WTFC - Wintrust Financial: Management Is Optimistic But I Remain Doubtful

2023-06-16 00:26:08 ET

Summary

- Wintrust Financial Corporation has managed to generate increasing net interest income and net interest margin in the current macroeconomic environment, with a focus on capital levels and efficiency ratios.

- Concerns arise from the bank's high exposure to Commercial Real Estate loans and the deteriorating deposit composition, which could affect profitability.

- Despite appearing undervalued, the uncertainties and risks involved make Wintrust Financial not a buy recommendation.

After SVB's bankruptcy, the entire banking industry came under pressure, but not all banks reacted in the same way. Over the past few weeks I have focused my attention mainly on the less popular ones, and in this article it is the turn of Wintrust Financial Corporation ( WTFC ), a financial holding company founded in 1991 and headquartered in Rosemont, Illinois.

Based on the latest available financial data , in this article I will analyze its main strengths and weaknesses based on the current macro environment; I will conclude with an evaluation of its fair value.

Main strengths

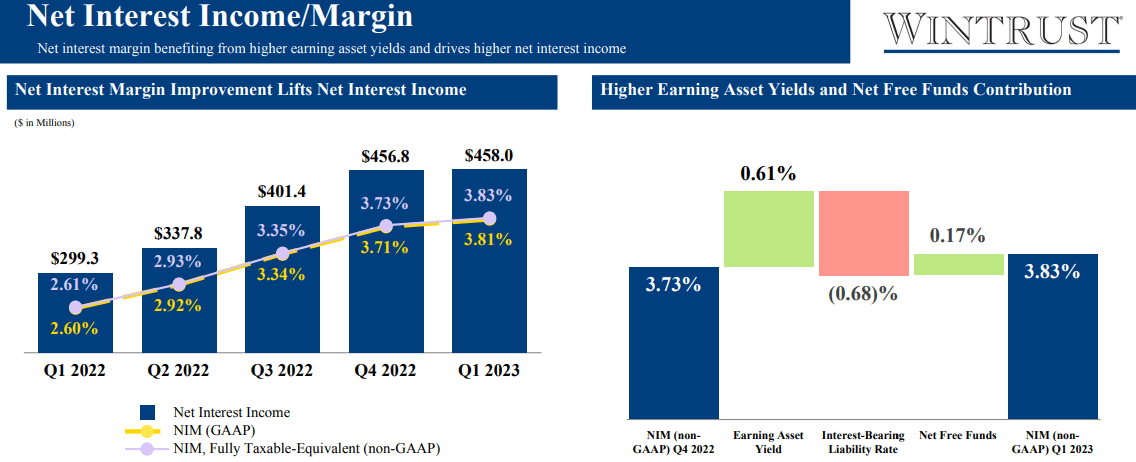

One of the most positive aspects of Wintrust Financial is that it has managed to generate increasing net interest income and net interest margin in the current macroeconomic environment.

{kind=link}

With a Fed Funds Rate at 5-5.25%, it is not a given to achieve this given the rising cost of money. It is no longer possible to offer deposits with rates close to 0%; now depositors are demanding much more since the T- bill yields around 5%.

If Wintrust Financial was able to achieve this result, it is because the upward repricing of earning assets outpaced increases in total funding cost. Specifically, the positive/negative factors that affected the net interest margin improvement of 10 basis points are:

- 61 basis points from the higher yield on assets

- (0.68) basis points due to the rising cost of interest-bearing liabilities.

- 17 basis points coming from net free funds, which is the difference between total average earning assets and total average interest-bearing liabilities.

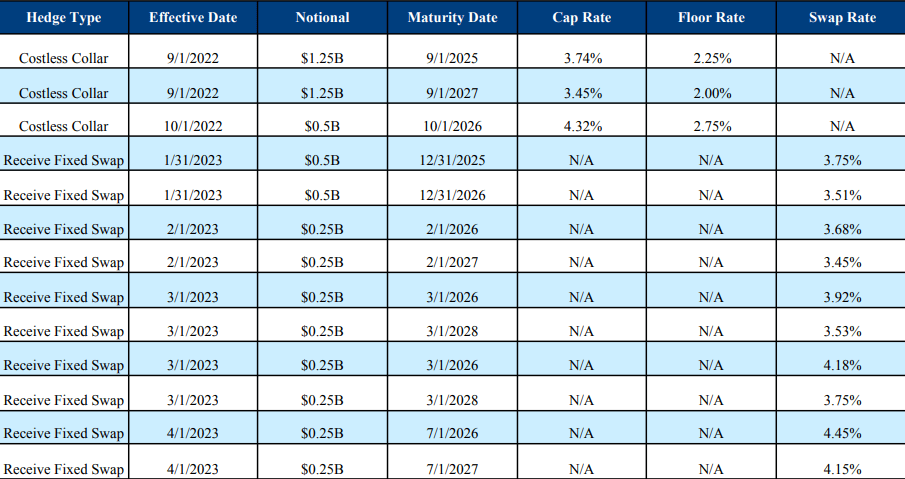

In any case, it is worth noting that the net interest margin would have increased by an additional 7 basis points if the bank had not decided to buy derivatives to hedge against a possible decline in interest rates.

{kind=link}

Over the past few months, multiple fixed swaps have been purchased to reduce the volatility of overall performance . Future interest rate trends will have less weight on the net interest margin, which will therefore be more limited on both improvements and deteriorations. The goal is to act prudently, and the guidance for the net interest margin for the coming quarters is 370 basis points. This forecast, includes an additional 8 basis points increase on the current cost of derivatives used for the purpose of hedging against interest rate movements.

Personally, I think it will not be easy to meet the guidance and maintain such a high margin if the Fed Funds Rate remains high for a long time: the cost of deposits could rise too much. At the last meeting, the Fed hinted that there could be two more rate hikes during the year and gave no hope on a cut as early as 2023. In other words, Wintrust Financial is sacrificing marginality to hedge against the risk of falling rates, but this seems highly improbable at the moment.

{kind=link}

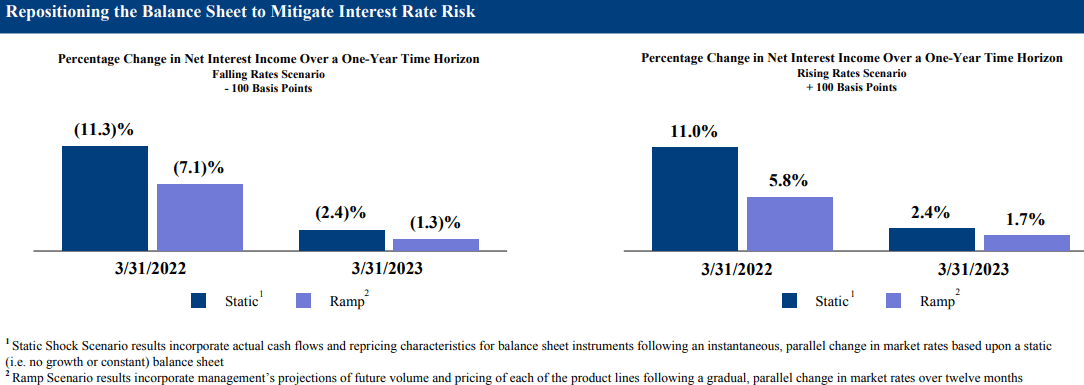

In any case, it would be wrong to believe that the bank is entirely positioned in favor of a rate cut. Under these two scenarios, net interest income would increase only in the event of a 100 basis point increase in the Fed Funds Rate and worsen in the event of a 100 basis point decrease. So, the purchase of fixed swaps does not change the bank's approach to the macroeconomic environment, it simply downgrades its outcomes, whether positive or negative. Given the uncertainty of the period, I find it understandable to sacrifice marginality slightly to increase prudence.

Two other aspects that I found positive analyzing the latest financial results are the capital levels and the efficiency ratio.

Wintrust Financial Corporation Q1 2023

The capital requirements imposed by the Basel Committee are all widely met. In particular, this quarter's record profits gave a further boost to CET1, which has improved by 600 basis points overall since Q1 2022.

What's more, according to management's estimates, the minimum capital requirements would be met even in the unlikely event that regulations change. In fact, even if unrealized losses in the investment portfolio were to go into regulatory capital deduction, the bank would still meet the mandatory requirements. In short, it would survive, but it would be significantly weakened given that total pre-tax unrealized losses amount to $1.11 billion, about 22% of equity.

Wintrust Financial Corporation Q1 2023

Finally, the last topic in this section is about the efficiency ratio.

Wintrust Financial Corporation Q1 2023

The ratio has fallen quarter by quarter and is currently 52.78%, an excellent result. The lower this ratio is, the better. This shows how well Wintrust Financial managers control their overhead.

Weaknesses and doubts about the future

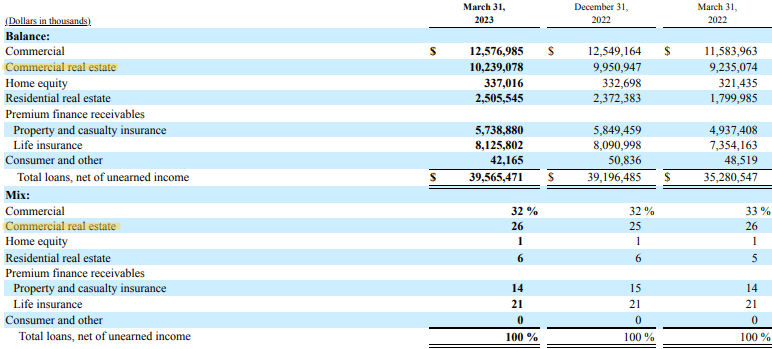

Previously, I had stated that the growth in yield on assets together with net free funds had managed to cover the increases in the liability cost, which is true. However, I did not specify what is driving this growth and the composition of the loan portfolio.

{kind=link}

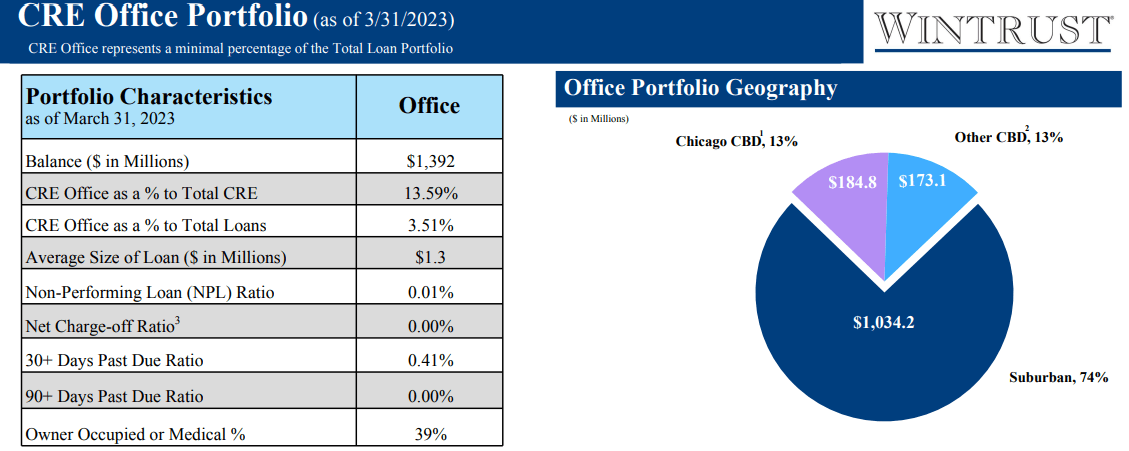

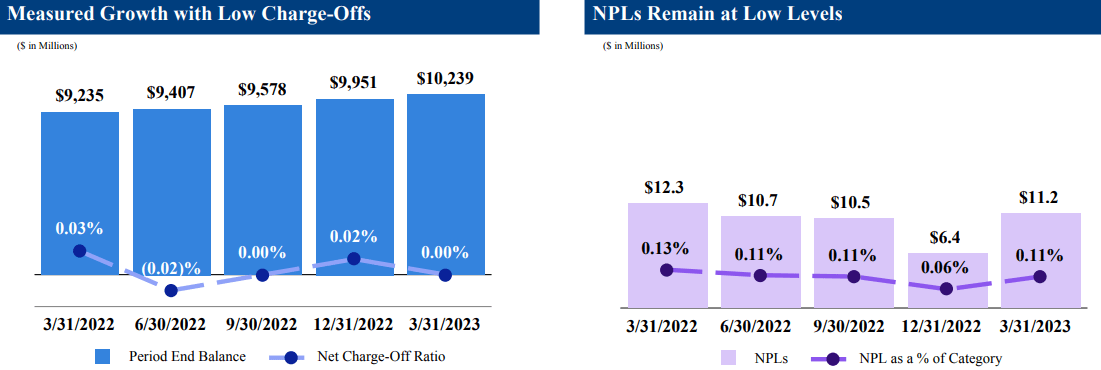

Commercial Real Estate [CRE] accounts for 26% of the loan portfolio, which by the way is also the fastest growing segment, $288 million more than in Q4 2022. Overall, this is quite a large exposure, and considering its riskiness, there is quite a bit of doubt as to how the situation will evolve. In addition, CRE office exposure is about 3.51% of total loans.

{kind=link}

Overall, management does not seem at all concerned about the composition of the loan portfolio; in fact, judging from the words during the conference call of CLO Richard Murphy the exact opposite appears to be the case. Beyond the type of loan required, Wintrust Financial is always ready to take advantage of an opportunity:

Would we do another office deal?

Absolutely, if it's structured the right way. We've got the right tenant mix, and we've got the right borrower, and we've got the right collateral structure. So we are trying to be very thoughtful, I think, as we talked about here, the granularity of our portfolio and the way it's structured allows us that flexibility. If I had a portfolio that was 50% CRE and most of that office, I'd feel a lot different. But right now, we are just trying to be opportunistic and also be really thoughtful about keeping dry powder for our customers.

Currently the data prove him right, in fact CRE NPLs remain at very low levels. However, in my opinion it is too early to say that the rate hike has not had negative consequences for borrowers. Several more months are needed before the consequences of tight monetary policy can be assessed.

{kind=link}

Finally, the last aspect I will discuss is the deposit composition, which is getting worse.

Wintrust Financial Corporation Q1 2023

The overall amount has not varied much, only by ($200 million); the problem is that non-interest-bearing deposits have gone from being 30% to 26% in about 3 months. The latter are the best source of funding being costless, and if they decrease they will be replaced by onerous liabilities. Of course, this all affects profitability accordingly.

During the conference call , David Long asked President Timothy Crane a very interesting question on this topic. Briefly, he was asked if he thought that non-interest-bearing deposits could return to their historical average (15-16% of total deposits) experienced before the great financial crisis. In fact, we are coming from 15 years of rates close to 0%, which may have accustomed depositors to settle for less and this definitely favored the banks. Here is his response:

Well, I think for us, the structural change has been the growth of our commercial businesses. And so they carry with them DDA deposits related to paying for both treasury services and excess. So I would hope that we don't go back that low and that we've got some very material differences in terms of how we looked pre-2008 or 2010. But clearly, the events of the second half of March have everybody to looking at their deposits very carefully. And so those conversations continue around the bank.

In short, it is difficult to understand the evolution of deposit composition, but everything points to a deterioration at least as long as rates remain high. After all, the deposit beta is currently 26% but is expected to be around 50% in the future.

It will be important to understand whether the higher cost of deposits will be offset by yields on assets without compromising the riskiness of the loan portfolio too much. At present, the bank is increasingly exploiting the CRE segment, but it is evident that its weight is already high.

Finally, the loan to deposit ratio in Q1 2023 was 92.62%, in Q1 2022 it was 83.58%. The bank has repeatedly stated that it does not want this ratio to reach 100%, probably not even 95%. We are very close to the maximum threshold, so new deposits will be needed in order for new favorable loans to be made. This is a complicated situation that will remain so as long as the Fed Funds Rate remains high.

Evaluation and final thoughts

Typically, I use discounted cash flow to calculate the fair value of a company, however, this would be misleading in this case. For a bank, it is equity growth that is the most important aspect as it reflects the ability to succeed in improving minimum capital requirements and increasing shareholder value. Thus, to understand what a bank is worth, it is necessary to analyze its book value.

In the case of Wintrust Financial the average Price/Book Value [TTM] over the past 5 years is 1.14x; multiplying this figure by the current Book Value per share of $75.24, the fair value amounts to $85.77 per share . In short, according to this calculation Wintrust Financial appears undervalued at first glance, but I personally do not consider it a buy.

Although the net interest margin is stable so far, the uncertainties are many and the expected sharply rising deposit beta could erode the margin more than predicted. Also, although management is quiet now, I prefer not to have exposure to banks with such a high percentage of CRE in their portfolio. In short, I don't think there is such a strong undervaluation to justify a buy given the risks involved.

For further details see:

Wintrust Financial: Management Is Optimistic, But I Remain Doubtful