AFMC - Withdrawal Of Pandemic Support Will Drag On The Consumer

2023-03-31 03:29:51 ET

Summary

- A number of COVID-era fiscal support measures are set to end in 2023, which could pressure consumer spending, particularly amongst lower-income individuals.

- The immediate impact of this will likely be muted as consumers still have fairly strong balance sheets.

- Over the next 12 months, a combination of dwindling savings and rising debt could begin to pressure consumers, unless wages significantly outpace inflation.

A number of COVID support programs are ending in 2023, which will further pressure consumers, particularly lower income households. While these support programs are not that large in themselves, consumers are already stretched and less government support could unduly impact discretionary spending. The financial position of most consumers is deteriorating rapidly, but starting from a position of extreme strength in 2021. It will therefore likely take time for excess savings to fall and debt levels to rise before consumer weakness really becomes apparent.

SNAP

SNAP is a food assistance program for low-income individuals in the US. SNAP benefits were expanded during COVID, but this ended in February 2023. Approximately 42 million people are enrolled in SNAP and the reduction in benefits is expected to decrease the average receipt by 90 USD per month. Food price inflation has been a significant issue over the past 2 years, meaning the reduction in SNAP benefits could significantly pressure the budgets of some lower income households.

Tax Refunds

Tax refunds in 2023 are expected to be lower than 2022 for a number of reasons, and this could surprise many individuals who are expecting a larger return. There are several reasons for this, including (2):

- End of stimulus checks

- End of enhanced child credit

- End of tax break for charitable deductions

The impact of these measures is likely to vary significantly across individuals, but for some the changes will be important. For example, many families with two children under the age of 6 will receive 3,200 USD less worth of tax credits.

As of March 17th, the average amount refunded in 2023 according to the IRS was 2,933 USD , around an 11% drop from the same time in 2022.

Medicaid

The Federal health emergency is set to end on May 11th, which will result in a number of health related support measures being withdrawn. Many individuals will now have to start paying for COVID-19 testing and treatment. Hospitals will also see an end to the 20% increase in Medicare's payment rate for treating COVID-19 patients. The most important COVID support measure may have been the fact that states have been barred from kicking people off Medicaid for the past 3 years. As a result, Medicaid enrollment increased to 90 million people. It is expected that around 15 million people could be dropped from Medicaid when the continuous enrollment requirements end.

Student Loan Repayments

Federal student loan repayments have also been suspended for the past three years, but are expected to resume soon. The timing on this is somewhat uncertain as it depends on the Supreme Court issuing a decision on the President's debt-forgiveness plan, but could be around June-August. The average undergraduate owes roughly 234 USD per month in federal student loan payments and there are 43.5 million Americans with student loans. In general, these should be higher income individuals and hence the impact of student loan repayments on consumer spending may be somewhat muted.

Consumer Strength

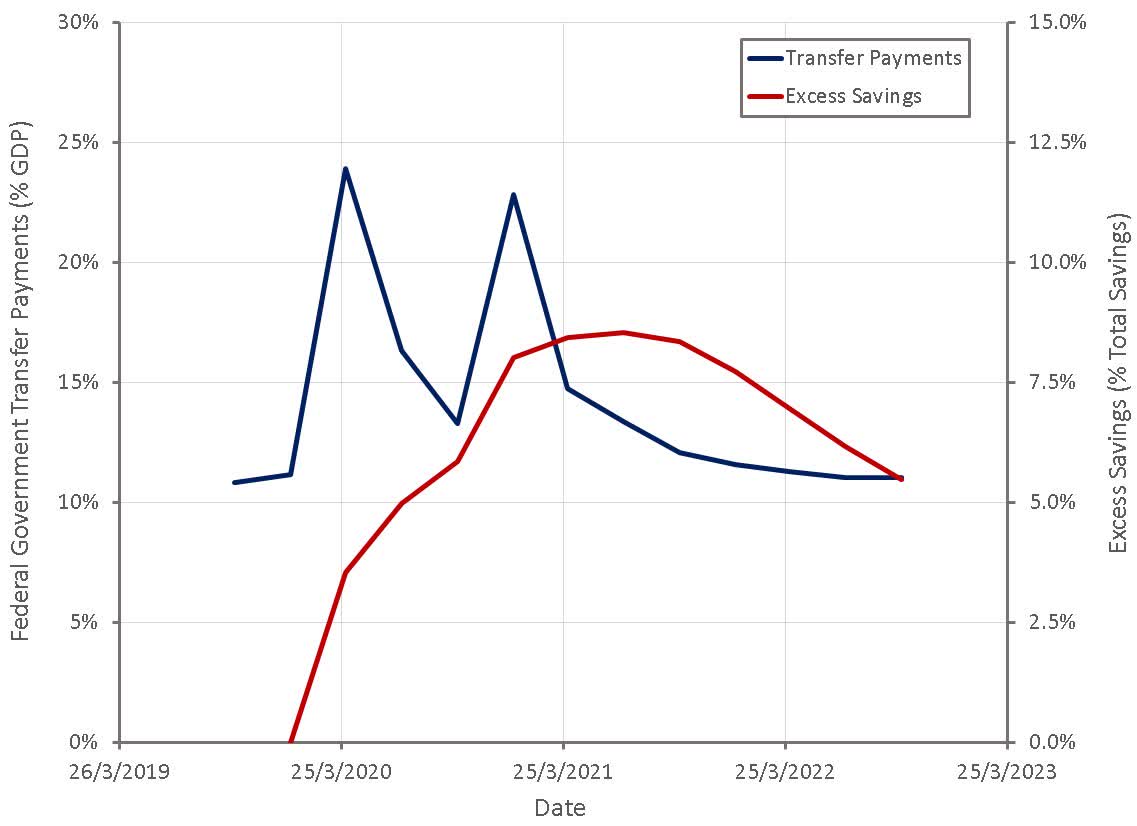

The reduction in government support comes at a time when the average consumer's balance sheet is rapidly deteriorating, albeit from a position of extreme strength. Government transfer payments were largely responsible for excess savings accumulated during COVID, and as these payments have normalized, excess savings have been drawn down.

Figure 1: Excess Savings and Government Transfer Payments (source: Created by author using data from The Federal Reserve)

{kind=link}

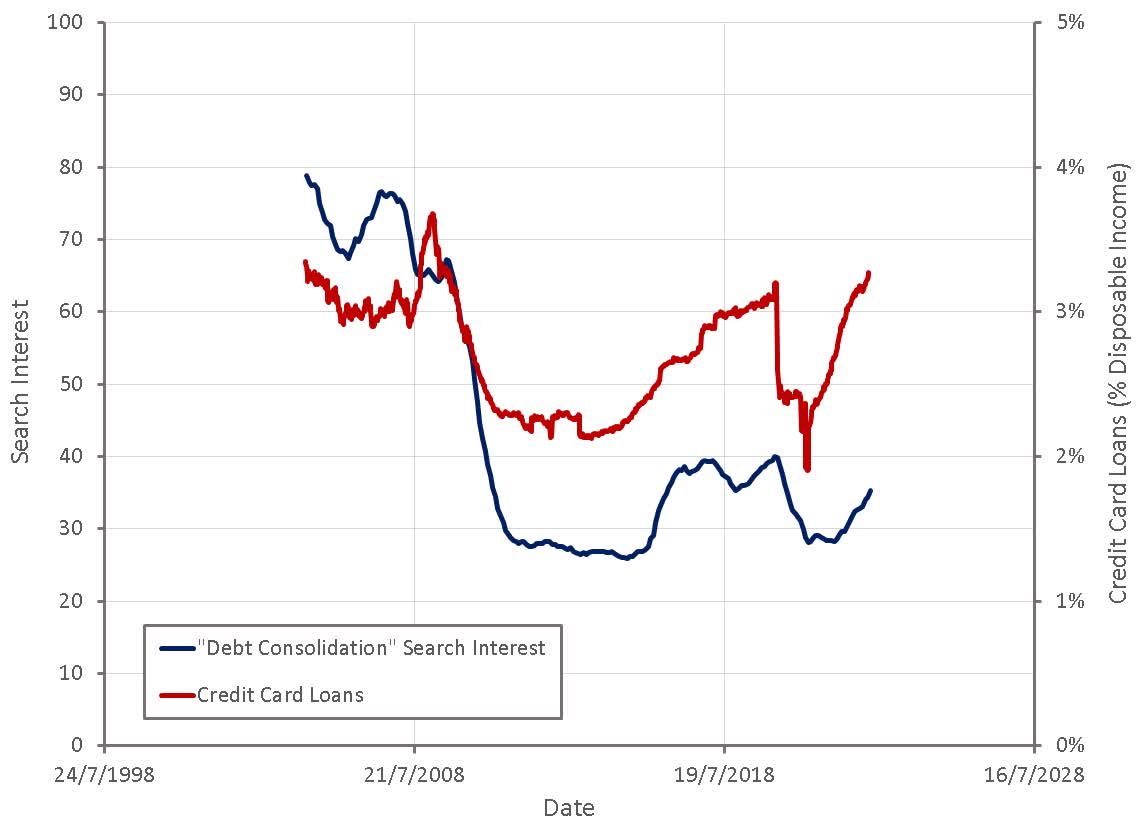

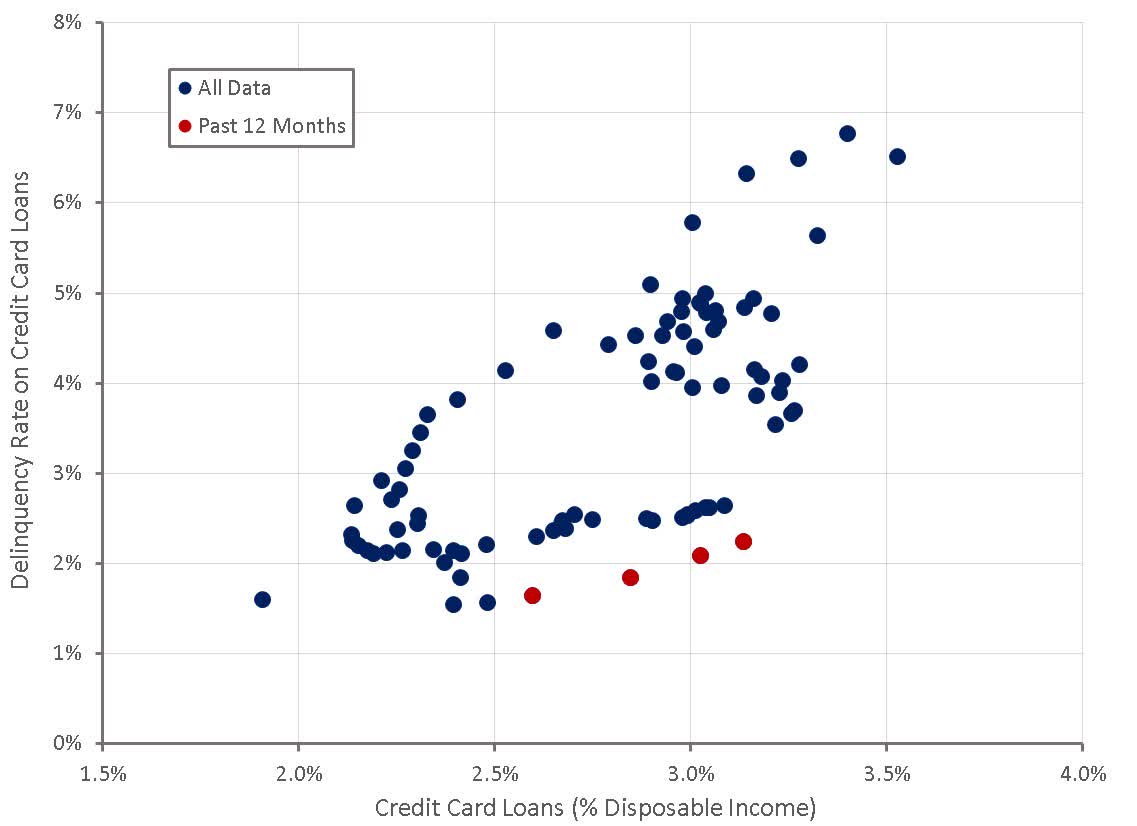

Consumer debt levels are rising to support spending, and this situation will likely continue unless wage increases begin to outpace inflation and/or consumer spending drops. This isn't causing widespread problems yet, and may not do so for some time, but it does not appear to be a sustainable situation. That is not to say that there aren't already problems though. For example, approximately 16.5% of US households owe an average of 791 USD on utility bills.

Figure 2: Consumer Loans: Credit Cards and Other Revolving Plans (source: Created by author using data from Google Trends and The Federal Reserve) Figure 3: Credit Card Loans and Delinquency Rates (source: Created by author using data from The Federal Reserve)

{kind=link}

{kind=link}

Conclusion

Expanded government support measures from the COVID era are now being withdrawn, and are likely to hit lower-income individuals particularly hard. This is important as these individuals have a high marginal propensity to consume, meaning a direct reduction in discretionary spending should be expected. While the amounts involved may not be sufficient to cause problems in themselves, the negative flow through effect on the economy could cause problems in time.

For further details see:

Withdrawal Of Pandemic Support Will Drag On The Consumer