WIT - Wipro: Growth In The AI Digital Age

2023-08-24 22:10:52 ET

Summary

- Wipro Limited is a global IT and consulting company offering a wide range of services.

- Wipro has achieved a revenue growth rate of 8%, slightly below the industry average, driven by technological developments such as Cloud-based solutions.

- We expect growth to remain strong, driven by factors such as AI, as businesses require support to incorporate the technology.

- Wipro's margins have poorly developed in the last decade, owing to increasing competition and the commoditization of the services it focuses on (Wipro does far less value-add services like Accenture).

- Wipro is trading in line with its historical average, which based on our analysis implies no upside.

Investment thesis

Our current investment thesis is:

- Wipro is a well-positioned business for continued growth as new technological developments, such as AI, drive IT investment within global businesses.

- Wipro's growth has been modest but with greater competition, margins have declined.

- Wipro performs well relative to its peers but its subpar growth and lack of value-add services means it is less attractive.

- Wipro's current valuation does not suggest upside, namely due to its lack of discount to its historical average.

Company description

Wipro Limited ( WIT ) is a global information technology, consulting, and business process services company. Headquartered in India, the company offers a wide range of services, including IT solutions, consulting, digital transformation, and business process outsourcing.

Share price

Wipro's share price performance has been underwhelming in the last decade, as modest financial development and a historically elevated valuation have left little room for expansion in its trading multiples.

Financial analysis

{kind=link}

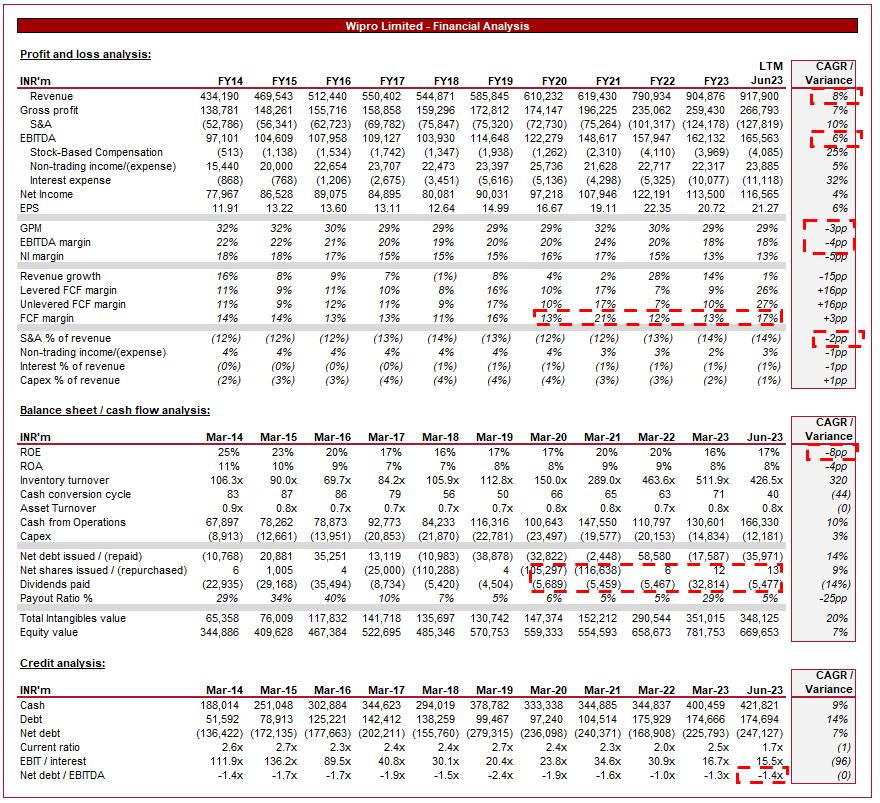

Presented above is Wipro's financial performance in the last decade.

Revenue & Commercial Factors

Wipro's revenue growth has been respectable during this period, with a CAGR of 8% into the LTM period. Growth has been relatively consistent, with only a single period of negative growth, illustrating the resilience of its business model.

Business Model

Wipro offers a wide range of IT services to clients across various industries. This includes application development and maintenance, infrastructure management, digital transformation, analytics, cloud computing, cybersecurity, and more.

Furthermore, the business has developed consulting services to help clients develop strategic plans, optimize operations, and implement technology solutions that align with their business goals. This is a natural progression from generic IT services, improving its profitability (greater value-add) while also further ingraining itself within its clients' operations.

Wipro's diversified portfolio of IT services has allowed the company to cater to a broad range of client needs. Global Management teams are increasingly seeking integrated solutions and "partners" to help their companies navigate a rapidly developing environment. Operationally, Wipro is able to maximize the value creation from its deep IT expertise through expanding its product offering. The wide breadth has allowed the business to target a range of industries. A secondary benefit of this is a reduced reliance on any single industry, softening cyclical impacts.

{kind=link}

Wipro operates on a global scale, serving clients in multiple regions and industries, much of which is defined as "offshore" (59.5% of revenue) rather than "Onsite". Its global delivery model allows it to provide cost-effective solutions while leveraging a diverse talent pool. Expansion overseas continues to represent a key opportunity for the business, particularly in emerging markets as they experience rapid digitalization. As of Q1-24, no single region represents over 30% of revenue.

Geography mix (Wipro)

Wipro builds long-term relationships with clients by delivering customized solutions, understanding their unique needs, and helping them navigate the complexities of technology adoption. The business has positioned itself to develop its services alongside the growth of its clients, rather than being single project-based. Wipro's largest customer represents 3.1% of revenue, with its top 10 representing 20.5%.

Revenue mix (Wipro)

Wipro strategically acquired companies that complemented its existing capabilities and expanded its service offerings, while also developing its expertise in new markets to ensure it remains ahead. In the last decade, the business has spent over INR250k of cash, supplementing growth. We expect this strategy to continue, particularly as Capex commitments are low.

Wipro's current "strategic priorities" are as follows:

- Accelerate growth - Prioritizing high-growth sectors.

- Strengthen clients and partnerships - Focus on winning transformational deals and strategic partnerships/M&A.

- Lead with business solutions - Scale within industry themes such as Cloud, AI, Industry 4.0, 5G, etc.

- Build talent @ scale - Upskilling and reskilling, as well as cultural development.

- Operational excellence - Internal transformation and delivery excellence.

All of these points are reasonable in our view. The key will be the focus on points 2 & 3, as these will drive 1.

IT Industry

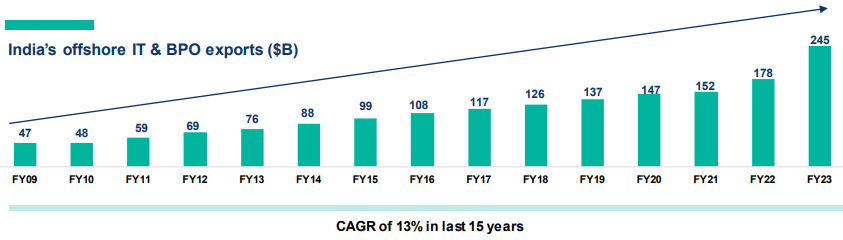

The rapid pace of technological change requires IT companies like Wipro to continuously adapt and invest in acquiring new skills and capabilities. Failure to keep up with emerging technologies can result in reduced competitiveness. India's offshore IT and BPO exports industry have grown at a CAGR of 13% in the last 15 years (interestingly Management disclose this statistic despite underperforming it).

{kind=link}

The current area of development, and what we consider to be the biggest development since the creation of the Internet, is AI. AI has the potential to propel businesses forward and improve the lives of much of society. Generative AI today can achieve improved efficiency, improvement in the personalization of services provided, and more greatly achieve reliable results (and this is across many differing industries). We do not consider this a short-lived trend.

Investors are piling cash into every AI company they can find but an attractive risk-based investment could be into an IT service businesses. Many Corporates will not have the expertise to utilize and implement this new technology, requiring support.

The shift from traditional IT infrastructure to cloud services and digital solutions has disrupted the traditional IT services model and is an illustration of the Corporate spending required to incorporate new technology (a roadmap of how AI incorporation could develop in the coming years). Companies have spent billions on the transition to Cloud-based solutions and will continue to do so, as more and more industries begin to see the value proposition. At first, mainly due to costs, this was a transition for tech businesses and a few others. Now, with the level of data accumulation and analysis, almost every business requires cloud solutions. We expect this to continue to be a value driver going forward.

Competitive Positioning

The Wipro brand is synonymous with high quality, affordable IT services. Many Corporates lack the expertise to make an informed decision, so will look to find options based on reputation and reviews.

Further, Wipro's emphasis on innovation and staying at the forefront of technological advancements has allowed it to offer cutting-edge solutions to clients. The company is positioned to outspend its competitors on R&D, with a current focus on emerging technologies like artificial intelligence, and industry-specific solutions. In 2023, the company was named a leader in "Data Center Outsourcing and Hybrid Infrastructure Managed Services Worldwide" by Gartner ( IT ).

Magic Quadrant (Gartner)

Finally, Wipro's other key competitive advantage is its scale. As a large, international business, it is positioned to service a range of companies in a flexible manner.

Despite its strong competitive position, Wipro's growth has been mediocre compared to the industry (11% above compared to 8.5%). Further, the wider technology sector has achieved far better growth.

The IT services industry is highly competitive, with numerous global and regional players vying for clients. This is not an industry where wide moats can be developed, contributing to margin pressures.

The availability of skilled talent is critical for IT services companies. Attracting and retaining top talent, especially in areas like artificial intelligence, data science, and cybersecurity, can be challenging, particularly with higher wage inflation and labor turnover (such as we are currently witnessing).

Wipro faces competition from several global IT services and consulting companies, including Infosys ( INFY ), Tata Consultancy Services, and Accenture ( ACN ).

Economic & External Consideration

With elevated interest rates and inflation, there is a risk of reduced IT spending as businesses see lower growth (thus need for support services) and are less likely to conduct transformational IT projects.

Wipro's revenue has declined QoQ although has maintained growth YoY, implying the business is experiencing a slowdown. There is a present risk that this continues in the coming 1-4 quarters, as interest rates remain high to combat inflation.

Q1 (Wipro)

Margins

Wipro's margins have declined in the last decade, with EBITDA-M falling 4ppts to 18% and NIM falling 5ppts to 13%.

The commoditization of certain IT services and competitive pricing have materially contributed to this margin pressure. With no clear evidence a bottom has been reached. Inflationary pressures are impacting labor, Wipro's primary cost base.

We believe a normalization at the current levels, an EBITDA-M of 18-20%, is reasonable to expect but there is a heightened risk of further deterioration.

Balance sheet & Cash Flows

Wipro's ROE has gradually declined due to the fall in NIM but its FCF margin has remained robust, allowing the business to generate a high amount of cash.

Management's capital allocation strategy is "Japanese" in nature. The company has a high cash balance (almost 50% of revenue!), low distributions, and a large net cash position. This business is less cyclical than most, has sticky revenue, and low cash commitments, implying it can operate with a moderate level of debt and a lower cash balance (although appreciating that it is a project-based business and so a heightened level of cash may be needed).

This means distributions could significantly increase but there seems to be an unwillingness to, contributing to an inefficient business for shareholders.

Industry analysis

{kind=link}

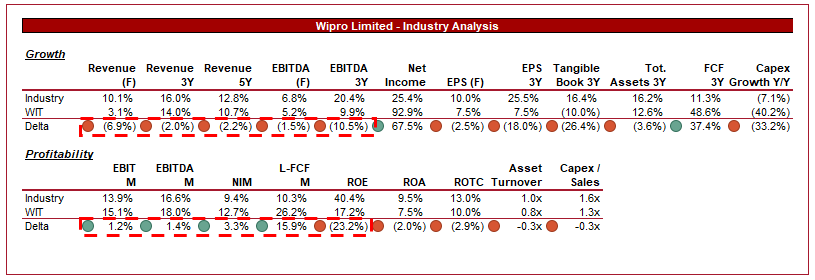

Presented above is a comparison of Wipro's growth and profitability to the average of its industry, as defined by Seeking Alpha (18 companies).

Wipro performs well relative to its peers. The company's key area of weakness is growth, with a clear revenue delta that is expected to widen on a forward basis. This is partially due to its size, making it difficult to achieve the absolute gains required. The business is comparable on a 5Y basis to similarly large businesses such as Accenture, Gartner, Infosys, and Capgemini ( CAPMF ).

Further, Wipro's area of strength is its margins, with a small premium across profitability metrics, a large premium in FCF, and a large discount in ROE. The FCF superiority is based on the timing of cash receipts and so if we took its normalized level of c.11%, the business is far more comparable.

Valuation

{kind=link}

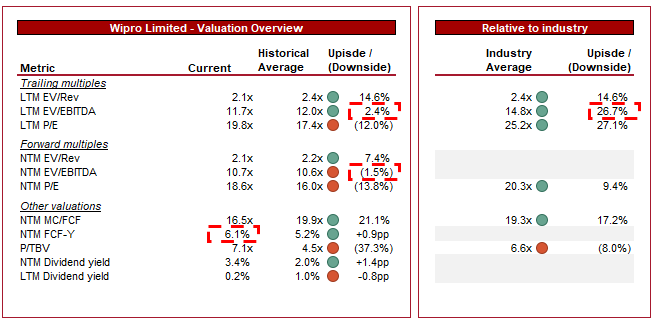

Wipro is currently trading at 12x LTM EBITDA and 11x NTM EBITDA. This is a discount to the industry average.

Wipro is trading at a small premium to its LTM EBITDA historical average and a premium to its NTM EBITDA average. This difference is likely due to the unexpected QoQ growth weakness (and the widening relative to peers), with investors likely expecting a swift improvement. Our view is that a small discount to its historical average is warranted, owing to the increased competition and margin reduction. AI represents a key opportunity but it will partially replace the Cloud spending experienced during this period.

The business is trading at a discount to its peers, with a 27% discount on an LTM EBITDA basis and a 17% discount on a NTM FCF basis. This discount reflects the simplicity of the services provided ("commoditized services") relative to peers such as Accenture, who provide greater value-add. This said, we still believe the discount is slightly larger than justifiable due to its good profitability.

Based on these two factors, it is likely Wipro is slightly undervalued but not to a material degree, particularly with risks around Q2/Q3 performance.

Final thoughts

Wipro is a solid investment that provides investors exposure to the development of our ever-digitalizing world. The company has significant scale, deep expertise, and a wide range of clients. We expect a continuation of the last decade, with healthy growth (potentially through AI) and healthy cash flow conversion. Despite its reasonable performance compared to peers, we do not believe the business is priced for upside.

For further details see:

Wipro: Growth In The AI Digital Age