WIT - Wipro: On The Recovery Path

2024-01-14 21:31:39 ET

Summary

- Wipro has been hit hard by IT spending cuts in recent years.

- With a recovery on the horizon, however, the company is now poised to outperform.

- Wipro stock is priced quite reasonably relative to underlying growth and broader Indian indices.

Fundamentally, 2023 was a poor year for Indian IT services. Revenue growth and profitability both trended in the wrong direction, particularly for the large caps. Still, IT services stocks did end the year higher (on both price level and valuations), suggesting that investors are turning optimistic on the outlook. Top-three Indian IT services company Wipro’s ( WIT ) latest quarterly update confirmed as much - the core business showed signs of improvement, and perhaps most importantly, forward-looking bookings growth at its consulting arm Capco hit double-digits %.

To be clear, there are risks here, particularly from new trends like generative AI , which should favor larger peers like Infosys (INFY). Governance is an additional concern, given the constant senior management reshuffling we’ve seen in recent years. But a rising tide floats all boats, and as a full-service IT player with solid client relationships, Wipro is highly levered to a discretionary spending recovery. Valuations are also at a wider discount to the Nifty after last year’s underperformance; hence, the stock isn’t all that pricey here, in my view, particularly in the context of a more accommodative interest rate backdrop ahead.

Still Declining but at a Moderating Pace

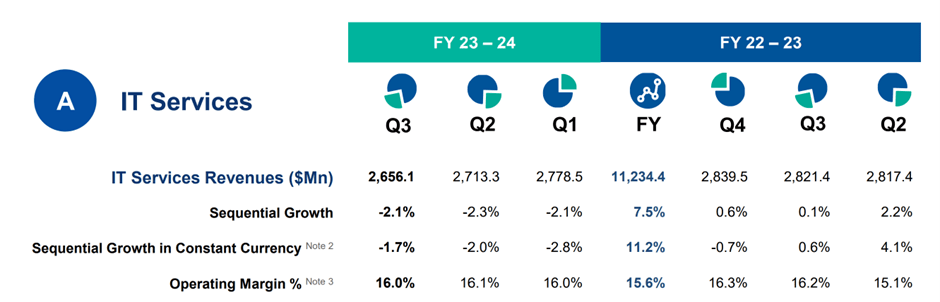

Rate hikes in the US/EU have disproportionately affected the tech sector, and Indian IT services names have felt the impact. Wipro has borne the brunt of the spending pullback, lagging its larger peers on the top line by a wider-than-usual margin in recent months. At first blush, its latest Q3 FY24 result was more of the same – the $2.7bn of revenue generation marked a QoQ decline in constant currency terms. Like prior quarters, the declines (steeper YoY) were broad-based across verticals, with only healthcare showing a meaningful acceleration.

But expectations were also low; relative to management’s prior guidance bar (-3.5% to -1.5%) and consensus estimates, Wipro has outperformed. Similarly, headline deal wins at USD3.8bn were surprisingly up sequentially, led by higher large (i.e., >$30m) deal bookings.

{kind=link}

In the face of an ongoing discretionary tech spending slowdown and seasonal headwinds, Wipro’s 16.0% IT services margin was also impressively resilient – only down 10bps QoQ. Below the operating line, net profit also came in slightly higher QoQ, helped by operational efficiencies (e.g., lower headcount, lower attrition) and corporate streamlining (e.g., exiting lower-margin businesses, focus on higher value contracts), all of which offset headwinds from higher wages.

{kind=link}

Guidance Numbers Reveal Encouraging Green Shoots

Perhaps the best news out of the Wipro results call was management citing visibility into a “certain form of stabilization” and “a pickup in discretionary spend” – even with clients very much in cost-saving mode for now. As things stand, the updated Q4 FY24 guidance range for revenue growth is between -1.5% and +0.5% QoQ (constant currency) – a clear step up from the -3.5% to -1.5% QoQ guidance range for Q3 FY24.

{kind=link}

There was some pushback on the call, but on balance, this update doesn’t seem all that aggressive, in my view. In fact, it might even be conservative in light of the significant Q3 FY24 bookings acceleration at Capco - a leading demand indicator due to its leverage to discretionary spending. While a full-fledged recovery in discretionary spending is likely some way off, the rate of change is key; as one of the few full-service IT services players, Wipro is well positioned to capitalize.

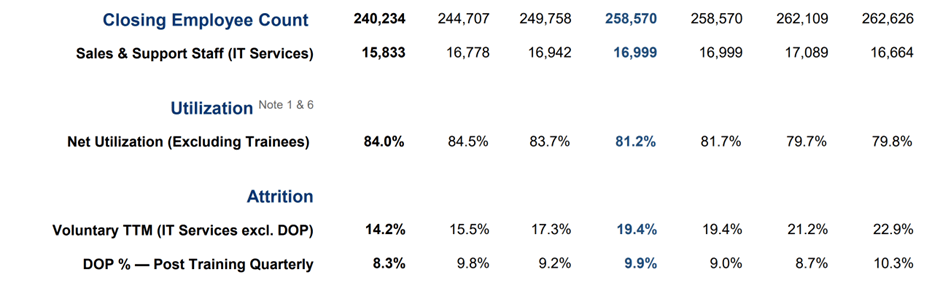

The other forward-looking highlight is that attrition has continued to trend lower – as of Q3, it was ~130bps lower QoQ at 14.2%. New hires are typically margin drags (at least initially), so by holding off on campus hires until the demand environment improves, Wipro should enjoy some near-term margin buffer. Also helping is that the company is almost done navigating a tough Q3/Q4 FY24 period amid wage hikes and operating deleverage (i.e., lower sales spread over a relatively fixed cost base).

Beyond the near term, Wipro still has plenty of levers available as well, including utilization, M&A synergies, and AI-led benefits. So, relative to a low near-term bar (Q4 margin guidance in line with recent quarters), I wouldn’t rule out more positive bottom-line surprises in the coming months.

{kind=link}

Where I’d like to see a more concerted effort at improvement, though, is in senior management retention - particularly in light of the many exits (the latest being chief growth officer Stephanie Trautman in Dec 2023) under CEO Thierry Delaporte’s tenure thus far. Stability here, a persistent issue under prior CEOs as well, would go a long way toward repairing the company’s image in the eyes of the investor community.

On the Recovery Path

Wipro ended the week strongly, coming in near the top end of its prior guidance range for the December quarter. While headline guidance was slightly disappointing vs. consensus expectations, any near-term blips were more than outweighed by emerging signs of a sustained revival in growth – particularly for its consulting business. Valuations might not seem cheap on an absolute basis (>20x fwd P/E), but relative to underlying earnings growth and a re-rated Nifty benchmark, Wipro isn’t all that pricey. And while there are unaddressed risks (e.g., the ongoing shift toward generative AI and key personnel turnover), the prospect of positive near-term earnings revisions could still re-rate the stock from here.

For further details see:

Wipro: On The Recovery Path