WIT - Wipro: Potential Upside Ahead

2024-01-16 04:36:12 ET

Summary

- Wipro's stock rallied by almost 17% after reporting better than consensus Q3 2024 results.

- The management's view of the change in discretionary spending outlook is encouraging.

- WIT has the potential to return 25% over the next few quarters.

Summary

Wipro ( WIT ) reported its Q3 2024 results on Friday (12th Jan 24) and the stock rallied by almost 17%.

While the market was enthused by the better-than-consensus report, we were encouraged by the management's view of the change in discretionary spending outlook. Although Wipro remains cautious with how the next few quarters pan out, we think the stock is now in a territory where it could potentially return 10-25% over the next few quarters.

Company description

Wipro operates in the IT services space, with a global clientele and a delivery base focused in India. It is part of the larger Azim Premji group, an Indian conglomerate spread across consumer goods, precision engineering, and healthcare systems.

Business segments

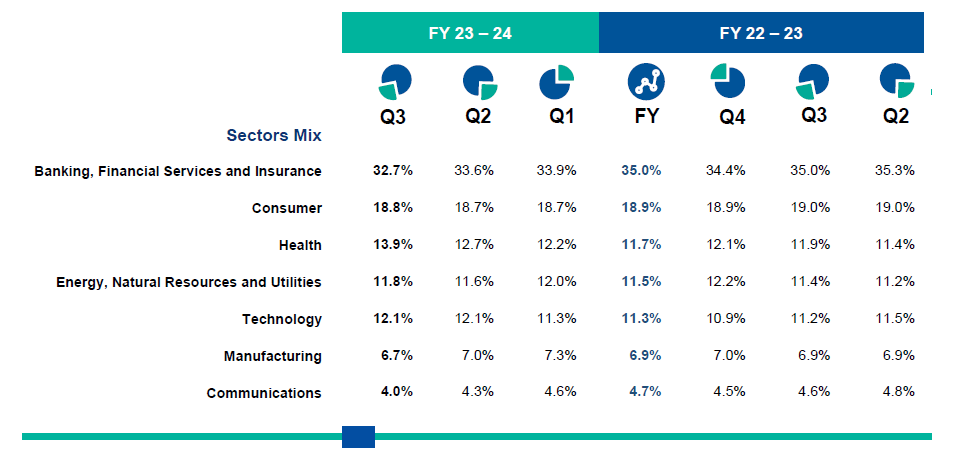

Wipro primarily operates in IT services, with a sectoral focus on financial services, consumer, and healthcare.

{kind=link}

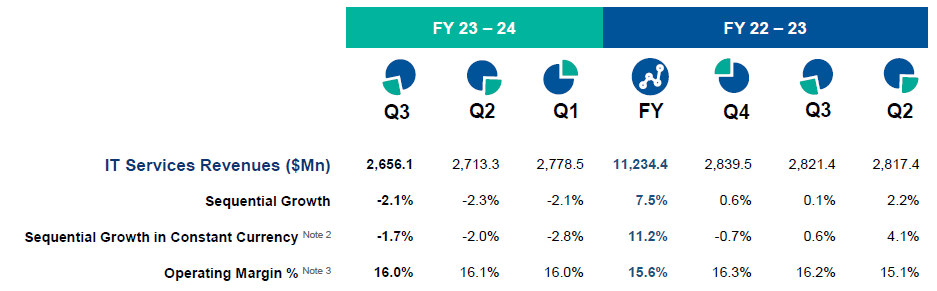

Per the consensus estimates on Seeking Alpha , Wipro is expected to do $10.84 billion in revenue for the year ending March 2024.

{kind=link}

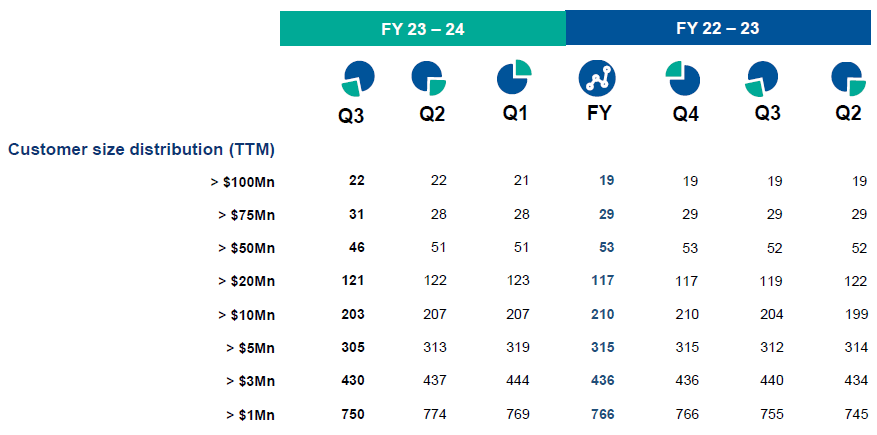

From a customer distribution standpoint, the company has been able to grow its $100 million plus client count, while having seen churn with the smaller customers.

{kind=link}

In response to the market changes, the company has been tightening its belt, with a reduction in employee count and growth in productivity.

Wipro investor relations

Investment thesis

Green shoots on the back of uptick in discretionary spending

- Wipro's results were calibrated with cautious optimism, despite the management finding traction coming back in the discretionary areas. More specifically, the improvement seen was in the consulting business (business side), as opposed to in the technology consulting. We think this is a major change versus the trend of the last many quarters where commodity IT services have been significantly questioned by the rise of LLMs (or large language models).

- Another aspect of the miss in the last many quarters was revenue leakage, again due to the discretionary spending (smaller projects with larger volumes).

- We also like the fact that despite the March quarter usually turning out to be stronger for the company, the management still maintains a bit of conservativism. This will allow for a decent beat, should the initial green shoot continue to mature.

Margin expansion versus investment in business

- Although the management wants to decide whether to invest back the margin strength in business or pass it on to the shareholders based on how the margin improvement pans out, we would have wanted a clearer roadmap to get greater confidence in the Wipro management's ability to look a few quarters out.

- Also, we see the hype around generative artificial intelligence (popularly known as GenAI) also subsiding with the focus moving towards building efficiencies in the existing platform, which to some extent is evident in the management commentary.

So, look at the entire supply chain, today, lower attrition, and headspace for higher utilization, we have enough talent pool available. And for certain specific skills which we require, we'll continue to hire. So, the current environment, we feel that it's -- from a supply, it will now be a constraint.

Source: Wipro Limited Q3 2024 Earnings Call Transcript on Seeking Alpha

- Coupled with the increase in discretionary spending, we think the focus on keeping hiring limited will lead to stronger cash flows over the next couple of quarters.

Valuation

Per Seeking Alpha, the company trades at a P/S of 2.76x versus 2.91x for the sector.

We think the narrative of discretionary spending coming back is a solid one and can lead to differentiated multiples for the companies that can follow through. While the Wipro management remains cautious on the growth trajectory, we think they are lowballing expectations to allow for strong beats.

{kind=link}

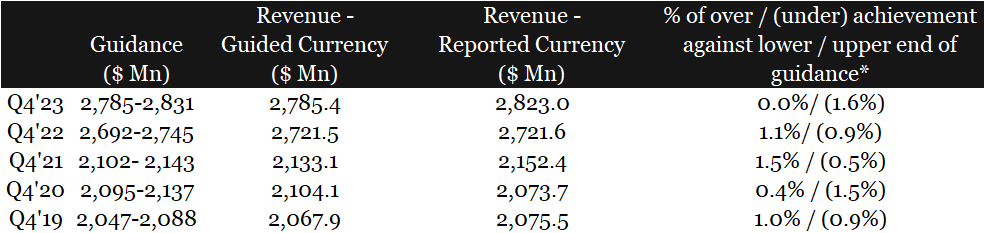

Over the last five years (except the Covid-impacted 2020), Wipro has overachieved more than it has underachieved versus the management guidance. March 2023 was an exceptional year, where the company delivered the least outperformance.

We think Q4 2024 should be in line with the norm and Wipro could outperform. The management has guided to $2,615 million to $2,669 million in revenue. We think the revenue is likely to come in 1% higher than the lower end of the guidance, at $2,641 million. This beat, along with the snowball effect from growing discretionary spending, should lead to a multiple expansion.

While SAAS (or software as a service) companies command a 6-7x revenue multiple, we think the turning tide could lead even commodity services companies such as Wipro to see a multiple expansion to 3.5x levels, representing a potential 25% upside from the current levels.

Risks

The key risk to Wipro's growth thesis is how the macroeconomic setup pans out. The current expectation is for seven rate cuts by the US Fed, which should lead to higher discretionary spending. However, continued weakness in data could lead to a change in the expected Fed behavior.

We however note Wipro's Q3 2024 numbers have come through in an environment of uncertainty around the Fed and general economy. Hence, looking at the margin trajectory and bottoming out of the revenue decline, we view the company positively.

Unless Wipro fails to grow at least one of its revenue and margins, we see limited downside in the stock. Our view stems from the fact that if the company grows revenue, a P/S re-rating is very much on the cards and if Wipro is able to enhance margins from here, it will be moving towards shedding the commodity services tag, which again would lead to higher multiples on EBIT.

Conclusion

While the stock may remain a bit active, owing to the results last Friday, we think Wipro is exhibiting the potential to be the leader of the pack when discretionary spending comes back to the IT universe. Of course, the likes of Accenture, etc. will catch up, but given the much smaller base that Wipro is at, the upside potential remains quite significant.

For further details see:

Wipro: Potential Upside Ahead