WIZEY - Wise: Economies Of Scale-Shared In Cross-Border Payments

2023-11-09 06:48:20 ET

Summary

- Wise aims to reduce transfer costs to zero by bypassing costly banking systems, giving it a competitive edge and creating entry barriers for new competitors.

- Wise's robust infrastructure and economies of scale contribute to its cost efficiency and growth in volumes.

- The company could reach an EBIT of over £1.7 billion by 2033, with a future valuation of £25.5 billion, presenting an attractive investment opportunity.

Executive Overview

Wise (WPLCF), formerly TransferWise, is a fintech innovator challenging the massive £11+ trillion cross-border payment industry by prioritizing affordability, rapid transaction speeds, and clear transparency. Its "Mission Zero" ambition is to reduce international transfer costs to zero, sidestepping the correspondent banking system through a vast network of local accounts and direct real-time payment channels. This approach not only positions Wise as a consumer-centric alternative amid a market rife with obscured charges but also establishes formidable entry barriers for rivals, reinforcing Wise's sustained market lead.

I project that Wise could reach an EBIT of over £1.7 billion by 2033, combining volume-based operating income and net interest earnings. With a normalized earnings yield of around 5% in FY 2024, Wise presents an attractive investment today. Despite potential risks, Wise's sharp focus, robust management with an ownership mindset, and superior payments platform indicate a wide safety margin, hinting at significant prospects for long-term growth.

An Internationally-Focused Money Account

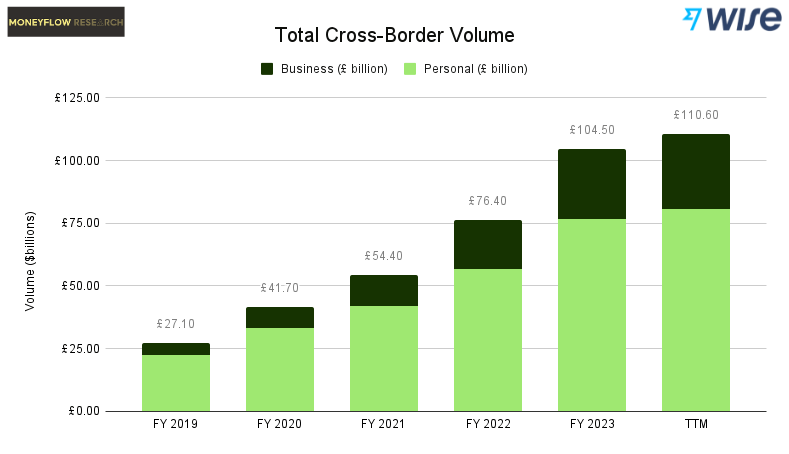

Wise Total Cross-Border Volume (Company Filings)

{kind=link}

Wise offers a multi-currency account, low-fee transfers, and a user-friendly platform for individual and business customers globally. Its core service, Wise Transfer, utilizes the mid-market FX rate for cost-effective and transparent transactions, with active customers growing 3x since 2019. Wise Account provides a global banking solution with 50+ currencies and local bank details in nine countries, while the Wise Debit Card enables international spending with automatic conversion of the currency with the most optimal fee.

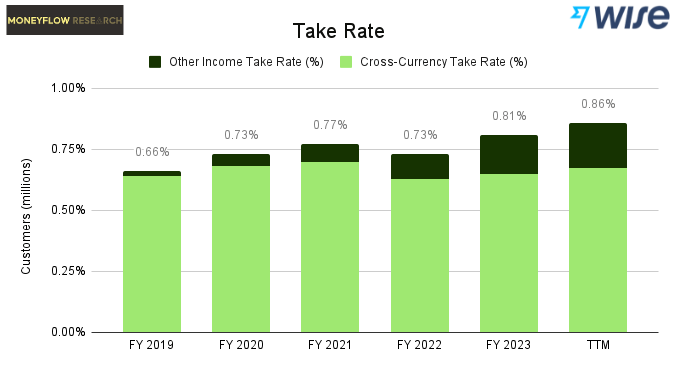

Take Rate Since FY 2019 (Company Filings)

{kind=link}

The company's financials reflect an increased take rate from .66% in FY 2019 to .86%, attributed to 'other income', which is primarily driven by debit card usage. Along with rising interest rates, Wise introduced interest-bearing accounts and index fund options through BlackRock iShares funds, aiming to pass 80% of interest income back to customers, though currently at 25%. Wise Business targets companies with features like batch payments and multi-user access, offering cost-efficient international transactions.

Finally, the Wise Platform expands the company's reach, allowing banks and financial services to integrate Wise's technology via API, enhancing their international payment offerings and retaining customers drawn to better alternatives.

The Cross-Border Payments Landscape

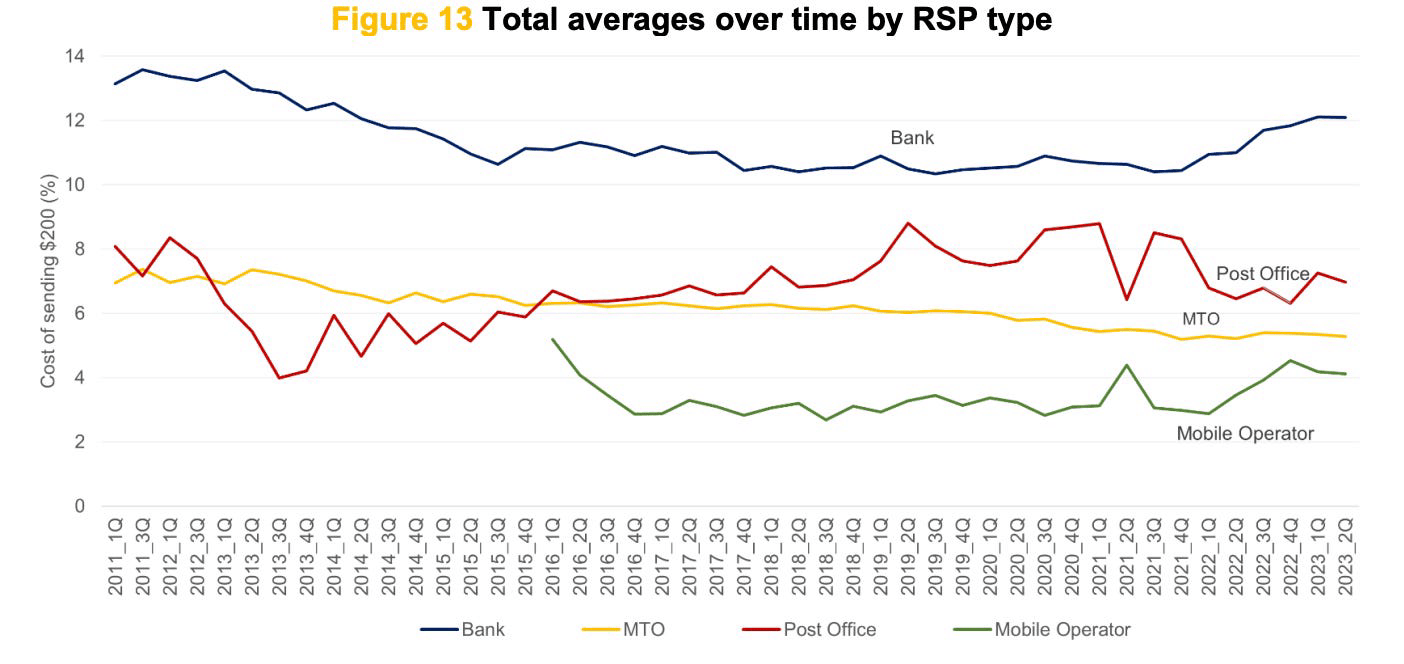

Average Cost Over Time by Remittance Service Provider by Type (The World Bank)

{kind=link}

The cross-border payments industry, known for its intense competition and fragmentation, encompasses banks, fintechs, neo-banks, card networks, MTOs, and government entities, catering to a wide array of segmented end-user needs with considerable overlap. The traditional correspondent banking system, criticized for delays and opaque fees, historically supported international transfers. Traditional MTOs like Western Union (WU) and MoneyGram have provided slow, costly transfers with little innovation due to a lack of competition. However, the 2010s saw a surge in digital-first fintech firms, funded by venture capital, which escalated competition and the costs of differentiation in this multi-trillion-dollar market. These firms face the choice of competing on price and features or continuing to exploit less-informed customers, with many still reliant on the old correspondent banking system.

In the industry, securing market leadership hinges on establishing oneself as the most low-cost producer. This requires establishing a proprietary network that circumvents the inefficiencies of the traditional correspondent banking system, achieving an intrinsic advantage in cost and speed. However, building out such a network is difficult as there are substantial barriers to entry and complexities.

Cross-border payment systems face formidable barriers due to varying regulations and standards across jurisdictions. Licensing, a prerequisite for operation, is a complex and costly endeavor, with ongoing compliance-ranging from AML to KYC and CFT standards-requiring costly legal counsel and adaptable software solutions. The risk of non-compliance is high, with substantial fines as exemplified by MoneyGram and Wise's penalties.

Efforts are being made to standardize data transmission through initiatives like ISO 20022, which facilitates richer payment data, but this does not address the inherent inefficiencies in the correspondent banking system. Moreover, non-bank entities struggle to gain direct access to payment rails, often necessitating partnerships with local financial institutions, which come at a high cost and reduce profitability due to the banks' pricing power. When access is granted, the rewards are phenomenal. For example, Wise's significant efforts to connect directly with the UK's FPS resulted in substantial cost ( 90% cheaper ) and time (96% reduction in payment times) savings.

Wise vs Remitly: Operating Costs as a % of Sales (Public Filings)

Developing a cross-border payment network involves not just heavy fixed costs but also navigating a maze of regulatory and financial complexities, with each incremental country adding more complexity. Costs begin with investments in physical hardware, cloud services, and establishing partnerships with financial institutions. Beyond these initial expenses lie the complexities of managing FX risks, mitigating credit losses, ensuring liquidity, and adhering to strict capital requirements. For instance, Remitly's operational costs, exclusive of marketing, have reached $1.32 billion or 89% of revenue since 2019. When the additional $409 million for marketing and escalating customer acquisition expenses are included, Remitly is unprofitable. These figures underscore the considerable weight of sustained investments in infrastructure and the intensified impact of rising marketing and customer acquisition expenditures. In stark contrast, Wise exemplifies operational efficacy, incurring pre-marketing operational costs at 85.4% of its revenue while maintaining marketing expenses at approximately 5%. It is also noteworthy that Remitly's take rate is 3x that of Wise, which suggests that the efficiency gap would become more pronounced if the business decided to close the gap.

Assessing the Strength of Wise's Moat

In the fiercely competitive landscape of cross-border payments, the key to success lies in offering a distinct edge that elevates a platform as the go-to choice for consumers. Success hinges on four critical aspects: affordability, speed, dependability, and transparency. A platform that dominates in these areas is well-positioned to lead the market.

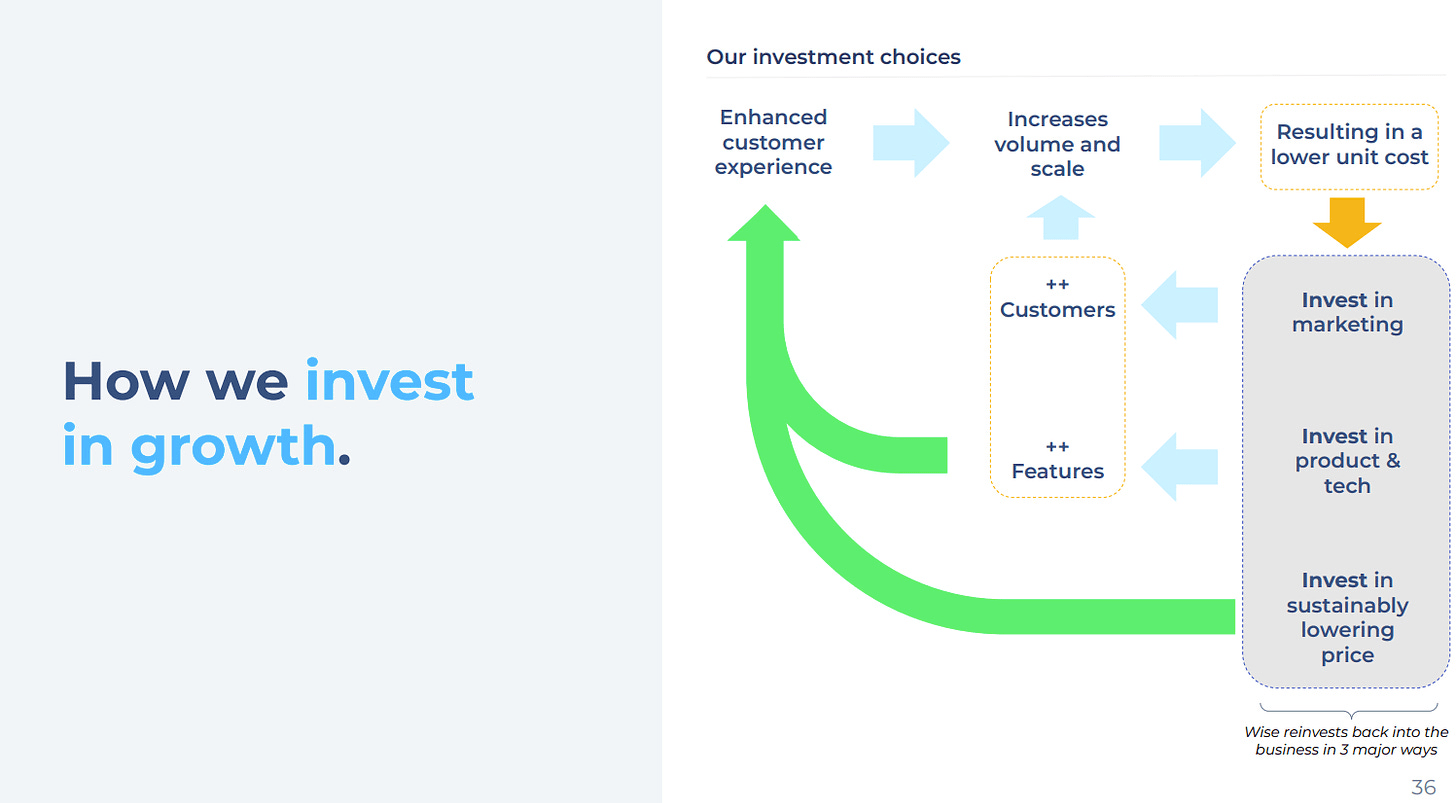

Economies of Scale Shared (Company Slide Deck)

{kind=link}

Wise sets itself apart in this competitive field by developing a specialized infrastructure that rivals find challenging to imitate. This infrastructure is a result of significant investment and creates high entry barriers for new competitors. Additionally, Wise is committed to passing on the savings from improved economies of scale and unit costs directly to its customers, cultivating loyalty and enhancing its value.

These strategies give Wise a significant competitive edge, leading to a virtuous cycle of growth and innovation. Wise's exceptional infrastructure provides a strong footing in the market, and its practice of sharing savings with customers increases its attractiveness. This appeal spurs more growth and innovation, further strengthening its infrastructure and savings for customers, cementing Wise's reputation as a cost-effective leader in the industry.

The Correspondent Banking Problem

The traditional model for international transactions is outdated, often involving several banks to complete a cross-border transfer, making the process expensive, slow, and complex. Without direct banking relationships, numerous intermediaries get involved, increasing costs and making the total fees unclear to the consumer due to the convoluted system. The process is laden with various operational and regulatory costs, including FX and liquidity charges, adding to the inefficiency. Mandatory anti-money laundering (AML), counter-financing of terrorism (CFT), and know-your-customer (KYC) checks by each bank create redundancies and slow down transactions. The lack of standard data formats leads to a 10% transaction failure rate for straight-through processing.

Additionally, inconsistencies in bank and FX market operating times due to different time zones, weekends, and holidays further delay transactions. Banks' batch processing results in accumulated liabilities and additional delays, stretching transaction times up to five business days-unacceptable in a time when people expect instantaneous data and payment transfers like those provided by domestic services such as Venmo or Zelle.

While fintech innovators such as Remitly, Revolut, and XE have greatly improved the front-end user experience, the archaic back-end infrastructure remains mostly unchanged .

Mission Zero: A Big Audacious Goal

There exists an immense opportunity for a cross-border platform that can revolutionize the entire value chain through the creation of a superior network. But this is a long-term endeavor, requiring a dedicated company to gain trust from regulators, secure direct access licenses, and comply with diverse regional laws-not easily achieved, especially under short-term investor pressures.

Since its inception, Wise has been dedicated to its 'Mission Zero'-a pledge to drive customer costs down to zero by minimizing FX markups and fees. This commitment to affordability is deeply embedded in Wise's operational ethos.

Wise's approach has been vindicated over 13 years, offering substantially lower rates than traditional banks, MTOs, and digital competitors, with a 0.67% take rate compared to the average remittance cost of 12% at banks and 4-6% at MTOs. Wise's rates are on average 10x less expensive than competitors, and even more when compared to bank transfers.

Cost per Transaction (Public Filings)

This is not Wise artificially dropping prices and starting price wars to gain market share. Transfer costs for Wise are structurally much lower than the competition. The company's public filings reveal a consistent cost advantage of 5x - 8x compared to others, with an average cost per transaction of $1.03 and an average charge of just over $2, maintaining around a 52% gross margin. To illustrate this advantage, if EuroNet (Ria/XE) slashed prices to zero gross margins, its services would still be 2.5x more expensive than Wise's retail pricing.

The Preeminent Low-Cost Producer

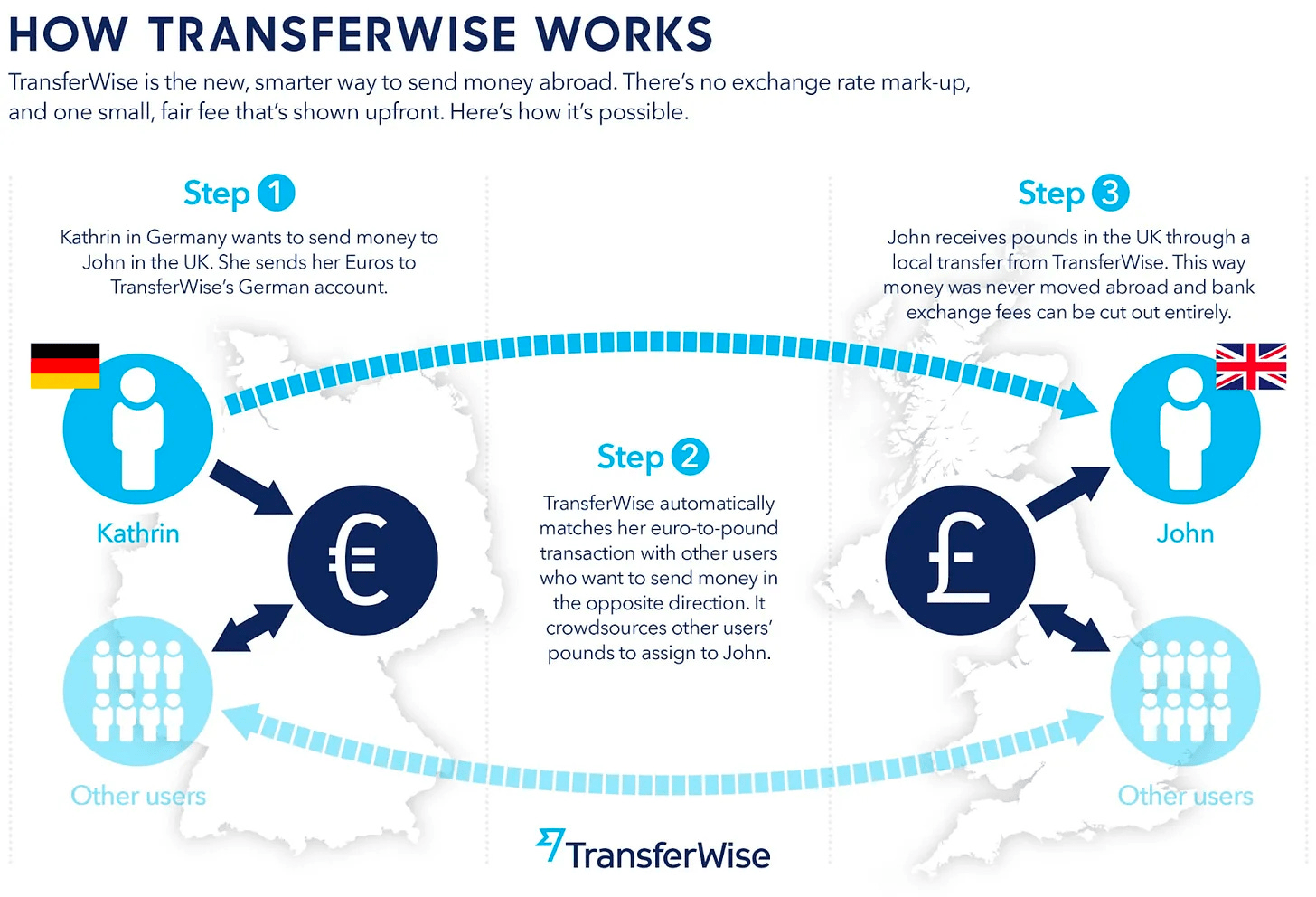

How Wise's Matching System Works (Company Slide Deck)

{kind=link}

Wise's efficient service is based on a peer-to-peer model conceived by co-founders Kristo Käärmann and Taavet Hinrikus out of frustration with high currency exchange rates and fees. By matching transactions domestically, Wise avoids the need to move money across borders, saving on costs. In the case of asymmetric currency flows, Wise established direct connections with domestic payment schemes, reducing its reliance on local banks to rebalance across its network, maintaining its cost efficiency.

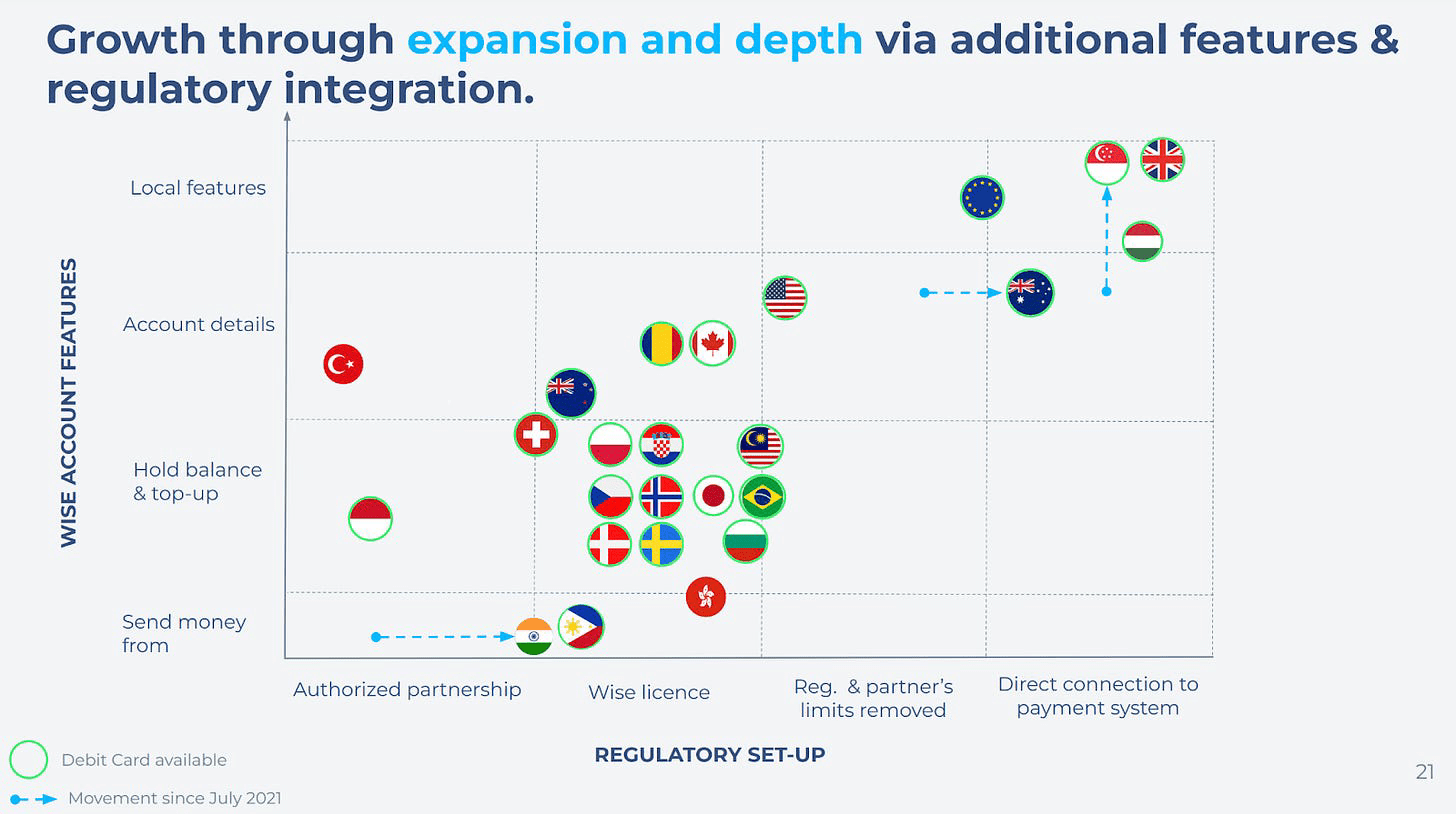

Wise Regulatory Map (Company Slide Deck)

{kind=link}

Gaining direct access is a significant challenge; even Wise, with over a decade in operation, has secured only four such connections. When expanding into new territories, Wise strategically partners with local financial institutions to gain initial market entry. Following this, the company diligently navigates through regulatory landscapes to obtain necessary licenses and alleviate product restrictions, striving to secure direct access to domestic payment schemes.

Wise enhances its competitive position with a bespoke global treasury management system, delivering immediate liquidity visibility and smart fund allocation to optimize investment choices and expedite payments. Leveraging machine learning, Wise forecasts approximately 50% of its foreign exchange transactions, minimizing required working capital and maintaining low operational costs.

The platform's expanding network effect entrenches its market advantage; as Wise's user base grows, the network's value and efficacy amplify. Transfers between Wise users are instantaneous, with transactions being mere ledger entries within Wise's system. This efficiency ensures that even large transactions, typically fragmented due to bank limits, are seamlessly executed on Wise.

Economies of Scale-Shared

Wise differentiates itself by sharing the benefits of economies of scale with its customers, resulting in a virtuous cycle of growth and increasing affordability, as eloquently described by investor Nick Sleep . The more customers Wise attracts, the lower the costs become due to the distribution of fixed costs over a larger revenue base.

Wise's scaling efficiencies manifest in its expanding volumes, user base, and operating profits. Despite its market-leading affordability, the global take rate has modestly decreased by 8% since FY 2017. This conservative figure mask more significant price cuts in over 50 regions, such as a 10% reduction in Brazil and nearly 50% in Mexico. Nonetheless, these benefits are balanced out by challenges such as FX volatility and a volume mix shift to pricier markets.

Efficiency at Wise also translates to speed, with 60% of transfers completed within 20 seconds and 93% of transfers being completed within a day-far outpacing traditional banking speeds.

Customer loyalty also underscores Wise's tangible value, with a volume retention rate exceeding 100% annually since FY 2019 and two-thirds of new customers being referrals. This strong organic growth allows Wise to maintain low marketing expenses, only 4.5% of revenue, compared to higher percentages seen with competitors like Remitly, Payoneer, and OFX.

Risks

Intense Competitive Threats

Wise faces intense competition from both traditional banks modernizing their services and big tech firms entering the payments arena. Banks are revamping their payment systems to provide more competitive FX rates and transparency, supported by central institutions, which could challenge Wise's market position. In the U.S., restrictions like the FedNow network's banking license requirement present entry barriers for non-bank fintech companies. Large tech companies, leveraging their vast user bases and financial prowess, could disrupt Wise's fee-based business by offering free payment services, subsidized by other parts of their business. The payment market's low switching costs also threaten Wise's customer retention, as consumers can easily transfer to cheaper or better offerings with a click of a button. This market dynamic, where Wise is threatened by multi-lateral collaborations, new entrants with substantial resources and distribution power, and the ease of customer migration, renders it difficult for the company to sustain its growth and profitability.

Rebuttal

The cross-border payment market is increasingly competitive, but Wise's specialized, efficient infrastructure gives it a significant edge. Its low-cost, speedy transactions are tough for new entrants, including tech giants, to match, as a large user base doesn't ensure success in service replication, highlighted by the failures of Google+ and Facebook Dating . Tech firms without Wise's partnership default to the slower correspondent banking system. Competitors may undercut on price, but strategies reliant on cross-subsidization or equity capital , such as Atlantic Money's, aren't as sustainable as Wise's model. Revolut's pivot away from FX services to domestic accounts underscores the retail FX market's challenges. Banks, while significant players, often falter in this niche-evidenced by Santander's PagoFX's limited impact-since international transfers make up a small revenue slice, lessening their competitive fervor. Despite market shifts, Wise's focus and cost-efficiency ensure it remains tough to displace, proving its strength against competitors who lack focus, grapple with antiquated systems, or follow unsustainable models.

Threat of Substitution

The Project Nexus Proof-Of-Concept IPS Network (BIS)

{kind=link}

The global financial transaction landscape is rapidly changing, presenting risks to Wise's business from modern payment infrastructure advancements and the rise of digital currencies. International initiatives like IXB and Project Nexus by the Bank for International Settlements are looking to modernize payments to allow instant, efficient transfers, potentially rendering Wise's private network as obsolete. Nexus's proposed standardized framework integrates global instant payment systems, aiming for transactions under 60 seconds, which if widely adopted, could limit Wise's market by setting higher industry benchmarks and reducing the company's access to central bank networks. Additionally, the shift towards digital currencies, with ~90% of central banks exploring CBDCs and the growing popularity of cryptocurrencies, could significantly reduce the need for Wise. If digital currencies become the standard for cross-border transactions, or if the costs and speed of crypto-to-fiat conversions improve, Wise may face decreased demand for its services.

Rebuttal

Global payment networks like Nexus and CBDCs face hurdles that may not readily displace Wise. Universally linking global payment systems is complex and costly, with projects like P27 scaling back due to overambitious goals. Despite Nexus's promise, its prototype stage and not-for-profit model might not match Wise's decade of infrastructure and customer focus. As for digital currencies, CBDCs are criticized for lacking a customer-centric approach and facing technical and management challenges. Jerome Powell of the U.S. Federal Reserve emphasizes the importance of careful consideration for CBDCs over being first to market, highlighting the dollar's reliability and legal framework as essential to a functional payment system. Bitcoin and similar cryptocurrencies, although global and decentralized, suffer from inefficiency, regulatory gaps, and volatility, making them unsuitable for cross-border payments according to the FSB. The high cost of crypto-to-fiat conversion further limits their practicality for transactions, unlike Wise's cost-efficient infrastructure.

Can Wise Achieve Operating Leverage?

Operating Expenses as a % of Sales Since FY 2019 (Public Filings)

Concerns linger over Wise's capacity to attain operating leverage due to growing costs amidst an expanding customer base. From FY 2019 to 2022, Wise's expenses rose steeply with COGS and administrative costs increasing by 73% and 58% respectively, while revenue grew by 51%. The 2023 Annual Report attributes higher expenses to an aggressive hiring policy, particularly in customer service, which is vital for handling 4.5 million new customers and maintaining round-the-clock support with over 1,300 agents. These strategies, intended to boost customer satisfaction, also put pressure on long-term profitability. Operational costs are further strained by the need for human oversight in KYC/AML procedures despite significant automation, and by rising legal and consultancy fees as Wise navigates complex global regulations, maintaining 69 licenses in 45 countries.

Rebuttal

The critiques of Wise's operating leverage due to rising expenses overlook key strategic factors. The company's heavy investments in hiring and customer onboarding are deliberate moves for long-term growth, which in my view represent at least 20% of operating costs that would increase operating income if those growth initiatives were scaled back. Wise's automated onboarding and verification are highly efficient, with most new customers added swiftly through automated processes, handling 20,000 applications and a million documents daily with over 90% automation. Furthermore, Wise's system resolves 80% of customer inquiries in one interaction, and an increasing number of transactions are processed without manual handling, showing potential for further cost reductions.

COGS Components as a % of Sales Since FY 2019 (Public Filings)

An in-depth look at COGS since FY 2019 indicates a stable or slightly improved gross margin, even accounting for high FX losses during periods of c urrency volatility . The company has also seen a decrease in banking and customer-related fees as a percentage of revenue, highlighting enhanced transactional efficiency. Management emphasized a shift to more prudent expansion following a year of significant hiring, aiming for a more sustainable growth rate that aligns with careful financial planning and a commitment to profitability. While the lack of significant operating leverage is a valid concern, it should be evaluated in the broader context of Wise's growth strategy.

Valuation

10-Year Projections for Wise's Economic Drivers (MoneyFlow Research)

Wise's earnings are mainly from volume-based revenue and interest income, which has increased dramatically in recent quarters. Volume-based revenue is calculated by total market volume times Wise's market share times the total take rate, while interest income is derived from the product of cross-border volume, the percentage of customer balances to volume, and net interest yield. Wise is poised to capitalize on the substantial tailwind of overall market growth, estimated at a conservative 3% per year-a figure that is notably more cautious compared to predictions by McKinsey and EY . This expansive market trajectory, alongside Wise's increasing market share, is expected to propel the company to handle £631 billion in transactions, even with its lower fee approach.

For operating margins, a ~20% margin is realistic, supported by Wise's recent performance and industry comps such as Western Union. This could result in about £5 billion in sales and £950 million in operating profits. Customer balances have grown, with an estimated increase to 12% of volumes, translating to £75 billion in balances. With competitive interest rates, Wise is positioned to attract more deposits. In this situation, a net interest yield of only 1% would generate £750 million in net interest income.

Together, these figures suggest a combined EBIT of £1.7 billion. If conditions improve, such as a 2% higher market share and a 1% higher take rate, operating income could reach £3 billion. At a 22% growth rate, a 15x EBIT valuation could mean a £25.50 billion enterprise value, equating to a 14% CAGR, supported by Wise's net cash position of £400 million.

There's no need to speculate on future potential alone. Right now, investors are acquiring a robust asset with a substantial 5% earnings yield and a rapid growth trajectory. Presently, net interest income stands at £158 million, with expectations to climb in tandem with customer balance increases. Revenue, excluding interest, has surged by 35% year-over-year. Projected EBIT growth of 20% for the year suggests a figure of £164 million. This, combined with operating income, indicates a normalized EBIT of £480 million, equating to post-tax earnings of £345 million-a solid investment by any measure.

For further details see:

Wise: Economies Of Scale-Shared In Cross-Border Payments