WTFCP - Wintrust Preferred: High Yield To Redemption Opportunity

2023-03-21 14:21:36 ET

Summary

- Wintrust's preferred shares trade at a discount to redemption value.

- The high reset rate margin makes it likely the preferred securities will be called in approximately two years.

- At recent quotations, a yield-to-call of 11% to 12% should be attractive to conservative investors.

Wintrust Financial Corporation (WTFC) is a $53 billion bank holding company primarily serving the Chicago metropolitan region and adjacent areas in southern Wisconsin and northern Indiana. Wintrust operates through 15 separate community banking subsidiaries and uses this structure to provide an opportunity for depositors to increase their effective insured deposits by distributing deposits across these institutions.

The company's preferred shares, which are our focus for this article, have been impacted by the recent turmoil in the banking industry. However, at the current quotation we consider the preferred shares a very compelling opportunity. The current yield of approximately 8.0% is attractive in its own right but is further boosted by the high probability that the preferred shares will be called for redemption in July 2025. The current quotation's discount to the redemption price plus the preferred dividend results in a potential annualized return through maturity approaching 11%-12% although the quickly moving nature of bank preferred share prices is a critical consideration.

Preferred Shares

The Wintrust Financial Corporation Series E preferred stock ( WTFCP ) is a series of non-cumulative reset rate preferred stock with a liquidation/redemption price of $25.00 per share. The preferred stock yields a fixed 6.875%, payable quarterly, until July 15, 2025, at which time the dividend rate is reset every five years at a premium of 6.507% over the then applicable rate on the five-year U.S. Treasury bond.

The preferred shares are redeemable at the company's option at the redemption price on July 15, 2025, and on July 15 every five years after the initial potential redemption date. In addition, the preferred shares are subject to potential redemption, as with many bank preferred shares, in the event that regulatory changes no longer permit the preferred shares to be included as a component of Tier 1 capital for regulatory purposes.

The preferred shares were originally issued on May 6, 2020, shortly after the beginning of the pandemic panic in markets which saw a number of companies seek to raise additional capital in an uncertain environment, thus the rather wide premium over five-year bond rates incorporated into the reset provision.

Issuer Strength

In assessing the attractiveness of bank preferred securities it's necessary to assess the strength of the issuer particularly in the current environment.

In doing so we adjusted the bank's consolidated calculations for capital adequacy ratios to include unrealized losses on investment securities which are excluded from regulatory capitalization calculations. In doing so, we estimate the bank would remain well capitalized by regulatory standards including all unrealized losses on both available-for sale and held-to-maturity investment securities as reported at the end of 2022. Specifically, we estimate that the company's adjusted Tier 1 capital to risk-weighted assets to be approximately 8.5% and the total capital to risk-weighted assets to be approximately 10.1%. However, we should note that our estimate for Tier 1 capital to risk-weighted assets falls slightly below the capital conservation buffer which essentially represents an increase in bank capitalization requirements; however, we do not consider this alone to be especially significant on the margin. In any event, the bank would retain capitalization ratios similar to or superior to many of its peers.

In addition, it's necessary to consider the proportion of total deposits represented by uninsured deposits as this can be an indicator of the potential for significant withdrawals in the event of a loss of confidence in the institution or the overall banking sector. Wintrust's percentage of uninsured deposits to total deposits is a little more difficult to assess since the company's financial statements only appear to provide a figure for uninsured certificates of deposit. In order to estimate overall uninsured deposits we looked to financial reports filed by each of the bank's subsidiary community banks, as reflected in the following table:

Uninsured Deposits (Winter Harbor Capital / FFIEC)

The total deposits reflected in the above consolidation of the company's various operating units differs slightly from that reported in the company's financial statements due to cross deposits between institutions which are eliminated on consolidation. In any event, we estimate that the company's proportion of uninsured deposits is approximately 42% - slightly above the 30% to 35% range common among smaller community banks but still reasonable below the 50% to 65% range common among regional banks.

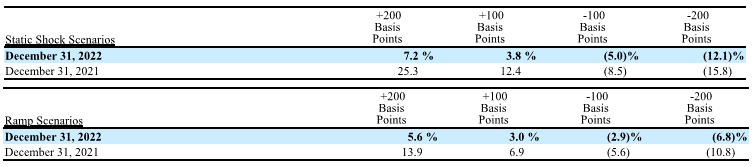

Moreover, the bank's asset/liability composition, interest rate sensitivity, and operating performance are all consistent with a strong regional lender. We will refrain from a detailed assessment of the company's overall performance as that is not a specific focus of this article but we will note that the company's interest rate sensitivity insofar as net interest income is concerned has been reduced over the last year and falls within a range which we consider quite acceptable for a financial institution of this type:

Wintrust Interest Rate Sensitivity (Wintrust Annual Report (10-K))

{kind=link}

In addition, preferred shares represent less than 10% of total shareholders' equity providing a robust capital margin for holders of the preferred shares.

Probability of Redemption

The rather wide margin associated with the rest rate - 6.507% over the applicable five-year treasury rate - reflects the pandemic conditions under which the company issued the preferred stock. The applicable margin for similar preferred shares under more normalized conditions (disregarding the current turmoil in the banking industry) would likely be closer to 4.0% to 5.5% consistent with recent reset rate preferred stock issued by Ellington Financial (EFC.PR.C) (which we consider to be an inferior institution based on the nature of its business) and Merchants Bancorp (MBINM) yet above the reset rate associated with Associated Banc-Corp's recently issued subordinated notes. Notably, prior to the recent banking concerns, the preferred shares were trading at a slight premium to redemption value and a yield closer to 6.75%. In the event the preferred share dividend rate was to adjust in today's market, even considering the recent decline in yields, the dividend reset rate would approach an incredible 10%.

In the event the company did not call the preferred shares for redemption in 2025, preferred shareholders would likely secure a robust preferred dividend yield for the next five years until the next potential redemption date.

We therefore view a redemption of the preferred shares in 2025 as highly likely assuming interest rates do not significantly decline in the next two years. Indeed, even if rates decline over the next two years, we consider a redemption still more likely that not given the dividend premium. In the event the preferred shares are redeemed, based on the current market quotation, the compound average annual return to preferred stock holders (yield to redemption) would be approximately 11%-12%.

Conclusion

The preferred shares at the current market quotation provide a robust compound yield to redemption of approximately 11%-12%. In combination with Wintrust's financial position, current market environment, and relatively short duration until the preferred shares likely redemption, we believe the preferred shares represent a very compelling opportunity, particularly for income-oriented investors, disproportionate to the realistic company and market risks.

For further details see:

Wintrust Preferred: High Yield To Redemption Opportunity