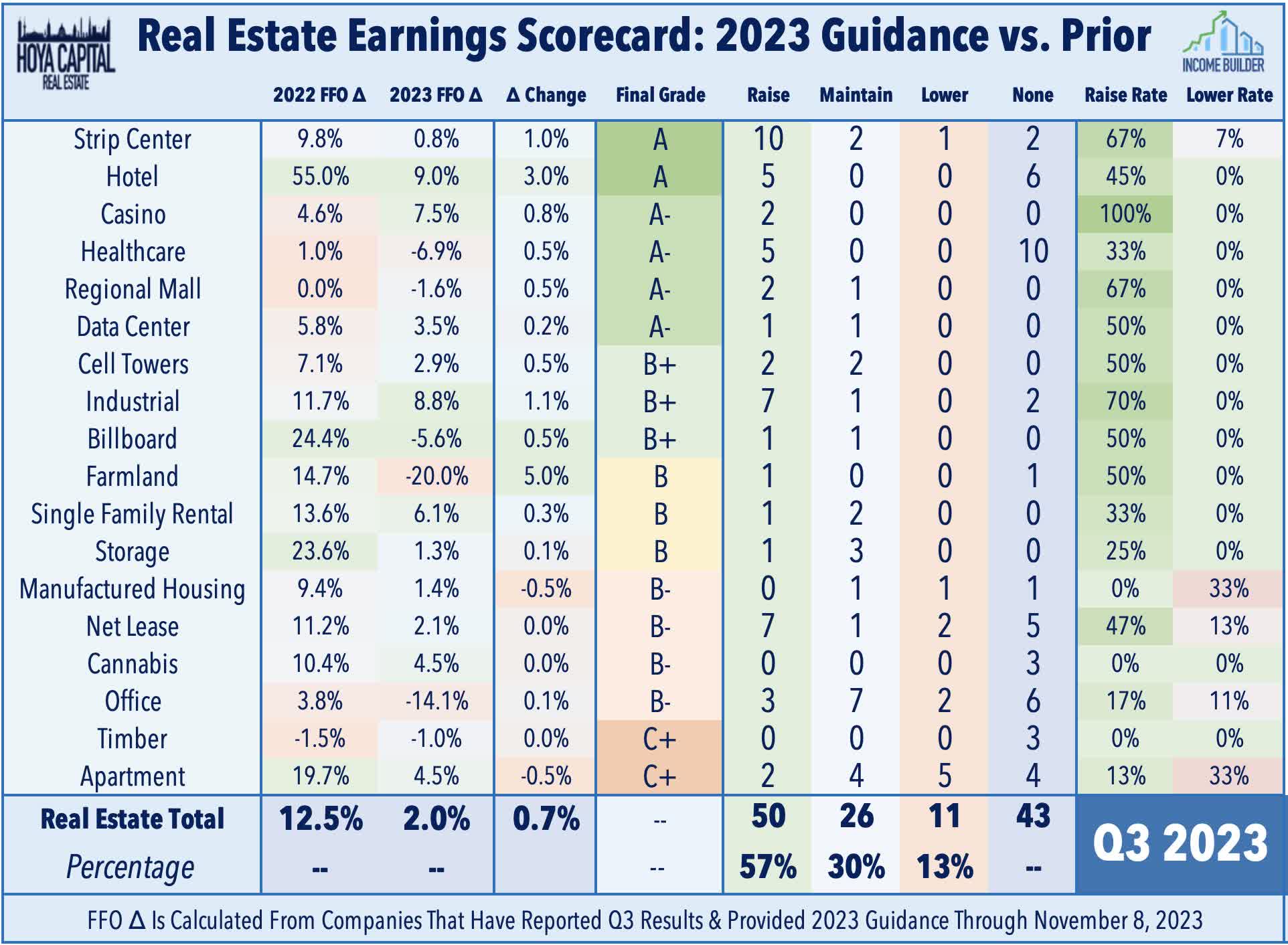

Nearly 200 U.S. REITs have reported third-quarter earnings results over the past month, providing critical information on the state of the commercial and residential real estate industry. As discussed in our Halftime Report, REIT earnings season was off to a hot start, and contrary to the historical trends, the back half of earnings season was actually notably stronger, led by impressive reports from dozens of retail and hotel REITs. Of the 87 equity REITs that provided updated full-year Funds From Operations ("FFO") guidance, 50 REITs increased their forecast, 26 maintained, and 11 lowered their outlook. Among the 61 REITs that adjusted their forecast, 82% were upward revisions, while 18% were downward revisions. By comparison, FactSet reports that 54% of S&P 500 components have raised the full-year EPS outlook, while 46% have reduced their guidance. The guidance "raise rate" was stronger at the property-level than at the corporate level, with just 10% of REITs lowering their full-year Net Operating Income ("NOI") outlook.

{kind=link}

In our Earnings Preview , we predicted that REIT M&A would remain a major theme this earnings season, and commented that " we expect several additional small and mid-cap REITs that trade at size-related discounts to be picked-up by larger peers." We saw exactly that, with another pair of mergers announced last week: Realty Income ( O ) - the largest net lease REIT - announced a deal to acquire Spirit Realty ( SRC ) - the fifth largest net lease REIT - in a $9.3B all-stock deal at a 15% premium to SRC's last closing price. Elsewhere, medical office building REITs Healthpeak Properties ( PEAK ) and Physicians Realty ( DOC ) agreed to merge in an all-stock merger of equals. We've now seen ten REIT-to-REIT consolidations this year, with this pair of deals following the merger between two of the four largest self-storage REITs Extra Space ( EXR ) and Life Storage , and a pair of shopping center REIT mergers: Regency Centers ( REG ) acquisition of Urstadt Biddle in May, and Kimco's ( KIM ) acquisition of RPT Realty ( RPT ) in August. Markets have generally been receptive to these moves, as equity REITs have become the "only game in town" for potential sellers given the scarcity of debt capital.

{kind=link}

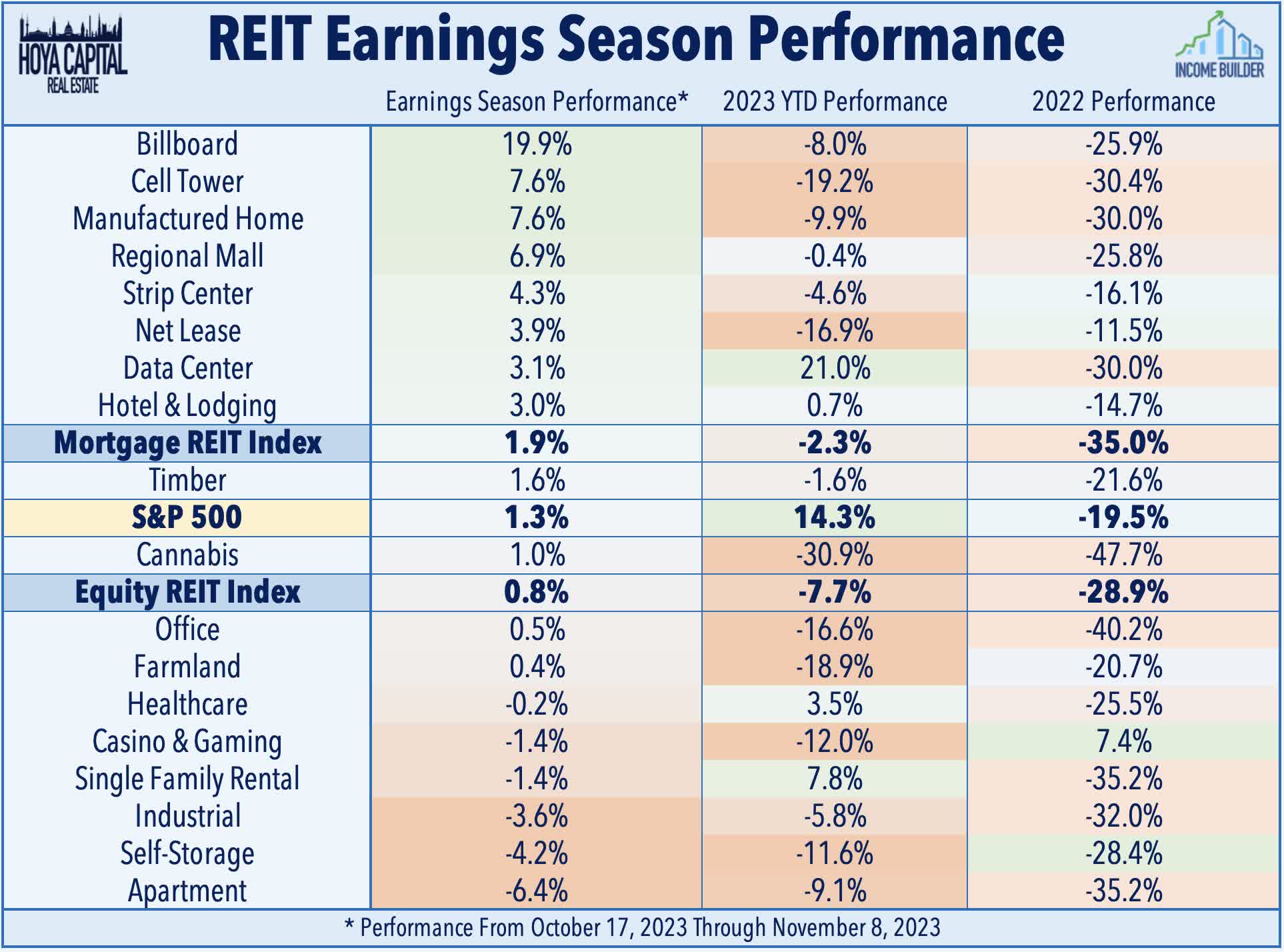

" Rates Up, REITs Down " was the theme early in earnings season as the benchmark 10-Year Treasury Yield climbed to fresh 15-year highs, but REITs were whipsawed in a positive direction in the back-half of earnings season as interest rates retreated sharply following a "dovish pause" in the Fed's November meeting and a much-needed dip in oil prices - the primary culprit behind the late-summer inflation resurgence. Resilient pricing power remained a common thread across most property sectors throughout earnings season - notably in data center, and retail REITs - while surprisingly solid demand in many of the most pro-cyclical sectors - notably hotel and billboard REITs - was a takeaway from the back-half of earnings season. Expense growth remained stubbornly persistent for residential REITs - which were responsible for the majority of the downward NOI revisions this quarter - with insurance and property taxes rising by double-digits across most markets and segments. Supply growth is becoming a headwind for multifamily, self-storage, and industrial REITs as the pandemic-era boom in new development reaches completion, but developers have pulled back significantly this year, providing reasons for optimism heading into 2024 if current demand trends can hold up.

{kind=link}

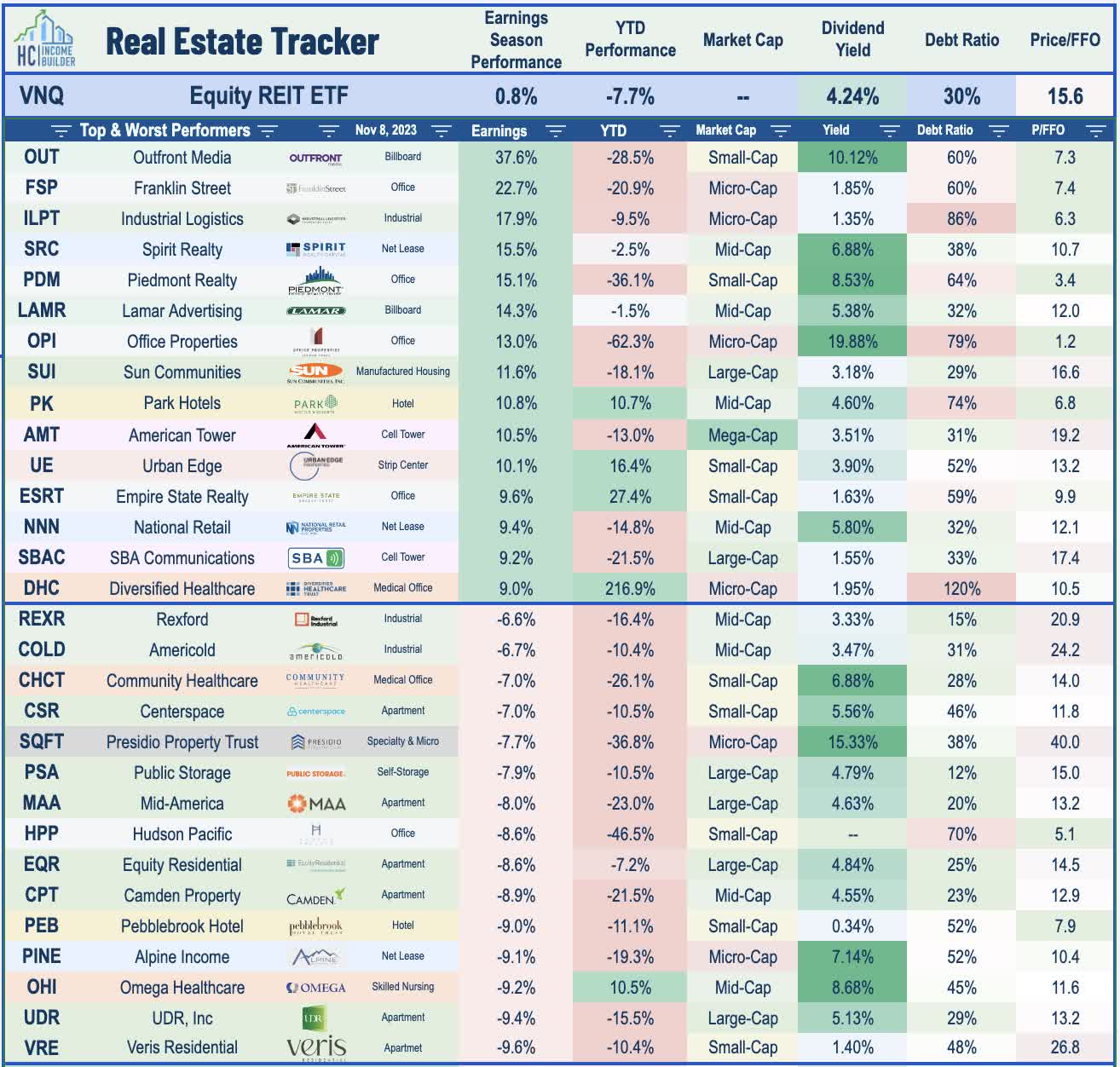

Among other notable positive themes this quarter, expense pressures abated a bit for some sub-sectors - notably in the labor-intensive senior housing, cold storage, and hospitality sectors - while tenant rent collection improved marginally for most healthcare and cannabis REITs. Outside of the expense pressures in the multifamily space, the handful of other earnings "misses" and downward earnings revisions were driven almost exclusively by elevated debt servicing expenses, underscoring the continued challenges facing more highly leveraged real estate portfolios from the higher rate environment. Unlike the second quarter, which saw a handful of truly poor reports and unexpectedly steep guidance and dividend cuts, there were no major 'bombshells' this earnings season. This theme is perhaps best illustrated by the fact that the single weakest performer this earnings season - Veris Residential ( VRE ) - actually raised its full-year guidance and expects double-digit NOI growth, while results from many of the other laggards were only mildly disappointing.

{kind=link}

Dividend sustainability is always a focus during earnings season, and we've been scouring through earnings calls to glean insights into the outlook for dividend hikes - and in some cases, dividend cuts - this year. Another half-dozen REITs hiked their dividends during earnings season - led by four dividend hikes from strip center REITs - bringing the full-year total to 73. Two REITs announced dividend cuts - both residential mortgage REITs - bringing the full-year total to an even 30. A small handful of REITs - primarily in the mREIT space - also hinted at a dividend reduction in the near future. With real estate earnings season now essentially complete - sans a handful of stragglers that report results over the coming days - we compiled the critical metrics across each real estate property sector. Part 1 of our two-part REIT Earnings Recap focuses on the "Winners of REIT Earnings Season."

{kind=link}

Winner #1: Strip Centers

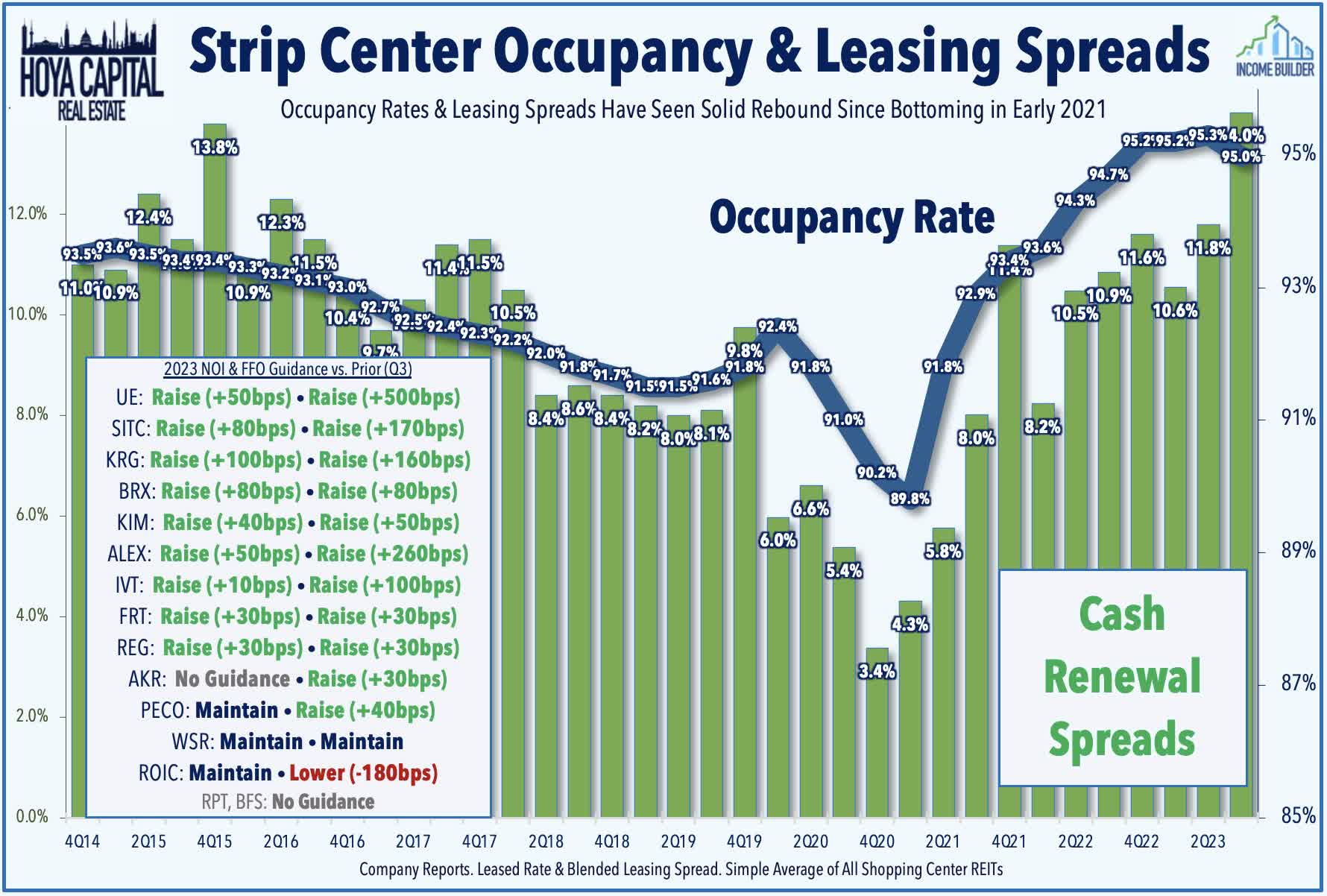

Strip Center : (Final Grade: A) Strip center REITs were a notable upside standout with a near-perfect slate of upward guidance boosts - and a half-dozen additional dividend hikes - as record-high occupancy rates resulting from a decade of limited new development fueled another quarter of double-digit rental rate spreads. Continuing a trend of better-than-expected results stretching back to late 2021, ten strip center REITs raised their full-year FFO outlook while just one lowered their FFO target as demand for "big box" space has significantly exceeded the available supply despite the recent high-profile bankruptcies of Bed Bath and Party City. Strip Center REITs reported that blended rent spreads averaged 14.0% in Q3 - the strongest on record - but occupancy rates declined slightly to 95.0% from the record-high of 95.3% last quarter. These REITs reported healthy demand for the vacated Bed Bath locations - space that is generally on the upper-end of the 'quality' spectrum - with several REITs highlighting impressive re-leasing rent spreads of over 50% on this space. Small-shop occupancy - which has generally lagged since the pandemic - also improved across the board, with several REITs identifying this as an area of focus and catalyst for growth in 2024.

{kind=link}

At the individual level, Kite Realty (KRG) and Brixmor Property (BRX) were once again upside standouts - each raising their guidance and hiking their dividend. Fueled by impressive blended leasing spreads of 14.2% and 22.3%, respectively, KRG and BRX now both expect full-year FFO growth of 4.1%. Regency Centers (REG) was also a notable upside standout, lifting its full-year outlook and its dividend. Kimco (KIM) - the largest strip center REIT - also increased its dividend while noting that it leased 2.1M square of space in Q3, achieving blended rent of 13.4%, the highest level of combined leasing spreads in six years. Also of note, SITE Centers (SITC) has been among the top-performers after reporting similarly strong results, raising its full-year outlook, while also announcing that it will spin-off its convenience store portfolio into a separate publicly-traded REIT to be named Curbline Properties (CURB), which will be classified as a triple net lease REIT.

{kind=link}

Winner #2: Hotels

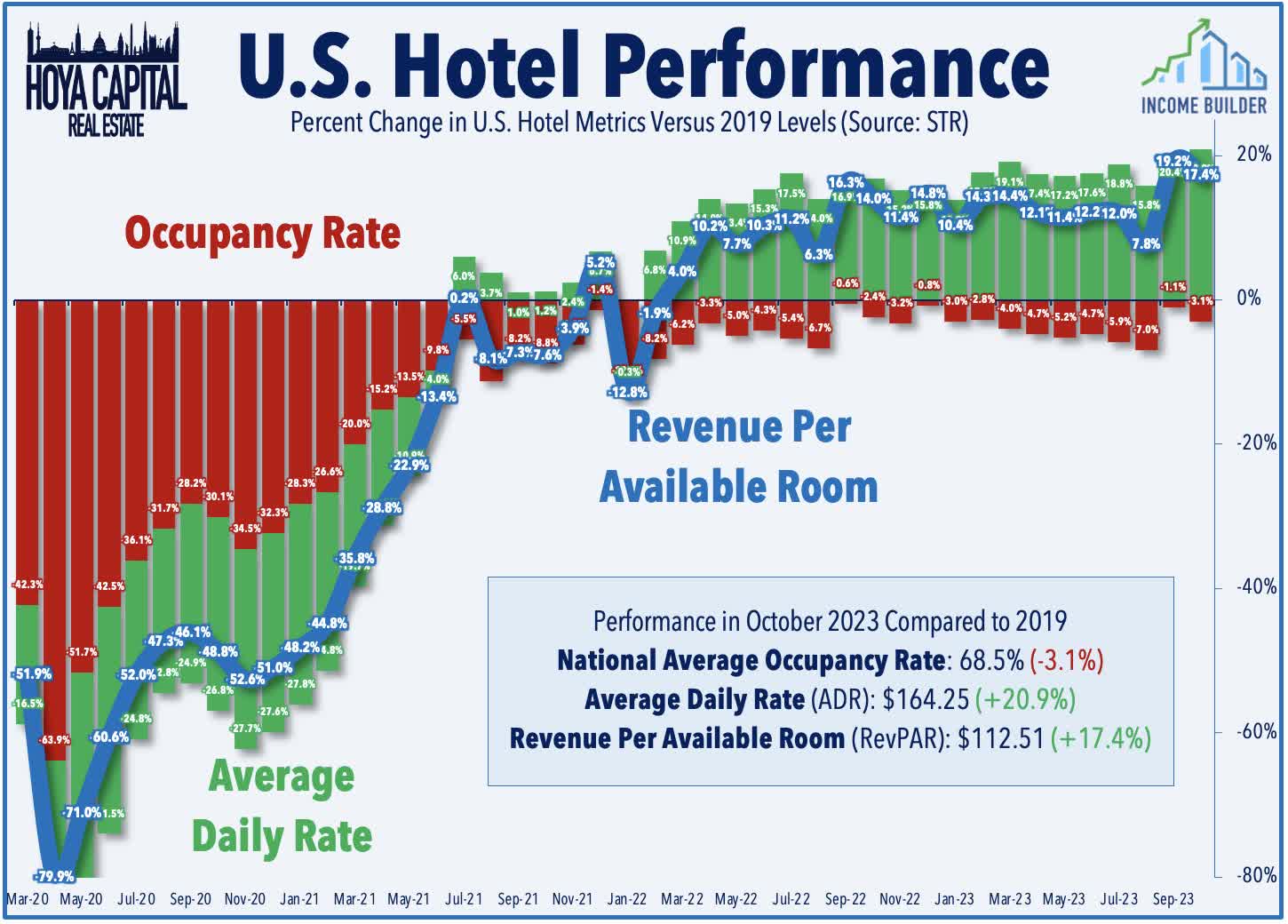

Hotel : (Final Grade: A) We had high expectations for hotel REITs given the recent encouraging high-frequency travel demand data from TSA and STR, and these REITs certainly delivered, with their most impressive earnings season since the start of the pandemic. All five hotel REITs that provide full-year FFO guidance lifted their full-year earnings, with commentary indicating that leisure demand has moderated only slightly in recent months, while business and group travel has continued its gradual recovery. Recent TSA Checkpoint data shows that throughput climbed to 105% of 2019-levels in October - the highest since the pandemic - while hotel data provider STR reports that industry-wide Revenue Per Available Room ("RevPAR") was 17% above 2019 levels in October, as a roughly 21% relative increase in Average Daily Room Rates ("ADR") offset a roughly 3% relative drag in average occupancy rates.

{kind=link}

At the individual level, Park Hotels (PK) was the upside standout after raising its full-year guidance and declaring a special dividend, citing strength in its urban portfolio and the exit from the troubled San Francisco market. Sunbelt-focused Ryman Hospitality (RHP) has also been an upside standout, noting that its Revenue Per Available Room ("RevPAR") was up 21% compared to the pre-pandemic baseline from 2019 - the strongest in the hotel REIT sector. Overall, the six guidance-providing hotel REITs now expect RevPAR to increase by 7.0% this year, up from the 6.9% outlook last quarter. Host Hotels (HST) lifted its full-year FFO growth outlook, and reiterated its outlook for full-year RevPAR growth target of 8.0%, which would be 5.6% above 2019 levels. Apple Hospitality (APLE) noted that its RevPAR was 7% above 2019-levels in Q3 - its best quarterly comparable since the onset of the pandemic - driven by "a steady recovery in business transient and continued strength in leisure." APLE now expects full-year RevPAR growth of 6.5% at the midpoint - up 50 basis points from last quarter - and provided positive commentary on recent trends, noting that "a continuation of current trends would position us to perform above the midpoint of our guidance."

{kind=link}

Winner #3: Casinos

Casino : (Final Grade: A-) Heralded last year for their inflation-hedging characteristics, casino REITs have faced the other side of that trade this year as inflation normalizes from the four-decade highs seen last year, but have been among the better-performers this earnings season on the heels of a pair of solid reports. VICI Properties (VICI) raised its full-year FFO growth target to 11.1% - up 100 basis points from last quarter - while Gaming and Leisure Properties (GLPI) hiked its FFO growth target to 3.8% - up 50 basis points from last quarter. "Defensive" was the theme of both VICI and GLIP's earnings call, underscored by commentary from GLPI that it being "very methodical in the way we think about things" and to not "mistake activity for progress. VICI focused on recent moves to bolster its balance sheet, while it also fielded questions about its deal to acquire the real estate assets of 38 bowling alleys from Bowlero Corp (BOWL) - the largest operator of bowling alleys in the United States with roughly 350 locations - in a sale-leaseback transaction.

{kind=link}

VICI's first major acquisition outside of its core casino property sector focus, the deal was completed at an acquisition cap rate of 7.3% based on total annual rent of $31.6M. Bowlero will represent 1% of VICI's rent roll, and VICI will have the right of first offer for eight years to acquire additional real estate assets of Bowlero. VICI - which already owns a relatively dominant share of casino assets in the Las Vegas strip following a half-decade of rapid external growth - has noted in recent earnings calls that it is exploring "experiential" asset classes with similar characteristics as the casino sector. VICI noted that Realty Income's (O) partial acquisition of The Bellagio from Blackstone (BX) at a 5.2% cap rate showed the "resilience" and "vitality" of the Las Vegas market. Also of note, VICI took the opportunity to highlight the higher average lease escalations for casino assets compared to traditional net lease properties, noting "same-store growth is going to mean something in the net lease space over the next year if things slowdown in the way they might."

{kind=link}

Winner #4: Healthcare

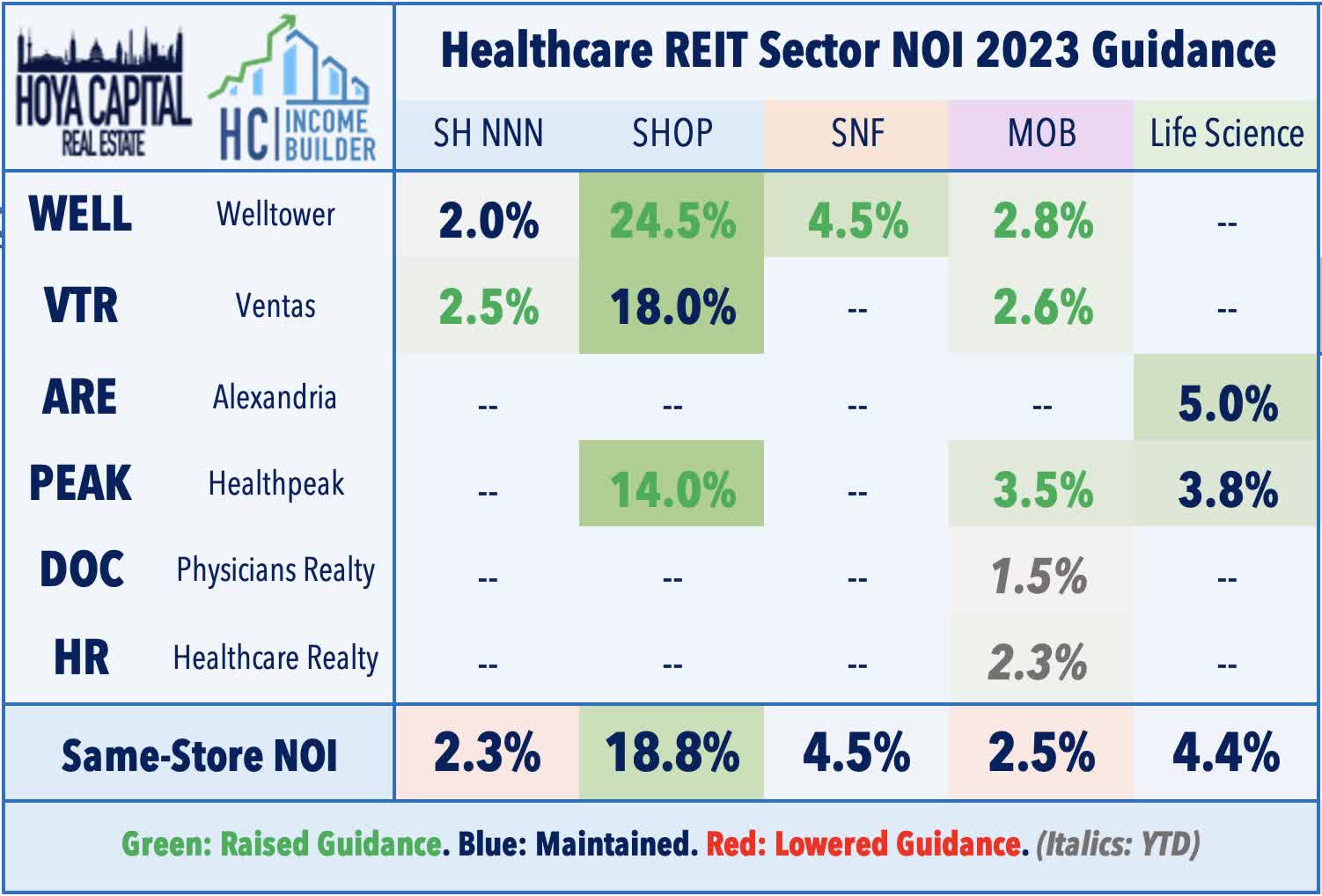

Healthcare : (Final Grade: A-) Continued record-setting rent growth in senior housing and a stabilization in tenant operator health within the skilled nursing and hospital segments were the takeaways from a relatively impressive slate of reports from healthcare REITs, as all five REITs that provide full-year FFO guidance lifted their outlook. Benefiting from COLA increases, pricing power remains robust across the sector, and, combined with moderating expense pressures, has driven a meaningful improvement in operating margins. Beginning on the private-pay side, Welltower (WELL) was an upside standout, lifting its full-year outlook driven by a significant profitability recovery in its critical Senior Housing Operating Portfolio ("SHOP") segment. WELL now expects same-store NOI growth in this segment to increase 24.5% this year, driven by rent growth of nearly 7% and by a gradual recovery in occupancy rates, which had been ravaged by the pandemic. WELL raised its full-year FFO growth outlook for the third time this year to 7.8% - up from 6.1% last quarter. Ventas (VTR) reported strong results as well and lifted its full-year outlook following a disappointment in the prior quarter. VTR continues to expect same-store NOI growth of 18% in its SHOP segment, while it raised its full-year outlook for its Skilled Nursing and MOB segment.

{kind=link}

Embattled hospital owners Medical Properties Trust (MPW) - which has plunged over 65% since the start of 2022 amid rent collection issues from a handful of struggling hospital operators - was the leader this earnings season after reporting decent results and raising its full-year outlook. MPW now expects its full-year FFO to decline 13.7% - a 110 basis point improvement from its prior outlook. Importantly, MPW noted that it resumed collecting cash rent payments in September and October from Prospect Medical, which had been struggling to pay rent. MPW - which had slashed its dividend by about 50% earlier this year - also detailed its new capital allocation strategy to raise $2B in new liquidity over the next year through asset sales and limited secured debt financing options. As with hospital operators, skilled nursing tenants aren't yet out of the woods, and the game of "wack-a-mole" continues, underscored by results from Omega Healthcare (OHI), which noted that 27% of its tenants have earnings levels that fail to cover rent, as measured by EBITDAR. OHI noted that it reduced 8% of this sum by selling 29 assets operated by LaVie - a long-troubled tenant - and segmented the balance into several groupings, narrowing the total to about 4% of high-risk tenants.

{kind=link}

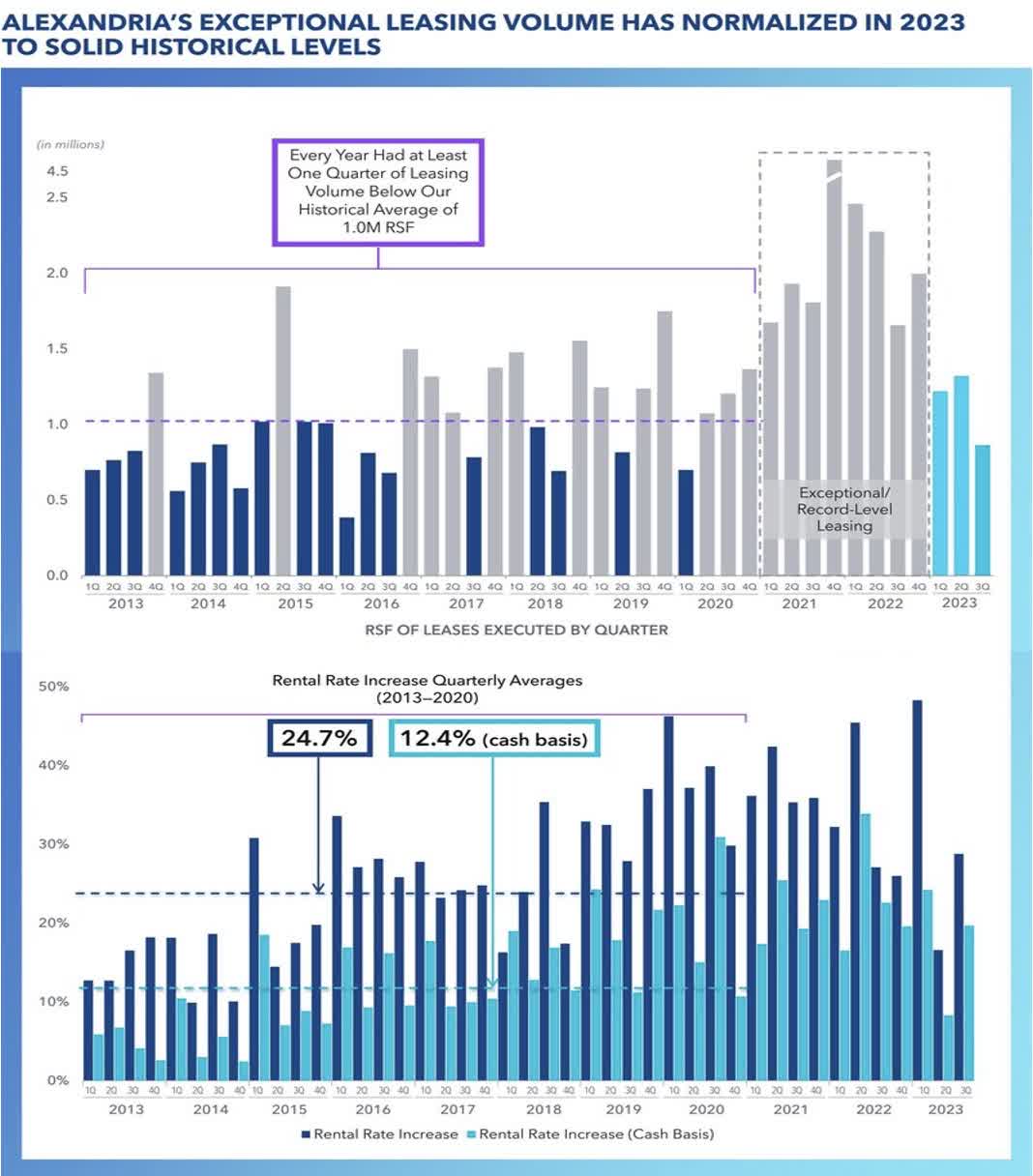

Results across the medical office building ("MOB") and lab space segments were generally in line with expectations. Healthpeak - which announced its plan to merge with Physicians Realty (DOC) - reported strong results and raised its full-year FFO and NOI outlook, but outperformance was driven primarily by its relatively small senior housing segment. Lab space owner Alexandria Real Estate ( ARE ) reported solid results as well and also raised the midpoint of its full-year FFO outlook. ARE - which has been among the laggards within the REIT sector this year on concern of sluggish lab space demand and oversupply in several major markets - now expects full-year FFO growth of 6.7%, up 30 basis points from its prior guidance. Leasing activity remained sluggish in Q3, as expected, with total volume of 867k square feet - its lowest since Q1 of 2020 - and down from 1.3M in Q2 and 1.2M in Q1. Rent spreads rebounded, however, with cash renewal increases of 19.7% in Q3 - up significantly from the 8.3% in Q2 - and allaying one source of concern from last quarter's results. Comparable occupancy stood at 93.7% - down 60 bps from last year, but up 10 bps from the prior quarter.

{kind=link}

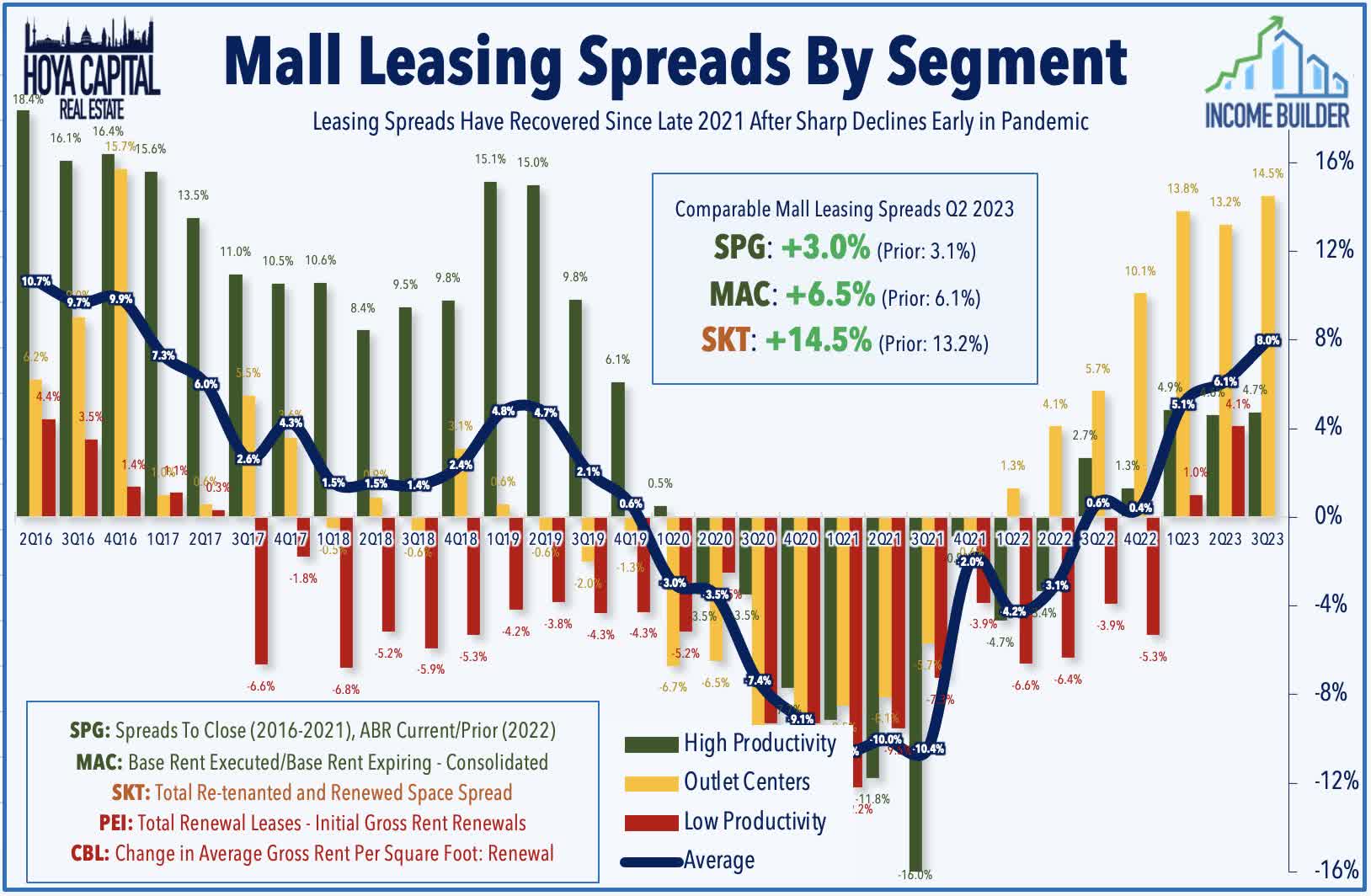

Winner #5: Regional Malls

Malls : (Final Grade: A-) Earnings results were also fairly impressive in the long-troubled regional mall space. While not displaying the outright strength seen in the strip center format, mall fundamentals have stabilized in recent quarters with occupancy rates rebounding to the cusp of pre-pandemic levels while rental rates have turned firmly positive following a dismal stretch of negative growth from late 2019 through mid-2022. Simon Property (SPG) - the largest mall owner in the nation- raised its full-year outlook to levels that are now 3% above the 2019 baseline. Lifted by a recovery in occupancy rates to over 95%, SPG now expects full-year FFO growth of 0.3% at its revised midpoint, which would be 1.3% above its full-year 2019 FFO. While SPG no longer provides leasing spread metrics, it reported that its base rents increased 2.9% and commented that "tenant demand is strong, occupancy is increasing, and base minimum rent levels are at record levels."

{kind=link}

Tanger Outlet (SKT) also reported strong results and lifted its full-year outlook driven by a continued recovery in occupancy rates and an acceleration in rent spreads. Tanger now expects FFO growth of 4.9% this year - up 190 basis points from its prior outlook - but still about 17% below full-year 2019 levels. Comparable occupancy climbed to 98.0% - the highest since 2016 and up 160 basis points from last year - which has driven year-to-date NOI growth of 6.5%. Leasing activity and rent growth has also been impressive in recent quarters following a stretch of nearly three years of negative rent spreads. Tanger reported blended spreads of 14.5% on a cash basis - the strongest since 2016 and marking the seventh-straight quarter of positive spreads. Macerich (MAC) reported in-line results and maintained its full-year FFO outlook, which calls for an 8.2% decline. Rent spreads and occupancy trends continued to trend in a positive direction, with blended leasing spreads of 10.6% in Q3 - its second-straight quarter of double-digit increases. Occupancy rose to 93.4% - still below the pre-pandemic average of around 94.5% - but up 80 basis points from last quarter and 170 basis points from last year.

{kind=link}

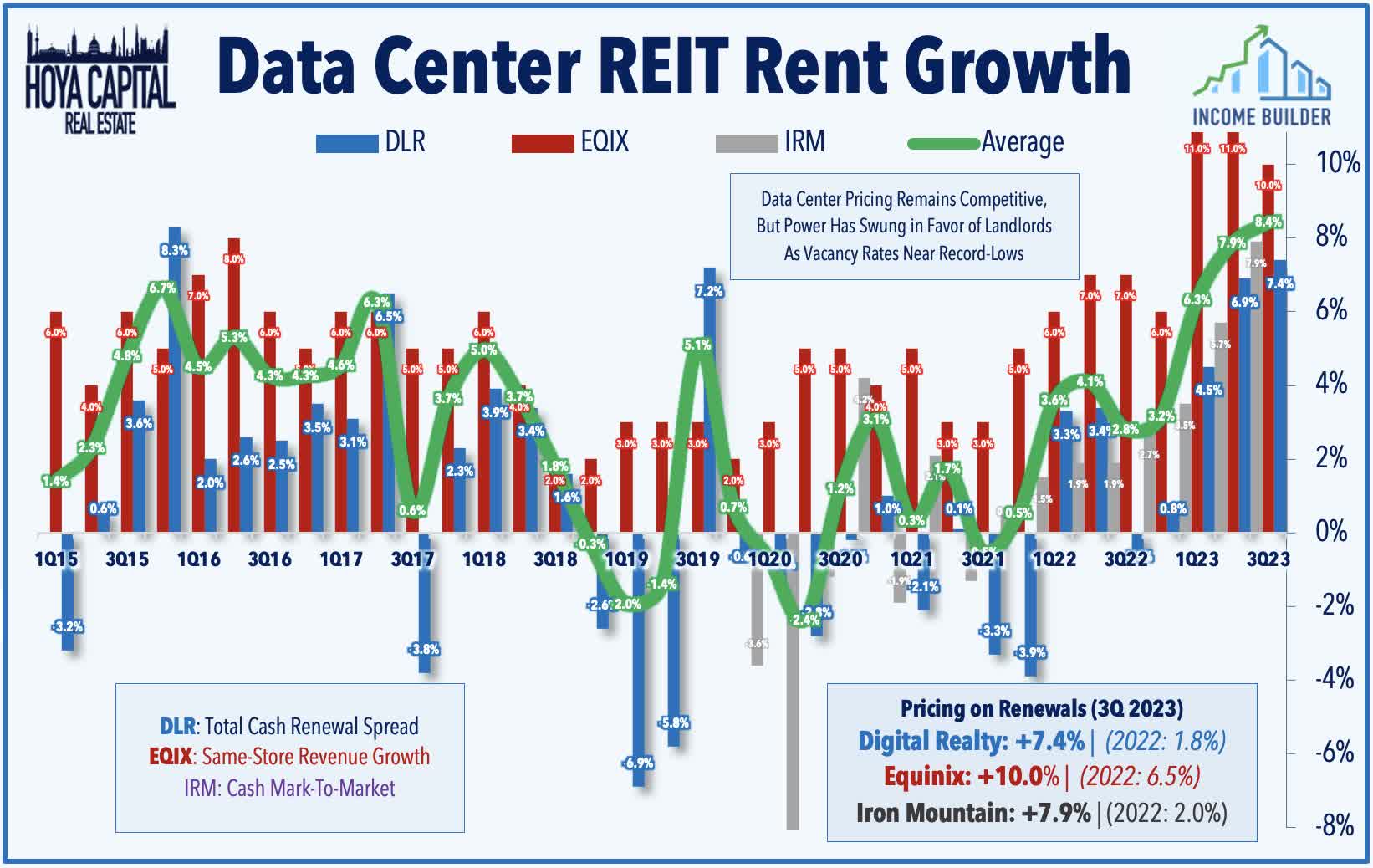

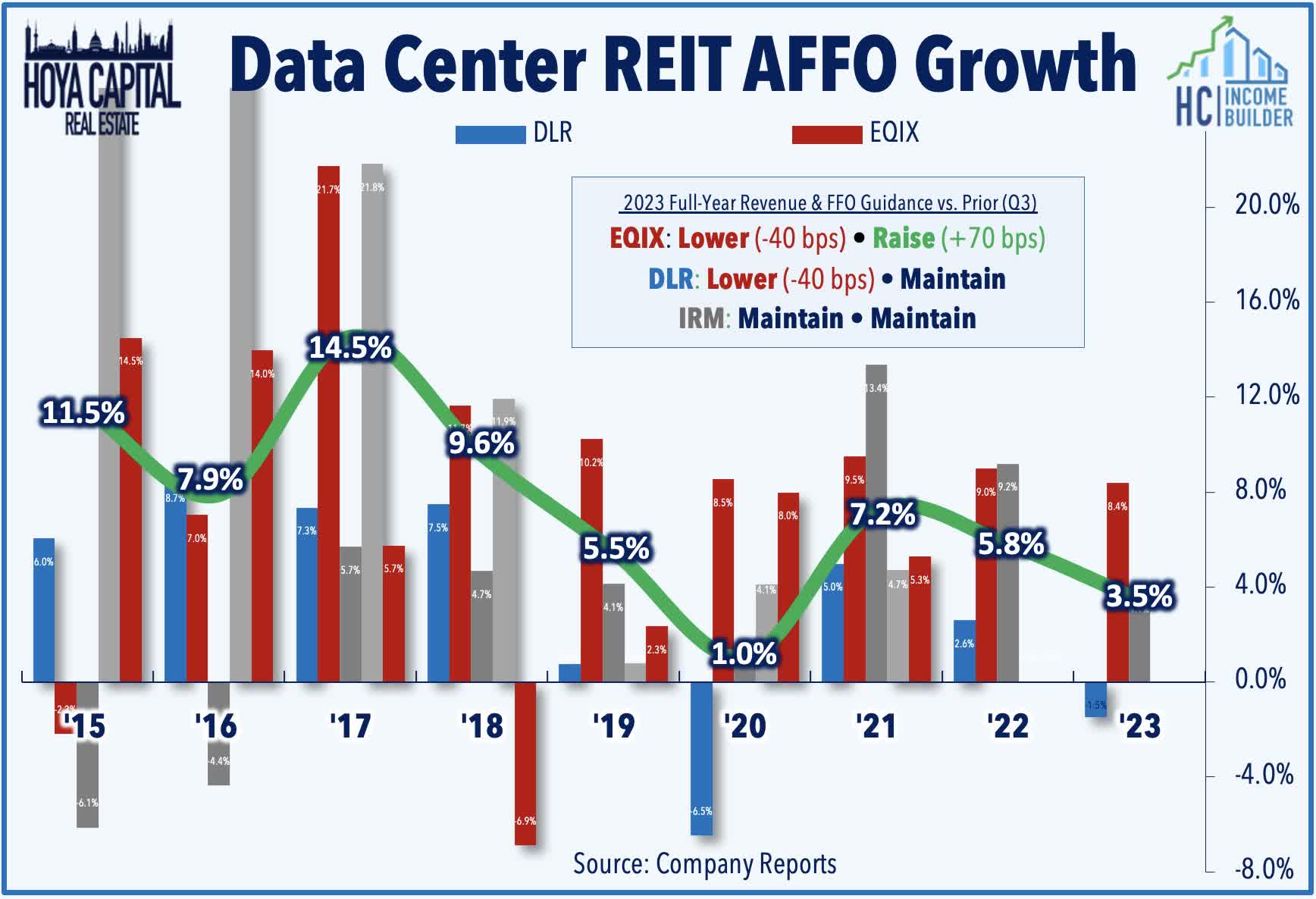

Winner #6: Data Centers

Data Center : (Final Grade: B+) Pricing power remained impressive for data center REITs as AI-driven demand has clashed with a confluence of development bottlenecks - power shortages, higher cost of capital, supply chain constraints, ecopolitics, and NIMBYism - to create a more favorable dynamic and swung the pendulum of pricing power towards existing property owners. Digital Realty (DLR) has been an upside standout after reporting strong results, with robust underlying pricing and AI-fueled demand trends partially offset by currency headwinds. DLR reported total bookings of $152M - its strongest quarter of leasing activity in a year - and achieved renewal rent growth of 7.4% - its best quarter for pricing since 2015. DLR now expects 5.0% rent growth on renewals - up from 4.0% last quarter - and expects same-capital cash NOI growth of 6.5% - up from 4.5% last quarter. DLR has been an active seller this year, raising $2.5B through non-core asset sales and joint venture monetizations in an effort to bolster its balance sheet and reduce its variable rate debt exposure, which remains relatively elevated at 14% of total debt. Underscoring this rate headwind, DLR maintained its guidance that its FFO will decline 1.5% this year despite a 17.2% jump in revenues.

{kind=link}

Elsewhere across the sector, Equinix (EQIX) reported similarly solid results and raised its dividend by 25% to $4.26/share (2.5% dividend yield). EQIX now expects its full-year FFO to increase by 8.4% - up 70 basis points - while its revenue outlook was trimmed on FX adjustments and interest rate impacts. EQIX commented, "Demand remains strong. New logo growth is accelerating. Our pricing dynamics are very positive given the tight supply environment across many of our metros." Iron Mountain (IRM) maintained its full-year outlook across both its business storage and data center segments but noted impressive rent growth on its data center leases at 7.9% - its highest on record. IRM leased 65 megawatts of additional capacity in Q3 - all to a single Fortune 500 technology company - lifting its full-year leasing total to 120 MW, already exceeding its initial full-year guidance of 80 MW.

{kind=link}

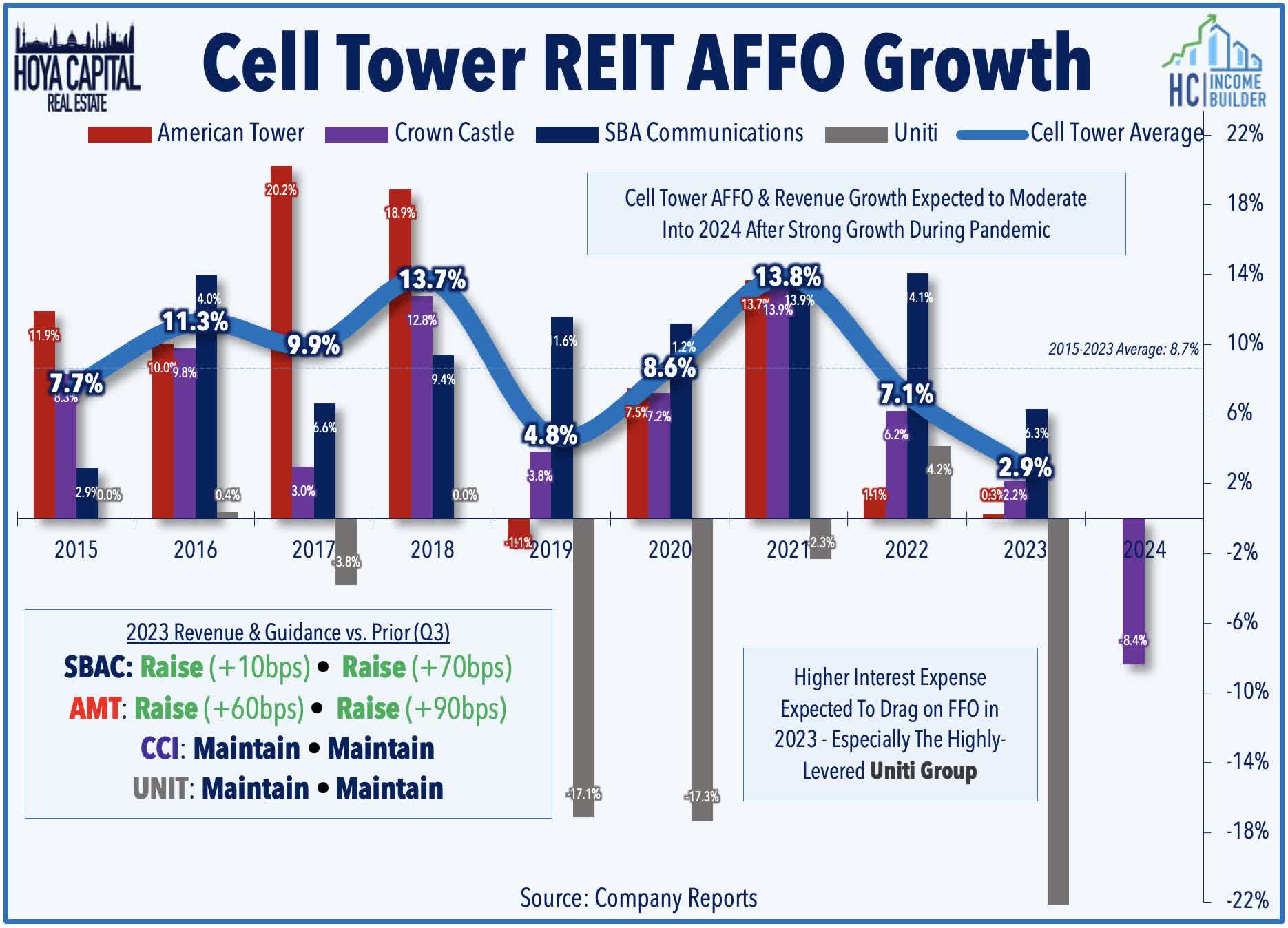

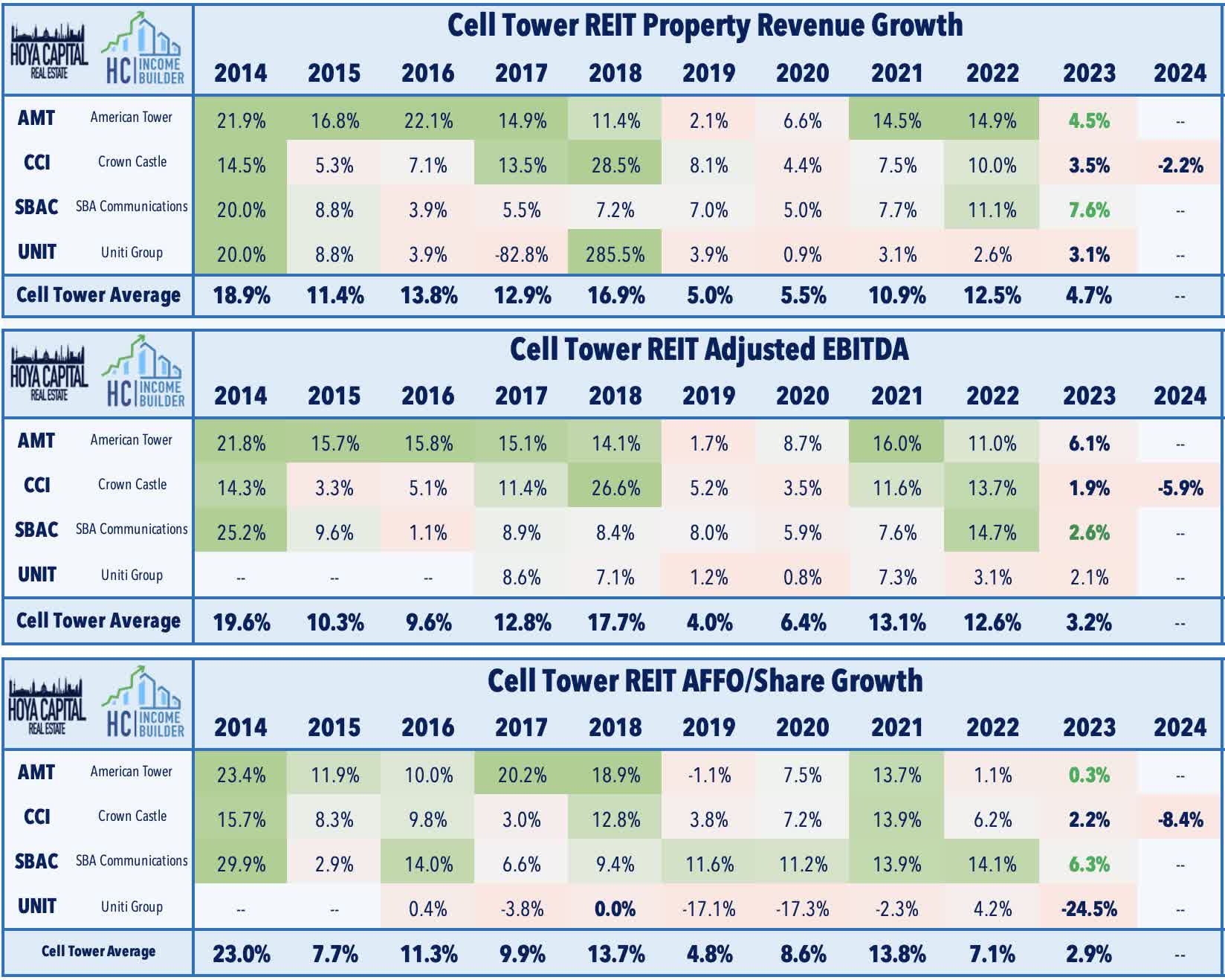

Winner #7: Cell Towers

Cell Tower : (Final Grade: B+) We observed similar trends of solid pricing power across the cell tower space. American Tower (AMT) has been the upside standout after reporting strong results and raising its full-year outlook while pushing back on concerns over a broader industry slowdown and noting the outperformance of its newly acquired data center business. Driven by domestic same-store ("organic billings") revenue growth of 6.3% - an acceleration from the 6.2% reported last quarter - AMT increased its full-year FFO growth target to 0.3% at the midpoint - up 90 basis points from its prior outlook. While AMT did not provide a full 2024 outlook, it noted that it expects continued same-tower revenue growth of "at least 5% in the U.S. and Canada segment between 2023 and 2027." Crown Castle (CCI) reported mixed results, maintaining its full-year 2023 outlook, but provided a downbeat initial 2024 outlook driven by higher interest expense. CCI continues to expect FFO growth of 2% this year, but forecasts an 8% decline in FFO in 2024, commenting that it expects the "low-point of AFFO to occur during the first half of 2024, with growth expected in the second half of the year and beyond."

{kind=link}

Despite having an investment-grade balance sheet with 86% of its debt at fixed interest rates, Crown Castle's updated outlook notes that interest expense is still expected to soar 22% in 2023 from a year earlier - amounting to a $0.35/share negative impact - and is expected to rise by another 12% in 2024 - an additional $0.12/share drag. As with AMT, property-level metrics remain steady, with CCI forecasting organic growth (excluding Sprint cancellations) of 4.8% next year - up from 4.1% in 2023 - comprised of 4.5% growth from towers, 13% from small-cells, and 3% from fiber. Elsewhere, SBA Communications (SBAC) lifted its full-year outlook across the board, commenting that "the growth in wireless demand is not slowing down and networks will continue to be strained, and our customers still have significant mid-band spectrum holdings that need to be deployed with little additional spectrum plan for release anytime soon...Macro tower sites are still the most efficient and effective way to deliver wireless connectivity."

{kind=link}

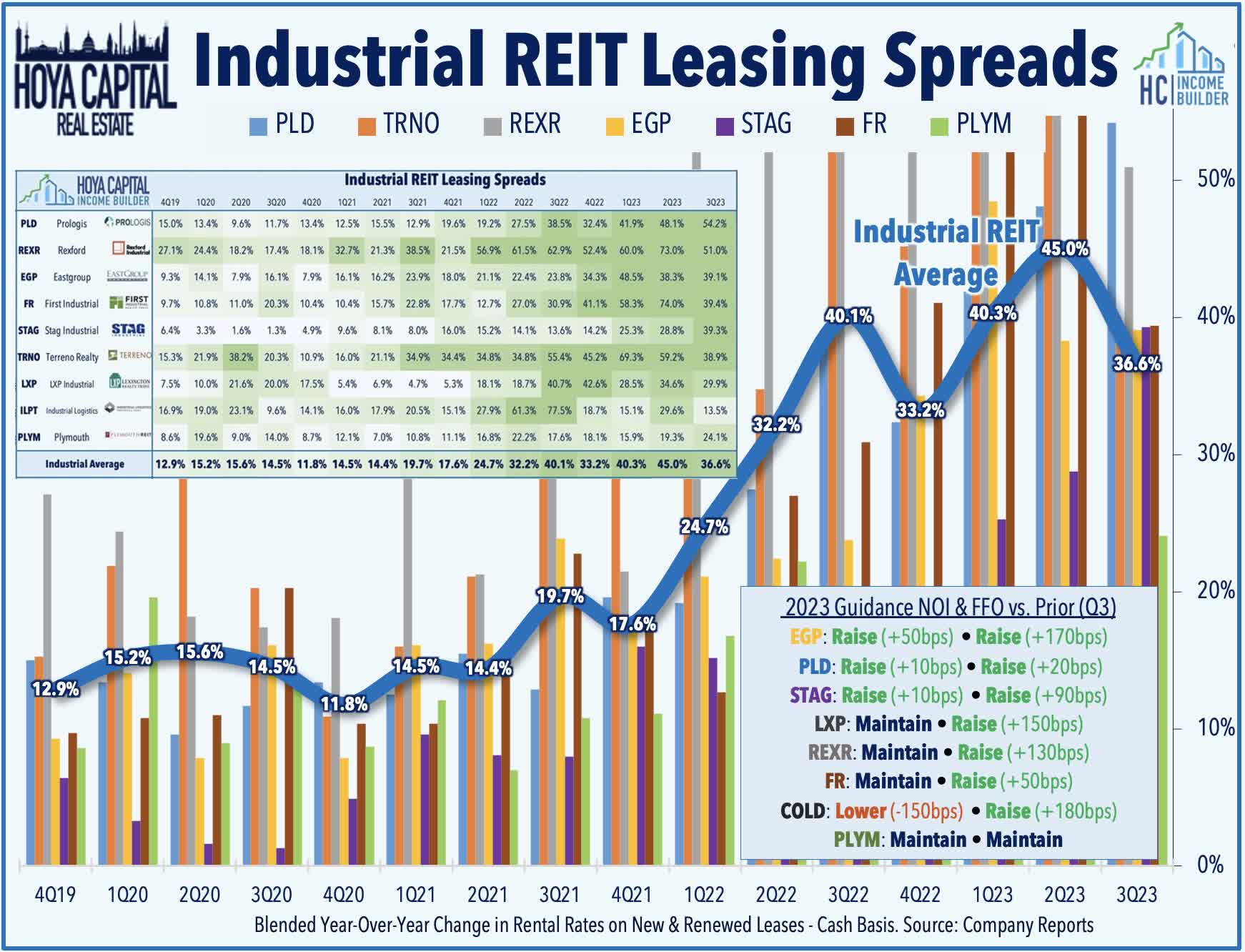

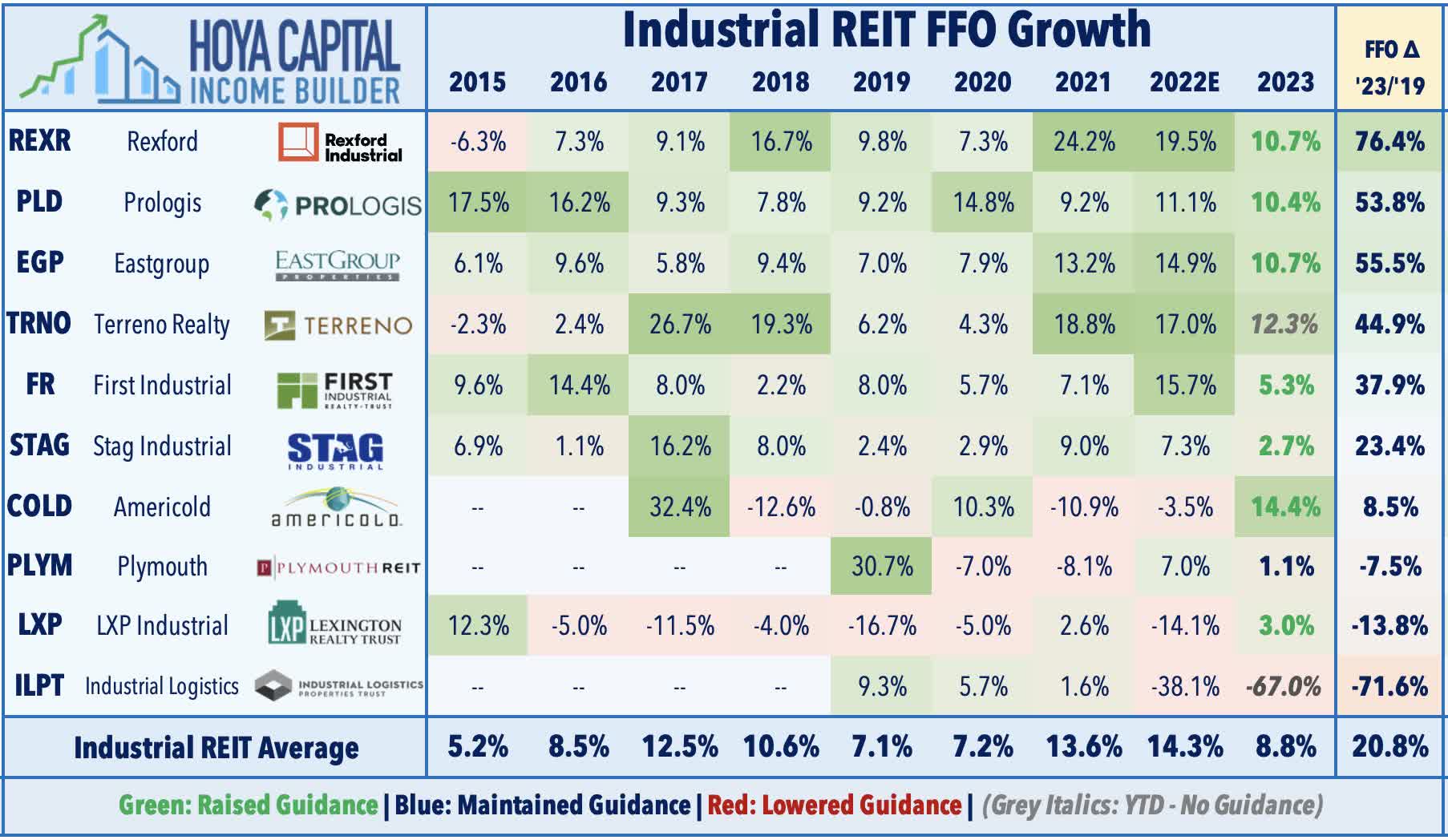

Winner #8: Industrial

Industrial : (Final Grade: B+) While not reflected in the relatively weak stock price performance during earnings season, industrial REITs reported another impressive slate of earnings results, with seven of the eight REITs raising their full-year outlook. Prologis (PLD) - the industry bellwether - reported "beat and raise" results but reiterated its expectation that elevated supply growth will negatively impact market fundamentals in the coming quarters and noted pockets of weakness in its Southern California markets. A common theme across the sector this earnings season, this cautious commentary was really nowhere to be seen in the third-quarter metrics or the updated full-year outlook, which continued to reflect extremely strong supply/demand conditions for logistics space, especially in the United States. Fueled by a record-setting cash re-leasing spread of 63.1% in the US, Prologis now sees FFO growth of 10.4% this year - up 20 basis points from its prior forecast - and expects NOI growth of 9.9% - up 10 basis points. Rexford (REXR) - which focuses exclusively on the Southern California region - has been a notable laggard after reporting mixed results, raising its full-year FFO outlook but recording a sequential deceleration in leasing activity. REXR noted that it leased 1.5M SF in Q3 with cash rent increases of 51.4% - down from the 74.8% increase achieved on 2.1M SF of activity in the prior quarter.

{kind=link}

Outside of Southern California and a handful of coastal metros, however, demand continues to outstrip supply. Sunbelt-focused EastGroup ( EGP ) has been an upside standout, reporting strong results and raising its outlook. EGP now expects full-year FFO growth of 10.7% - up 170 basis points - and expects same-store NOI growth of 7.8% - up 50 basis points. Bucking the trend of moderating leasing spreads seen across other industrial REITs, EGP reported an acceleration in cash leasing spreads to 39.1% in Q3, up from 38.3% in the prior quarter. EGP also upwardly revised its full-year occupancy outlook to 97.9% at the midpoint, up from 97.8% last quarter. EGP's commentary was notably upbeat, remarking that the "day-to-day industrial market remains resilient" and noted that it has seen a material decline in new construction starts this year. STAG Industrial (STAG) reported similarly solid results and raised its full-year outlook. Leasing activity and rent growth were particularly impressive, with STAG recording record-high blended cash leasing spreads of 39.3% on 2.3M square feet of space in the third-quarter. STAG now expects full-year FFO growth of 2.7% - up 90 basis points - and expects same-store NOI growth of 5.4% - up 30 basis points. STAG noted that it believes its Sunbelt-heavy portfolio in secondary markets is particularly well-positioned given the period of elevated supply growth that will persist through mid-2024.

{kind=link}

Winner #9: Billboard

Billboard : (Final Grade: B+) The "biggest loser" of second-quarter earnings season, billboard REITs have soared 20% since the start of earnings season as results exceeded the downbeat forecast provided in the prior quarter. OUTFRONT Media ( OUT ) has soared nearly 40% this earnings season after reporting stronger-than-expected results, with strength in its traditional billboard segment offsetting continued struggles in its transit advertising business. OUT noted that billboard revenues grew 2.6% year-over-year - driven largely by digital billboard conversions - while transit revenues declined nearly 9%. OUT noted weak advertising demand from national television and technology companies but reported that its local business segment performed "extremely well" with revenue growth of 6%. Lamar Advertising ( LAMR ) also reported solid results and raised its full-year outlook. LAMR expects to "reach or slightly exceed the upper end" of its guidance, implying that its FFO will be roughly flat this year, up from its prior outlook calling for a roughly 2% decline. LAMR reported similar industry trends, with local and regional revenues posting 2.3% growth while national revenues decreasing 3.4%. LAMR reiterated that political spending will be a drag in Q4 compared to the record-spending levels in 2022, but that it has seen "strengthening" trends early in the fourth quarter, led by a rebound in the national segment.

{kind=link}

Takeaway: Strength From Unexpected Sources

While there were some of the usual suspects among the Winners of REIT Earnings Season - namely industrial and technology REITs - we also saw strength from unexpected sources: retail and hotel REITs. Resilient pricing power remained a common thread across most property sectors throughout earnings season, while surprisingly solid demand in many of the most pro-cyclical sectors was a takeaway from the back-half of earnings season. As predicted, REIT M&A was also a major theme this earnings season, and most of the top-performing REITs this year have mid-caps and small-caps that have been those that have been scooped up by their larger peers - a trend that we expect to continue into early 2024. Expense growth remained stubbornly persistent for residential REITs - which were responsible for the majority of the downward NOI revisions this quarter - with insurance and property taxes rising by double-digits across most markets and segments - themes that we'll discuss in Losers of REIT Earnings Season later this week.

{kind=link}

For an in-depth analysis of all real estate sectors, check out all of our quarterly reports: Apartments , Homebuilders , Manufactured Housing , Student Housing , Single-Family Rentals , Cell Towers , Casinos , Industrial , Data Center , Malls, Healthcare , Net Lease , Shopping Centers , Hotels , Billboards , Office , Farmland , Storage , Timber , Mortgage , and Cannabis.

Disclosure : Hoya Capital Real Estate advises two Exchange-Traded Funds listed on the NYSE. In addition to any long positions listed below, Hoya Capital is long all components in the Hoya Capital Housing 100 Index and in the Hoya Capital High Dividend Yield Index . Index definitions and a complete list of holdings are available on our website.

{kind=link}

For further details see:

Winners Of REIT Earnings Season