IBKR - Wise: Higher Interest Rates Proving A Huge Tailwind But Might Not Last

2023-12-04 00:43:46 ET

Summary

- Wise has experienced impressive organic growth and user growth, competing with legacy banks and financial institutions.

- The company is targeting a massive addressable market, with trillions of pounds moved cross currency annually.

- Wise's H1 2024 results show strong revenue growth across regions, with word-of-mouth leading customer acquisition.

We started coverage of Wise ( WPLCF )( WIZEY ) a little over a year ago, and it has since almost tripled its share price. Given that it recently reported its 1H 2024 results, we thought it would be an appropriate time to look into the company and see how it is currently doing.

We believe this is an incredible company with very high word-of-mouth organic growth, impressive user growth, and going after a huge addressable market. Importantly, it competes with mostly legacy banks and financial institutions ( XLF ) which operate with old technology and have lost a lot of goodwill with their customers. For these reasons, we believe the company has a long growth runway.

Seeking Alpha

Big Opportunity

To give an idea of the opportunity Wise is going after, the company estimates that more than two trillion pounds, or more than $2.5 trillion, are moved cross-currency annually by people, and more than nine trillion pounds, or $11.4 trillion, are moved cross currency annually by small and medium businesses. Banks usually charge hefty fees for this service, and it is therefore a massive problem for people and businesses resulting in a very large addressable market.

Importantly, this is just the core offering of Wise, with other add-on services that can bring additional revenue. For example, it is currently offering in certain countries the possibility to invest in the iShares MSCI World ETF ( URTH ) through a partnership with BlackRock ( BLK ). This allows Wise to earn a small percentage of assets under management, and it gives its customers an easy way to invest in a fund that includes some of the most popular companies in the world including Apple ( AAPL ), Microsoft ( MSFT ), and Amazon ( AMZN ). As time goes by, the company will probably find other services it can offer its customers to increase its revenue per customer.

H1 2024 Results

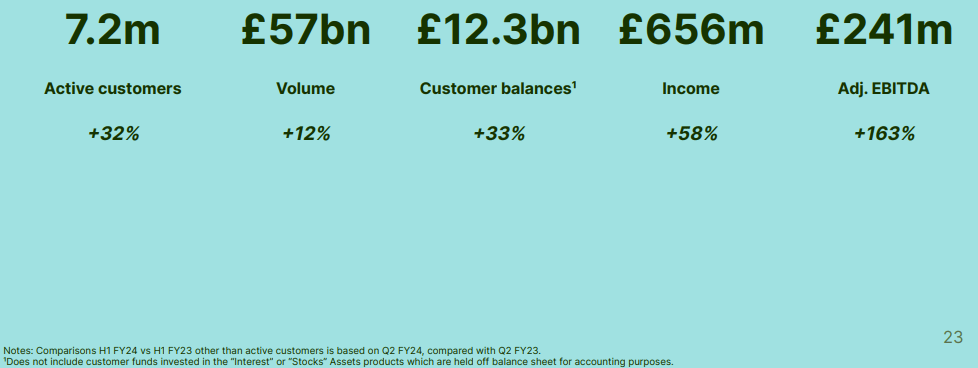

Looking at the first half of FY24 results for Wise, one thing is clear, their revenue is growing across regions. With Europe, its most mature market, growing at a healthy 18%, the UK at 19%, North America at 21%, Asia Pacific at 39%, and the rest of the world at an impressive 53%.

What is most impressive is that this is word-of-mouth-led growth, with more than 67% of new customers joining through word-of-mouth according to the company. The slide below summarizes the key indicators reported by the company for H1 FY24.

{kind=link}

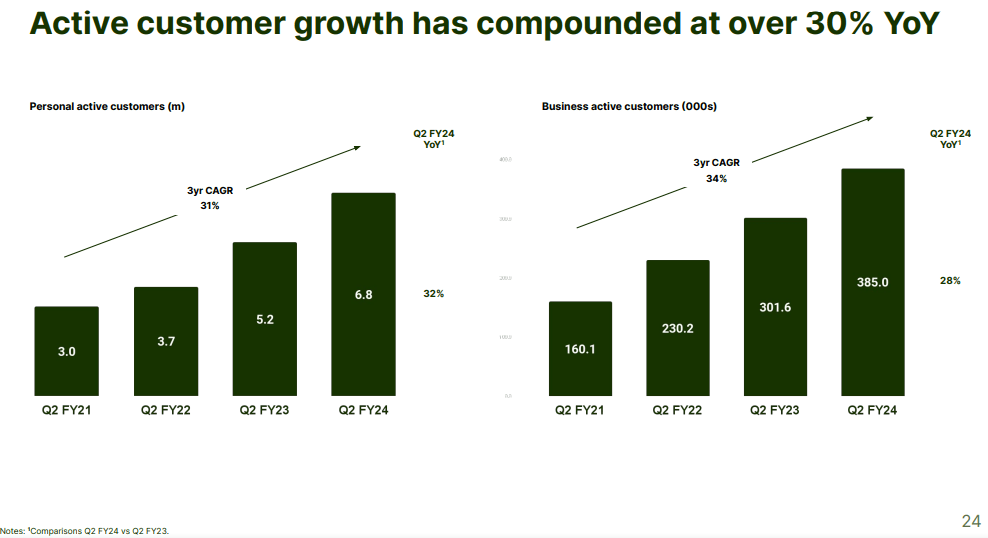

Importantly, this is not a sudden growth spike, the company has been adding customers in a very consistent manner for a long time. Its three-year active customer CAGR is around 30%, which is an incredible rate of growth for a financial company.

{kind=link}

At the same time that it is gaining more customers, its revenue take rate is increasing as a result of account feature adoption. Revenue take rate comprises the cross border take rate plus the take rate on other fees.

Wise Investor Presentation

Financials

Gross profit margin has reached an unbelievable 75%, in large part thanks to higher interest rates. As we'll see, the higher interest rate environment has provided enormous tailwinds for the company, but this will probably be temporary.

Wise Investor Presentation

A significant part of the gross profit increase has made its way to adjusted EBITDA, which has skyrocketed from where it was the year before. While part of the increase comes from customer growth and new account services, profitability received an enormous boost from the interest rate environment.

Wise Investor Presentation

Stock-based Compensation

We like to compare adjusted EBITDA to stock-based compensation, to make sure the company is not giving away more in stock options. We have noticed that in general European companies tend to give away lower amounts for SBC.

In the case of Wise, it appears to be around 5% of revenue, which is still significant, but considerably lower compared to other technology companies where we have seen SBC above 20% of revenue. In any case, Wise remains profitable even after subtracting SBC from adjusted EBITDA.

Understanding Interest Rate Impact

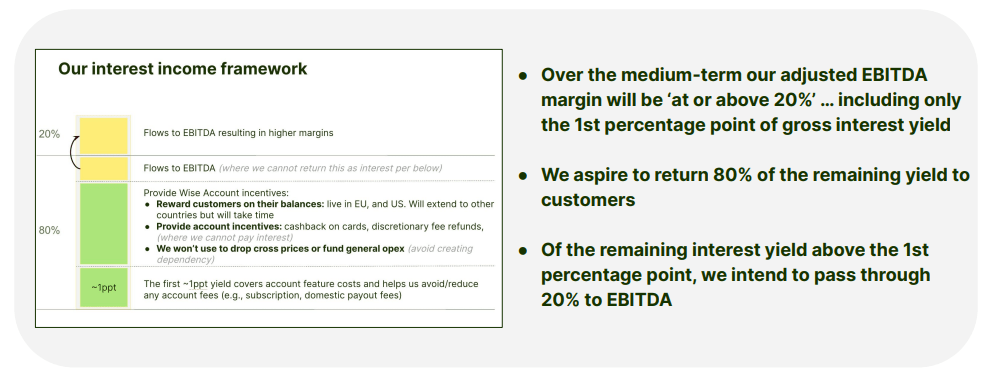

One critical aspect of Wise's business model that investors must understand is its interest income framework. Right now Wise's adj. EBITDA margin is structurally higher due to the current interest rate environment and will likely go down once interest rates normalize. Wise's medium-term adjusted EBITDA margin is to be at or above 20%.

It designed an interest rate framework where the first 1% of gross interest yield from customers' balances goes directly to the company. After that, it aims to return 80% of the remaining interest income to customers in different ways (interest on their balances, cash-back, etc.), and 20% of the interest income excess should flow to EBITDA. This is a key reason why profitability has increased so much this year.

{kind=link}

Looking at the financial notes, interest income on customer balances went up almost 10x from 2022 to 2023. As previously mentioned, a lot of this interest went directly to Wise, as interest rates in Europe are several points above the 1% threshold.

Wise Investor Presentation

The company is likely to enjoy this tailwind for some time, as interest rates remain elevated in its main markets, including the European Union and the United Kingdom.

Still, it is likely a matter of time before elevated interest rates slow down the economy and inflation to the point where central banks have to start easing. Inflation is already showing clear signs of trending down, and if this continues it is just a matter of time before central banks begin to lower rates. This is why we believe investors should not expect Wise's EBITDA margin to remain this high going forward.

Competitive Moat

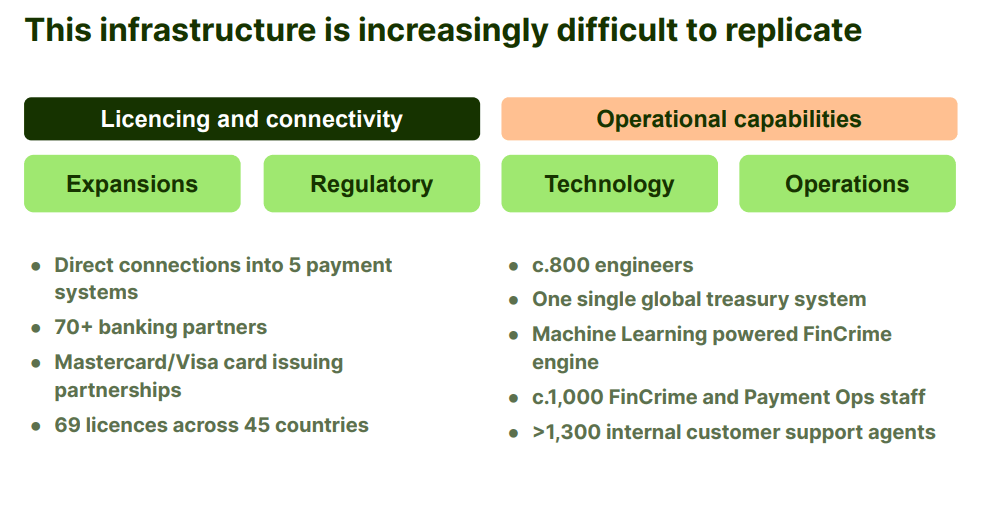

We believe that Wise has been increasing the size of its competitive moat in several ways. First, by offering more services to customers it increases "stickiness" and creates higher switching costs for customers. Second, by improving its technology, licensing, and connectivity, it widens the quality of service gap with competitors and reduces its operating costs at the same time. The company has had to make significant investments in technology, operations, and regulatory efforts. However, these investments have improved its competitive position and it's becoming increasingly difficult for competitors to catch up to where they are, making Wise a low-cost operator.

{kind=link}

Partnerships

At the same time, the company has been busy building partnerships that accelerate its growth and also increase its competitive moat. One example is its partnership with Interactive Brokers ( IBKR ), where its customers can make use of Wise's low-cost currency conversions when purchasing shares in some international exchanges.

{kind=link}

Balance Sheet

Wise has a very strong balance sheet, with most borrowings resulting from drawing money from its revolving credit facility. At the end of September, it had roughly 310 million GBP, or about $400 million in total borrowings, including lease liabilities.

Wise Investor Presentation

This is actually less than the corporate cash the company had at the end of September since it finished with roughly 911 million GBP, or about $1.15 billion. This gives the company plenty of liquidity to continue investing in growth, pursue strategic M&A, etc.

Wise Investor Presentation

Valuation

Both the shares ((WPLCF)) and the ADRs ((WIZEY)) are trading close to $10 as the ADR to native share ratio is 1:1. With about a billion shares outstanding, the market cap is roughly $10 billion. If we annualize the first half of FY24 profit of 140 million GBP, or about $178 million, we get a price/earnings ratio of about 28x.

This does not appear expensive for a company growing its customer base at ~30% annually. With this information, we can approximate the Price/Earnings-to-Growth or PEG ratio to be ~1x, which according to the legendary investor Peter Lynch is usually a very reasonable multiple. For comparison, competitor PayPal ( PYPL ) is currently trading with a PEG ratio of close to 1x too, but with a much lower P/E ratio and significantly lower expected earnings growth. Adyen ( ADYEY ), however, is trading at a higher price/earnings ratio, and with lower expected growth, resulting in a PEG ratio of ~2x.

The problem with Wise is that we believe current profit margins to be unsustainably high due to the high interest rate environment. We believe the company can eventually grow into its valuation and are therefore rating it as a 'Hold', but do not believe this to be a particularly opportune time to purchase shares.

Wise Investor Presentation

Risks

The company faces many risks that range from increased regulation to intensifying competition from both legacy players and other startups. Still, we believe the main risk for investors right now is the demanding valuation. At current prices, investors are already assuming significant growth will continue for several more years. Further complicating things, the interest rate tailwind is not likely to last for very long, as central banks are likely to lower interest rates as inflation comes under control.

Conclusion

Wise delivered impressive results for the first half of its fiscal 2024, continuing to add customers at a rapid pace and showing significant profitability. Shares have performed very well since we last wrote about the company, greatly outperforming the market. Unfortunately, shares no longer look attractive, and profit margins are expected to go down once central banks start lowering rates. While we believe the company has improved its competitive moat, and believe it still has a long growth runway, we do not think this is the best time to buy the shares. For these reasons, we are updating our rating to 'Hold', from 'Buy' previously, and will continue to follow this very interesting company.

For further details see:

Wise: Higher Interest Rates Proving A Huge Tailwind, But Might Not Last